King & Spalding PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock the external forces shaping King & Spalding with our concise PESTLE snapshot—covering regulatory shifts, economic pressures, tech disruption, social trends, and environmental risks. Perfect for investors and strategists seeking a competitive edge. Purchase the full PESTLE for an actionable, downloadable deep dive now.

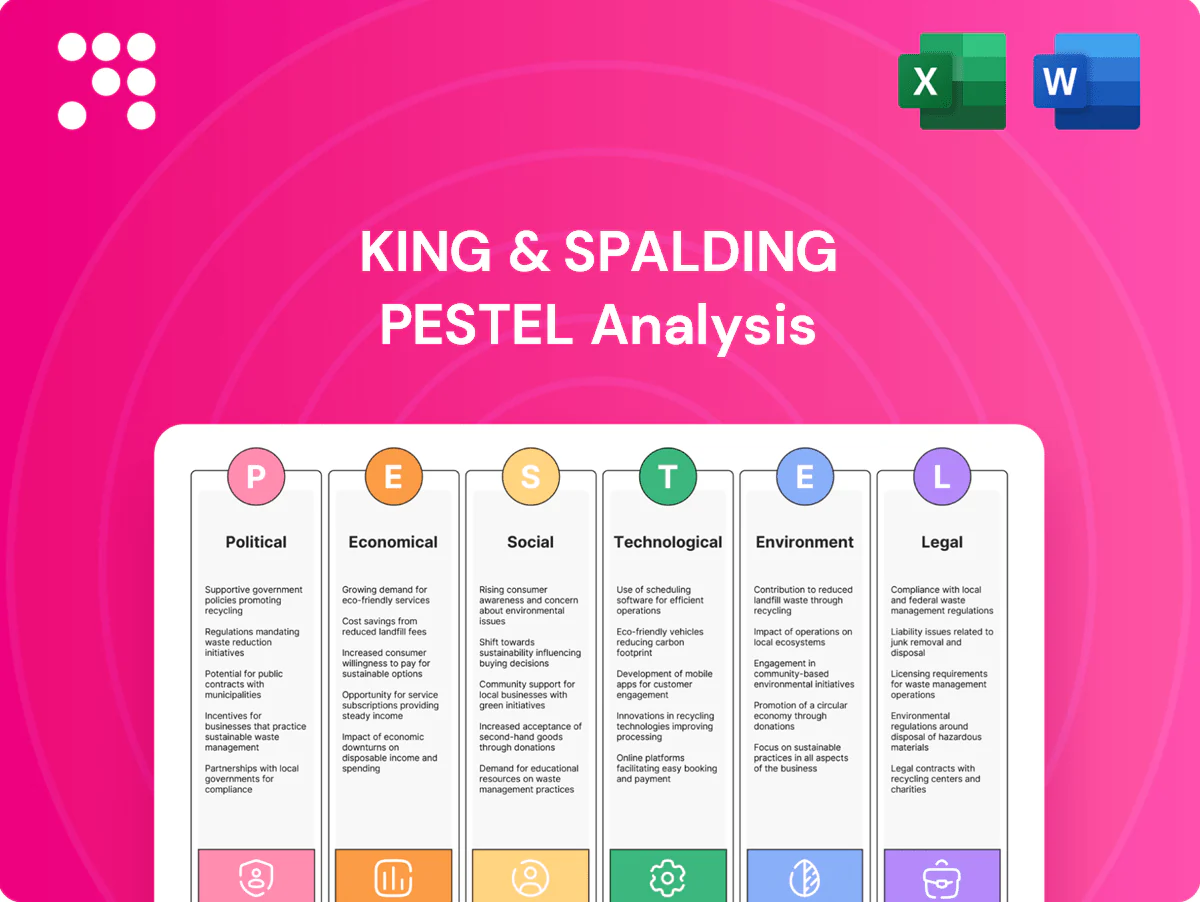

Political factors

Geopolitical volatility

Shifting geopolitics reshape cross-border transactions, disputes and enforcement priorities, with UNCTAD reporting global FDI flows down roughly 20% to about $1.2 trillion in 2023–24; heightened tensions delay approvals and raise diligence costs. King & Spalding must monitor regional risk to advise on structuring, venue selection and dispute resolution, using scenario planning to hedge political exposure.

Sanctions and export controls

Expanding U.S., UK and EU sanctions and export controls since 2022 — including more than a dozen EU packages on Russia and U.S. semiconductor export curbs in 2022–23 — are reshaping supply chains and project financing. Clients need real-time screening, licensing and remediation guidance. The firm’s global reach must align cross-regime advice to avoid conflicts, and rapid updates plus internal playbooks are critical.

Trade and industrial policy

Industrial policies, tariffs and subsidies reshape investment and M&A playbooks—US CHIPS Act ($52.7B) and Inflation Reduction Act (~$369B) are redirecting capital. Tech, energy and healthcare clients face shifting incentives, export controls and reimbursement changes. King & Spalding can structure deals to capture benefits while mitigating compliance risk and add value via advocacy and real‑time policy monitoring.

Anticorruption enforcement

Active FCPA and UK Bribery enforcement continues to drive cross-border investigations, DPAs and monitorships, requiring coordinated dawn-raids and multijurisdictional response teams; firms face dozens of related inquiries annually across DOJ, SEC and UK authorities.

King & Spalding supports risk assessments, tailored training, remediation and robust privilege and data-handling protocols to manage production, privilege logs and e-discovery under simultaneous foreign requests.

Foreign investment screening

CFIUS and allied FDI reviews, broadened by FIRRMA (2018), now target critical tech, data and infrastructure, driving earlier risk mapping and mitigation agreements that reshape deal terms and timelines. King & Spalding advises on carve-outs, governance and bespoke mitigation plans to secure clearances and limit divestiture risk. Strategic bidder coordination preserves transaction value and timing.

- CFIUS scope expanded 2018 (FIRRMA)

- Early mitigation shortens review delays

- Carve-outs and governance reduce clearance risk

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Geopolitical tensions cut global FDI ~20% to ~$1.2T in 2023–24 (UNCTAD), slowing cross‑border deals and raising diligence costs. Expanded sanctions/export controls and >12 EU Russia packages plus 2022–23 U.S. chip export curbs force real‑time screening and licensing. Industrial subsidies (CHIPS $52.7B; IRA ~$369B) and broadened CFIUS/FIRRMA reviews reshape deal terms and timelines.

| Metric | Value |

|---|---|

| Global FDI (2023–24) | $1.2T (-~20%) |

| EU sanctions on Russia | >12 packages |

| CHIPS Act | $52.7B |

| Inflation Reduction Act | ~$369B |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect King & Spalding, with data-driven trends, market/regulatory context and forward-looking insights to support executives, consultants and investors in identifying risks, opportunities and funding-ready strategy recommendations.

A concise, visually segmented King & Spalding PESTLE summary that’s easy to drop into presentations, editable for local context or practice area, and shareable for quick alignment across teams during strategy and risk discussions.

Economic factors

Deal cycle sensitivity

Deal cycle sensitivity: M&A and capital markets work track interest rates, liquidity, and valuations; with the US federal funds target at 5.25–5.50% in July 2025 higher financing costs have tightened deal pipelines. Slowdowns shift client demand toward restructuring, disputes, and distressed M&A. King & Spalding balances practice mix and uses cross-selling to stabilize revenue and cushion cyclical swings.

Client budget pressure

Client budget pressure drives corporate legal departments toward alternative fees and value-based billing, with surveys in 2024 showing firms increasingly offering AFAs to retain panel status; pricing strategies and matter-management tools are now key differentiators. Firms must deliver measurable outcomes and predictability—realization rates near 85–90% and reduced write-offs are tied to stronger knowledge management and process optimization.

Sector diversification

King & Spalding’s exposure across energy, healthcare, life sciences, tech and finance—supported by over 1,200 lawyers in 20+ offices—spreads client and revenue risk while capturing sector-specific mandates.

Sector cycles drive matter flow and staffing needs, with healthcare spending above 18% of US GDP and energy transition investment topping $1 trillion in 2024 shaping demand.

Deep regulatory expertise and thought leadership secure premium mandates; targeted business development aligns practices with macro tailwinds and rising sector deal activity.

Currency and cost dynamics

Global FX swings (USD trade-weighted moves ~7% in 2023) plus wage inflation (~4% global average in 2024 per OECD) and rising commercial rents pressure King & Spalding margins across geographies.

Nearshoring and legal-ops hubs, adaptive local rate cards/expense policies, hedging programs and flexible staffing can recover 10–30% of margin erosion.

- FX exposure

- Wage inflation

- Real-estate cost

- Hedging & staffing

Litigation funding growth

Third-party funding has expanded dispute pipelines and client access to justice, with leading funders reporting combined assets under management exceeding 10 billion USD by mid-2024, driving more commercial and class-action filings. Funding shifts case selection, budgeting and risk sharing, while King & Spalding must navigate disclosure and conflicts rules across jurisdictions. Portfolio funding increasingly aligns incentives between funders, counsel and clients, enabling strategic multi-case management.

- expands pipelines & access to justice

- impacts selection, budgeting, risk sharing

- requires cross-venue disclosure/conflicts management

- portfolio funding aligns incentives

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Higher rates (US fed funds 5.25–5.50% Jul 2025) and tighter liquidity have slowed M&A, shifting demand to restructurings and disputes; King & Spalding mitigates via cross-selling and practice mix. Wage inflation (~4% global 2024), FX volatility (~7% USD moves 2023) and rents compress margins; hedging and flexible staffing can recover 10–30%. Litigation fund AUM >10bn by mid-2024 expands dispute pipelines.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| Healthcare % GDP (US) | ≈18% |

| Energy transition 2024 | ≈$1tn |

| Litigation fund AUM (mid-2024) | >$10bn |

| Wage inflation (2024) | ~4% |

| USD TWI vol (2023) | ~7% |

Preview Before You Purchase

King & Spalding PESTLE Analysis

The King & Spalding PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a genuine screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are identical to the downloadable file you’ll get upon payment. You’ll receive this final, professionally structured report instantly after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock the external forces shaping King & Spalding with our concise PESTLE snapshot—covering regulatory shifts, economic pressures, tech disruption, social trends, and environmental risks. Perfect for investors and strategists seeking a competitive edge. Purchase the full PESTLE for an actionable, downloadable deep dive now.

Political factors

Geopolitical volatility

Shifting geopolitics reshape cross-border transactions, disputes and enforcement priorities, with UNCTAD reporting global FDI flows down roughly 20% to about $1.2 trillion in 2023–24; heightened tensions delay approvals and raise diligence costs. King & Spalding must monitor regional risk to advise on structuring, venue selection and dispute resolution, using scenario planning to hedge political exposure.

Sanctions and export controls

Expanding U.S., UK and EU sanctions and export controls since 2022 — including more than a dozen EU packages on Russia and U.S. semiconductor export curbs in 2022–23 — are reshaping supply chains and project financing. Clients need real-time screening, licensing and remediation guidance. The firm’s global reach must align cross-regime advice to avoid conflicts, and rapid updates plus internal playbooks are critical.

Trade and industrial policy

Industrial policies, tariffs and subsidies reshape investment and M&A playbooks—US CHIPS Act ($52.7B) and Inflation Reduction Act (~$369B) are redirecting capital. Tech, energy and healthcare clients face shifting incentives, export controls and reimbursement changes. King & Spalding can structure deals to capture benefits while mitigating compliance risk and add value via advocacy and real‑time policy monitoring.

Anticorruption enforcement

Active FCPA and UK Bribery enforcement continues to drive cross-border investigations, DPAs and monitorships, requiring coordinated dawn-raids and multijurisdictional response teams; firms face dozens of related inquiries annually across DOJ, SEC and UK authorities.

King & Spalding supports risk assessments, tailored training, remediation and robust privilege and data-handling protocols to manage production, privilege logs and e-discovery under simultaneous foreign requests.

Foreign investment screening

CFIUS and allied FDI reviews, broadened by FIRRMA (2018), now target critical tech, data and infrastructure, driving earlier risk mapping and mitigation agreements that reshape deal terms and timelines. King & Spalding advises on carve-outs, governance and bespoke mitigation plans to secure clearances and limit divestiture risk. Strategic bidder coordination preserves transaction value and timing.

- CFIUS scope expanded 2018 (FIRRMA)

- Early mitigation shortens review delays

- Carve-outs and governance reduce clearance risk

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Geopolitical tensions cut global FDI ~20% to ~$1.2T in 2023–24 (UNCTAD), slowing cross‑border deals and raising diligence costs. Expanded sanctions/export controls and >12 EU Russia packages plus 2022–23 U.S. chip export curbs force real‑time screening and licensing. Industrial subsidies (CHIPS $52.7B; IRA ~$369B) and broadened CFIUS/FIRRMA reviews reshape deal terms and timelines.

| Metric | Value |

|---|---|

| Global FDI (2023–24) | $1.2T (-~20%) |

| EU sanctions on Russia | >12 packages |

| CHIPS Act | $52.7B |

| Inflation Reduction Act | ~$369B |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect King & Spalding, with data-driven trends, market/regulatory context and forward-looking insights to support executives, consultants and investors in identifying risks, opportunities and funding-ready strategy recommendations.

A concise, visually segmented King & Spalding PESTLE summary that’s easy to drop into presentations, editable for local context or practice area, and shareable for quick alignment across teams during strategy and risk discussions.

Economic factors

Deal cycle sensitivity

Deal cycle sensitivity: M&A and capital markets work track interest rates, liquidity, and valuations; with the US federal funds target at 5.25–5.50% in July 2025 higher financing costs have tightened deal pipelines. Slowdowns shift client demand toward restructuring, disputes, and distressed M&A. King & Spalding balances practice mix and uses cross-selling to stabilize revenue and cushion cyclical swings.

Client budget pressure

Client budget pressure drives corporate legal departments toward alternative fees and value-based billing, with surveys in 2024 showing firms increasingly offering AFAs to retain panel status; pricing strategies and matter-management tools are now key differentiators. Firms must deliver measurable outcomes and predictability—realization rates near 85–90% and reduced write-offs are tied to stronger knowledge management and process optimization.

Sector diversification

King & Spalding’s exposure across energy, healthcare, life sciences, tech and finance—supported by over 1,200 lawyers in 20+ offices—spreads client and revenue risk while capturing sector-specific mandates.

Sector cycles drive matter flow and staffing needs, with healthcare spending above 18% of US GDP and energy transition investment topping $1 trillion in 2024 shaping demand.

Deep regulatory expertise and thought leadership secure premium mandates; targeted business development aligns practices with macro tailwinds and rising sector deal activity.

Currency and cost dynamics

Global FX swings (USD trade-weighted moves ~7% in 2023) plus wage inflation (~4% global average in 2024 per OECD) and rising commercial rents pressure King & Spalding margins across geographies.

Nearshoring and legal-ops hubs, adaptive local rate cards/expense policies, hedging programs and flexible staffing can recover 10–30% of margin erosion.

- FX exposure

- Wage inflation

- Real-estate cost

- Hedging & staffing

Litigation funding growth

Third-party funding has expanded dispute pipelines and client access to justice, with leading funders reporting combined assets under management exceeding 10 billion USD by mid-2024, driving more commercial and class-action filings. Funding shifts case selection, budgeting and risk sharing, while King & Spalding must navigate disclosure and conflicts rules across jurisdictions. Portfolio funding increasingly aligns incentives between funders, counsel and clients, enabling strategic multi-case management.

- expands pipelines & access to justice

- impacts selection, budgeting, risk sharing

- requires cross-venue disclosure/conflicts management

- portfolio funding aligns incentives

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Higher rates (US fed funds 5.25–5.50% Jul 2025) and tighter liquidity have slowed M&A, shifting demand to restructurings and disputes; King & Spalding mitigates via cross-selling and practice mix. Wage inflation (~4% global 2024), FX volatility (~7% USD moves 2023) and rents compress margins; hedging and flexible staffing can recover 10–30%. Litigation fund AUM >10bn by mid-2024 expands dispute pipelines.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| Healthcare % GDP (US) | ≈18% |

| Energy transition 2024 | ≈$1tn |

| Litigation fund AUM (mid-2024) | >$10bn |

| Wage inflation (2024) | ~4% |

| USD TWI vol (2023) | ~7% |

Preview Before You Purchase

King & Spalding PESTLE Analysis

The King & Spalding PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a genuine screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are identical to the downloadable file you’ll get upon payment. You’ll receive this final, professionally structured report instantly after checkout.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock the external forces shaping King & Spalding with our concise PESTLE snapshot—covering regulatory shifts, economic pressures, tech disruption, social trends, and environmental risks. Perfect for investors and strategists seeking a competitive edge. Purchase the full PESTLE for an actionable, downloadable deep dive now.

Political factors

Geopolitical volatility

Shifting geopolitics reshape cross-border transactions, disputes and enforcement priorities, with UNCTAD reporting global FDI flows down roughly 20% to about $1.2 trillion in 2023–24; heightened tensions delay approvals and raise diligence costs. King & Spalding must monitor regional risk to advise on structuring, venue selection and dispute resolution, using scenario planning to hedge political exposure.

Sanctions and export controls

Expanding U.S., UK and EU sanctions and export controls since 2022 — including more than a dozen EU packages on Russia and U.S. semiconductor export curbs in 2022–23 — are reshaping supply chains and project financing. Clients need real-time screening, licensing and remediation guidance. The firm’s global reach must align cross-regime advice to avoid conflicts, and rapid updates plus internal playbooks are critical.

Trade and industrial policy

Industrial policies, tariffs and subsidies reshape investment and M&A playbooks—US CHIPS Act ($52.7B) and Inflation Reduction Act (~$369B) are redirecting capital. Tech, energy and healthcare clients face shifting incentives, export controls and reimbursement changes. King & Spalding can structure deals to capture benefits while mitigating compliance risk and add value via advocacy and real‑time policy monitoring.

Anticorruption enforcement

Active FCPA and UK Bribery enforcement continues to drive cross-border investigations, DPAs and monitorships, requiring coordinated dawn-raids and multijurisdictional response teams; firms face dozens of related inquiries annually across DOJ, SEC and UK authorities.

King & Spalding supports risk assessments, tailored training, remediation and robust privilege and data-handling protocols to manage production, privilege logs and e-discovery under simultaneous foreign requests.

Foreign investment screening

CFIUS and allied FDI reviews, broadened by FIRRMA (2018), now target critical tech, data and infrastructure, driving earlier risk mapping and mitigation agreements that reshape deal terms and timelines. King & Spalding advises on carve-outs, governance and bespoke mitigation plans to secure clearances and limit divestiture risk. Strategic bidder coordination preserves transaction value and timing.

- CFIUS scope expanded 2018 (FIRRMA)

- Early mitigation shortens review delays

- Carve-outs and governance reduce clearance risk

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Geopolitical tensions cut global FDI ~20% to ~$1.2T in 2023–24 (UNCTAD), slowing cross‑border deals and raising diligence costs. Expanded sanctions/export controls and >12 EU Russia packages plus 2022–23 U.S. chip export curbs force real‑time screening and licensing. Industrial subsidies (CHIPS $52.7B; IRA ~$369B) and broadened CFIUS/FIRRMA reviews reshape deal terms and timelines.

| Metric | Value |

|---|---|

| Global FDI (2023–24) | $1.2T (-~20%) |

| EU sanctions on Russia | >12 packages |

| CHIPS Act | $52.7B |

| Inflation Reduction Act | ~$369B |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect King & Spalding, with data-driven trends, market/regulatory context and forward-looking insights to support executives, consultants and investors in identifying risks, opportunities and funding-ready strategy recommendations.

A concise, visually segmented King & Spalding PESTLE summary that’s easy to drop into presentations, editable for local context or practice area, and shareable for quick alignment across teams during strategy and risk discussions.

Economic factors

Deal cycle sensitivity

Deal cycle sensitivity: M&A and capital markets work track interest rates, liquidity, and valuations; with the US federal funds target at 5.25–5.50% in July 2025 higher financing costs have tightened deal pipelines. Slowdowns shift client demand toward restructuring, disputes, and distressed M&A. King & Spalding balances practice mix and uses cross-selling to stabilize revenue and cushion cyclical swings.

Client budget pressure

Client budget pressure drives corporate legal departments toward alternative fees and value-based billing, with surveys in 2024 showing firms increasingly offering AFAs to retain panel status; pricing strategies and matter-management tools are now key differentiators. Firms must deliver measurable outcomes and predictability—realization rates near 85–90% and reduced write-offs are tied to stronger knowledge management and process optimization.

Sector diversification

King & Spalding’s exposure across energy, healthcare, life sciences, tech and finance—supported by over 1,200 lawyers in 20+ offices—spreads client and revenue risk while capturing sector-specific mandates.

Sector cycles drive matter flow and staffing needs, with healthcare spending above 18% of US GDP and energy transition investment topping $1 trillion in 2024 shaping demand.

Deep regulatory expertise and thought leadership secure premium mandates; targeted business development aligns practices with macro tailwinds and rising sector deal activity.

Currency and cost dynamics

Global FX swings (USD trade-weighted moves ~7% in 2023) plus wage inflation (~4% global average in 2024 per OECD) and rising commercial rents pressure King & Spalding margins across geographies.

Nearshoring and legal-ops hubs, adaptive local rate cards/expense policies, hedging programs and flexible staffing can recover 10–30% of margin erosion.

- FX exposure

- Wage inflation

- Real-estate cost

- Hedging & staffing

Litigation funding growth

Third-party funding has expanded dispute pipelines and client access to justice, with leading funders reporting combined assets under management exceeding 10 billion USD by mid-2024, driving more commercial and class-action filings. Funding shifts case selection, budgeting and risk sharing, while King & Spalding must navigate disclosure and conflicts rules across jurisdictions. Portfolio funding increasingly aligns incentives between funders, counsel and clients, enabling strategic multi-case management.

- expands pipelines & access to justice

- impacts selection, budgeting, risk sharing

- requires cross-venue disclosure/conflicts management

- portfolio funding aligns incentives

Geopolitics cuts FDI ~20% to ~$1.2T; sanctions, subsidies and export controls reshape deals

Higher rates (US fed funds 5.25–5.50% Jul 2025) and tighter liquidity have slowed M&A, shifting demand to restructurings and disputes; King & Spalding mitigates via cross-selling and practice mix. Wage inflation (~4% global 2024), FX volatility (~7% USD moves 2023) and rents compress margins; hedging and flexible staffing can recover 10–30%. Litigation fund AUM >10bn by mid-2024 expands dispute pipelines.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| Healthcare % GDP (US) | ≈18% |

| Energy transition 2024 | ≈$1tn |

| Litigation fund AUM (mid-2024) | >$10bn |

| Wage inflation (2024) | ~4% |

| USD TWI vol (2023) | ~7% |

Preview Before You Purchase

King & Spalding PESTLE Analysis

The King & Spalding PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a genuine screenshot of the product with no placeholders or teasers. The layout, content, and structure visible are identical to the downloadable file you’ll get upon payment. You’ll receive this final, professionally structured report instantly after checkout.