Kyushu Financial Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

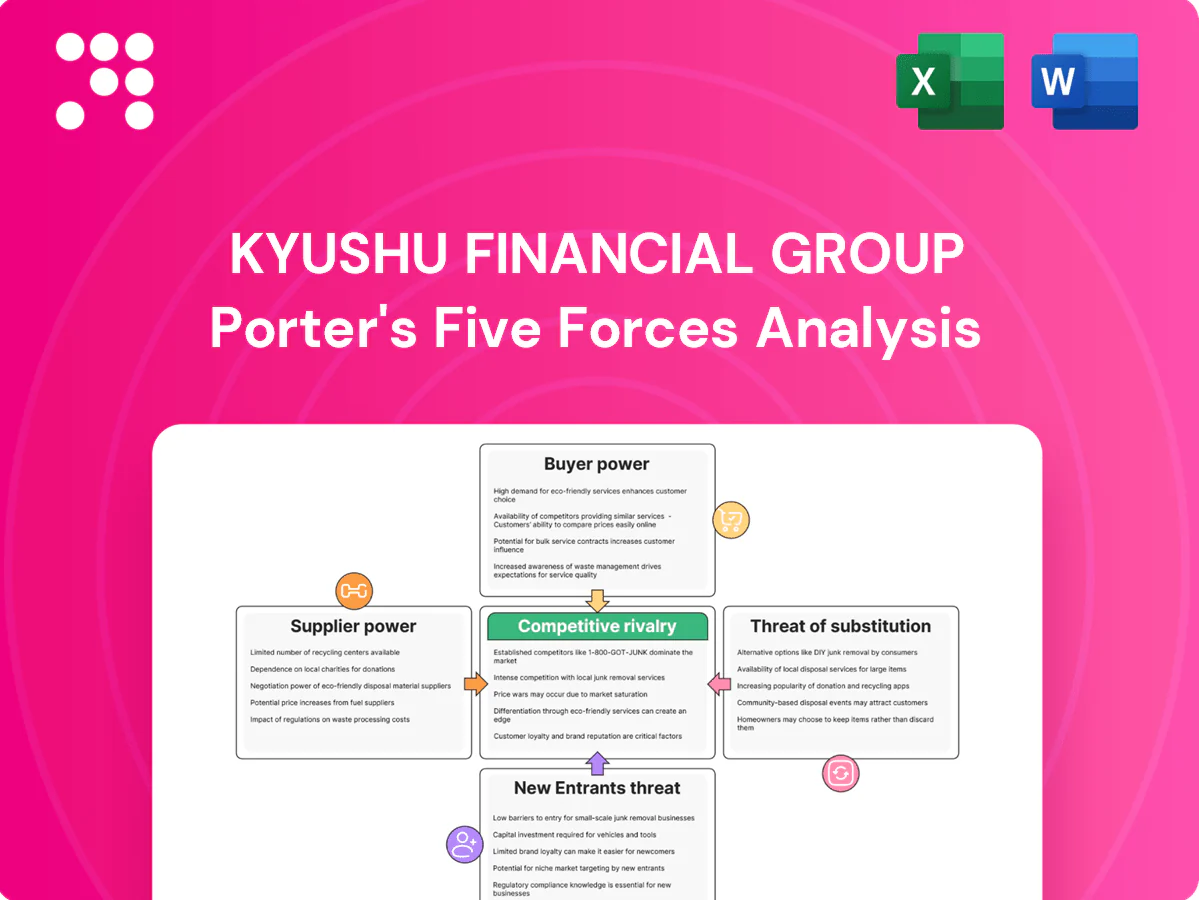

Kyushu Financial Group faces moderate competitive rivalry, constrained by regional banking concentration and rising fintech substitutes, while customer bargaining power grows with digital channels and low-rate sensitivity. Regulatory oversight and capital needs temper new entrants, yet supplier influence remains limited. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated core IT vendors

Japanese banks depend on a few core-banking and payment providers such as Fujitsu, NEC, NTT DATA and Hitachi, creating vendor concentration risk. Core replacements are costly, risky and time-consuming, typically taking 2–5 years and costing from several hundred million to multiple billion yen, giving suppliers leverage on pricing and roadmap. Long-term contracts and industry standards limit abrupt hikes, while group-scale across subsidiaries can modestly improve negotiation leverage.

Payment networks and card schemes

Card networks and domestic rails set fees, rules and mandatory tech upgrades, leaving Kyushu Financial Group as a price-taker on interchange and assessment charges. Co-branding with JCB/visa and higher transaction volumes can secure modest fee concessions, but bargaining leverage remains limited. Japan’s cashless transaction value exceeded ¥300 trillion in 2024 with a cashless ratio near 37%, and regulatory oversight increasingly caps fee hikes.

Data centers and cybersecurity providers

Dependence on regulated-grade hosting, cloud, and security vendors creates high switching costs for Kyushu Financial Group, embedding supplier leverage through compliance and certification requirements. Cyber resilience mandates push the bank to premium partners, further elevating supplier power. Multi-vendor strategies reduce lock-in risk but add integration complexity and operational overhead. Group scale improves negotiating leverage to secure stronger SLAs and terms.

Skilled workforce and local talent

Experienced relationship bankers, risk managers and fintech talent are scarce in Kyushu, raising supplier power of labor as Japan’s 65+ population reached about 29.1% in 2024, tightening local labor markets and lifting wage pressure for banks competing for specialists. Training pipelines and rotation across subsidiaries can lower dependence, while remote/hybrid hiring expands the talent pool but risks diluting culture and client intimacy.

Wholesale and interbank funding

In stressed markets wholesale and interbank providers tighten spreads and add covenants, raising costs and bargaining power; in 2024 KFG’s stable retail deposit base—over 80% of total funding—limits reliance on volatile wholesale channels.

Maintaining strong credit ratings and liquid buffers (liquidity coverage backed by JPY reserves) and access to BOJ facilities provide a backstop that weakens supplier leverage.

- Wholesale spreads widen in stress

- Retail deposits >80% of funding in 2024

- Strong ratings + liquidity buffers reduce supplier power

- BOJ facilities serve as ultimate backstop

High supplier leverage; core replacement 2–5 years, retail funding > 80%, 65+ 29.1%

Suppliers (core IT, card networks, cloud, specialist staff, wholesale lenders) hold moderate-to-high leverage due to high switching costs, regulatory certifications and vendor concentration; core replacements cost hundreds of millions–billions yen and take 2–5 years. KFG’s group scale, >80% retail funding (2024) and BOJ access temper supplier power. Demographics (65+ ≈29.1% in 2024) tighten local labor supply.

| Metric | Value (2024) |

|---|---|

| Cashless transaction value | ¥300 trillion |

| Cashless ratio | ≈37% |

| 65+ population | 29.1% |

| Retail deposits share | >80% |

| Core replacement time | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for Kyushu Financial Group uncovering competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic levers to protect market share and profitability.

A one-sheet Porter's Five Forces summary for Kyushu Financial Group that highlights competitive pressures and regulatory risks—ideal for quick strategic decisions. Customize force intensities, swap in your data, and drop the clean radar chart straight into decks to clarify priorities for management or investors.

Customers Bargaining Power

Depositors’ rate sensitivity

Low-rate years muted depositor price sensitivity, but with global tightening (US Fed funds ~5.25–5.50% in 2024) and 10‑yr JGBs rising near 0.9% in 2024, depositor bargaining power grows as savers shift to higher‑yield time deposits, MMFs or rivals’ campaigns; easy digital rate comparison intensifies churn, while loyalty programs and bundled services help cushion outflows for Kyushu Financial Group.

SMEs and local corporates

As of 2024 SMEs account for roughly 99.7% of Japanese firms and about 70% of employment, so large local borrowers in Kyushu leverage ticket size to negotiate pricing, covenants and fees. Deep relationships and cross-sell (leasing, cards) help KFG offset rate concessions. Concentration in tourism, manufacturing and agriculture makes buyer power cyclically higher. Advisory value-add shifts negotiations away from pure price.

Retail switching frictions

Account switching costs in Japan remain non-trivial, keeping buyer power moderated despite digital trends; regional bank relationships and branch-based services still anchor many customers. Mobile onboarding and payment apps, supported by Japan’s 24/7 Zengin instant-transfer infrastructure (rolled out in 2021) and roughly 88% smartphone penetration in 2024, reduce friction and raise expectations. Customers now demand low fees, instant transfers and app UX parity with megabanks and fintechs, though loyalty to regional brands still provides some stickiness.

Public sector and institutions

Municipalities and public bodies in Kyushu are highly price sensitive and procurement-driven, forcing competitive tenders that raise buyer leverage against Kyushu Financial Group; winning treasury and payroll mandates supplies low-cost deposits but typically at slim margins. Community mission alignment and local ties often tip awards toward regional banks despite narrow spreads, preserving strategic presence in key prefectures. Regulatory mandates can periodically re-open tenders, keeping churn and margin pressure elevated.

- Procurement-driven tenders increase buyer leverage

- Treasury/payroll mandates = low-cost deposits, slim margins

- Community alignment can outweigh price in awards

- Regulatory mandates cause periodic tender churn

Fee transparency and comparability

Regulatory pushes for mandatory fee disclosure and growing cross-bank fintech aggregators make fees and service levels readily comparable, strengthening customer bargaining power and compressing spreads and non-interest income opportunities for Kyushu Financial Group. Differentiation must therefore rely on superior service quality and regional expertise to retain margins and customer loyalty.

- Disclosure-driven comparability

- Fintech aggregators increase price visibility

- Pressures on spreads/non-interest income

- Service quality and regional expertise as differentiators

Savers and SMEs raised customer bargaining power in 2024

Customer bargaining power for Kyushu Financial Group rose in 2024 as global tightening (US Fed 5.25–5.50%) and 10‑yr JGBs ≈0.9% pushed savers toward higher yields, while SMEs (≈99.7% of firms; ~70% employment) and municipalities use procurement and ticket size to extract concessions. Digital comparators, 88% smartphone penetration and Zengin instant transfers (since 2021) lower switching costs, forcing fee transparency and service differentiation.

| Metric | 2024 value |

|---|---|

| US Fed funds | 5.25–5.50% |

| 10‑yr JGB | ≈0.9% |

| SME share of firms | 99.7% |

| SME employment share | ~70% |

| Smartphone penetration | ≈88% |

Full Version Awaits

Kyushu Financial Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Kyushu Financial Group you’ll receive after purchase, covering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes. The file is fully formatted and professionally written for immediate download. No samples or placeholders—what you see is what you get instantly after payment.

Go Beyond the Preview—Access the Full Strategic Report

Kyushu Financial Group faces moderate competitive rivalry, constrained by regional banking concentration and rising fintech substitutes, while customer bargaining power grows with digital channels and low-rate sensitivity. Regulatory oversight and capital needs temper new entrants, yet supplier influence remains limited. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated core IT vendors

Japanese banks depend on a few core-banking and payment providers such as Fujitsu, NEC, NTT DATA and Hitachi, creating vendor concentration risk. Core replacements are costly, risky and time-consuming, typically taking 2–5 years and costing from several hundred million to multiple billion yen, giving suppliers leverage on pricing and roadmap. Long-term contracts and industry standards limit abrupt hikes, while group-scale across subsidiaries can modestly improve negotiation leverage.

Payment networks and card schemes

Card networks and domestic rails set fees, rules and mandatory tech upgrades, leaving Kyushu Financial Group as a price-taker on interchange and assessment charges. Co-branding with JCB/visa and higher transaction volumes can secure modest fee concessions, but bargaining leverage remains limited. Japan’s cashless transaction value exceeded ¥300 trillion in 2024 with a cashless ratio near 37%, and regulatory oversight increasingly caps fee hikes.

Data centers and cybersecurity providers

Dependence on regulated-grade hosting, cloud, and security vendors creates high switching costs for Kyushu Financial Group, embedding supplier leverage through compliance and certification requirements. Cyber resilience mandates push the bank to premium partners, further elevating supplier power. Multi-vendor strategies reduce lock-in risk but add integration complexity and operational overhead. Group scale improves negotiating leverage to secure stronger SLAs and terms.

Skilled workforce and local talent

Experienced relationship bankers, risk managers and fintech talent are scarce in Kyushu, raising supplier power of labor as Japan’s 65+ population reached about 29.1% in 2024, tightening local labor markets and lifting wage pressure for banks competing for specialists. Training pipelines and rotation across subsidiaries can lower dependence, while remote/hybrid hiring expands the talent pool but risks diluting culture and client intimacy.

Wholesale and interbank funding

In stressed markets wholesale and interbank providers tighten spreads and add covenants, raising costs and bargaining power; in 2024 KFG’s stable retail deposit base—over 80% of total funding—limits reliance on volatile wholesale channels.

Maintaining strong credit ratings and liquid buffers (liquidity coverage backed by JPY reserves) and access to BOJ facilities provide a backstop that weakens supplier leverage.

- Wholesale spreads widen in stress

- Retail deposits >80% of funding in 2024

- Strong ratings + liquidity buffers reduce supplier power

- BOJ facilities serve as ultimate backstop

High supplier leverage; core replacement 2–5 years, retail funding > 80%, 65+ 29.1%

Suppliers (core IT, card networks, cloud, specialist staff, wholesale lenders) hold moderate-to-high leverage due to high switching costs, regulatory certifications and vendor concentration; core replacements cost hundreds of millions–billions yen and take 2–5 years. KFG’s group scale, >80% retail funding (2024) and BOJ access temper supplier power. Demographics (65+ ≈29.1% in 2024) tighten local labor supply.

| Metric | Value (2024) |

|---|---|

| Cashless transaction value | ¥300 trillion |

| Cashless ratio | ≈37% |

| 65+ population | 29.1% |

| Retail deposits share | >80% |

| Core replacement time | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for Kyushu Financial Group uncovering competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic levers to protect market share and profitability.

A one-sheet Porter's Five Forces summary for Kyushu Financial Group that highlights competitive pressures and regulatory risks—ideal for quick strategic decisions. Customize force intensities, swap in your data, and drop the clean radar chart straight into decks to clarify priorities for management or investors.

Customers Bargaining Power

Depositors’ rate sensitivity

Low-rate years muted depositor price sensitivity, but with global tightening (US Fed funds ~5.25–5.50% in 2024) and 10‑yr JGBs rising near 0.9% in 2024, depositor bargaining power grows as savers shift to higher‑yield time deposits, MMFs or rivals’ campaigns; easy digital rate comparison intensifies churn, while loyalty programs and bundled services help cushion outflows for Kyushu Financial Group.

SMEs and local corporates

As of 2024 SMEs account for roughly 99.7% of Japanese firms and about 70% of employment, so large local borrowers in Kyushu leverage ticket size to negotiate pricing, covenants and fees. Deep relationships and cross-sell (leasing, cards) help KFG offset rate concessions. Concentration in tourism, manufacturing and agriculture makes buyer power cyclically higher. Advisory value-add shifts negotiations away from pure price.

Retail switching frictions

Account switching costs in Japan remain non-trivial, keeping buyer power moderated despite digital trends; regional bank relationships and branch-based services still anchor many customers. Mobile onboarding and payment apps, supported by Japan’s 24/7 Zengin instant-transfer infrastructure (rolled out in 2021) and roughly 88% smartphone penetration in 2024, reduce friction and raise expectations. Customers now demand low fees, instant transfers and app UX parity with megabanks and fintechs, though loyalty to regional brands still provides some stickiness.

Public sector and institutions

Municipalities and public bodies in Kyushu are highly price sensitive and procurement-driven, forcing competitive tenders that raise buyer leverage against Kyushu Financial Group; winning treasury and payroll mandates supplies low-cost deposits but typically at slim margins. Community mission alignment and local ties often tip awards toward regional banks despite narrow spreads, preserving strategic presence in key prefectures. Regulatory mandates can periodically re-open tenders, keeping churn and margin pressure elevated.

- Procurement-driven tenders increase buyer leverage

- Treasury/payroll mandates = low-cost deposits, slim margins

- Community alignment can outweigh price in awards

- Regulatory mandates cause periodic tender churn

Fee transparency and comparability

Regulatory pushes for mandatory fee disclosure and growing cross-bank fintech aggregators make fees and service levels readily comparable, strengthening customer bargaining power and compressing spreads and non-interest income opportunities for Kyushu Financial Group. Differentiation must therefore rely on superior service quality and regional expertise to retain margins and customer loyalty.

- Disclosure-driven comparability

- Fintech aggregators increase price visibility

- Pressures on spreads/non-interest income

- Service quality and regional expertise as differentiators

Savers and SMEs raised customer bargaining power in 2024

Customer bargaining power for Kyushu Financial Group rose in 2024 as global tightening (US Fed 5.25–5.50%) and 10‑yr JGBs ≈0.9% pushed savers toward higher yields, while SMEs (≈99.7% of firms; ~70% employment) and municipalities use procurement and ticket size to extract concessions. Digital comparators, 88% smartphone penetration and Zengin instant transfers (since 2021) lower switching costs, forcing fee transparency and service differentiation.

| Metric | 2024 value |

|---|---|

| US Fed funds | 5.25–5.50% |

| 10‑yr JGB | ≈0.9% |

| SME share of firms | 99.7% |

| SME employment share | ~70% |

| Smartphone penetration | ≈88% |

Full Version Awaits

Kyushu Financial Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Kyushu Financial Group you’ll receive after purchase, covering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes. The file is fully formatted and professionally written for immediate download. No samples or placeholders—what you see is what you get instantly after payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Kyushu Financial Group faces moderate competitive rivalry, constrained by regional banking concentration and rising fintech substitutes, while customer bargaining power grows with digital channels and low-rate sensitivity. Regulatory oversight and capital needs temper new entrants, yet supplier influence remains limited. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Concentrated core IT vendors

Japanese banks depend on a few core-banking and payment providers such as Fujitsu, NEC, NTT DATA and Hitachi, creating vendor concentration risk. Core replacements are costly, risky and time-consuming, typically taking 2–5 years and costing from several hundred million to multiple billion yen, giving suppliers leverage on pricing and roadmap. Long-term contracts and industry standards limit abrupt hikes, while group-scale across subsidiaries can modestly improve negotiation leverage.

Payment networks and card schemes

Card networks and domestic rails set fees, rules and mandatory tech upgrades, leaving Kyushu Financial Group as a price-taker on interchange and assessment charges. Co-branding with JCB/visa and higher transaction volumes can secure modest fee concessions, but bargaining leverage remains limited. Japan’s cashless transaction value exceeded ¥300 trillion in 2024 with a cashless ratio near 37%, and regulatory oversight increasingly caps fee hikes.

Data centers and cybersecurity providers

Dependence on regulated-grade hosting, cloud, and security vendors creates high switching costs for Kyushu Financial Group, embedding supplier leverage through compliance and certification requirements. Cyber resilience mandates push the bank to premium partners, further elevating supplier power. Multi-vendor strategies reduce lock-in risk but add integration complexity and operational overhead. Group scale improves negotiating leverage to secure stronger SLAs and terms.

Skilled workforce and local talent

Experienced relationship bankers, risk managers and fintech talent are scarce in Kyushu, raising supplier power of labor as Japan’s 65+ population reached about 29.1% in 2024, tightening local labor markets and lifting wage pressure for banks competing for specialists. Training pipelines and rotation across subsidiaries can lower dependence, while remote/hybrid hiring expands the talent pool but risks diluting culture and client intimacy.

Wholesale and interbank funding

In stressed markets wholesale and interbank providers tighten spreads and add covenants, raising costs and bargaining power; in 2024 KFG’s stable retail deposit base—over 80% of total funding—limits reliance on volatile wholesale channels.

Maintaining strong credit ratings and liquid buffers (liquidity coverage backed by JPY reserves) and access to BOJ facilities provide a backstop that weakens supplier leverage.

- Wholesale spreads widen in stress

- Retail deposits >80% of funding in 2024

- Strong ratings + liquidity buffers reduce supplier power

- BOJ facilities serve as ultimate backstop

High supplier leverage; core replacement 2–5 years, retail funding > 80%, 65+ 29.1%

Suppliers (core IT, card networks, cloud, specialist staff, wholesale lenders) hold moderate-to-high leverage due to high switching costs, regulatory certifications and vendor concentration; core replacements cost hundreds of millions–billions yen and take 2–5 years. KFG’s group scale, >80% retail funding (2024) and BOJ access temper supplier power. Demographics (65+ ≈29.1% in 2024) tighten local labor supply.

| Metric | Value (2024) |

|---|---|

| Cashless transaction value | ¥300 trillion |

| Cashless ratio | ≈37% |

| 65+ population | 29.1% |

| Retail deposits share | >80% |

| Core replacement time | 2–5 years |

What is included in the product

Tailored Porter's Five Forces analysis for Kyushu Financial Group uncovering competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and strategic levers to protect market share and profitability.

A one-sheet Porter's Five Forces summary for Kyushu Financial Group that highlights competitive pressures and regulatory risks—ideal for quick strategic decisions. Customize force intensities, swap in your data, and drop the clean radar chart straight into decks to clarify priorities for management or investors.

Customers Bargaining Power

Depositors’ rate sensitivity

Low-rate years muted depositor price sensitivity, but with global tightening (US Fed funds ~5.25–5.50% in 2024) and 10‑yr JGBs rising near 0.9% in 2024, depositor bargaining power grows as savers shift to higher‑yield time deposits, MMFs or rivals’ campaigns; easy digital rate comparison intensifies churn, while loyalty programs and bundled services help cushion outflows for Kyushu Financial Group.

SMEs and local corporates

As of 2024 SMEs account for roughly 99.7% of Japanese firms and about 70% of employment, so large local borrowers in Kyushu leverage ticket size to negotiate pricing, covenants and fees. Deep relationships and cross-sell (leasing, cards) help KFG offset rate concessions. Concentration in tourism, manufacturing and agriculture makes buyer power cyclically higher. Advisory value-add shifts negotiations away from pure price.

Retail switching frictions

Account switching costs in Japan remain non-trivial, keeping buyer power moderated despite digital trends; regional bank relationships and branch-based services still anchor many customers. Mobile onboarding and payment apps, supported by Japan’s 24/7 Zengin instant-transfer infrastructure (rolled out in 2021) and roughly 88% smartphone penetration in 2024, reduce friction and raise expectations. Customers now demand low fees, instant transfers and app UX parity with megabanks and fintechs, though loyalty to regional brands still provides some stickiness.

Public sector and institutions

Municipalities and public bodies in Kyushu are highly price sensitive and procurement-driven, forcing competitive tenders that raise buyer leverage against Kyushu Financial Group; winning treasury and payroll mandates supplies low-cost deposits but typically at slim margins. Community mission alignment and local ties often tip awards toward regional banks despite narrow spreads, preserving strategic presence in key prefectures. Regulatory mandates can periodically re-open tenders, keeping churn and margin pressure elevated.

- Procurement-driven tenders increase buyer leverage

- Treasury/payroll mandates = low-cost deposits, slim margins

- Community alignment can outweigh price in awards

- Regulatory mandates cause periodic tender churn

Fee transparency and comparability

Regulatory pushes for mandatory fee disclosure and growing cross-bank fintech aggregators make fees and service levels readily comparable, strengthening customer bargaining power and compressing spreads and non-interest income opportunities for Kyushu Financial Group. Differentiation must therefore rely on superior service quality and regional expertise to retain margins and customer loyalty.

- Disclosure-driven comparability

- Fintech aggregators increase price visibility

- Pressures on spreads/non-interest income

- Service quality and regional expertise as differentiators

Savers and SMEs raised customer bargaining power in 2024

Customer bargaining power for Kyushu Financial Group rose in 2024 as global tightening (US Fed 5.25–5.50%) and 10‑yr JGBs ≈0.9% pushed savers toward higher yields, while SMEs (≈99.7% of firms; ~70% employment) and municipalities use procurement and ticket size to extract concessions. Digital comparators, 88% smartphone penetration and Zengin instant transfers (since 2021) lower switching costs, forcing fee transparency and service differentiation.

| Metric | 2024 value |

|---|---|

| US Fed funds | 5.25–5.50% |

| 10‑yr JGB | ≈0.9% |

| SME share of firms | 99.7% |

| SME employment share | ~70% |

| Smartphone penetration | ≈88% |

Full Version Awaits

Kyushu Financial Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Kyushu Financial Group you’ll receive after purchase, covering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes. The file is fully formatted and professionally written for immediate download. No samples or placeholders—what you see is what you get instantly after payment.