La-Z-Boy PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

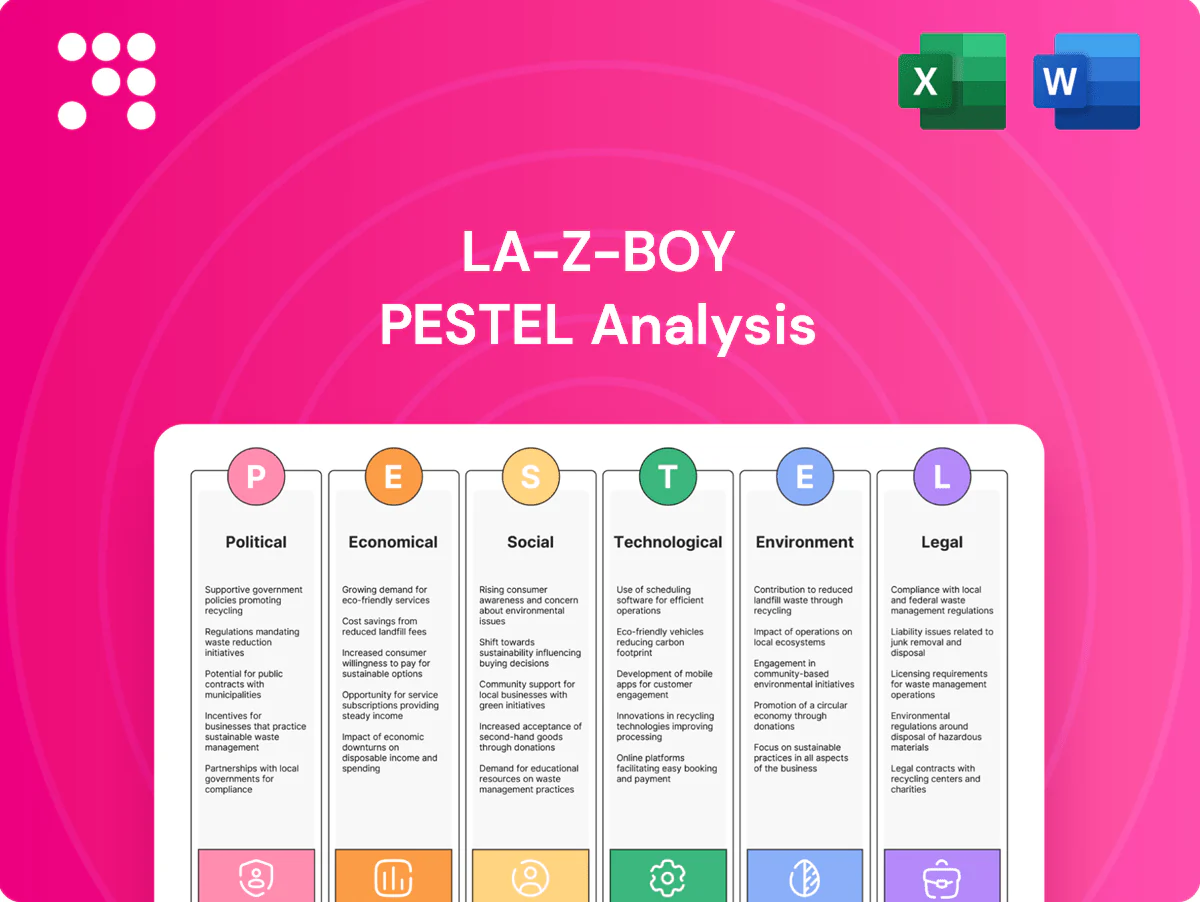

Unlock strategic clarity with our concise PESTLE Analysis of La-Z-Boy—three to five expert-level insights reveal how political, economic, social, technological, legal, and environmental forces are reshaping the furniture leader’s prospects. Use these findings to refine forecasts and competitive moves. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

Trade policy and tariffs on furniture inputs

U.S. Section 301 tariffs on many Chinese imports remain as high as 25%, raising input costs for components, fabrics and finished furniture; antidumping duties on wooden casegoods and upholstery have in specific cases exceeded 100%, materially changing sourcing economics. La-Z-Boy has signaled supplier rebalancing and nearshoring to reduce tariff exposure, which can compress or expand wholesale price lists and margins depending on duty changes.

Buy American and reshoring incentives

Industrial policy such as the Build America, Buy America Act and the Inflation Reduction Act’s manufacturing incentives increase procurement preference and tax-credit support for domestic production, creating potential tailwinds for La-Z-Boy’s U.S. plants.

Targeted tax credits, grants and state reshoring programs reduce effective capex and can support job creation, while expanded federal procurement preferences steer orders toward domestic suppliers.

These benefits are offset by added compliance and reporting requirements that raise administrative costs; the net impact for La-Z-Boy depends on whether incentive receipts materially exceed incremental capex and labor expenses.

Labor and immigration policy

Policies shaping skilled trades availability constrain upholstery, foam, and woodworking labor pools critical to La-Z-Boy, with federal minimum wage unchanged at $7.25 and state floors like California at $16/hr raising regional unit labor cost. Immigration constraints in 2024–25 tightened manufacturing labor in key hubs, pushing recruitment costs up. Federal workforce programs (WIOA funding ~ $3.6B) and state training subsidies can partially offset shortages.

Geopolitical supply-chain risk

Geopolitical conflicts and sanctions since 2022 have intermittently disrupted textiles, metal mechanisms and chemical inputs, pushing some component lead times from 8–12 weeks to 16+ weeks as of 2024.

Ocean freight volatility—container rates surged over 100% in 2021–22 before easing by 2024—and war-risk insurance premiums spiked regionally, prompting La-Z-Boy to dual-source critical SKUs and diversify ports.

- Diversify ports

- Dual-source critical SKUs

- Strategic inventory buffers

- Plan for 16+ week lead times

State and local incentives/zoning

State and local zoning, permitting, and tax abatements directly affect La-Z-Boy plant expansions and can cut capital costs; La-Z-Boy reported roughly $1.8B revenue in FY2024, making site incentives material to margins. Municipal approvals and signage rules shape Retail Gallery rollouts and store format timing. Competition among states for incentives can lower net operating costs but permit delays (commonly 30–90 days) push Galleries openings and time-to-revenue.

- Plant expansions: zoning, permits, abatements

- Retail rollouts: municipal approvals, signage

- Incentive competition lowers costs

- Permitting delays increase time-to-revenue

Tariffs 25%, lead times > 16w raise costs, dual-source

Tariffs (Section 301 up to 25%, some antidumping >100%) and 2024–25 geopolitical shocks extended component lead times to 16+ weeks, raising input costs. Build America/IRA incentives and state abatements favor domestic sourcing—La‑Z‑Boy revenue ~$1.8B FY2024—offset by higher compliance and regional wages (federal $7.25, CA $16/hr). Ocean freight volatility and insurance spikes drove dual‑sourcing and inventory buffers.

| Factor | Metric | 2024–25 Data | Impact |

|---|---|---|---|

| Tariffs | Section 301/AD | 25%/>100% | Higher COGS |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect La‑Z‑Boy, with data‑backed, regionally relevant insights, detailed subpoints and forward‑looking scenarios to support executives, investors and strategists in spotting risks, opportunities and actionable responses.

Concise, visually segmented La-Z-Boy PESTLE summary that can be dropped into presentations, edited for regional or business-line nuances, and easily shared to align teams quickly during strategic or risk discussions.

Economic factors

Housing cycle and consumer sentiment

New and existing home activity drives furniture refreshes: U.S. new single-family starts ran near 1.1 million annualized in 2024 and existing-home sales were roughly 4.2 million, supporting demand for upholstery. Weak consumer sentiment or declining home sales dampens discretionary spend on higher-ticket La-Z-Boy offerings. Strong remodel activity—U.S. remodeling market near $450 billion in 2024—partially offsets lower move-related purchases, but La-Z-Boy’s mid-premium positioning remains sensitive to confidence swings.

Interest rates and credit availability

Higher interest rates raise financing costs for consumers and for La-Z-Boy, tightening discretionary spending and increasing corporate borrowing costs; the federal funds target was 5.25–5.50% in mid-2024. Promotional financing approval rates in Galleries materially influence conversion and AURs, while tighter credit elevates inventory carrying and capex costs. Rate cuts typically boost showroom traffic and order flow, improving conversion and margin recovery.

Input costs: foam, lumber, fabric, freight

Petrochemical foam and fabric costs are cyclical and tied to oil; Brent averaged about $86/bbl in 2024, keeping polyurethane feedstock volatile. Lumber and plywood — Random Lengths lumber index near $500/mbf in 2024 — directly affect casegoods and frame costs. Freight and parcel rates, with the Drewry WCI falling to roughly $1,500/40ft in 2024, materially squeeze wholesale-to-retail margins. Pricing power and contractual surcharges remain essential to defend margins.

Labor market and wages

Tight U.S. labor markets (around 3.5–4.0% unemployment, BLS 2024–25) have pushed manufacturing and retail wages higher, increasing La-Z-Boy’s wage-driven SG&A and COGS pressure. Expanded training and retention programs improve throughput and product quality, reducing turnover-related costs. Over time productivity gains and targeted automation investments can materially offset wage inflation.

- Labor tightness: U.S. unemployment ~3.5–4.0% (BLS 2024–25)

- Impact: upward pressure on SG&A and COGS

- Mitigation: training/retention stabilizes output

- Offset: productivity and automation investments

Currency fluctuations

Currency fluctuations materially affect La-Z-Boy: a stronger US dollar lowers domestic costs for imported upholstery and component inputs but can compress reported international revenue when translated back to dollars; the ICE U.S. Dollar Index rose roughly 4% in 2024, intensifying these effects. La-Z-Boy’s corporate hedging policies are used to dampen short-term FX volatility, while sustained FX moves can prompt shifts in sourcing toward lower-cost regions.

- FX impact: imported input cost down / translated overseas revenue down

- ICE DXY ~+4% in 2024

- Hedging: corporate policy used to reduce volatility

- Sourcing: likely shift if FX trends persist

Tariffs 25%, lead times > 16w raise costs, dual-source

Housing activity (1.1M starts; 4.2M existing sales) and a ~$450B remodel market sustain upholstery demand but remain confidence-sensitive. Fed funds 5.25–5.50% in mid‑2024 tightened consumer financing and corporate costs; rate cuts boost traffic. Input inflation: Brent ~$86/bbl, lumber ~$500/mbf, Drewry WCI ~$1,500/40ft. Unemployment ~3.5–4.0% raises wage pressure; ICE DXY +4% affects sourcing and translation.

| Metric | 2024 Value |

|---|---|

| Single‑family starts | 1.1M |

| Existing sales | 4.2M |

| Remodel market | $450B |

| Fed funds | 5.25–5.50% |

| Brent | $86/bbl |

| Lumber | $500/mbf |

| Drewry WCI | $1,500/40ft |

| Unemployment | 3.5–4.0% |

| ICE DXY | +4% |

Preview the Actual Deliverable

La-Z-Boy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This La-Z-Boy PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the company and industry. No placeholders or teasers; the file is the complete, professionally structured report you’ll download immediately after payment.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of La-Z-Boy—three to five expert-level insights reveal how political, economic, social, technological, legal, and environmental forces are reshaping the furniture leader’s prospects. Use these findings to refine forecasts and competitive moves. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

Trade policy and tariffs on furniture inputs

U.S. Section 301 tariffs on many Chinese imports remain as high as 25%, raising input costs for components, fabrics and finished furniture; antidumping duties on wooden casegoods and upholstery have in specific cases exceeded 100%, materially changing sourcing economics. La-Z-Boy has signaled supplier rebalancing and nearshoring to reduce tariff exposure, which can compress or expand wholesale price lists and margins depending on duty changes.

Buy American and reshoring incentives

Industrial policy such as the Build America, Buy America Act and the Inflation Reduction Act’s manufacturing incentives increase procurement preference and tax-credit support for domestic production, creating potential tailwinds for La-Z-Boy’s U.S. plants.

Targeted tax credits, grants and state reshoring programs reduce effective capex and can support job creation, while expanded federal procurement preferences steer orders toward domestic suppliers.

These benefits are offset by added compliance and reporting requirements that raise administrative costs; the net impact for La-Z-Boy depends on whether incentive receipts materially exceed incremental capex and labor expenses.

Labor and immigration policy

Policies shaping skilled trades availability constrain upholstery, foam, and woodworking labor pools critical to La-Z-Boy, with federal minimum wage unchanged at $7.25 and state floors like California at $16/hr raising regional unit labor cost. Immigration constraints in 2024–25 tightened manufacturing labor in key hubs, pushing recruitment costs up. Federal workforce programs (WIOA funding ~ $3.6B) and state training subsidies can partially offset shortages.

Geopolitical supply-chain risk

Geopolitical conflicts and sanctions since 2022 have intermittently disrupted textiles, metal mechanisms and chemical inputs, pushing some component lead times from 8–12 weeks to 16+ weeks as of 2024.

Ocean freight volatility—container rates surged over 100% in 2021–22 before easing by 2024—and war-risk insurance premiums spiked regionally, prompting La-Z-Boy to dual-source critical SKUs and diversify ports.

- Diversify ports

- Dual-source critical SKUs

- Strategic inventory buffers

- Plan for 16+ week lead times

State and local incentives/zoning

State and local zoning, permitting, and tax abatements directly affect La-Z-Boy plant expansions and can cut capital costs; La-Z-Boy reported roughly $1.8B revenue in FY2024, making site incentives material to margins. Municipal approvals and signage rules shape Retail Gallery rollouts and store format timing. Competition among states for incentives can lower net operating costs but permit delays (commonly 30–90 days) push Galleries openings and time-to-revenue.

- Plant expansions: zoning, permits, abatements

- Retail rollouts: municipal approvals, signage

- Incentive competition lowers costs

- Permitting delays increase time-to-revenue

Tariffs 25%, lead times > 16w raise costs, dual-source

Tariffs (Section 301 up to 25%, some antidumping >100%) and 2024–25 geopolitical shocks extended component lead times to 16+ weeks, raising input costs. Build America/IRA incentives and state abatements favor domestic sourcing—La‑Z‑Boy revenue ~$1.8B FY2024—offset by higher compliance and regional wages (federal $7.25, CA $16/hr). Ocean freight volatility and insurance spikes drove dual‑sourcing and inventory buffers.

| Factor | Metric | 2024–25 Data | Impact |

|---|---|---|---|

| Tariffs | Section 301/AD | 25%/>100% | Higher COGS |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect La‑Z‑Boy, with data‑backed, regionally relevant insights, detailed subpoints and forward‑looking scenarios to support executives, investors and strategists in spotting risks, opportunities and actionable responses.

Concise, visually segmented La-Z-Boy PESTLE summary that can be dropped into presentations, edited for regional or business-line nuances, and easily shared to align teams quickly during strategic or risk discussions.

Economic factors

Housing cycle and consumer sentiment

New and existing home activity drives furniture refreshes: U.S. new single-family starts ran near 1.1 million annualized in 2024 and existing-home sales were roughly 4.2 million, supporting demand for upholstery. Weak consumer sentiment or declining home sales dampens discretionary spend on higher-ticket La-Z-Boy offerings. Strong remodel activity—U.S. remodeling market near $450 billion in 2024—partially offsets lower move-related purchases, but La-Z-Boy’s mid-premium positioning remains sensitive to confidence swings.

Interest rates and credit availability

Higher interest rates raise financing costs for consumers and for La-Z-Boy, tightening discretionary spending and increasing corporate borrowing costs; the federal funds target was 5.25–5.50% in mid-2024. Promotional financing approval rates in Galleries materially influence conversion and AURs, while tighter credit elevates inventory carrying and capex costs. Rate cuts typically boost showroom traffic and order flow, improving conversion and margin recovery.

Input costs: foam, lumber, fabric, freight

Petrochemical foam and fabric costs are cyclical and tied to oil; Brent averaged about $86/bbl in 2024, keeping polyurethane feedstock volatile. Lumber and plywood — Random Lengths lumber index near $500/mbf in 2024 — directly affect casegoods and frame costs. Freight and parcel rates, with the Drewry WCI falling to roughly $1,500/40ft in 2024, materially squeeze wholesale-to-retail margins. Pricing power and contractual surcharges remain essential to defend margins.

Labor market and wages

Tight U.S. labor markets (around 3.5–4.0% unemployment, BLS 2024–25) have pushed manufacturing and retail wages higher, increasing La-Z-Boy’s wage-driven SG&A and COGS pressure. Expanded training and retention programs improve throughput and product quality, reducing turnover-related costs. Over time productivity gains and targeted automation investments can materially offset wage inflation.

- Labor tightness: U.S. unemployment ~3.5–4.0% (BLS 2024–25)

- Impact: upward pressure on SG&A and COGS

- Mitigation: training/retention stabilizes output

- Offset: productivity and automation investments

Currency fluctuations

Currency fluctuations materially affect La-Z-Boy: a stronger US dollar lowers domestic costs for imported upholstery and component inputs but can compress reported international revenue when translated back to dollars; the ICE U.S. Dollar Index rose roughly 4% in 2024, intensifying these effects. La-Z-Boy’s corporate hedging policies are used to dampen short-term FX volatility, while sustained FX moves can prompt shifts in sourcing toward lower-cost regions.

- FX impact: imported input cost down / translated overseas revenue down

- ICE DXY ~+4% in 2024

- Hedging: corporate policy used to reduce volatility

- Sourcing: likely shift if FX trends persist

Tariffs 25%, lead times > 16w raise costs, dual-source

Housing activity (1.1M starts; 4.2M existing sales) and a ~$450B remodel market sustain upholstery demand but remain confidence-sensitive. Fed funds 5.25–5.50% in mid‑2024 tightened consumer financing and corporate costs; rate cuts boost traffic. Input inflation: Brent ~$86/bbl, lumber ~$500/mbf, Drewry WCI ~$1,500/40ft. Unemployment ~3.5–4.0% raises wage pressure; ICE DXY +4% affects sourcing and translation.

| Metric | 2024 Value |

|---|---|

| Single‑family starts | 1.1M |

| Existing sales | 4.2M |

| Remodel market | $450B |

| Fed funds | 5.25–5.50% |

| Brent | $86/bbl |

| Lumber | $500/mbf |

| Drewry WCI | $1,500/40ft |

| Unemployment | 3.5–4.0% |

| ICE DXY | +4% |

Preview the Actual Deliverable

La-Z-Boy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This La-Z-Boy PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the company and industry. No placeholders or teasers; the file is the complete, professionally structured report you’ll download immediately after payment.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of La-Z-Boy—three to five expert-level insights reveal how political, economic, social, technological, legal, and environmental forces are reshaping the furniture leader’s prospects. Use these findings to refine forecasts and competitive moves. Purchase the full report to access the complete, actionable breakdown instantly.

Political factors

Trade policy and tariffs on furniture inputs

U.S. Section 301 tariffs on many Chinese imports remain as high as 25%, raising input costs for components, fabrics and finished furniture; antidumping duties on wooden casegoods and upholstery have in specific cases exceeded 100%, materially changing sourcing economics. La-Z-Boy has signaled supplier rebalancing and nearshoring to reduce tariff exposure, which can compress or expand wholesale price lists and margins depending on duty changes.

Buy American and reshoring incentives

Industrial policy such as the Build America, Buy America Act and the Inflation Reduction Act’s manufacturing incentives increase procurement preference and tax-credit support for domestic production, creating potential tailwinds for La-Z-Boy’s U.S. plants.

Targeted tax credits, grants and state reshoring programs reduce effective capex and can support job creation, while expanded federal procurement preferences steer orders toward domestic suppliers.

These benefits are offset by added compliance and reporting requirements that raise administrative costs; the net impact for La-Z-Boy depends on whether incentive receipts materially exceed incremental capex and labor expenses.

Labor and immigration policy

Policies shaping skilled trades availability constrain upholstery, foam, and woodworking labor pools critical to La-Z-Boy, with federal minimum wage unchanged at $7.25 and state floors like California at $16/hr raising regional unit labor cost. Immigration constraints in 2024–25 tightened manufacturing labor in key hubs, pushing recruitment costs up. Federal workforce programs (WIOA funding ~ $3.6B) and state training subsidies can partially offset shortages.

Geopolitical supply-chain risk

Geopolitical conflicts and sanctions since 2022 have intermittently disrupted textiles, metal mechanisms and chemical inputs, pushing some component lead times from 8–12 weeks to 16+ weeks as of 2024.

Ocean freight volatility—container rates surged over 100% in 2021–22 before easing by 2024—and war-risk insurance premiums spiked regionally, prompting La-Z-Boy to dual-source critical SKUs and diversify ports.

- Diversify ports

- Dual-source critical SKUs

- Strategic inventory buffers

- Plan for 16+ week lead times

State and local incentives/zoning

State and local zoning, permitting, and tax abatements directly affect La-Z-Boy plant expansions and can cut capital costs; La-Z-Boy reported roughly $1.8B revenue in FY2024, making site incentives material to margins. Municipal approvals and signage rules shape Retail Gallery rollouts and store format timing. Competition among states for incentives can lower net operating costs but permit delays (commonly 30–90 days) push Galleries openings and time-to-revenue.

- Plant expansions: zoning, permits, abatements

- Retail rollouts: municipal approvals, signage

- Incentive competition lowers costs

- Permitting delays increase time-to-revenue

Tariffs 25%, lead times > 16w raise costs, dual-source

Tariffs (Section 301 up to 25%, some antidumping >100%) and 2024–25 geopolitical shocks extended component lead times to 16+ weeks, raising input costs. Build America/IRA incentives and state abatements favor domestic sourcing—La‑Z‑Boy revenue ~$1.8B FY2024—offset by higher compliance and regional wages (federal $7.25, CA $16/hr). Ocean freight volatility and insurance spikes drove dual‑sourcing and inventory buffers.

| Factor | Metric | 2024–25 Data | Impact |

|---|---|---|---|

| Tariffs | Section 301/AD | 25%/>100% | Higher COGS |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect La‑Z‑Boy, with data‑backed, regionally relevant insights, detailed subpoints and forward‑looking scenarios to support executives, investors and strategists in spotting risks, opportunities and actionable responses.

Concise, visually segmented La-Z-Boy PESTLE summary that can be dropped into presentations, edited for regional or business-line nuances, and easily shared to align teams quickly during strategic or risk discussions.

Economic factors

Housing cycle and consumer sentiment

New and existing home activity drives furniture refreshes: U.S. new single-family starts ran near 1.1 million annualized in 2024 and existing-home sales were roughly 4.2 million, supporting demand for upholstery. Weak consumer sentiment or declining home sales dampens discretionary spend on higher-ticket La-Z-Boy offerings. Strong remodel activity—U.S. remodeling market near $450 billion in 2024—partially offsets lower move-related purchases, but La-Z-Boy’s mid-premium positioning remains sensitive to confidence swings.

Interest rates and credit availability

Higher interest rates raise financing costs for consumers and for La-Z-Boy, tightening discretionary spending and increasing corporate borrowing costs; the federal funds target was 5.25–5.50% in mid-2024. Promotional financing approval rates in Galleries materially influence conversion and AURs, while tighter credit elevates inventory carrying and capex costs. Rate cuts typically boost showroom traffic and order flow, improving conversion and margin recovery.

Input costs: foam, lumber, fabric, freight

Petrochemical foam and fabric costs are cyclical and tied to oil; Brent averaged about $86/bbl in 2024, keeping polyurethane feedstock volatile. Lumber and plywood — Random Lengths lumber index near $500/mbf in 2024 — directly affect casegoods and frame costs. Freight and parcel rates, with the Drewry WCI falling to roughly $1,500/40ft in 2024, materially squeeze wholesale-to-retail margins. Pricing power and contractual surcharges remain essential to defend margins.

Labor market and wages

Tight U.S. labor markets (around 3.5–4.0% unemployment, BLS 2024–25) have pushed manufacturing and retail wages higher, increasing La-Z-Boy’s wage-driven SG&A and COGS pressure. Expanded training and retention programs improve throughput and product quality, reducing turnover-related costs. Over time productivity gains and targeted automation investments can materially offset wage inflation.

- Labor tightness: U.S. unemployment ~3.5–4.0% (BLS 2024–25)

- Impact: upward pressure on SG&A and COGS

- Mitigation: training/retention stabilizes output

- Offset: productivity and automation investments

Currency fluctuations

Currency fluctuations materially affect La-Z-Boy: a stronger US dollar lowers domestic costs for imported upholstery and component inputs but can compress reported international revenue when translated back to dollars; the ICE U.S. Dollar Index rose roughly 4% in 2024, intensifying these effects. La-Z-Boy’s corporate hedging policies are used to dampen short-term FX volatility, while sustained FX moves can prompt shifts in sourcing toward lower-cost regions.

- FX impact: imported input cost down / translated overseas revenue down

- ICE DXY ~+4% in 2024

- Hedging: corporate policy used to reduce volatility

- Sourcing: likely shift if FX trends persist

Tariffs 25%, lead times > 16w raise costs, dual-source

Housing activity (1.1M starts; 4.2M existing sales) and a ~$450B remodel market sustain upholstery demand but remain confidence-sensitive. Fed funds 5.25–5.50% in mid‑2024 tightened consumer financing and corporate costs; rate cuts boost traffic. Input inflation: Brent ~$86/bbl, lumber ~$500/mbf, Drewry WCI ~$1,500/40ft. Unemployment ~3.5–4.0% raises wage pressure; ICE DXY +4% affects sourcing and translation.

| Metric | 2024 Value |

|---|---|

| Single‑family starts | 1.1M |

| Existing sales | 4.2M |

| Remodel market | $450B |

| Fed funds | 5.25–5.50% |

| Brent | $86/bbl |

| Lumber | $500/mbf |

| Drewry WCI | $1,500/40ft |

| Unemployment | 3.5–4.0% |

| ICE DXY | +4% |

Preview the Actual Deliverable

La-Z-Boy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This La-Z-Boy PESTLE Analysis examines political, economic, social, technological, legal and environmental factors affecting the company and industry. No placeholders or teasers; the file is the complete, professionally structured report you’ll download immediately after payment.