Kyushu Financial Group Business Model Canvas

Unlock the strategic Business Model Canvas for a regional financial group — concise & actionable

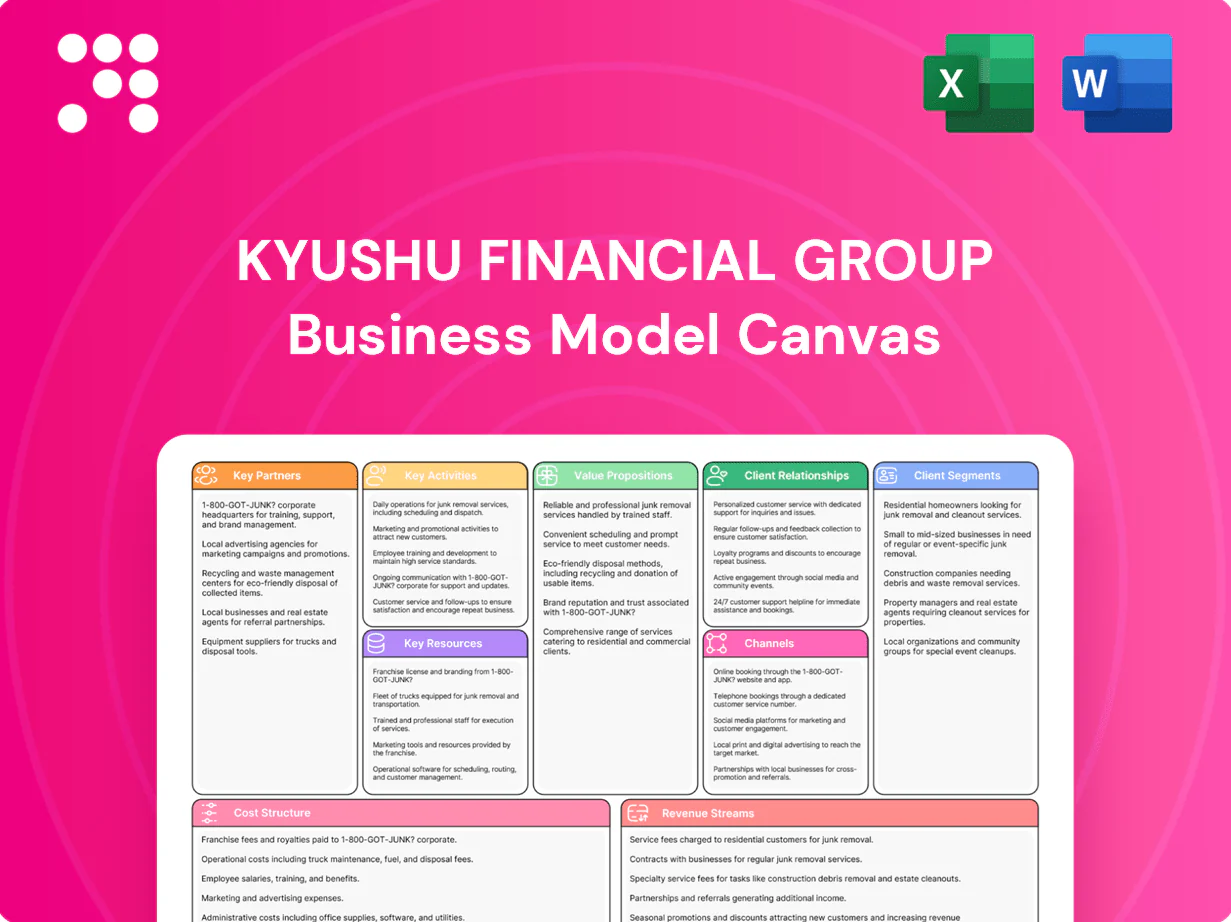

Unlock the strategic blueprint behind Kyushu Financial Group with our concise Business Model Canvas summary—covering customer segments, value propositions, channels and revenue streams. Dive deeper by purchasing the full, editable Canvas for a section-by-section analysis and actionable insights for investors and strategists.

Partnerships

Regional industry alliances

Partnerships with local chambers of commerce and industry associations anchor SME outreach, tapping into Kyushu’s ~13.1 million population and dense SME base. These alliances provide sector insights and co-host financing programs, improving credit pipeline quality and borrower trust. By aligning product design with regional development priorities, lending supports local industrial strategies; SMEs, which account for 99.7% of Japanese firms, benefit directly.

Government and municipal bodies

Collaboration with prefectural and city governments unlocks subsidies, guarantee schemes and disaster-recovery finance that supported over ¥120 billion in regionally targeted projects in 2024, enhancing Kyushu Financial Group’s ability to fund reconstruction and SMEs. Joint programs in infrastructure, tourism and agriculture boost loan pipelines and fee income while guarantee schemes reduce credit risk by transferring loss exposure. Such partnerships elevate public-good impact and visibility across Kyushu, aligning bank lending with municipal development goals.

Fintech and IT vendors

Alliances with fintechs accelerate digital onboarding, payments, and analytics, cutting onboarding time and aligning with Japan's push toward higher cashless adoption (around 40% by 2024). Core-banking and cybersecurity vendors provide stability, regulatory compliance, and uptime for KFG’s retail and SME platforms. Co-innovation partnerships speed feature rollout and integrations, improving customer experience and lowering operational friction and processing costs.

Merchant and card networks

Ties with JCB (accepted in ~190 countries) and Visa (229 billion network transactions in 2022) expand card acceptance and rewards across Kyushu, lifting card penetration as Japan targets a 40% cashless ratio by 2025. Co-branded programs increase spend and retention, while interchange economics scale fee income and cement links between consumers and regional SMEs.

- Network reach: JCB ~190 countries, Visa global scale

- Transaction scale: Visa 229B txns (2022)

- Cashless push: Japan 40% target by 2025

- Benefits: higher spend, retention, interchange-led revenue

Leasing, insurance, and JV partners

Leasing, insurance, and JV partners—including equipment suppliers, insurers, and OEMs—co-develop leasing and bancassurance offers that integrate point-of-sale financing to capture capex cycles; Kyushu Financial Group reported a 2024 uptick in POS loan originations aligning with regional corporate capex recovery. Risk-sharing structures with insurers and OEMs stabilize returns and broaden non-interest income, contributing to fee revenue diversification in 2024.

- Equipment suppliers: co-developed leasing

- Insurers: bancassurance risk-share

- OEMs: POS financing at sale

- Impact: stabilizes returns, boosts non-interest income (2024)

Kyushu scale: SME lending, disaster finance & cashless growth with ¥120B projects

KFG leverages chambers, local governments, fintechs, card networks and insurers to drive SME lending, disaster finance and digital services across Kyushu’s ~13.1M population. Partnerships enabled over ¥120 billion in regionally targeted projects in 2024, boosted POS loans and diversified fee income via bancassurance and leasing. Card alliances (JCB ~190 countries, Visa 229B txns 2022) and cashless push (~40% by 2024) raise spend and retention.

| Metric | Value |

|---|---|

| Kyushu pop (2024) | ~13.1M |

| SME share | 99.7% |

| Regional projects (2024) | ¥120B |

| Cashless rate (Japan, 2024) | ~40% |

| Visa txns (2022) | 229B |

| JCB reach | ~190 countries |

What is included in the product

A concise, pre-built Business Model Canvas for Kyushu Financial Group mapping customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks. Reflects bank/regional finance operations, strategic strengths and risks, and is ideal for investor presentations, strategic planning and validating growth initiatives.

High-level view of Kyushu Financial Group’s business model with editable cells, saving hours of structuring while condensing strategy into a digestible one-page snapshot for teams, boardrooms, and fast decision-making.

Activities

Retail and SME lending

Originate and manage mortgages, consumer loans and SME credit lines with risk-based pricing and strict collateral management, targeting credit quality aligned with regional demographics (Japan 65+ share ~29% in 2024). Portfolios are monitored via early-warning systems and monthly scoring to detect deterioration. Recovery teams offer restructuring and tailored repayment plans to preserve borrower viability and limit losses.

Deposit gathering

Attract stable retail and corporate deposits across Kyushu regions, tailoring offers to local industries while optimizing rates and product mix to balance cost of funds. Promote payroll and transaction accounts to deepen relationships and fee income. Maintain liquidity buffers in line with Basel III LCR target of ≥100% as of 2024.

Payments and cards

Kyushu Financial Group issues and acquires consumer and merchant cards, operating settlement, fraud monitoring and rewards programs to support regional commerce. The group is expanding contactless and QR ecosystems to capture rising digital spend as Japan targets a 40% cashless payment ratio by 2025 (METI). Partnerships with retailers and local governments drive cashless adoption and merchant onboarding across Kyushu.

Leasing and asset finance

Provide equipment, vehicle and IT leasing to SMEs and municipalities, underwriting residual values prudently and bundling maintenance and insurance to reduce client operational risk. Tenors are aligned with asset life and client cash flows to minimize maturity mismatches and credit stress. Pricing reflects lifecycle risk and service bundles to improve retention.

- Focus: SME and municipal leasing

- Risk: prudent residual valuation

- Service: maintenance + insurance bundled

- Structuring: tenor = asset life + cash flow

Advisory and community programs

Originate mortgages & SME loans; 65+ ~29%, Kyushu ~13M

Originate/manage mortgages, consumer and SME loans with risk-based pricing; 65+ share ~29% (2024), Kyushu pop ~13M.

Attract retail/corporate deposits, push payroll/transaction accounts; maintain LCR ≥100% (2024).

Operate card acquiring, fraud monitoring, expand QR/contactless to hit 40% cashless target by 2025.

Leasing and SME advisory; SMEs = 99.7% firms, ~70% workforce; host seminars and channel public funds.

| Metric | 2024 |

|---|---|

| 65+ share | ~29% |

| Kyushu pop | ~13M |

| LCR | ≥100% |

Preview Before You Purchase

Business Model Canvas

The Kyushu Financial Group Business Model Canvas previewed here is the actual document you will receive—no mockups or samples. Upon purchase you'll get this same complete, editable file exactly as shown, ready for presentation and editing in Word and Excel formats. No surprises.

Unlock the strategic Business Model Canvas for a regional financial group — concise & actionable

Unlock the strategic blueprint behind Kyushu Financial Group with our concise Business Model Canvas summary—covering customer segments, value propositions, channels and revenue streams. Dive deeper by purchasing the full, editable Canvas for a section-by-section analysis and actionable insights for investors and strategists.

Partnerships

Regional industry alliances

Partnerships with local chambers of commerce and industry associations anchor SME outreach, tapping into Kyushu’s ~13.1 million population and dense SME base. These alliances provide sector insights and co-host financing programs, improving credit pipeline quality and borrower trust. By aligning product design with regional development priorities, lending supports local industrial strategies; SMEs, which account for 99.7% of Japanese firms, benefit directly.

Government and municipal bodies

Collaboration with prefectural and city governments unlocks subsidies, guarantee schemes and disaster-recovery finance that supported over ¥120 billion in regionally targeted projects in 2024, enhancing Kyushu Financial Group’s ability to fund reconstruction and SMEs. Joint programs in infrastructure, tourism and agriculture boost loan pipelines and fee income while guarantee schemes reduce credit risk by transferring loss exposure. Such partnerships elevate public-good impact and visibility across Kyushu, aligning bank lending with municipal development goals.

Fintech and IT vendors

Alliances with fintechs accelerate digital onboarding, payments, and analytics, cutting onboarding time and aligning with Japan's push toward higher cashless adoption (around 40% by 2024). Core-banking and cybersecurity vendors provide stability, regulatory compliance, and uptime for KFG’s retail and SME platforms. Co-innovation partnerships speed feature rollout and integrations, improving customer experience and lowering operational friction and processing costs.

Merchant and card networks

Ties with JCB (accepted in ~190 countries) and Visa (229 billion network transactions in 2022) expand card acceptance and rewards across Kyushu, lifting card penetration as Japan targets a 40% cashless ratio by 2025. Co-branded programs increase spend and retention, while interchange economics scale fee income and cement links between consumers and regional SMEs.

- Network reach: JCB ~190 countries, Visa global scale

- Transaction scale: Visa 229B txns (2022)

- Cashless push: Japan 40% target by 2025

- Benefits: higher spend, retention, interchange-led revenue

Leasing, insurance, and JV partners

Leasing, insurance, and JV partners—including equipment suppliers, insurers, and OEMs—co-develop leasing and bancassurance offers that integrate point-of-sale financing to capture capex cycles; Kyushu Financial Group reported a 2024 uptick in POS loan originations aligning with regional corporate capex recovery. Risk-sharing structures with insurers and OEMs stabilize returns and broaden non-interest income, contributing to fee revenue diversification in 2024.

- Equipment suppliers: co-developed leasing

- Insurers: bancassurance risk-share

- OEMs: POS financing at sale

- Impact: stabilizes returns, boosts non-interest income (2024)

Kyushu scale: SME lending, disaster finance & cashless growth with ¥120B projects

KFG leverages chambers, local governments, fintechs, card networks and insurers to drive SME lending, disaster finance and digital services across Kyushu’s ~13.1M population. Partnerships enabled over ¥120 billion in regionally targeted projects in 2024, boosted POS loans and diversified fee income via bancassurance and leasing. Card alliances (JCB ~190 countries, Visa 229B txns 2022) and cashless push (~40% by 2024) raise spend and retention.

| Metric | Value |

|---|---|

| Kyushu pop (2024) | ~13.1M |

| SME share | 99.7% |

| Regional projects (2024) | ¥120B |

| Cashless rate (Japan, 2024) | ~40% |

| Visa txns (2022) | 229B |

| JCB reach | ~190 countries |

What is included in the product

A concise, pre-built Business Model Canvas for Kyushu Financial Group mapping customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks. Reflects bank/regional finance operations, strategic strengths and risks, and is ideal for investor presentations, strategic planning and validating growth initiatives.

High-level view of Kyushu Financial Group’s business model with editable cells, saving hours of structuring while condensing strategy into a digestible one-page snapshot for teams, boardrooms, and fast decision-making.

Activities

Retail and SME lending

Originate and manage mortgages, consumer loans and SME credit lines with risk-based pricing and strict collateral management, targeting credit quality aligned with regional demographics (Japan 65+ share ~29% in 2024). Portfolios are monitored via early-warning systems and monthly scoring to detect deterioration. Recovery teams offer restructuring and tailored repayment plans to preserve borrower viability and limit losses.

Deposit gathering

Attract stable retail and corporate deposits across Kyushu regions, tailoring offers to local industries while optimizing rates and product mix to balance cost of funds. Promote payroll and transaction accounts to deepen relationships and fee income. Maintain liquidity buffers in line with Basel III LCR target of ≥100% as of 2024.

Payments and cards

Kyushu Financial Group issues and acquires consumer and merchant cards, operating settlement, fraud monitoring and rewards programs to support regional commerce. The group is expanding contactless and QR ecosystems to capture rising digital spend as Japan targets a 40% cashless payment ratio by 2025 (METI). Partnerships with retailers and local governments drive cashless adoption and merchant onboarding across Kyushu.

Leasing and asset finance

Provide equipment, vehicle and IT leasing to SMEs and municipalities, underwriting residual values prudently and bundling maintenance and insurance to reduce client operational risk. Tenors are aligned with asset life and client cash flows to minimize maturity mismatches and credit stress. Pricing reflects lifecycle risk and service bundles to improve retention.

- Focus: SME and municipal leasing

- Risk: prudent residual valuation

- Service: maintenance + insurance bundled

- Structuring: tenor = asset life + cash flow

Advisory and community programs

Originate mortgages & SME loans; 65+ ~29%, Kyushu ~13M

Originate/manage mortgages, consumer and SME loans with risk-based pricing; 65+ share ~29% (2024), Kyushu pop ~13M.

Attract retail/corporate deposits, push payroll/transaction accounts; maintain LCR ≥100% (2024).

Operate card acquiring, fraud monitoring, expand QR/contactless to hit 40% cashless target by 2025.

Leasing and SME advisory; SMEs = 99.7% firms, ~70% workforce; host seminars and channel public funds.

| Metric | 2024 |

|---|---|

| 65+ share | ~29% |

| Kyushu pop | ~13M |

| LCR | ≥100% |

Preview Before You Purchase

Business Model Canvas

The Kyushu Financial Group Business Model Canvas previewed here is the actual document you will receive—no mockups or samples. Upon purchase you'll get this same complete, editable file exactly as shown, ready for presentation and editing in Word and Excel formats. No surprises.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic Business Model Canvas for a regional financial group — concise & actionable

Unlock the strategic blueprint behind Kyushu Financial Group with our concise Business Model Canvas summary—covering customer segments, value propositions, channels and revenue streams. Dive deeper by purchasing the full, editable Canvas for a section-by-section analysis and actionable insights for investors and strategists.

Partnerships

Regional industry alliances

Partnerships with local chambers of commerce and industry associations anchor SME outreach, tapping into Kyushu’s ~13.1 million population and dense SME base. These alliances provide sector insights and co-host financing programs, improving credit pipeline quality and borrower trust. By aligning product design with regional development priorities, lending supports local industrial strategies; SMEs, which account for 99.7% of Japanese firms, benefit directly.

Government and municipal bodies

Collaboration with prefectural and city governments unlocks subsidies, guarantee schemes and disaster-recovery finance that supported over ¥120 billion in regionally targeted projects in 2024, enhancing Kyushu Financial Group’s ability to fund reconstruction and SMEs. Joint programs in infrastructure, tourism and agriculture boost loan pipelines and fee income while guarantee schemes reduce credit risk by transferring loss exposure. Such partnerships elevate public-good impact and visibility across Kyushu, aligning bank lending with municipal development goals.

Fintech and IT vendors

Alliances with fintechs accelerate digital onboarding, payments, and analytics, cutting onboarding time and aligning with Japan's push toward higher cashless adoption (around 40% by 2024). Core-banking and cybersecurity vendors provide stability, regulatory compliance, and uptime for KFG’s retail and SME platforms. Co-innovation partnerships speed feature rollout and integrations, improving customer experience and lowering operational friction and processing costs.

Merchant and card networks

Ties with JCB (accepted in ~190 countries) and Visa (229 billion network transactions in 2022) expand card acceptance and rewards across Kyushu, lifting card penetration as Japan targets a 40% cashless ratio by 2025. Co-branded programs increase spend and retention, while interchange economics scale fee income and cement links between consumers and regional SMEs.

- Network reach: JCB ~190 countries, Visa global scale

- Transaction scale: Visa 229B txns (2022)

- Cashless push: Japan 40% target by 2025

- Benefits: higher spend, retention, interchange-led revenue

Leasing, insurance, and JV partners

Leasing, insurance, and JV partners—including equipment suppliers, insurers, and OEMs—co-develop leasing and bancassurance offers that integrate point-of-sale financing to capture capex cycles; Kyushu Financial Group reported a 2024 uptick in POS loan originations aligning with regional corporate capex recovery. Risk-sharing structures with insurers and OEMs stabilize returns and broaden non-interest income, contributing to fee revenue diversification in 2024.

- Equipment suppliers: co-developed leasing

- Insurers: bancassurance risk-share

- OEMs: POS financing at sale

- Impact: stabilizes returns, boosts non-interest income (2024)

Kyushu scale: SME lending, disaster finance & cashless growth with ¥120B projects

KFG leverages chambers, local governments, fintechs, card networks and insurers to drive SME lending, disaster finance and digital services across Kyushu’s ~13.1M population. Partnerships enabled over ¥120 billion in regionally targeted projects in 2024, boosted POS loans and diversified fee income via bancassurance and leasing. Card alliances (JCB ~190 countries, Visa 229B txns 2022) and cashless push (~40% by 2024) raise spend and retention.

| Metric | Value |

|---|---|

| Kyushu pop (2024) | ~13.1M |

| SME share | 99.7% |

| Regional projects (2024) | ¥120B |

| Cashless rate (Japan, 2024) | ~40% |

| Visa txns (2022) | 229B |

| JCB reach | ~190 countries |

What is included in the product

A concise, pre-built Business Model Canvas for Kyushu Financial Group mapping customer segments, channels, value propositions, revenue streams, key resources and partners across the 9 BMC blocks. Reflects bank/regional finance operations, strategic strengths and risks, and is ideal for investor presentations, strategic planning and validating growth initiatives.

High-level view of Kyushu Financial Group’s business model with editable cells, saving hours of structuring while condensing strategy into a digestible one-page snapshot for teams, boardrooms, and fast decision-making.

Activities

Retail and SME lending

Originate and manage mortgages, consumer loans and SME credit lines with risk-based pricing and strict collateral management, targeting credit quality aligned with regional demographics (Japan 65+ share ~29% in 2024). Portfolios are monitored via early-warning systems and monthly scoring to detect deterioration. Recovery teams offer restructuring and tailored repayment plans to preserve borrower viability and limit losses.

Deposit gathering

Attract stable retail and corporate deposits across Kyushu regions, tailoring offers to local industries while optimizing rates and product mix to balance cost of funds. Promote payroll and transaction accounts to deepen relationships and fee income. Maintain liquidity buffers in line with Basel III LCR target of ≥100% as of 2024.

Payments and cards

Kyushu Financial Group issues and acquires consumer and merchant cards, operating settlement, fraud monitoring and rewards programs to support regional commerce. The group is expanding contactless and QR ecosystems to capture rising digital spend as Japan targets a 40% cashless payment ratio by 2025 (METI). Partnerships with retailers and local governments drive cashless adoption and merchant onboarding across Kyushu.

Leasing and asset finance

Provide equipment, vehicle and IT leasing to SMEs and municipalities, underwriting residual values prudently and bundling maintenance and insurance to reduce client operational risk. Tenors are aligned with asset life and client cash flows to minimize maturity mismatches and credit stress. Pricing reflects lifecycle risk and service bundles to improve retention.

- Focus: SME and municipal leasing

- Risk: prudent residual valuation

- Service: maintenance + insurance bundled

- Structuring: tenor = asset life + cash flow

Advisory and community programs

Originate mortgages & SME loans; 65+ ~29%, Kyushu ~13M

Originate/manage mortgages, consumer and SME loans with risk-based pricing; 65+ share ~29% (2024), Kyushu pop ~13M.

Attract retail/corporate deposits, push payroll/transaction accounts; maintain LCR ≥100% (2024).

Operate card acquiring, fraud monitoring, expand QR/contactless to hit 40% cashless target by 2025.

Leasing and SME advisory; SMEs = 99.7% firms, ~70% workforce; host seminars and channel public funds.

| Metric | 2024 |

|---|---|

| 65+ share | ~29% |

| Kyushu pop | ~13M |

| LCR | ≥100% |

Preview Before You Purchase

Business Model Canvas

The Kyushu Financial Group Business Model Canvas previewed here is the actual document you will receive—no mockups or samples. Upon purchase you'll get this same complete, editable file exactly as shown, ready for presentation and editing in Word and Excel formats. No surprises.