Krispy Kreme Porter's Five Forces Analysis

From Overview to Strategy Blueprint

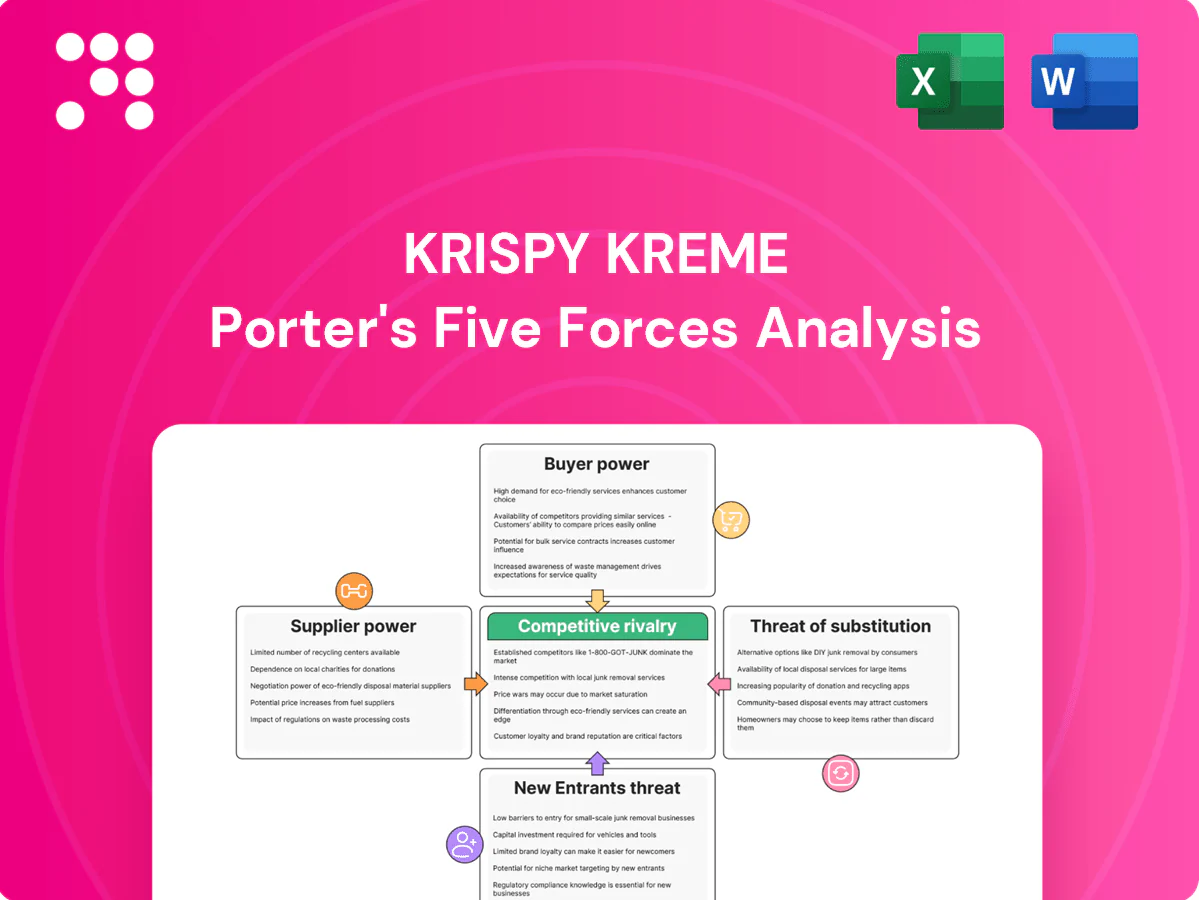

Krispy Kreme faces intense competitive rivalry from coffee chains and fast-casual bakeries, moderate buyer power, low supplier influence, a high threat of substitutes, and moderate barriers to entry driven by brand and scale. This snapshot highlights key pressures shaping the business. Unlock the full Porter's Five Forces Analysis to explore Krispy Kreme’s competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Commodity inputs concentration

Krispy Kreme depends on flour, sugar, oils, dairy and cocoa—commodities covered by many global suppliers but exposed to cyclical volatility; the FAO Food Price Index fell about 16% in 2023 from 2022, illustrating recent swings. Multi-sourcing is feasible but weather, energy and geopolitical shocks can spike costs simultaneously. Hedging smooths but cannot eliminate swings. Supplier power rises in tight commodity cycles.

Specialty ingredients and glaze

Proprietary glaze and mix formulas in 2024 are manufactured by a limited set of approved co-packers, narrowing the supplier base and raising switching costs. Fewer qualified partners lengthen lead times and complicate rapid scale-up for Krispy Kreme, given the brand sensitivity to product consistency. Reliance on these specialty suppliers concentrates negotiating leverage and increases supply-side risk.

Equipment and maintenance vendors

Production lines, fryers and glazing conveyors for Krispy Kreme come from a concentrated set of OEMs and certified service partners, so vendor control over parts and specialized maintenance raises leverage on service contracts and pricing.

Downtime risk—especially for high-throughput shops—gives vendors bargaining power for premium MRO terms; standardization lowers some costs but retrofit requirements and regulatory certifications create practical lock-in.

Packaging and logistics partners

Packaging and cold‑chain distribution for boxes, film and refrigerated freight come from large global packaging firms and major carriers, giving suppliers leverage; freight market cyclicality in 2024 pushed spot surcharges intermittently higher, tightening costs for daily fresh deliveries. KK’s route density improves negotiating leverage, but strict last‑mile freshness windows limit carrier flexibility and sustain supplier power during capacity contractions.

- Large packaging firms dominate supply

- Cold‑chain/carrier cycles raise surcharges

- Route density aids negotiation

- Last‑mile freshness limits options

Scale and global sourcing offsets

Krispy Kreme’s growing global volume and roughly 1,500 retail outlets across 30+ markets provide counter-leverage in supplier negotiations through competitive bidding and diversified sourcing; long-term contracts, commodity hedges, and regional suppliers help mitigate input spikes. The hub-and-spoke procurement model concentrates buying, enforces standard specs, and contains supplier power, though exposure remains cyclical with commodity price swings.

- Scale: ~1,500 outlets, 30+ countries

- Mitigants: long-term contracts, hedges, regional suppliers

- Procurement: hub-and-spoke enables standard specs, reduces supplier leverage

Supplier leverage rises amid input volatility; FAO -16%, ≈1,500 outlets

Supplier power is moderate-to-high: commodity inputs (flour, sugar, oils) saw volatility—FAO Food Price Index down ~16% in 2023 but volatile into 2024—raising cost risk. Specialty co-packers and OEMs for equipment concentrate leverage; packaging and freight surcharges rose intermittently in 2024. Scale (≈1,500 outlets, 30+ markets) and hub-and-spoke procurement mitigate but do not eliminate supplier bargaining power.

| Metric | 2023/2024 |

|---|---|

| FAO Food Price Index change | -16% (2023) |

| Outlets / Markets | ≈1,500 / 30+ |

| Freight trend | Spot surcharges ↑ intermittently (2024) |

What is included in the product

Tailored exclusively for Krispy Kreme, this analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks that shape pricing and profitability. It identifies disruptive substitutes and emerging threats while highlighting dynamics that deter new entrants and protect incumbents.

A concise Krispy Kreme Porter's Five Forces snapshot that clarifies competitive, supplier, buyer, entrant and substitute pressures for faster strategic decisions. Easy to customize and export—ready to drop into pitch decks or boardroom slides for instant stakeholder alignment.

Customers Bargaining Power

Diverse channels, mixed leverage

End consumers are fragmented with low individual price sensitivity, while large retail partners — grocery chains, convenience-store networks and QSR collaborators — exert meaningful leverage over price, promotions and shelf/point-of-sale placement. Krispy Kreme operated roughly 1,600 retail shops worldwide in 2024, and its expanding grocery and wholesale channels concentrate volume with a few large buyers, creating a barbell of low consumer power and high retailer/QSR bargaining power.

Low switching costs for consumers

Low switching costs let buyers pick pastries, muffins or rival doughnuts with minimal friction; Krispy Kreme reported systemwide sales of about $1.6 billion in FY2024, but promotions from competitors and over 1,500 quick-serve bakery outlets nationally shift traffic near points of access, raising price sensitivity outside the Hot Light and keeping pressure on perceived value and novelty.

Brand pull and experiential moat

The hot, fresh Original Glazed and theater-style bakery experience blunt buyer price sensitivity by creating sensory-driven demand; in 2024 Krispy Kreme’s ~1,800 global shops amplified this experiential pull. Strong brand equity drives traffic and willingness to pay, while limited-time offers (e.g., seasonal drops) boost repeat visits and basket size. This consumer pull weakens retailers’ leverage in price negotiations.

Retailer margin and shelf constraints

Grocers and convenience chains run razor-thin net margins (roughly 1–3% in the US in 2024), forcing demands for trade spend, high shelf turns and strict delivery windows; OTIF penalties and chargebacks commonly reach around 2–3% of invoice value, boosting buyer leverage and favoring private label or in‑store bakery alternatives.

- Retailer margins: 1–3% (2024)

- Private label share: ~18–20%

- OTIF/penalties: ~2–3% of invoices

Data and direct relationships

Digital ordering, a loyalty base of over 20 million members and 1,600+ owned/franchised shops in 2024 give Krispy Kreme first-party data and tighter pricing control, enabling targeted DTC offers and reduced reliance on intermediaries. Those insights drive assortment and promotion tweaks that lift price elasticity and progressively weaken buyer bargaining power.

- First-party data: loyalty + digital orders

- DTC reduces intermediary dependence

- Assortment/promotions raise elasticity

- Net effect: diminished buyer power over time

Retail partners keep pricing leverage despite $1.6B system sales, 20M+ loyalty

End consumers are fragmented with low individual price sensitivity, while large grocery, convenience and QSR partners (1,600+ shops in 2024) hold concentrated leverage over price, placement and promotions. Krispy Kreme reported ~$1.6B systemwide sales FY2024 and >20M loyalty members, which strengthen DTC pricing power but retailers' thin margins (1–3%) and OTIF penalties (2–3%) keep buyer leverage high.

| Metric | 2024 |

|---|---|

| Systemwide sales | $1.6B |

| Shops | 1,600+ |

| Loyalty members | >20M |

| Retailer margins | 1–3% |

| OTIF/penalties | 2–3% |

What You See Is What You Get

Krispy Kreme Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Krispy Kreme evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products to clarify strategic pressures and margin levers; it highlights brand strength, franchise dynamics, cost sensitivities, and convenience-led differentiation. The preview you see is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no surprises, ready for download and use.

From Overview to Strategy Blueprint

Krispy Kreme faces intense competitive rivalry from coffee chains and fast-casual bakeries, moderate buyer power, low supplier influence, a high threat of substitutes, and moderate barriers to entry driven by brand and scale. This snapshot highlights key pressures shaping the business. Unlock the full Porter's Five Forces Analysis to explore Krispy Kreme’s competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Commodity inputs concentration

Krispy Kreme depends on flour, sugar, oils, dairy and cocoa—commodities covered by many global suppliers but exposed to cyclical volatility; the FAO Food Price Index fell about 16% in 2023 from 2022, illustrating recent swings. Multi-sourcing is feasible but weather, energy and geopolitical shocks can spike costs simultaneously. Hedging smooths but cannot eliminate swings. Supplier power rises in tight commodity cycles.

Specialty ingredients and glaze

Proprietary glaze and mix formulas in 2024 are manufactured by a limited set of approved co-packers, narrowing the supplier base and raising switching costs. Fewer qualified partners lengthen lead times and complicate rapid scale-up for Krispy Kreme, given the brand sensitivity to product consistency. Reliance on these specialty suppliers concentrates negotiating leverage and increases supply-side risk.

Equipment and maintenance vendors

Production lines, fryers and glazing conveyors for Krispy Kreme come from a concentrated set of OEMs and certified service partners, so vendor control over parts and specialized maintenance raises leverage on service contracts and pricing.

Downtime risk—especially for high-throughput shops—gives vendors bargaining power for premium MRO terms; standardization lowers some costs but retrofit requirements and regulatory certifications create practical lock-in.

Packaging and logistics partners

Packaging and cold‑chain distribution for boxes, film and refrigerated freight come from large global packaging firms and major carriers, giving suppliers leverage; freight market cyclicality in 2024 pushed spot surcharges intermittently higher, tightening costs for daily fresh deliveries. KK’s route density improves negotiating leverage, but strict last‑mile freshness windows limit carrier flexibility and sustain supplier power during capacity contractions.

- Large packaging firms dominate supply

- Cold‑chain/carrier cycles raise surcharges

- Route density aids negotiation

- Last‑mile freshness limits options

Scale and global sourcing offsets

Krispy Kreme’s growing global volume and roughly 1,500 retail outlets across 30+ markets provide counter-leverage in supplier negotiations through competitive bidding and diversified sourcing; long-term contracts, commodity hedges, and regional suppliers help mitigate input spikes. The hub-and-spoke procurement model concentrates buying, enforces standard specs, and contains supplier power, though exposure remains cyclical with commodity price swings.

- Scale: ~1,500 outlets, 30+ countries

- Mitigants: long-term contracts, hedges, regional suppliers

- Procurement: hub-and-spoke enables standard specs, reduces supplier leverage

Supplier leverage rises amid input volatility; FAO -16%, ≈1,500 outlets

Supplier power is moderate-to-high: commodity inputs (flour, sugar, oils) saw volatility—FAO Food Price Index down ~16% in 2023 but volatile into 2024—raising cost risk. Specialty co-packers and OEMs for equipment concentrate leverage; packaging and freight surcharges rose intermittently in 2024. Scale (≈1,500 outlets, 30+ markets) and hub-and-spoke procurement mitigate but do not eliminate supplier bargaining power.

| Metric | 2023/2024 |

|---|---|

| FAO Food Price Index change | -16% (2023) |

| Outlets / Markets | ≈1,500 / 30+ |

| Freight trend | Spot surcharges ↑ intermittently (2024) |

What is included in the product

Tailored exclusively for Krispy Kreme, this analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks that shape pricing and profitability. It identifies disruptive substitutes and emerging threats while highlighting dynamics that deter new entrants and protect incumbents.

A concise Krispy Kreme Porter's Five Forces snapshot that clarifies competitive, supplier, buyer, entrant and substitute pressures for faster strategic decisions. Easy to customize and export—ready to drop into pitch decks or boardroom slides for instant stakeholder alignment.

Customers Bargaining Power

Diverse channels, mixed leverage

End consumers are fragmented with low individual price sensitivity, while large retail partners — grocery chains, convenience-store networks and QSR collaborators — exert meaningful leverage over price, promotions and shelf/point-of-sale placement. Krispy Kreme operated roughly 1,600 retail shops worldwide in 2024, and its expanding grocery and wholesale channels concentrate volume with a few large buyers, creating a barbell of low consumer power and high retailer/QSR bargaining power.

Low switching costs for consumers

Low switching costs let buyers pick pastries, muffins or rival doughnuts with minimal friction; Krispy Kreme reported systemwide sales of about $1.6 billion in FY2024, but promotions from competitors and over 1,500 quick-serve bakery outlets nationally shift traffic near points of access, raising price sensitivity outside the Hot Light and keeping pressure on perceived value and novelty.

Brand pull and experiential moat

The hot, fresh Original Glazed and theater-style bakery experience blunt buyer price sensitivity by creating sensory-driven demand; in 2024 Krispy Kreme’s ~1,800 global shops amplified this experiential pull. Strong brand equity drives traffic and willingness to pay, while limited-time offers (e.g., seasonal drops) boost repeat visits and basket size. This consumer pull weakens retailers’ leverage in price negotiations.

Retailer margin and shelf constraints

Grocers and convenience chains run razor-thin net margins (roughly 1–3% in the US in 2024), forcing demands for trade spend, high shelf turns and strict delivery windows; OTIF penalties and chargebacks commonly reach around 2–3% of invoice value, boosting buyer leverage and favoring private label or in‑store bakery alternatives.

- Retailer margins: 1–3% (2024)

- Private label share: ~18–20%

- OTIF/penalties: ~2–3% of invoices

Data and direct relationships

Digital ordering, a loyalty base of over 20 million members and 1,600+ owned/franchised shops in 2024 give Krispy Kreme first-party data and tighter pricing control, enabling targeted DTC offers and reduced reliance on intermediaries. Those insights drive assortment and promotion tweaks that lift price elasticity and progressively weaken buyer bargaining power.

- First-party data: loyalty + digital orders

- DTC reduces intermediary dependence

- Assortment/promotions raise elasticity

- Net effect: diminished buyer power over time

Retail partners keep pricing leverage despite $1.6B system sales, 20M+ loyalty

End consumers are fragmented with low individual price sensitivity, while large grocery, convenience and QSR partners (1,600+ shops in 2024) hold concentrated leverage over price, placement and promotions. Krispy Kreme reported ~$1.6B systemwide sales FY2024 and >20M loyalty members, which strengthen DTC pricing power but retailers' thin margins (1–3%) and OTIF penalties (2–3%) keep buyer leverage high.

| Metric | 2024 |

|---|---|

| Systemwide sales | $1.6B |

| Shops | 1,600+ |

| Loyalty members | >20M |

| Retailer margins | 1–3% |

| OTIF/penalties | 2–3% |

What You See Is What You Get

Krispy Kreme Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Krispy Kreme evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products to clarify strategic pressures and margin levers; it highlights brand strength, franchise dynamics, cost sensitivities, and convenience-led differentiation. The preview you see is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no surprises, ready for download and use.

Description

From Overview to Strategy Blueprint

Krispy Kreme faces intense competitive rivalry from coffee chains and fast-casual bakeries, moderate buyer power, low supplier influence, a high threat of substitutes, and moderate barriers to entry driven by brand and scale. This snapshot highlights key pressures shaping the business. Unlock the full Porter's Five Forces Analysis to explore Krispy Kreme’s competitive dynamics and strategic advantages in detail.

Suppliers Bargaining Power

Commodity inputs concentration

Krispy Kreme depends on flour, sugar, oils, dairy and cocoa—commodities covered by many global suppliers but exposed to cyclical volatility; the FAO Food Price Index fell about 16% in 2023 from 2022, illustrating recent swings. Multi-sourcing is feasible but weather, energy and geopolitical shocks can spike costs simultaneously. Hedging smooths but cannot eliminate swings. Supplier power rises in tight commodity cycles.

Specialty ingredients and glaze

Proprietary glaze and mix formulas in 2024 are manufactured by a limited set of approved co-packers, narrowing the supplier base and raising switching costs. Fewer qualified partners lengthen lead times and complicate rapid scale-up for Krispy Kreme, given the brand sensitivity to product consistency. Reliance on these specialty suppliers concentrates negotiating leverage and increases supply-side risk.

Equipment and maintenance vendors

Production lines, fryers and glazing conveyors for Krispy Kreme come from a concentrated set of OEMs and certified service partners, so vendor control over parts and specialized maintenance raises leverage on service contracts and pricing.

Downtime risk—especially for high-throughput shops—gives vendors bargaining power for premium MRO terms; standardization lowers some costs but retrofit requirements and regulatory certifications create practical lock-in.

Packaging and logistics partners

Packaging and cold‑chain distribution for boxes, film and refrigerated freight come from large global packaging firms and major carriers, giving suppliers leverage; freight market cyclicality in 2024 pushed spot surcharges intermittently higher, tightening costs for daily fresh deliveries. KK’s route density improves negotiating leverage, but strict last‑mile freshness windows limit carrier flexibility and sustain supplier power during capacity contractions.

- Large packaging firms dominate supply

- Cold‑chain/carrier cycles raise surcharges

- Route density aids negotiation

- Last‑mile freshness limits options

Scale and global sourcing offsets

Krispy Kreme’s growing global volume and roughly 1,500 retail outlets across 30+ markets provide counter-leverage in supplier negotiations through competitive bidding and diversified sourcing; long-term contracts, commodity hedges, and regional suppliers help mitigate input spikes. The hub-and-spoke procurement model concentrates buying, enforces standard specs, and contains supplier power, though exposure remains cyclical with commodity price swings.

- Scale: ~1,500 outlets, 30+ countries

- Mitigants: long-term contracts, hedges, regional suppliers

- Procurement: hub-and-spoke enables standard specs, reduces supplier leverage

Supplier leverage rises amid input volatility; FAO -16%, ≈1,500 outlets

Supplier power is moderate-to-high: commodity inputs (flour, sugar, oils) saw volatility—FAO Food Price Index down ~16% in 2023 but volatile into 2024—raising cost risk. Specialty co-packers and OEMs for equipment concentrate leverage; packaging and freight surcharges rose intermittently in 2024. Scale (≈1,500 outlets, 30+ markets) and hub-and-spoke procurement mitigate but do not eliminate supplier bargaining power.

| Metric | 2023/2024 |

|---|---|

| FAO Food Price Index change | -16% (2023) |

| Outlets / Markets | ≈1,500 / 30+ |

| Freight trend | Spot surcharges ↑ intermittently (2024) |

What is included in the product

Tailored exclusively for Krispy Kreme, this analysis uncovers key drivers of competition, customer influence, supplier power, and market entry risks that shape pricing and profitability. It identifies disruptive substitutes and emerging threats while highlighting dynamics that deter new entrants and protect incumbents.

A concise Krispy Kreme Porter's Five Forces snapshot that clarifies competitive, supplier, buyer, entrant and substitute pressures for faster strategic decisions. Easy to customize and export—ready to drop into pitch decks or boardroom slides for instant stakeholder alignment.

Customers Bargaining Power

Diverse channels, mixed leverage

End consumers are fragmented with low individual price sensitivity, while large retail partners — grocery chains, convenience-store networks and QSR collaborators — exert meaningful leverage over price, promotions and shelf/point-of-sale placement. Krispy Kreme operated roughly 1,600 retail shops worldwide in 2024, and its expanding grocery and wholesale channels concentrate volume with a few large buyers, creating a barbell of low consumer power and high retailer/QSR bargaining power.

Low switching costs for consumers

Low switching costs let buyers pick pastries, muffins or rival doughnuts with minimal friction; Krispy Kreme reported systemwide sales of about $1.6 billion in FY2024, but promotions from competitors and over 1,500 quick-serve bakery outlets nationally shift traffic near points of access, raising price sensitivity outside the Hot Light and keeping pressure on perceived value and novelty.

Brand pull and experiential moat

The hot, fresh Original Glazed and theater-style bakery experience blunt buyer price sensitivity by creating sensory-driven demand; in 2024 Krispy Kreme’s ~1,800 global shops amplified this experiential pull. Strong brand equity drives traffic and willingness to pay, while limited-time offers (e.g., seasonal drops) boost repeat visits and basket size. This consumer pull weakens retailers’ leverage in price negotiations.

Retailer margin and shelf constraints

Grocers and convenience chains run razor-thin net margins (roughly 1–3% in the US in 2024), forcing demands for trade spend, high shelf turns and strict delivery windows; OTIF penalties and chargebacks commonly reach around 2–3% of invoice value, boosting buyer leverage and favoring private label or in‑store bakery alternatives.

- Retailer margins: 1–3% (2024)

- Private label share: ~18–20%

- OTIF/penalties: ~2–3% of invoices

Data and direct relationships

Digital ordering, a loyalty base of over 20 million members and 1,600+ owned/franchised shops in 2024 give Krispy Kreme first-party data and tighter pricing control, enabling targeted DTC offers and reduced reliance on intermediaries. Those insights drive assortment and promotion tweaks that lift price elasticity and progressively weaken buyer bargaining power.

- First-party data: loyalty + digital orders

- DTC reduces intermediary dependence

- Assortment/promotions raise elasticity

- Net effect: diminished buyer power over time

Retail partners keep pricing leverage despite $1.6B system sales, 20M+ loyalty

End consumers are fragmented with low individual price sensitivity, while large grocery, convenience and QSR partners (1,600+ shops in 2024) hold concentrated leverage over price, placement and promotions. Krispy Kreme reported ~$1.6B systemwide sales FY2024 and >20M loyalty members, which strengthen DTC pricing power but retailers' thin margins (1–3%) and OTIF penalties (2–3%) keep buyer leverage high.

| Metric | 2024 |

|---|---|

| Systemwide sales | $1.6B |

| Shops | 1,600+ |

| Loyalty members | >20M |

| Retailer margins | 1–3% |

| OTIF/penalties | 2–3% |

What You See Is What You Get

Krispy Kreme Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Krispy Kreme evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products to clarify strategic pressures and margin levers; it highlights brand strength, franchise dynamics, cost sensitivities, and convenience-led differentiation. The preview you see is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no surprises, ready for download and use.