Kyndryl Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

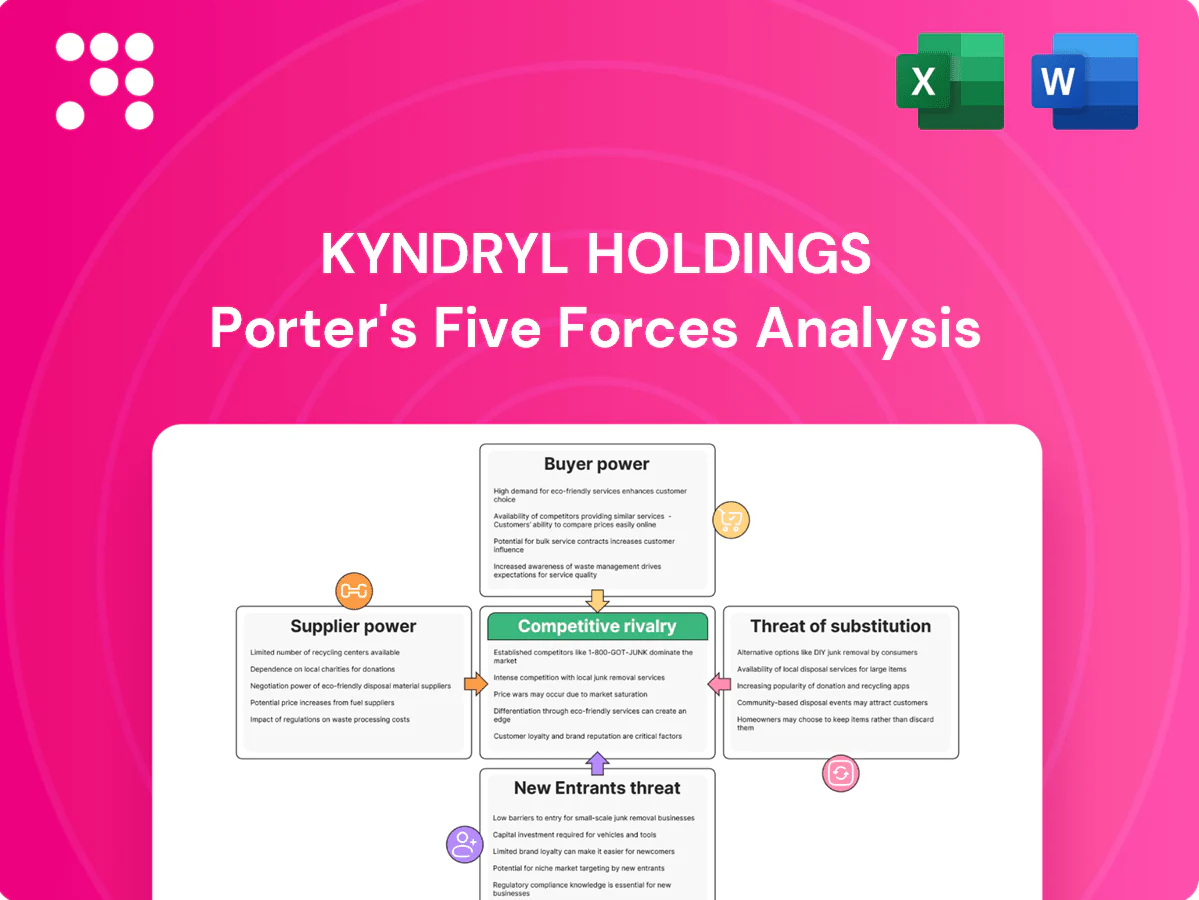

Kyndryl faces intense rivalry from global IT services giants and growing cloud-native competitors, with powerful enterprise buyers pressuring pricing and service breadth; supplier leverage is moderate while threat of new entrants remains low but substitutes like automation and hyperscaler platforms are rising. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kyndryl’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Hyperscaler platform dependence

Cloud providers AWS (≈33%), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024 control pricing, certification and partner rules that shape delivery economics. Their proprietary features and APIs create switching frictions for service providers, increasing costs and integration timelines. Kyndryl, with FY2024 revenue about $4.9B, needs preferred partnerships to secure discounts and roadmap influence. Concentration raises supplier leverage, though Kyndryl’s multi-cloud strategy partially offsets this risk.

Specialized hardware and software vendors

Kyndryl relies on a few OEMs for mainframes, servers, storage and network gear—zSystems and high-end storage have few substitutes, boosting supplier power. Long refresh cycles of 5–7 years and extended support contracts lock in pricing and terms. Kyndryl’s ~90,000 employees and volume buying improve negotiating leverage but do not remove dependence.

Skilled labor and niche talent scarcity

Architects for hybrid cloud, cybersecurity and mainframe ops remain scarce (cybersecurity workforce gap ~3.4M), giving contractors and specialist firms strong bargaining power; tight 2024 labor markets and ~6% tech wage inflation pressure Kyndryl’s margins and delivery capacity. Kyndryl offsets by ramping training, automation and offshore delivery centers to contain costs and scale talent.

Third-party software and tooling ecosystems

Third-party ITSM, observability, security and automation platforms are deeply embedded in Kyndryl delivery stacks, creating high licensing and integration costs and strong switching barriers; vendors can raise prices or bundle features to capture value. In 2024 the global cybersecurity market was roughly $220B and enterprise observability spending rose sharply, reinforcing supplier leverage, while pervasive open-source use (>90% of enterprises in 2024) provides some counterweight.

- High switching costs: licensing + integration

- Vendors can bundle/raise prices to capture margin

- Security market ≈$220B (2024) — strong supplier power

- Open-source >90% adoption (2024) gives partial leverage

Data center colocation and network providers

Where on-prem or hosted assets persist, colocation and telecom providers materially influence Kyndryl’s cost base and SLA terms; location scarcity in top metros drove premium pricing and sub-10% vacancy in several 2024 markets. Long-term contracts with carriers create exit barriers and stranded-cost risk for migrations. Diversifying sites and adopting software-defined networking reduced supplier leverage and lowered interconnect expense in real deployments during 2024.

- colocation scarcity: sub-10% vacancy in select 2024 metros

- long-term contracts: create exit barriers

- SdN benefits: lowers interconnect spend

Cloud concentration 33%/23%/11% - multi-cloud eases integrator exposure

Major cloud players (AWS ~33%, Azure ~23%, GCP ~11% in 2024) and a concentrated OEM base give suppliers strong pricing and integration leverage; Kyndryl (FY2024 revenue ~$4.9B) mitigates via preferred partnerships and multi-cloud. Talent scarcity (cyber gap ~3.4M) and a ~$220B security market raise contractor/vendor bargaining power; open-source (>90% adoption) offers partial counterbalance.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP share | 33% / 23% / 11% |

| Kyndryl revenue | $4.9B |

| Cyber gap | ~3.4M |

| Security market | $220B |

| Open-source adoption | >90% |

What is included in the product

Tailored exclusively for Kyndryl Holdings, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, and market entry risks affecting its IT services positioning. It identifies disruptive substitutes, supplier and buyer power, and market dynamics that shape pricing, profitability, and strategic defenses.

A compact Porter's Five Forces snapshot for Kyndryl—clearly scores competitive pressures and reveals where strategic moves will relieve supplier/customer or entrant threats.

Customers Bargaining Power

Large enterprise procurement muscle

Global 2000 customers (Forbes Global 2000, 2024) run competitive RFPs with full price transparency, forcing Kyndryl to unbundle multi-year, multi-tower deals to pressure rates. Strong vendor management offices enforce SLAs and financial penalties, driving renegotiations and shorter terms. The result is margin compression and a shift from multi‑year to 1–3 year contracts.

Ability to multisource services

Enterprises increasingly multisource services, splitting scope across providers for best-of-breed and cost control; industry surveys in 2024 show a majority adopting multi-vendor strategies, eroding single-vendor lock-in. Switching specific towers such as network and workplace is more feasible, heightening customer negotiation leverage. Kyndryl, with FY2024 revenue ~15.6B, must differentiate via integration prowess and outcome-based SLAs to retain clients.

Cloud-native alternatives

Customers can shift workloads to hyperscalers' managed services—hyperscalers captured roughly 70% of global cloud infrastructure spend in 2024—while native tools reduce reliance on third-party vendors, strengthening buyer leverage in price and scope negotiations. Kyndryl counters with multi-cloud governance and complex migration expertise leveraged by 92% of enterprises using multi-cloud per the 2024 Flexera report.

Outcome and risk-sharing expectations

Buyers increasingly demand consumption, gainshare and penalty-heavy contracts that bake cybersecurity resilience and regulatory compliance into service level agreements, shifting measurable downside risk onto providers and compressing margins; Kyndryl (NYSE: KD) must price in this redistributed risk and demonstrate quantifiable ROI. Robust risk management, insurance, and outcome metrics are now prerequisites for large enterprise deals.

- Risk shift: provider bears compliance/cyber liabilities

- Commercials: consumption + gainshare + penalties

- Requirement: measurable value delivery and KPIs

- Must-have: enterprise-grade risk controls and insurance

High information availability

High information availability lets buyers use benchmarking and analyst reports to spot pricing and performance gaps; Kyndryl reported $4.88 billion revenue in FY2023, making its public metrics easy to compare. Reference architectures and case studies reduce asymmetry, enabling rapid alternative comparisons and tougher concession negotiations. Strong differentiated IP and referenceable outcomes are critical to avoid descent into price-only competition.

- Benchmarking visibility: public FY2023 revenue $4.88B

- Info asymmetry reduced: reference architectures/case studies

- Buyer leverage: fast alternative comparison, tougher negotiations

- Defense: differentiated IP and referenceable outcomes essential

Enterprises force 1-3yr deals as hyperscalers seize ~70% of cloud spend

Large Global 2000 buyers run transparent RFPs and multisource strategies, shifting Kyndryl from multi‑year to 1–3 year contracts and compressing margins. Hyperscalers captured ~70% of cloud infra spend in 2024, boosting buyer leverage; 92% of enterprises ran multi‑cloud in 2024 (Flexera). Buyers demand consumption/gainshare models and penalty-heavy SLAs, pushing compliance/cyber risk onto providers.

| Metric | 2024 Value |

|---|---|

| Kyndryl FY2024 revenue | $15.6B |

| Kyndryl FY2023 revenue | $4.88B |

| Hyperscaler cloud infra share | ~70% |

| Multi‑cloud adoption (Flexera) | 92% |

| Contract term trend | 1–3 years |

Same Document Delivered

Kyndryl Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Kyndryl Holdings provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It highlights strategic implications and actionable recommendations for stakeholders. This preview is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no edits required.

A Must-Have Tool for Decision-Makers

Kyndryl faces intense rivalry from global IT services giants and growing cloud-native competitors, with powerful enterprise buyers pressuring pricing and service breadth; supplier leverage is moderate while threat of new entrants remains low but substitutes like automation and hyperscaler platforms are rising. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kyndryl’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Hyperscaler platform dependence

Cloud providers AWS (≈33%), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024 control pricing, certification and partner rules that shape delivery economics. Their proprietary features and APIs create switching frictions for service providers, increasing costs and integration timelines. Kyndryl, with FY2024 revenue about $4.9B, needs preferred partnerships to secure discounts and roadmap influence. Concentration raises supplier leverage, though Kyndryl’s multi-cloud strategy partially offsets this risk.

Specialized hardware and software vendors

Kyndryl relies on a few OEMs for mainframes, servers, storage and network gear—zSystems and high-end storage have few substitutes, boosting supplier power. Long refresh cycles of 5–7 years and extended support contracts lock in pricing and terms. Kyndryl’s ~90,000 employees and volume buying improve negotiating leverage but do not remove dependence.

Skilled labor and niche talent scarcity

Architects for hybrid cloud, cybersecurity and mainframe ops remain scarce (cybersecurity workforce gap ~3.4M), giving contractors and specialist firms strong bargaining power; tight 2024 labor markets and ~6% tech wage inflation pressure Kyndryl’s margins and delivery capacity. Kyndryl offsets by ramping training, automation and offshore delivery centers to contain costs and scale talent.

Third-party software and tooling ecosystems

Third-party ITSM, observability, security and automation platforms are deeply embedded in Kyndryl delivery stacks, creating high licensing and integration costs and strong switching barriers; vendors can raise prices or bundle features to capture value. In 2024 the global cybersecurity market was roughly $220B and enterprise observability spending rose sharply, reinforcing supplier leverage, while pervasive open-source use (>90% of enterprises in 2024) provides some counterweight.

- High switching costs: licensing + integration

- Vendors can bundle/raise prices to capture margin

- Security market ≈$220B (2024) — strong supplier power

- Open-source >90% adoption (2024) gives partial leverage

Data center colocation and network providers

Where on-prem or hosted assets persist, colocation and telecom providers materially influence Kyndryl’s cost base and SLA terms; location scarcity in top metros drove premium pricing and sub-10% vacancy in several 2024 markets. Long-term contracts with carriers create exit barriers and stranded-cost risk for migrations. Diversifying sites and adopting software-defined networking reduced supplier leverage and lowered interconnect expense in real deployments during 2024.

- colocation scarcity: sub-10% vacancy in select 2024 metros

- long-term contracts: create exit barriers

- SdN benefits: lowers interconnect spend

Cloud concentration 33%/23%/11% - multi-cloud eases integrator exposure

Major cloud players (AWS ~33%, Azure ~23%, GCP ~11% in 2024) and a concentrated OEM base give suppliers strong pricing and integration leverage; Kyndryl (FY2024 revenue ~$4.9B) mitigates via preferred partnerships and multi-cloud. Talent scarcity (cyber gap ~3.4M) and a ~$220B security market raise contractor/vendor bargaining power; open-source (>90% adoption) offers partial counterbalance.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP share | 33% / 23% / 11% |

| Kyndryl revenue | $4.9B |

| Cyber gap | ~3.4M |

| Security market | $220B |

| Open-source adoption | >90% |

What is included in the product

Tailored exclusively for Kyndryl Holdings, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, and market entry risks affecting its IT services positioning. It identifies disruptive substitutes, supplier and buyer power, and market dynamics that shape pricing, profitability, and strategic defenses.

A compact Porter's Five Forces snapshot for Kyndryl—clearly scores competitive pressures and reveals where strategic moves will relieve supplier/customer or entrant threats.

Customers Bargaining Power

Large enterprise procurement muscle

Global 2000 customers (Forbes Global 2000, 2024) run competitive RFPs with full price transparency, forcing Kyndryl to unbundle multi-year, multi-tower deals to pressure rates. Strong vendor management offices enforce SLAs and financial penalties, driving renegotiations and shorter terms. The result is margin compression and a shift from multi‑year to 1–3 year contracts.

Ability to multisource services

Enterprises increasingly multisource services, splitting scope across providers for best-of-breed and cost control; industry surveys in 2024 show a majority adopting multi-vendor strategies, eroding single-vendor lock-in. Switching specific towers such as network and workplace is more feasible, heightening customer negotiation leverage. Kyndryl, with FY2024 revenue ~15.6B, must differentiate via integration prowess and outcome-based SLAs to retain clients.

Cloud-native alternatives

Customers can shift workloads to hyperscalers' managed services—hyperscalers captured roughly 70% of global cloud infrastructure spend in 2024—while native tools reduce reliance on third-party vendors, strengthening buyer leverage in price and scope negotiations. Kyndryl counters with multi-cloud governance and complex migration expertise leveraged by 92% of enterprises using multi-cloud per the 2024 Flexera report.

Outcome and risk-sharing expectations

Buyers increasingly demand consumption, gainshare and penalty-heavy contracts that bake cybersecurity resilience and regulatory compliance into service level agreements, shifting measurable downside risk onto providers and compressing margins; Kyndryl (NYSE: KD) must price in this redistributed risk and demonstrate quantifiable ROI. Robust risk management, insurance, and outcome metrics are now prerequisites for large enterprise deals.

- Risk shift: provider bears compliance/cyber liabilities

- Commercials: consumption + gainshare + penalties

- Requirement: measurable value delivery and KPIs

- Must-have: enterprise-grade risk controls and insurance

High information availability

High information availability lets buyers use benchmarking and analyst reports to spot pricing and performance gaps; Kyndryl reported $4.88 billion revenue in FY2023, making its public metrics easy to compare. Reference architectures and case studies reduce asymmetry, enabling rapid alternative comparisons and tougher concession negotiations. Strong differentiated IP and referenceable outcomes are critical to avoid descent into price-only competition.

- Benchmarking visibility: public FY2023 revenue $4.88B

- Info asymmetry reduced: reference architectures/case studies

- Buyer leverage: fast alternative comparison, tougher negotiations

- Defense: differentiated IP and referenceable outcomes essential

Enterprises force 1-3yr deals as hyperscalers seize ~70% of cloud spend

Large Global 2000 buyers run transparent RFPs and multisource strategies, shifting Kyndryl from multi‑year to 1–3 year contracts and compressing margins. Hyperscalers captured ~70% of cloud infra spend in 2024, boosting buyer leverage; 92% of enterprises ran multi‑cloud in 2024 (Flexera). Buyers demand consumption/gainshare models and penalty-heavy SLAs, pushing compliance/cyber risk onto providers.

| Metric | 2024 Value |

|---|---|

| Kyndryl FY2024 revenue | $15.6B |

| Kyndryl FY2023 revenue | $4.88B |

| Hyperscaler cloud infra share | ~70% |

| Multi‑cloud adoption (Flexera) | 92% |

| Contract term trend | 1–3 years |

Same Document Delivered

Kyndryl Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Kyndryl Holdings provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It highlights strategic implications and actionable recommendations for stakeholders. This preview is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no edits required.

Description

A Must-Have Tool for Decision-Makers

Kyndryl faces intense rivalry from global IT services giants and growing cloud-native competitors, with powerful enterprise buyers pressuring pricing and service breadth; supplier leverage is moderate while threat of new entrants remains low but substitutes like automation and hyperscaler platforms are rising. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kyndryl’s competitive dynamics and strategic implications in depth.

Suppliers Bargaining Power

Hyperscaler platform dependence

Cloud providers AWS (≈33%), Microsoft Azure (≈23%) and Google Cloud (≈11%) in 2024 control pricing, certification and partner rules that shape delivery economics. Their proprietary features and APIs create switching frictions for service providers, increasing costs and integration timelines. Kyndryl, with FY2024 revenue about $4.9B, needs preferred partnerships to secure discounts and roadmap influence. Concentration raises supplier leverage, though Kyndryl’s multi-cloud strategy partially offsets this risk.

Specialized hardware and software vendors

Kyndryl relies on a few OEMs for mainframes, servers, storage and network gear—zSystems and high-end storage have few substitutes, boosting supplier power. Long refresh cycles of 5–7 years and extended support contracts lock in pricing and terms. Kyndryl’s ~90,000 employees and volume buying improve negotiating leverage but do not remove dependence.

Skilled labor and niche talent scarcity

Architects for hybrid cloud, cybersecurity and mainframe ops remain scarce (cybersecurity workforce gap ~3.4M), giving contractors and specialist firms strong bargaining power; tight 2024 labor markets and ~6% tech wage inflation pressure Kyndryl’s margins and delivery capacity. Kyndryl offsets by ramping training, automation and offshore delivery centers to contain costs and scale talent.

Third-party software and tooling ecosystems

Third-party ITSM, observability, security and automation platforms are deeply embedded in Kyndryl delivery stacks, creating high licensing and integration costs and strong switching barriers; vendors can raise prices or bundle features to capture value. In 2024 the global cybersecurity market was roughly $220B and enterprise observability spending rose sharply, reinforcing supplier leverage, while pervasive open-source use (>90% of enterprises in 2024) provides some counterweight.

- High switching costs: licensing + integration

- Vendors can bundle/raise prices to capture margin

- Security market ≈$220B (2024) — strong supplier power

- Open-source >90% adoption (2024) gives partial leverage

Data center colocation and network providers

Where on-prem or hosted assets persist, colocation and telecom providers materially influence Kyndryl’s cost base and SLA terms; location scarcity in top metros drove premium pricing and sub-10% vacancy in several 2024 markets. Long-term contracts with carriers create exit barriers and stranded-cost risk for migrations. Diversifying sites and adopting software-defined networking reduced supplier leverage and lowered interconnect expense in real deployments during 2024.

- colocation scarcity: sub-10% vacancy in select 2024 metros

- long-term contracts: create exit barriers

- SdN benefits: lowers interconnect spend

Cloud concentration 33%/23%/11% - multi-cloud eases integrator exposure

Major cloud players (AWS ~33%, Azure ~23%, GCP ~11% in 2024) and a concentrated OEM base give suppliers strong pricing and integration leverage; Kyndryl (FY2024 revenue ~$4.9B) mitigates via preferred partnerships and multi-cloud. Talent scarcity (cyber gap ~3.4M) and a ~$220B security market raise contractor/vendor bargaining power; open-source (>90% adoption) offers partial counterbalance.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP share | 33% / 23% / 11% |

| Kyndryl revenue | $4.9B |

| Cyber gap | ~3.4M |

| Security market | $220B |

| Open-source adoption | >90% |

What is included in the product

Tailored exclusively for Kyndryl Holdings, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, and market entry risks affecting its IT services positioning. It identifies disruptive substitutes, supplier and buyer power, and market dynamics that shape pricing, profitability, and strategic defenses.

A compact Porter's Five Forces snapshot for Kyndryl—clearly scores competitive pressures and reveals where strategic moves will relieve supplier/customer or entrant threats.

Customers Bargaining Power

Large enterprise procurement muscle

Global 2000 customers (Forbes Global 2000, 2024) run competitive RFPs with full price transparency, forcing Kyndryl to unbundle multi-year, multi-tower deals to pressure rates. Strong vendor management offices enforce SLAs and financial penalties, driving renegotiations and shorter terms. The result is margin compression and a shift from multi‑year to 1–3 year contracts.

Ability to multisource services

Enterprises increasingly multisource services, splitting scope across providers for best-of-breed and cost control; industry surveys in 2024 show a majority adopting multi-vendor strategies, eroding single-vendor lock-in. Switching specific towers such as network and workplace is more feasible, heightening customer negotiation leverage. Kyndryl, with FY2024 revenue ~15.6B, must differentiate via integration prowess and outcome-based SLAs to retain clients.

Cloud-native alternatives

Customers can shift workloads to hyperscalers' managed services—hyperscalers captured roughly 70% of global cloud infrastructure spend in 2024—while native tools reduce reliance on third-party vendors, strengthening buyer leverage in price and scope negotiations. Kyndryl counters with multi-cloud governance and complex migration expertise leveraged by 92% of enterprises using multi-cloud per the 2024 Flexera report.

Outcome and risk-sharing expectations

Buyers increasingly demand consumption, gainshare and penalty-heavy contracts that bake cybersecurity resilience and regulatory compliance into service level agreements, shifting measurable downside risk onto providers and compressing margins; Kyndryl (NYSE: KD) must price in this redistributed risk and demonstrate quantifiable ROI. Robust risk management, insurance, and outcome metrics are now prerequisites for large enterprise deals.

- Risk shift: provider bears compliance/cyber liabilities

- Commercials: consumption + gainshare + penalties

- Requirement: measurable value delivery and KPIs

- Must-have: enterprise-grade risk controls and insurance

High information availability

High information availability lets buyers use benchmarking and analyst reports to spot pricing and performance gaps; Kyndryl reported $4.88 billion revenue in FY2023, making its public metrics easy to compare. Reference architectures and case studies reduce asymmetry, enabling rapid alternative comparisons and tougher concession negotiations. Strong differentiated IP and referenceable outcomes are critical to avoid descent into price-only competition.

- Benchmarking visibility: public FY2023 revenue $4.88B

- Info asymmetry reduced: reference architectures/case studies

- Buyer leverage: fast alternative comparison, tougher negotiations

- Defense: differentiated IP and referenceable outcomes essential

Enterprises force 1-3yr deals as hyperscalers seize ~70% of cloud spend

Large Global 2000 buyers run transparent RFPs and multisource strategies, shifting Kyndryl from multi‑year to 1–3 year contracts and compressing margins. Hyperscalers captured ~70% of cloud infra spend in 2024, boosting buyer leverage; 92% of enterprises ran multi‑cloud in 2024 (Flexera). Buyers demand consumption/gainshare models and penalty-heavy SLAs, pushing compliance/cyber risk onto providers.

| Metric | 2024 Value |

|---|---|

| Kyndryl FY2024 revenue | $15.6B |

| Kyndryl FY2023 revenue | $4.88B |

| Hyperscaler cloud infra share | ~70% |

| Multi‑cloud adoption (Flexera) | 92% |

| Contract term trend | 1–3 years |

Same Document Delivered

Kyndryl Holdings Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Kyndryl Holdings provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It highlights strategic implications and actionable recommendations for stakeholders. This preview is the exact, fully formatted document you’ll receive instantly after purchase—no placeholders, no edits required.