King & Spalding Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

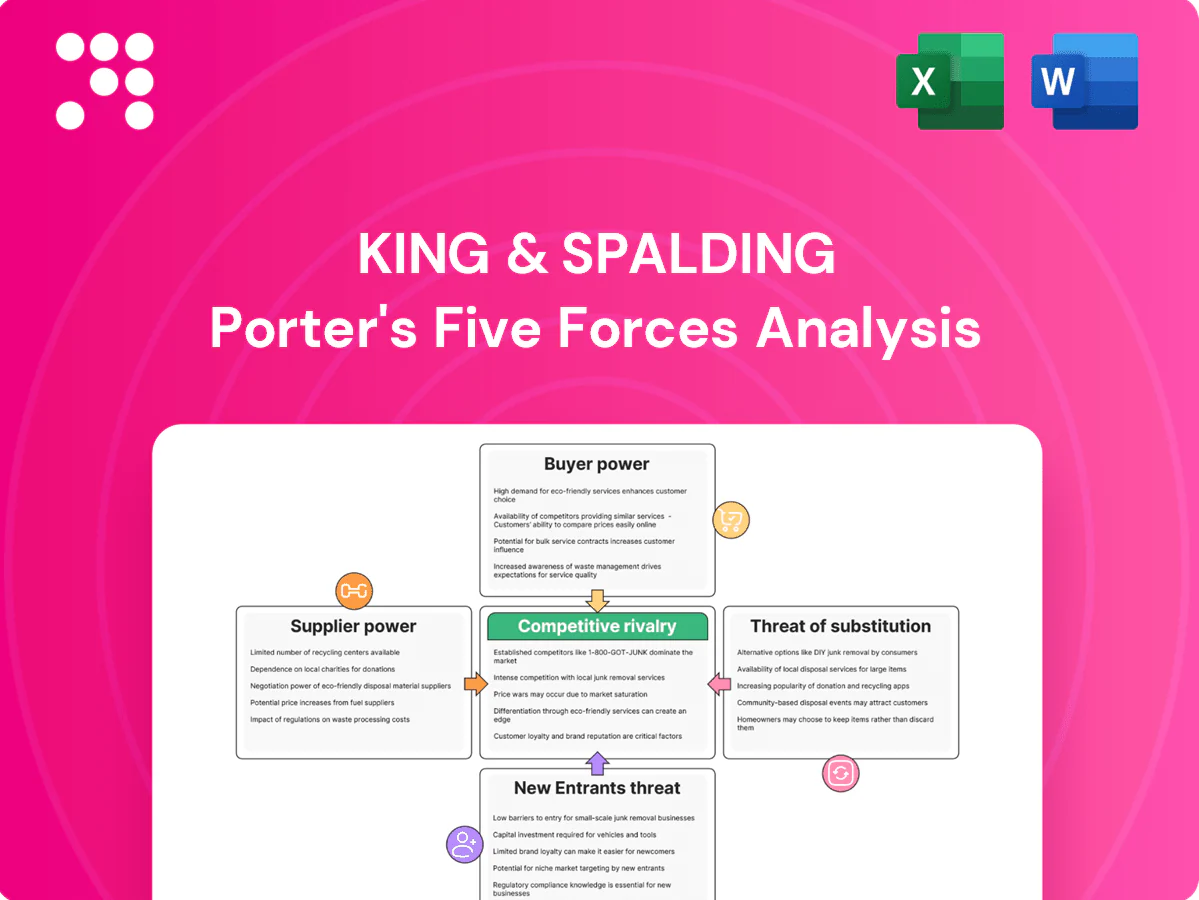

King & Spalding’s Porter’s Five Forces snapshot highlights client bargaining power, intense rivalry among elite firms, threats from boutique entrants and substitutes, and supplier dynamics shaping margins. This brief preview scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance tailored to King & Spalding.

Suppliers Bargaining Power

Scarcity of elite legal talent

Top-tier partners and associates are the primary inputs; scarcity of elite talent gives them strong leverage over pay and work terms, with King & Spalding staffing roughly 1,200 lawyers globally in 2024. Lateral markets intensify bidding for rainmakers and niche experts, driving higher signing bonuses and retention costs that compress margins. Global mobility lets high-demand lawyers arbitrage firms and jurisdictions, raising bargaining power further.

Concentrated legal tech and research vendors

Essential platforms like Westlaw and Lexis held roughly 80% of the legal research market in 2024, and dominant e-discovery and CLM vendors similarly concentrate share, giving suppliers clear pricing power. Integration costs and data migration risks make switching costly for firms. Vendor bundling and multi-year enterprise licenses lock in spend. Built-in cybersecurity and compliance features further heighten dependence.

Expert witnesses and niche consultants

Specialized expert witnesses in energy, life sciences or antitrust are scarce, driving fees that frequently reach six figures per matter and raising supplier power. Top credentials and court-tested track records limit substitution, especially in high-stakes cases. Scheduling conflicts and exclusivity agreements constrain availability, and global disputes typically require multi-jurisdictional teams.

Premium real estate and facilities in key hubs

Flagship offices in global financial centers carry high lease costs with limited comparable alternatives, and long-term leases commonly run 5–15 years, reducing flexibility during demand swings. Landlords in prime districts retain clear pricing power at renewals, while space design for hybrid work can mitigate but not eliminate cost pressure by typically enabling 20–30% footprint reduction.

- High lease concentration in key hubs

- Long-term leases 5–15 years

- Landlord renewal pricing power

- Hybrid design reduces footprint 20–30%

Local counsel and translation providers

Cross-border matters depend on trusted local firms and certified translators, scarce in niche jurisdictions and limiting substitution; EU has 24 official languages (2024), underscoring complexity. Quality and timeliness are critical, and court accreditation or conflict rules further narrow supplier choices. Currency swings and geopolitical tensions since 2022 have raised cost and availability risks.

- Scarcity of niche local counsel

- Certified translation requirements

- Court accreditation/conflicts constrain choices

- FX and geopolitics increase costs

Elite-lawyer scarcity boosts supplier leverage; dominant platforms and long leases raise costs

Scarcity of elite lawyers gives suppliers strong leverage over pay and terms; King & Spalding staffs ~1,200 lawyers globally (2024). Dominant platforms (Westlaw/Lexis ~80% of legal research market in 2024) and e-discovery/CLM vendors create high switching costs and pricing power. Specialized expert witnesses often command six-figure fees; flagship leases run 5–15 years, limiting flexibility while hybrid design can cut footprint 20–30%.

| Metric | 2024 value |

|---|---|

| Lawyers (firm) | ~1,200 |

| Legal research share | ~80% |

| Lease term | 5–15 years |

| Hybrid footprint reduction | 20–30% |

| Expert witness fees | Often six-figure |

What is included in the product

Uncovers key drivers of competition, client bargaining power, supplier influence, threat of new entrants, and substitutes specifically for King & Spalding, identifying disruptive forces and regulatory or market barriers that protect or challenge its market position.

King & Spalding's Porter's Five Forces template delivers a clean, one-sheet summary with customizable pressure levels and a spider chart for instant strategic clarity—perfect for sliding straight into pitch decks or board reports.

Customers Bargaining Power

Corporate procurement and panel consolidation

Corporate procurement centralization drives competitive RFPs that squeeze fees; in 2024 procurement-led RFPs represented a majority of large-enterprise sourcing events and helped buyers secure panel discounts of 10–25% on average. Preferred panels shrink supplier pools and push alternative fee arrangements; rate audits and KPIs (e.g., matter-cycle time, budget variance) intensify margin pressure, while multi-year frameworks commonly trade guaranteed volume for lower margins.

Switching costs moderated by relationship and knowledge

Institutional client knowledge, case history, and strategic alignment create moderate switching costs for King & Spalding, as deep matter-specific expertise and relationship continuity raise the barrier to change. Conflicts, confidentiality waivers, and file transitions can further complicate moves between firms. For bet-the-company matters clients exhibit a markedly higher willingness to pay, while routine transactional or compliance work remains price-sensitive and more easily shifted to lower-cost providers.

Alternative fee arrangements and budgeting discipline

Clients increasingly push AFAs, matter caps and success fees—about 40% of large matters use AFAs by 2024—tying pay to outcomes and compressing hourly margins. Matter-level budgeting plus e-billing and analytics (adoption ~85% in corporate legal departments) reduce tolerance for overruns. Portfolio pricing drives rate compression on commoditized tasks, while risk-sharing structures transfer margin volatility and downside to the firm.

Global reach requirements narrow options

Complex cross-border deals and disputes require integrated international coverage, limiting viable firms and reducing buyer leverage when speed and coordination are critical; clients often prioritize one-stop service over price, especially in sectors with intensive regulation where specialized expertise is scarce in many jurisdictions (global cross-border deal activity remained elevated into 2024).

- Integrated global teams narrow supplier pool

- Speed/coordination > price in urgent disputes

- Sector regulation further restricts choices

Reputation and outcomes dampen price sensitivity

For high-stakes litigation, investigations, and transformative M&A clients prioritize track record and courtroom credibility, reducing price elasticity; in 2024 Am Law 100 partner rates remained above $1,000/hour, reflecting willingness to pay for perceived downside protection and regulator familiarity.

- Track record-driven pricing

- Lower price sensitivity

- Courtroom/regulator premium

- Pockets of premium fees

Procurement centralization cuts fees 10–25%; AFAs ~40%, e-billing ~85% compress rates

Corporate procurement centralization and preferred panels (discounts 10–25%) increased buyer leverage; procurement-led RFPs were the majority of large-enterprise sourcing events in 2024. AFAs reached ~40% of large matters and e-billing/analytics adoption was ~85%, compressing hourly margins. High-stakes cross-border and bet-the-company work retains low price sensitivity; Am Law 100 partner rates remained >$1,000/hour in 2024.

| Metric | 2024 |

|---|---|

| Panel discounts | 10–25% |

| AFAs (large matters) | ~40% |

| E-billing adoption | ~85% |

| AmLaw100 partner rate | >$1,000/hr |

What You See Is What You Get

King & Spalding Porter's Five Forces Analysis

This King & Spalding Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive after purchase. It contains the complete competitive assessment, insights, and supporting details ready for immediate download. No placeholders, no samples—what you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

King & Spalding’s Porter’s Five Forces snapshot highlights client bargaining power, intense rivalry among elite firms, threats from boutique entrants and substitutes, and supplier dynamics shaping margins. This brief preview scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance tailored to King & Spalding.

Suppliers Bargaining Power

Scarcity of elite legal talent

Top-tier partners and associates are the primary inputs; scarcity of elite talent gives them strong leverage over pay and work terms, with King & Spalding staffing roughly 1,200 lawyers globally in 2024. Lateral markets intensify bidding for rainmakers and niche experts, driving higher signing bonuses and retention costs that compress margins. Global mobility lets high-demand lawyers arbitrage firms and jurisdictions, raising bargaining power further.

Concentrated legal tech and research vendors

Essential platforms like Westlaw and Lexis held roughly 80% of the legal research market in 2024, and dominant e-discovery and CLM vendors similarly concentrate share, giving suppliers clear pricing power. Integration costs and data migration risks make switching costly for firms. Vendor bundling and multi-year enterprise licenses lock in spend. Built-in cybersecurity and compliance features further heighten dependence.

Expert witnesses and niche consultants

Specialized expert witnesses in energy, life sciences or antitrust are scarce, driving fees that frequently reach six figures per matter and raising supplier power. Top credentials and court-tested track records limit substitution, especially in high-stakes cases. Scheduling conflicts and exclusivity agreements constrain availability, and global disputes typically require multi-jurisdictional teams.

Premium real estate and facilities in key hubs

Flagship offices in global financial centers carry high lease costs with limited comparable alternatives, and long-term leases commonly run 5–15 years, reducing flexibility during demand swings. Landlords in prime districts retain clear pricing power at renewals, while space design for hybrid work can mitigate but not eliminate cost pressure by typically enabling 20–30% footprint reduction.

- High lease concentration in key hubs

- Long-term leases 5–15 years

- Landlord renewal pricing power

- Hybrid design reduces footprint 20–30%

Local counsel and translation providers

Cross-border matters depend on trusted local firms and certified translators, scarce in niche jurisdictions and limiting substitution; EU has 24 official languages (2024), underscoring complexity. Quality and timeliness are critical, and court accreditation or conflict rules further narrow supplier choices. Currency swings and geopolitical tensions since 2022 have raised cost and availability risks.

- Scarcity of niche local counsel

- Certified translation requirements

- Court accreditation/conflicts constrain choices

- FX and geopolitics increase costs

Elite-lawyer scarcity boosts supplier leverage; dominant platforms and long leases raise costs

Scarcity of elite lawyers gives suppliers strong leverage over pay and terms; King & Spalding staffs ~1,200 lawyers globally (2024). Dominant platforms (Westlaw/Lexis ~80% of legal research market in 2024) and e-discovery/CLM vendors create high switching costs and pricing power. Specialized expert witnesses often command six-figure fees; flagship leases run 5–15 years, limiting flexibility while hybrid design can cut footprint 20–30%.

| Metric | 2024 value |

|---|---|

| Lawyers (firm) | ~1,200 |

| Legal research share | ~80% |

| Lease term | 5–15 years |

| Hybrid footprint reduction | 20–30% |

| Expert witness fees | Often six-figure |

What is included in the product

Uncovers key drivers of competition, client bargaining power, supplier influence, threat of new entrants, and substitutes specifically for King & Spalding, identifying disruptive forces and regulatory or market barriers that protect or challenge its market position.

King & Spalding's Porter's Five Forces template delivers a clean, one-sheet summary with customizable pressure levels and a spider chart for instant strategic clarity—perfect for sliding straight into pitch decks or board reports.

Customers Bargaining Power

Corporate procurement and panel consolidation

Corporate procurement centralization drives competitive RFPs that squeeze fees; in 2024 procurement-led RFPs represented a majority of large-enterprise sourcing events and helped buyers secure panel discounts of 10–25% on average. Preferred panels shrink supplier pools and push alternative fee arrangements; rate audits and KPIs (e.g., matter-cycle time, budget variance) intensify margin pressure, while multi-year frameworks commonly trade guaranteed volume for lower margins.

Switching costs moderated by relationship and knowledge

Institutional client knowledge, case history, and strategic alignment create moderate switching costs for King & Spalding, as deep matter-specific expertise and relationship continuity raise the barrier to change. Conflicts, confidentiality waivers, and file transitions can further complicate moves between firms. For bet-the-company matters clients exhibit a markedly higher willingness to pay, while routine transactional or compliance work remains price-sensitive and more easily shifted to lower-cost providers.

Alternative fee arrangements and budgeting discipline

Clients increasingly push AFAs, matter caps and success fees—about 40% of large matters use AFAs by 2024—tying pay to outcomes and compressing hourly margins. Matter-level budgeting plus e-billing and analytics (adoption ~85% in corporate legal departments) reduce tolerance for overruns. Portfolio pricing drives rate compression on commoditized tasks, while risk-sharing structures transfer margin volatility and downside to the firm.

Global reach requirements narrow options

Complex cross-border deals and disputes require integrated international coverage, limiting viable firms and reducing buyer leverage when speed and coordination are critical; clients often prioritize one-stop service over price, especially in sectors with intensive regulation where specialized expertise is scarce in many jurisdictions (global cross-border deal activity remained elevated into 2024).

- Integrated global teams narrow supplier pool

- Speed/coordination > price in urgent disputes

- Sector regulation further restricts choices

Reputation and outcomes dampen price sensitivity

For high-stakes litigation, investigations, and transformative M&A clients prioritize track record and courtroom credibility, reducing price elasticity; in 2024 Am Law 100 partner rates remained above $1,000/hour, reflecting willingness to pay for perceived downside protection and regulator familiarity.

- Track record-driven pricing

- Lower price sensitivity

- Courtroom/regulator premium

- Pockets of premium fees

Procurement centralization cuts fees 10–25%; AFAs ~40%, e-billing ~85% compress rates

Corporate procurement centralization and preferred panels (discounts 10–25%) increased buyer leverage; procurement-led RFPs were the majority of large-enterprise sourcing events in 2024. AFAs reached ~40% of large matters and e-billing/analytics adoption was ~85%, compressing hourly margins. High-stakes cross-border and bet-the-company work retains low price sensitivity; Am Law 100 partner rates remained >$1,000/hour in 2024.

| Metric | 2024 |

|---|---|

| Panel discounts | 10–25% |

| AFAs (large matters) | ~40% |

| E-billing adoption | ~85% |

| AmLaw100 partner rate | >$1,000/hr |

What You See Is What You Get

King & Spalding Porter's Five Forces Analysis

This King & Spalding Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive after purchase. It contains the complete competitive assessment, insights, and supporting details ready for immediate download. No placeholders, no samples—what you see is what you get.

Description

Go Beyond the Preview—Access the Full Strategic Report

King & Spalding’s Porter’s Five Forces snapshot highlights client bargaining power, intense rivalry among elite firms, threats from boutique entrants and substitutes, and supplier dynamics shaping margins. This brief preview scratches the surface—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance tailored to King & Spalding.

Suppliers Bargaining Power

Scarcity of elite legal talent

Top-tier partners and associates are the primary inputs; scarcity of elite talent gives them strong leverage over pay and work terms, with King & Spalding staffing roughly 1,200 lawyers globally in 2024. Lateral markets intensify bidding for rainmakers and niche experts, driving higher signing bonuses and retention costs that compress margins. Global mobility lets high-demand lawyers arbitrage firms and jurisdictions, raising bargaining power further.

Concentrated legal tech and research vendors

Essential platforms like Westlaw and Lexis held roughly 80% of the legal research market in 2024, and dominant e-discovery and CLM vendors similarly concentrate share, giving suppliers clear pricing power. Integration costs and data migration risks make switching costly for firms. Vendor bundling and multi-year enterprise licenses lock in spend. Built-in cybersecurity and compliance features further heighten dependence.

Expert witnesses and niche consultants

Specialized expert witnesses in energy, life sciences or antitrust are scarce, driving fees that frequently reach six figures per matter and raising supplier power. Top credentials and court-tested track records limit substitution, especially in high-stakes cases. Scheduling conflicts and exclusivity agreements constrain availability, and global disputes typically require multi-jurisdictional teams.

Premium real estate and facilities in key hubs

Flagship offices in global financial centers carry high lease costs with limited comparable alternatives, and long-term leases commonly run 5–15 years, reducing flexibility during demand swings. Landlords in prime districts retain clear pricing power at renewals, while space design for hybrid work can mitigate but not eliminate cost pressure by typically enabling 20–30% footprint reduction.

- High lease concentration in key hubs

- Long-term leases 5–15 years

- Landlord renewal pricing power

- Hybrid design reduces footprint 20–30%

Local counsel and translation providers

Cross-border matters depend on trusted local firms and certified translators, scarce in niche jurisdictions and limiting substitution; EU has 24 official languages (2024), underscoring complexity. Quality and timeliness are critical, and court accreditation or conflict rules further narrow supplier choices. Currency swings and geopolitical tensions since 2022 have raised cost and availability risks.

- Scarcity of niche local counsel

- Certified translation requirements

- Court accreditation/conflicts constrain choices

- FX and geopolitics increase costs

Elite-lawyer scarcity boosts supplier leverage; dominant platforms and long leases raise costs

Scarcity of elite lawyers gives suppliers strong leverage over pay and terms; King & Spalding staffs ~1,200 lawyers globally (2024). Dominant platforms (Westlaw/Lexis ~80% of legal research market in 2024) and e-discovery/CLM vendors create high switching costs and pricing power. Specialized expert witnesses often command six-figure fees; flagship leases run 5–15 years, limiting flexibility while hybrid design can cut footprint 20–30%.

| Metric | 2024 value |

|---|---|

| Lawyers (firm) | ~1,200 |

| Legal research share | ~80% |

| Lease term | 5–15 years |

| Hybrid footprint reduction | 20–30% |

| Expert witness fees | Often six-figure |

What is included in the product

Uncovers key drivers of competition, client bargaining power, supplier influence, threat of new entrants, and substitutes specifically for King & Spalding, identifying disruptive forces and regulatory or market barriers that protect or challenge its market position.

King & Spalding's Porter's Five Forces template delivers a clean, one-sheet summary with customizable pressure levels and a spider chart for instant strategic clarity—perfect for sliding straight into pitch decks or board reports.

Customers Bargaining Power

Corporate procurement and panel consolidation

Corporate procurement centralization drives competitive RFPs that squeeze fees; in 2024 procurement-led RFPs represented a majority of large-enterprise sourcing events and helped buyers secure panel discounts of 10–25% on average. Preferred panels shrink supplier pools and push alternative fee arrangements; rate audits and KPIs (e.g., matter-cycle time, budget variance) intensify margin pressure, while multi-year frameworks commonly trade guaranteed volume for lower margins.

Switching costs moderated by relationship and knowledge

Institutional client knowledge, case history, and strategic alignment create moderate switching costs for King & Spalding, as deep matter-specific expertise and relationship continuity raise the barrier to change. Conflicts, confidentiality waivers, and file transitions can further complicate moves between firms. For bet-the-company matters clients exhibit a markedly higher willingness to pay, while routine transactional or compliance work remains price-sensitive and more easily shifted to lower-cost providers.

Alternative fee arrangements and budgeting discipline

Clients increasingly push AFAs, matter caps and success fees—about 40% of large matters use AFAs by 2024—tying pay to outcomes and compressing hourly margins. Matter-level budgeting plus e-billing and analytics (adoption ~85% in corporate legal departments) reduce tolerance for overruns. Portfolio pricing drives rate compression on commoditized tasks, while risk-sharing structures transfer margin volatility and downside to the firm.

Global reach requirements narrow options

Complex cross-border deals and disputes require integrated international coverage, limiting viable firms and reducing buyer leverage when speed and coordination are critical; clients often prioritize one-stop service over price, especially in sectors with intensive regulation where specialized expertise is scarce in many jurisdictions (global cross-border deal activity remained elevated into 2024).

- Integrated global teams narrow supplier pool

- Speed/coordination > price in urgent disputes

- Sector regulation further restricts choices

Reputation and outcomes dampen price sensitivity

For high-stakes litigation, investigations, and transformative M&A clients prioritize track record and courtroom credibility, reducing price elasticity; in 2024 Am Law 100 partner rates remained above $1,000/hour, reflecting willingness to pay for perceived downside protection and regulator familiarity.

- Track record-driven pricing

- Lower price sensitivity

- Courtroom/regulator premium

- Pockets of premium fees

Procurement centralization cuts fees 10–25%; AFAs ~40%, e-billing ~85% compress rates

Corporate procurement centralization and preferred panels (discounts 10–25%) increased buyer leverage; procurement-led RFPs were the majority of large-enterprise sourcing events in 2024. AFAs reached ~40% of large matters and e-billing/analytics adoption was ~85%, compressing hourly margins. High-stakes cross-border and bet-the-company work retains low price sensitivity; Am Law 100 partner rates remained >$1,000/hour in 2024.

| Metric | 2024 |

|---|---|

| Panel discounts | 10–25% |

| AFAs (large matters) | ~40% |

| E-billing adoption | ~85% |

| AmLaw100 partner rate | >$1,000/hr |

What You See Is What You Get

King & Spalding Porter's Five Forces Analysis

This King & Spalding Porter's Five Forces Analysis preview is the exact, fully formatted document you will receive after purchase. It contains the complete competitive assessment, insights, and supporting details ready for immediate download. No placeholders, no samples—what you see is what you get.