Koninklijke KPN Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

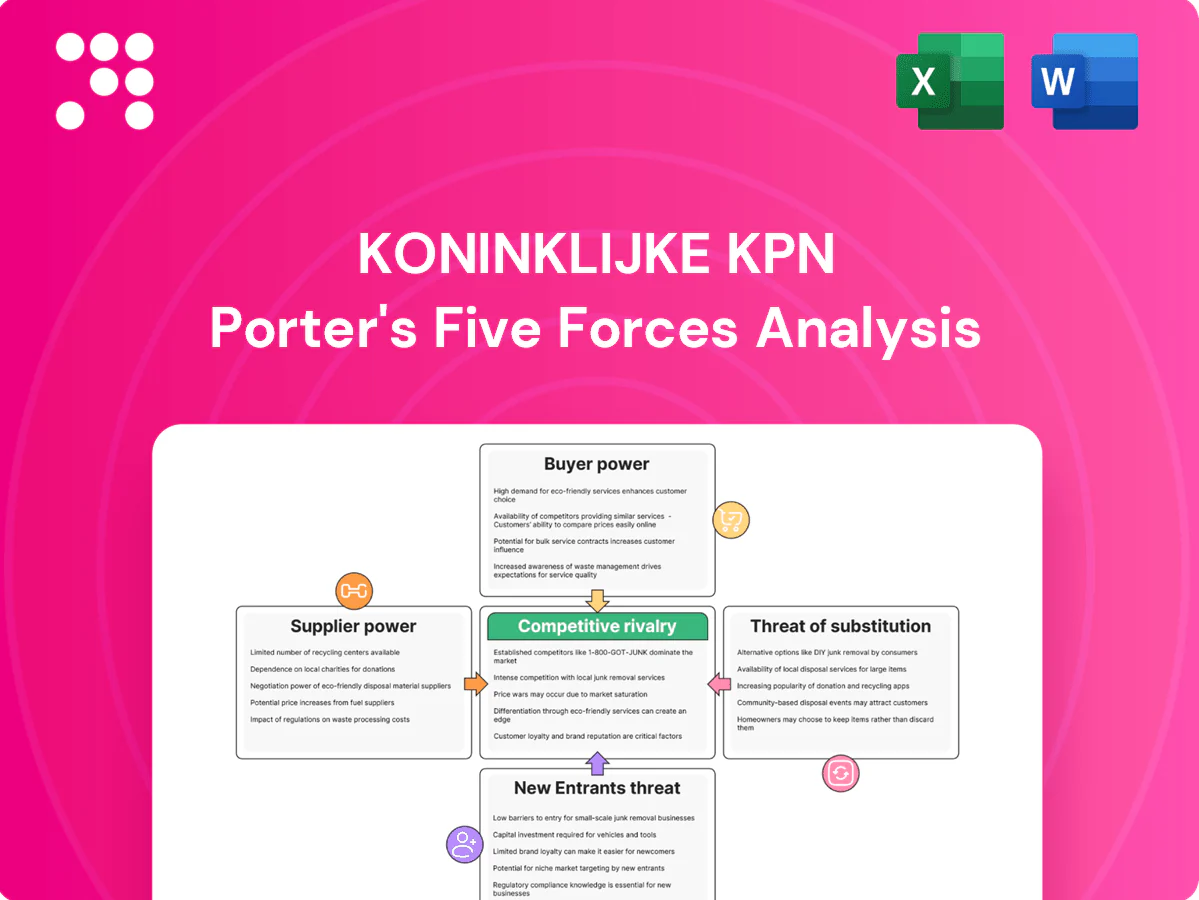

Koninklijke KPN faces intense competitive dynamics across consumer and enterprise segments, with regulatory constraints, infrastructure costs, and evolving substitute services shaping profitability. Supplier and buyer power vary by service line while scale and network assets offer durable advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke KPN’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

KPN depends on a small set of global RAN/core suppliers—primarily Ericsson and Nokia—whose combined share of the global RAN market was roughly 60–65% in 2023–24, making switching costly and time-consuming. Multi-vendor strategies and open RAN standards reduce outright lock-in but raise integration and vendor-interoperability risk. Supplier roadmaps and support terms directly shape KPN’s upgrade cadence and total cost of ownership, and while KPN’s scale improves negotiating leverage, differentiated 5G feature sets preserve supplier bargaining power.

Spectrum and regulation as inputs

State-controlled spectrum licensing in the Netherlands acts as a key supplier to KPN: auction outcomes and coverage mandates materially shape capex — KPN reported roughly €1.3bn capex in 2024 — and create recurring fees. Renewal risk and refarming constraints can delay 5G/IoT rollouts and increase costs. Regulatory obligations and compliance reduce KPN’s operational flexibility compared with ordinary commercial inputs.

Fiber build partners and civil works

Contractors, municipalities and rights-of-way drive KPNs fiber rollout speed and cost; limited trenching capacity and permit timing have created bottlenecks that raised build costs by double digits in parts of 2023–24 and increased project lead times to 6–12 months. Long-term supplier frameworks and indexed contracts have stabilized pricing, but scarcity of skilled civil crews and material tightness keep upward pressure on margins. Co-builds and clustering reduce unit costs, improving ROI on new rolls.

Content and platform dependencies

TV offerings force KPN to secure content rights and platform integrations with dominant media owners; premium sports and must-have channels command high carriage fees and restrictive terms, pressuring margins in the Netherlands (population ~17.7 million in 2024). Aggregation via bundles and OTT partnerships reduces single-supplier exposure but raises churn risk if marquee content lapses; KPN mixes proprietary bundles with OTT deals to limit this.

- Content fees: concentrated with few rights holders

- Churn risk: rises when marquee content removed

- Mitigation: proprietary bundles + OTT partnerships

Energy and data center ecosystems

Network reliability for KPN depends on continuous power and resilient colo; data centers consume about 1% of global electricity, pressuring uptime decisions. Energy price volatility and sustainability goals (KPN: 100% renewable electricity by 2030, net-zero by 2040) shape OPEX and capex choices. Hyperscaler interconnects are semi-commoditized but >60% cloud market concentration (AWS+Azure+GCP) and location/latency needs can limit options; PPAs and efficiency upgrades reduce supplier leverage over time.

- 1. Data centers ≈1% global electricity use

- 2. Hyperscalers >60% market share (2024)

- 3. KPN targets: 100% renewable by 2030, net-zero by 2040

- 4. PPAs/efficiency lower supplier bargaining power

Concentrated RAN, switching costs, spectrum limits and €1.3bn capex

KPN faces concentrated RAN supply (Ericsson+Nokia ~60–65% global share 2023–24), costly switching, and differentiated 5G roadmaps that sustain supplier leverage; state spectrum regimes and €1.3bn 2024 capex constrain timing; fiber build delays (permits 6–12 months) and rising civil costs lift unit costs; hyperscalers >60% cloud share (2024) and premium content fees add recurring supplier pressure.

| Supplier | Metric | Value |

|---|---|---|

| RAN vendors | Market share | 60–65% (2023–24) |

| Capex | KPN 2024 | €1.3bn |

| Fiber | Lead time | 6–12 months |

| Cloud | Hyperscaler share | >60% (2024) |

What is included in the product

Tailored exclusively for Koninklijke KPN, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to the Dutch telecom incumbent. It evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that could erode KPN’s market share and profitability.

Concise one-sheet Porter's Five Forces for Koninklijke KPN—alleviates analysis bottlenecks by instantly highlighting competitive pressures, supplier/regulator risks and areas needing strategic focus for faster decision-making.

Customers Bargaining Power

Price-savvy consumers

Dutch customers face highly transparent pricing, widespread SIM-only plans and frequent promotions, with mobile penetration around 140% and KPN serving about 5.3 million mobile customers in 2024, which raises buyer price sensitivity. Number portability and digital onboarding slash switching costs, boosting bargaining power. Loyalty programs and converged bundles reduce churn but must match market promos. Strong network quality and service differentiation limit pure price-only competition.

Large enterprise negotiations

Corporate and public-sector clients negotiate bespoke SLAs and multi-year deals, using formal tender processes—Dutch public procurement represented about 14% of GDP in 2024—giving large buyers strong leverage on price and terms. Mission-critical connectivity and cybersecurity raise switching costs moderately, while bundled value-added services (managed security, SD-WAN) increasingly shift negotiations from pure price to outcome-based metrics.

SMEs and microbusiness flexibility

SMEs, which make up about 99% of Dutch businesses, routinely compare modular packages from KPN, MVNOs and challengers, privileging price and flexibility. Contract lengths of 12–36 months and equipment financing options shape perceived lock-in. Self-service portals and unified-communications bundles increase stickiness, while aggressive competitor pricing keeps SME margins tight.

Bundling dynamics

Bundling dynamics: KPN’s quad-play and family plans pool services to cut churn, with the 2024 annual report showing service revenue resilience (roughly EUR 5.4bn) and a mobile postpaid base near 5.1m, signaling bundle stickiness. Customers get discounts but accept partial lock-in to keep bundle benefits. Cross-sell depth helps defend ARPU versus stand-alone price pressure. Poor bundle relevance can quickly erode this edge.

- Quad-play pools lines, lowers churn

- Discounts vs partial lock-in

- Cross-sell sustains ARPU

- Irrelevant bundles reverse gains

Quality-of-service expectations

Customers demand robust 5G, fiber speeds and low latency; KPN reported c.98% 5G population coverage and ~3.8m homes passed by fiber in 2024, raising service expectations. In a saturated Dutch market outages or coverage gaps trigger rapid switching, but superior NPS and customer care enable modest price premia. Continuous UX and network upgrades blunt buyer bargaining power.

- 5G coverage: c.98% (2024)

- Fiber homes passed: ~3.8m (2024)

- Outages → fast churn

- NPS-driven price premium

Dutch mobile buyers: price-sensitive, high SIM-only uptake, 5G ~98% and 3.8m fiber reach

Dutch retail buyers are price‑sensitive with ~5.3m KPN mobile subs (2024), high SIM‑only uptake and easy number portability; switching costs low but bundles/UX and network quality (5G c.98%, fiber ~3.8m homes) retain customers. Large corporate/public tenders (public procurement ~14% of GDP) wield strong negotiating leverage; SMEs (99% of firms) push for flexible, low‑cost packages. Bundles sustain ARPU but irrelevance risks churn.

| Metric | 2024 |

|---|---|

| KPN mobile subs | ~5.3m |

| Service revenue | €5.4bn |

| 5G coverage | c.98% |

| Fiber homes passed | ~3.8m |

| Public procurement | ~14% GDP |

Full Version Awaits

Koninklijke KPN Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Koninklijke KPN you'll receive immediately after purchase—no surprises or placeholders. It is the full, professionally formatted document covering rivalry, supplier and buyer power, and threats of entry and substitutes, ready for download and use the moment you buy. Instant access; same file, same content.

Go Beyond the Preview—Access the Full Strategic Report

Koninklijke KPN faces intense competitive dynamics across consumer and enterprise segments, with regulatory constraints, infrastructure costs, and evolving substitute services shaping profitability. Supplier and buyer power vary by service line while scale and network assets offer durable advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke KPN’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

KPN depends on a small set of global RAN/core suppliers—primarily Ericsson and Nokia—whose combined share of the global RAN market was roughly 60–65% in 2023–24, making switching costly and time-consuming. Multi-vendor strategies and open RAN standards reduce outright lock-in but raise integration and vendor-interoperability risk. Supplier roadmaps and support terms directly shape KPN’s upgrade cadence and total cost of ownership, and while KPN’s scale improves negotiating leverage, differentiated 5G feature sets preserve supplier bargaining power.

Spectrum and regulation as inputs

State-controlled spectrum licensing in the Netherlands acts as a key supplier to KPN: auction outcomes and coverage mandates materially shape capex — KPN reported roughly €1.3bn capex in 2024 — and create recurring fees. Renewal risk and refarming constraints can delay 5G/IoT rollouts and increase costs. Regulatory obligations and compliance reduce KPN’s operational flexibility compared with ordinary commercial inputs.

Fiber build partners and civil works

Contractors, municipalities and rights-of-way drive KPNs fiber rollout speed and cost; limited trenching capacity and permit timing have created bottlenecks that raised build costs by double digits in parts of 2023–24 and increased project lead times to 6–12 months. Long-term supplier frameworks and indexed contracts have stabilized pricing, but scarcity of skilled civil crews and material tightness keep upward pressure on margins. Co-builds and clustering reduce unit costs, improving ROI on new rolls.

Content and platform dependencies

TV offerings force KPN to secure content rights and platform integrations with dominant media owners; premium sports and must-have channels command high carriage fees and restrictive terms, pressuring margins in the Netherlands (population ~17.7 million in 2024). Aggregation via bundles and OTT partnerships reduces single-supplier exposure but raises churn risk if marquee content lapses; KPN mixes proprietary bundles with OTT deals to limit this.

- Content fees: concentrated with few rights holders

- Churn risk: rises when marquee content removed

- Mitigation: proprietary bundles + OTT partnerships

Energy and data center ecosystems

Network reliability for KPN depends on continuous power and resilient colo; data centers consume about 1% of global electricity, pressuring uptime decisions. Energy price volatility and sustainability goals (KPN: 100% renewable electricity by 2030, net-zero by 2040) shape OPEX and capex choices. Hyperscaler interconnects are semi-commoditized but >60% cloud market concentration (AWS+Azure+GCP) and location/latency needs can limit options; PPAs and efficiency upgrades reduce supplier leverage over time.

- 1. Data centers ≈1% global electricity use

- 2. Hyperscalers >60% market share (2024)

- 3. KPN targets: 100% renewable by 2030, net-zero by 2040

- 4. PPAs/efficiency lower supplier bargaining power

Concentrated RAN, switching costs, spectrum limits and €1.3bn capex

KPN faces concentrated RAN supply (Ericsson+Nokia ~60–65% global share 2023–24), costly switching, and differentiated 5G roadmaps that sustain supplier leverage; state spectrum regimes and €1.3bn 2024 capex constrain timing; fiber build delays (permits 6–12 months) and rising civil costs lift unit costs; hyperscalers >60% cloud share (2024) and premium content fees add recurring supplier pressure.

| Supplier | Metric | Value |

|---|---|---|

| RAN vendors | Market share | 60–65% (2023–24) |

| Capex | KPN 2024 | €1.3bn |

| Fiber | Lead time | 6–12 months |

| Cloud | Hyperscaler share | >60% (2024) |

What is included in the product

Tailored exclusively for Koninklijke KPN, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to the Dutch telecom incumbent. It evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that could erode KPN’s market share and profitability.

Concise one-sheet Porter's Five Forces for Koninklijke KPN—alleviates analysis bottlenecks by instantly highlighting competitive pressures, supplier/regulator risks and areas needing strategic focus for faster decision-making.

Customers Bargaining Power

Price-savvy consumers

Dutch customers face highly transparent pricing, widespread SIM-only plans and frequent promotions, with mobile penetration around 140% and KPN serving about 5.3 million mobile customers in 2024, which raises buyer price sensitivity. Number portability and digital onboarding slash switching costs, boosting bargaining power. Loyalty programs and converged bundles reduce churn but must match market promos. Strong network quality and service differentiation limit pure price-only competition.

Large enterprise negotiations

Corporate and public-sector clients negotiate bespoke SLAs and multi-year deals, using formal tender processes—Dutch public procurement represented about 14% of GDP in 2024—giving large buyers strong leverage on price and terms. Mission-critical connectivity and cybersecurity raise switching costs moderately, while bundled value-added services (managed security, SD-WAN) increasingly shift negotiations from pure price to outcome-based metrics.

SMEs and microbusiness flexibility

SMEs, which make up about 99% of Dutch businesses, routinely compare modular packages from KPN, MVNOs and challengers, privileging price and flexibility. Contract lengths of 12–36 months and equipment financing options shape perceived lock-in. Self-service portals and unified-communications bundles increase stickiness, while aggressive competitor pricing keeps SME margins tight.

Bundling dynamics

Bundling dynamics: KPN’s quad-play and family plans pool services to cut churn, with the 2024 annual report showing service revenue resilience (roughly EUR 5.4bn) and a mobile postpaid base near 5.1m, signaling bundle stickiness. Customers get discounts but accept partial lock-in to keep bundle benefits. Cross-sell depth helps defend ARPU versus stand-alone price pressure. Poor bundle relevance can quickly erode this edge.

- Quad-play pools lines, lowers churn

- Discounts vs partial lock-in

- Cross-sell sustains ARPU

- Irrelevant bundles reverse gains

Quality-of-service expectations

Customers demand robust 5G, fiber speeds and low latency; KPN reported c.98% 5G population coverage and ~3.8m homes passed by fiber in 2024, raising service expectations. In a saturated Dutch market outages or coverage gaps trigger rapid switching, but superior NPS and customer care enable modest price premia. Continuous UX and network upgrades blunt buyer bargaining power.

- 5G coverage: c.98% (2024)

- Fiber homes passed: ~3.8m (2024)

- Outages → fast churn

- NPS-driven price premium

Dutch mobile buyers: price-sensitive, high SIM-only uptake, 5G ~98% and 3.8m fiber reach

Dutch retail buyers are price‑sensitive with ~5.3m KPN mobile subs (2024), high SIM‑only uptake and easy number portability; switching costs low but bundles/UX and network quality (5G c.98%, fiber ~3.8m homes) retain customers. Large corporate/public tenders (public procurement ~14% of GDP) wield strong negotiating leverage; SMEs (99% of firms) push for flexible, low‑cost packages. Bundles sustain ARPU but irrelevance risks churn.

| Metric | 2024 |

|---|---|

| KPN mobile subs | ~5.3m |

| Service revenue | €5.4bn |

| 5G coverage | c.98% |

| Fiber homes passed | ~3.8m |

| Public procurement | ~14% GDP |

Full Version Awaits

Koninklijke KPN Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Koninklijke KPN you'll receive immediately after purchase—no surprises or placeholders. It is the full, professionally formatted document covering rivalry, supplier and buyer power, and threats of entry and substitutes, ready for download and use the moment you buy. Instant access; same file, same content.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Koninklijke KPN faces intense competitive dynamics across consumer and enterprise segments, with regulatory constraints, infrastructure costs, and evolving substitute services shaping profitability. Supplier and buyer power vary by service line while scale and network assets offer durable advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Koninklijke KPN’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated network vendors

KPN depends on a small set of global RAN/core suppliers—primarily Ericsson and Nokia—whose combined share of the global RAN market was roughly 60–65% in 2023–24, making switching costly and time-consuming. Multi-vendor strategies and open RAN standards reduce outright lock-in but raise integration and vendor-interoperability risk. Supplier roadmaps and support terms directly shape KPN’s upgrade cadence and total cost of ownership, and while KPN’s scale improves negotiating leverage, differentiated 5G feature sets preserve supplier bargaining power.

Spectrum and regulation as inputs

State-controlled spectrum licensing in the Netherlands acts as a key supplier to KPN: auction outcomes and coverage mandates materially shape capex — KPN reported roughly €1.3bn capex in 2024 — and create recurring fees. Renewal risk and refarming constraints can delay 5G/IoT rollouts and increase costs. Regulatory obligations and compliance reduce KPN’s operational flexibility compared with ordinary commercial inputs.

Fiber build partners and civil works

Contractors, municipalities and rights-of-way drive KPNs fiber rollout speed and cost; limited trenching capacity and permit timing have created bottlenecks that raised build costs by double digits in parts of 2023–24 and increased project lead times to 6–12 months. Long-term supplier frameworks and indexed contracts have stabilized pricing, but scarcity of skilled civil crews and material tightness keep upward pressure on margins. Co-builds and clustering reduce unit costs, improving ROI on new rolls.

Content and platform dependencies

TV offerings force KPN to secure content rights and platform integrations with dominant media owners; premium sports and must-have channels command high carriage fees and restrictive terms, pressuring margins in the Netherlands (population ~17.7 million in 2024). Aggregation via bundles and OTT partnerships reduces single-supplier exposure but raises churn risk if marquee content lapses; KPN mixes proprietary bundles with OTT deals to limit this.

- Content fees: concentrated with few rights holders

- Churn risk: rises when marquee content removed

- Mitigation: proprietary bundles + OTT partnerships

Energy and data center ecosystems

Network reliability for KPN depends on continuous power and resilient colo; data centers consume about 1% of global electricity, pressuring uptime decisions. Energy price volatility and sustainability goals (KPN: 100% renewable electricity by 2030, net-zero by 2040) shape OPEX and capex choices. Hyperscaler interconnects are semi-commoditized but >60% cloud market concentration (AWS+Azure+GCP) and location/latency needs can limit options; PPAs and efficiency upgrades reduce supplier leverage over time.

- 1. Data centers ≈1% global electricity use

- 2. Hyperscalers >60% market share (2024)

- 3. KPN targets: 100% renewable by 2030, net-zero by 2040

- 4. PPAs/efficiency lower supplier bargaining power

Concentrated RAN, switching costs, spectrum limits and €1.3bn capex

KPN faces concentrated RAN supply (Ericsson+Nokia ~60–65% global share 2023–24), costly switching, and differentiated 5G roadmaps that sustain supplier leverage; state spectrum regimes and €1.3bn 2024 capex constrain timing; fiber build delays (permits 6–12 months) and rising civil costs lift unit costs; hyperscalers >60% cloud share (2024) and premium content fees add recurring supplier pressure.

| Supplier | Metric | Value |

|---|---|---|

| RAN vendors | Market share | 60–65% (2023–24) |

| Capex | KPN 2024 | €1.3bn |

| Fiber | Lead time | 6–12 months |

| Cloud | Hyperscaler share | >60% (2024) |

What is included in the product

Tailored exclusively for Koninklijke KPN, this Porter's Five Forces analysis uncovers key drivers of competition, customer influence, and market entry risks specific to the Dutch telecom incumbent. It evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces that could erode KPN’s market share and profitability.

Concise one-sheet Porter's Five Forces for Koninklijke KPN—alleviates analysis bottlenecks by instantly highlighting competitive pressures, supplier/regulator risks and areas needing strategic focus for faster decision-making.

Customers Bargaining Power

Price-savvy consumers

Dutch customers face highly transparent pricing, widespread SIM-only plans and frequent promotions, with mobile penetration around 140% and KPN serving about 5.3 million mobile customers in 2024, which raises buyer price sensitivity. Number portability and digital onboarding slash switching costs, boosting bargaining power. Loyalty programs and converged bundles reduce churn but must match market promos. Strong network quality and service differentiation limit pure price-only competition.

Large enterprise negotiations

Corporate and public-sector clients negotiate bespoke SLAs and multi-year deals, using formal tender processes—Dutch public procurement represented about 14% of GDP in 2024—giving large buyers strong leverage on price and terms. Mission-critical connectivity and cybersecurity raise switching costs moderately, while bundled value-added services (managed security, SD-WAN) increasingly shift negotiations from pure price to outcome-based metrics.

SMEs and microbusiness flexibility

SMEs, which make up about 99% of Dutch businesses, routinely compare modular packages from KPN, MVNOs and challengers, privileging price and flexibility. Contract lengths of 12–36 months and equipment financing options shape perceived lock-in. Self-service portals and unified-communications bundles increase stickiness, while aggressive competitor pricing keeps SME margins tight.

Bundling dynamics

Bundling dynamics: KPN’s quad-play and family plans pool services to cut churn, with the 2024 annual report showing service revenue resilience (roughly EUR 5.4bn) and a mobile postpaid base near 5.1m, signaling bundle stickiness. Customers get discounts but accept partial lock-in to keep bundle benefits. Cross-sell depth helps defend ARPU versus stand-alone price pressure. Poor bundle relevance can quickly erode this edge.

- Quad-play pools lines, lowers churn

- Discounts vs partial lock-in

- Cross-sell sustains ARPU

- Irrelevant bundles reverse gains

Quality-of-service expectations

Customers demand robust 5G, fiber speeds and low latency; KPN reported c.98% 5G population coverage and ~3.8m homes passed by fiber in 2024, raising service expectations. In a saturated Dutch market outages or coverage gaps trigger rapid switching, but superior NPS and customer care enable modest price premia. Continuous UX and network upgrades blunt buyer bargaining power.

- 5G coverage: c.98% (2024)

- Fiber homes passed: ~3.8m (2024)

- Outages → fast churn

- NPS-driven price premium

Dutch mobile buyers: price-sensitive, high SIM-only uptake, 5G ~98% and 3.8m fiber reach

Dutch retail buyers are price‑sensitive with ~5.3m KPN mobile subs (2024), high SIM‑only uptake and easy number portability; switching costs low but bundles/UX and network quality (5G c.98%, fiber ~3.8m homes) retain customers. Large corporate/public tenders (public procurement ~14% of GDP) wield strong negotiating leverage; SMEs (99% of firms) push for flexible, low‑cost packages. Bundles sustain ARPU but irrelevance risks churn.

| Metric | 2024 |

|---|---|

| KPN mobile subs | ~5.3m |

| Service revenue | €5.4bn |

| 5G coverage | c.98% |

| Fiber homes passed | ~3.8m |

| Public procurement | ~14% GDP |

Full Version Awaits

Koninklijke KPN Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Koninklijke KPN you'll receive immediately after purchase—no surprises or placeholders. It is the full, professionally formatted document covering rivalry, supplier and buyer power, and threats of entry and substitutes, ready for download and use the moment you buy. Instant access; same file, same content.