Labcorp PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressure, and rapid tech advances are reshaping Labcorp’s strategic outlook in this concise PESTLE snapshot. Our full analysis delivers the detailed risks and opportunities behind these trends, refined for investors and strategists. Purchase the complete report to access actionable insights and ready-to-use recommendations.

Political factors

Healthcare policy and reimbursement

Government healthcare priorities shape coverage and test utilization, with Medicare covering about 66 million and Medicaid/CHIP roughly 82 million beneficiaries in 2024, directly influencing Labcorp volumes. Shifts in Medicare/Medicaid reimbursement rules can materially alter pricing and throughput. Policy moves toward value-based care favor diagnostics that show clear clinical utility and cost-effectiveness. Labcorp must align test menus and evidence dossiers with evolving payer expectations.

Public health funding and preparedness

National and local public health budgets directly drive demand for infectious disease testing and surveillance, influencing Labcorp’s contracted testing volumes and reimbursement rates. Emergency funding during outbreaks has historically produced rapid volume spikes and capacity strain, then post-crisis normalization creates revenue volatility for lab operators. Strategic partnerships with federal and state health agencies improve pipeline visibility and can stabilize demand through multi-year contracts and preparedness programs.

Global regulatory harmonization

Differences between U.S. and EU review clocks—FDA PDUFA ~10 months versus EMA centralized review 210 days—plus divergent emerging-market rules extend trial timelines and complicate Labcorp’s lab operations. Harmonization efforts can lower compliance burden but require proactive alignment of global SOPs and IT systems. Active participation in ICH and regional standard-setting helps shape favorable pathways as fragmentation raises costs and delays market entry.

Geopolitical risk and supply chains

Tariffs, sanctions, and export controls can disrupt flows of reagents and instrumentation to Labcorp, raising procurement costs and causing substitution or retrofit needs. Political instability along transit corridors increases logistics costs and lead times for lab supplies and trial materials. Dual-sourcing, regional inventory buffers, and nearshoring have been adopted to mitigate exposure, while cross-border data restrictions complicate global trial data sharing and compliance.

- Tariffs/sanctions: disrupt reagent and instrument imports

- Logistics: instability increases costs and lead times

- Mitigation: dual-sourcing and regional buffers

- Data: cross-border restrictions complicate trial management

Government pricing pressure

Government payers, led by Medicare and Medicaid, negotiate aggressively and their fee schedules effectively anchor many commercial lab rates, pressuring Labcorp margins.

Price-transparency rules (CMS hospital rule in force since 2021) and 2024 enforcement trends are compressing negotiated spreads; reference pricing in markets like the UK/EU can echo into multinational contracts.

Political emphasis on outcomes means Labcorp must demonstrate cost-offsets with real-world evidence to protect reimbursement and secure value-based deals.

- Public payers anchor commercial rates

- Transparency rules tighten margins (heightened enforcement 2024)

- Reference pricing abroad impacts multinational contracts

- Outcomes data critical for value-based reimbursement

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Government payers (Medicare ~66M, Medicaid/CHIP ~82M in 2024) anchor pricing and drive volumes; 2024 enforcement of CMS price-transparency compresses spreads. Regulatory divergence (FDA PDUFA ~10 months vs EMA 210 days) and trade controls raise time-to-market and reagent costs. Labcorp mitigates via dual-sourcing, regional buffers and value-evidence for payers.

| Metric | 2024/2025 |

|---|---|

| Medicare beneficiaries | ~66M (2024) |

| Medicaid/CHIP | ~82M (2024) |

| FDA vs EMA review | PDUFA ~10 mo / EMA 210 days |

| CMS enforcement | Heightened (2024) |

What is included in the product

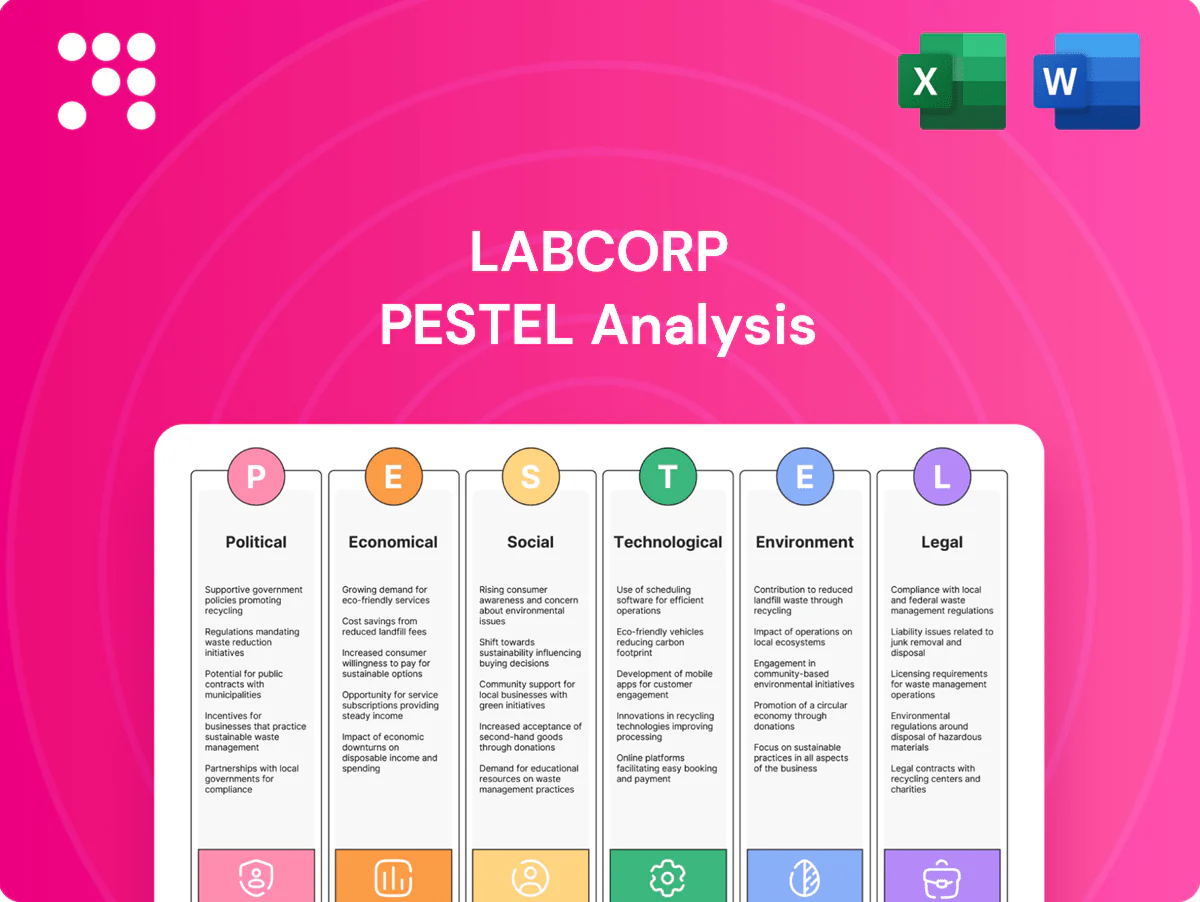

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely affect Labcorp, with data-backed trends, specific sub-point examples, and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios for planning and funding.

A concise, visually segmented PESTLE summary of Labcorp that can be dropped into presentations, shared across teams, and annotated for local business lines—streamlining external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and testing demand

Employment levels and employer-sponsored insurance (49% of US population in 2023, KFF) drive routine test volumes; US unemployment was 3.7% in 2024 (BLS). Recessions historically compress discretionary screening and wellness panels, while counter-cyclical infectious-disease spikes (eg COVID testing surges) can partially offset volume declines. Diversification into Labcorp Drug Development smooths revenue volatility.

Payer mix and reimbursement rates

Shifts toward government programs — Medicare enrollment of about 67 million in 2024 — and expanded Medicaid pressure average reimbursement, lowering margins on high-volume testing. Private payer consolidation (large insurers and pharmacy benefit managers) increases negotiating leverage, compressing price per test. Denial management and revenue-cycle optimization have become key profit levers, while contracting must balance volume with sustainable pricing to protect EBITDA.

Labor costs and talent scarcity

Medical technologist shortages—BLS reports 335,800 clinical laboratory technologists and technicians employed in May 2022 with a median annual wage of $57,800—inflate wages and overtime costs for Labcorp. Recruiting and retention compete directly with hospital labs and peers, raising labor expense pressure. Investment in automation and workflow redesign can lower per-test labor costs, while partnerships with training programs and schools build longer-term pipelines.

Biopharma funding and pipeline health

Biopharma funding and capital markets drive Labcorp test volumes as drug development revenues track venture flows; strong oncology and rare-disease pipelines particularly lift demand for specialized diagnostics and biomarker services. Trial delays or funding droughts compress utilization and pressure margins, while flexible capacity and modular services let Labcorp reallocate resources and preserve utilization.

- Market sensitivity: ties to VC and public biotech funding

- Demand drivers: oncology and rare-disease pipelines

- Risks: trial delays, capital droughts

- Mitigants: flexible capacity, modular services

M&A and industry consolidation

M&A and consolidation let Labcorp capture scale: broader test menus and procurement savings that can boost margins in a diagnostics market valued at about 92 billion USD in 2023. Integration risk and cultural mismatches can erode synergies and raise costs. Heightened antitrust review (often 6–12 months) affects deal timing and structure. Portfolio pruning focuses capital on higher-ROIC assets.

- Scale: procurement savings, menu breadth

- Risk: integration can erode synergies

- Antitrust: 6–12 month review impacts deals

- Capital: pruning to improve ROIC

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Employment and 49% employer-sponsored coverage (2023, KFF) plus 3.7% US unemployment (2024, BLS) drive routine volumes; diversification into Labcorp Drug Development smooths volatility. Medicare enrollment ~67M (2024) and payer consolidation compress reimbursement. Lab tech shortages (335,800; median $57,800, May 2022) raise labor costs; diagnostics market ~$92B (2023) favors scale.

| Metric | Value |

|---|---|

| Unemployment (2024) | 3.7% |

| Employer coverage (2023) | 49% |

| Medicare (2024) | ~67M |

| Diagnostics market (2023) | $92B |

Preview the Actual Deliverable

Labcorp PESTLE Analysis

The Labcorp PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting Labcorp. It includes actionable insights for investors and strategic decision‑makers. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressure, and rapid tech advances are reshaping Labcorp’s strategic outlook in this concise PESTLE snapshot. Our full analysis delivers the detailed risks and opportunities behind these trends, refined for investors and strategists. Purchase the complete report to access actionable insights and ready-to-use recommendations.

Political factors

Healthcare policy and reimbursement

Government healthcare priorities shape coverage and test utilization, with Medicare covering about 66 million and Medicaid/CHIP roughly 82 million beneficiaries in 2024, directly influencing Labcorp volumes. Shifts in Medicare/Medicaid reimbursement rules can materially alter pricing and throughput. Policy moves toward value-based care favor diagnostics that show clear clinical utility and cost-effectiveness. Labcorp must align test menus and evidence dossiers with evolving payer expectations.

Public health funding and preparedness

National and local public health budgets directly drive demand for infectious disease testing and surveillance, influencing Labcorp’s contracted testing volumes and reimbursement rates. Emergency funding during outbreaks has historically produced rapid volume spikes and capacity strain, then post-crisis normalization creates revenue volatility for lab operators. Strategic partnerships with federal and state health agencies improve pipeline visibility and can stabilize demand through multi-year contracts and preparedness programs.

Global regulatory harmonization

Differences between U.S. and EU review clocks—FDA PDUFA ~10 months versus EMA centralized review 210 days—plus divergent emerging-market rules extend trial timelines and complicate Labcorp’s lab operations. Harmonization efforts can lower compliance burden but require proactive alignment of global SOPs and IT systems. Active participation in ICH and regional standard-setting helps shape favorable pathways as fragmentation raises costs and delays market entry.

Geopolitical risk and supply chains

Tariffs, sanctions, and export controls can disrupt flows of reagents and instrumentation to Labcorp, raising procurement costs and causing substitution or retrofit needs. Political instability along transit corridors increases logistics costs and lead times for lab supplies and trial materials. Dual-sourcing, regional inventory buffers, and nearshoring have been adopted to mitigate exposure, while cross-border data restrictions complicate global trial data sharing and compliance.

- Tariffs/sanctions: disrupt reagent and instrument imports

- Logistics: instability increases costs and lead times

- Mitigation: dual-sourcing and regional buffers

- Data: cross-border restrictions complicate trial management

Government pricing pressure

Government payers, led by Medicare and Medicaid, negotiate aggressively and their fee schedules effectively anchor many commercial lab rates, pressuring Labcorp margins.

Price-transparency rules (CMS hospital rule in force since 2021) and 2024 enforcement trends are compressing negotiated spreads; reference pricing in markets like the UK/EU can echo into multinational contracts.

Political emphasis on outcomes means Labcorp must demonstrate cost-offsets with real-world evidence to protect reimbursement and secure value-based deals.

- Public payers anchor commercial rates

- Transparency rules tighten margins (heightened enforcement 2024)

- Reference pricing abroad impacts multinational contracts

- Outcomes data critical for value-based reimbursement

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Government payers (Medicare ~66M, Medicaid/CHIP ~82M in 2024) anchor pricing and drive volumes; 2024 enforcement of CMS price-transparency compresses spreads. Regulatory divergence (FDA PDUFA ~10 months vs EMA 210 days) and trade controls raise time-to-market and reagent costs. Labcorp mitigates via dual-sourcing, regional buffers and value-evidence for payers.

| Metric | 2024/2025 |

|---|---|

| Medicare beneficiaries | ~66M (2024) |

| Medicaid/CHIP | ~82M (2024) |

| FDA vs EMA review | PDUFA ~10 mo / EMA 210 days |

| CMS enforcement | Heightened (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely affect Labcorp, with data-backed trends, specific sub-point examples, and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios for planning and funding.

A concise, visually segmented PESTLE summary of Labcorp that can be dropped into presentations, shared across teams, and annotated for local business lines—streamlining external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and testing demand

Employment levels and employer-sponsored insurance (49% of US population in 2023, KFF) drive routine test volumes; US unemployment was 3.7% in 2024 (BLS). Recessions historically compress discretionary screening and wellness panels, while counter-cyclical infectious-disease spikes (eg COVID testing surges) can partially offset volume declines. Diversification into Labcorp Drug Development smooths revenue volatility.

Payer mix and reimbursement rates

Shifts toward government programs — Medicare enrollment of about 67 million in 2024 — and expanded Medicaid pressure average reimbursement, lowering margins on high-volume testing. Private payer consolidation (large insurers and pharmacy benefit managers) increases negotiating leverage, compressing price per test. Denial management and revenue-cycle optimization have become key profit levers, while contracting must balance volume with sustainable pricing to protect EBITDA.

Labor costs and talent scarcity

Medical technologist shortages—BLS reports 335,800 clinical laboratory technologists and technicians employed in May 2022 with a median annual wage of $57,800—inflate wages and overtime costs for Labcorp. Recruiting and retention compete directly with hospital labs and peers, raising labor expense pressure. Investment in automation and workflow redesign can lower per-test labor costs, while partnerships with training programs and schools build longer-term pipelines.

Biopharma funding and pipeline health

Biopharma funding and capital markets drive Labcorp test volumes as drug development revenues track venture flows; strong oncology and rare-disease pipelines particularly lift demand for specialized diagnostics and biomarker services. Trial delays or funding droughts compress utilization and pressure margins, while flexible capacity and modular services let Labcorp reallocate resources and preserve utilization.

- Market sensitivity: ties to VC and public biotech funding

- Demand drivers: oncology and rare-disease pipelines

- Risks: trial delays, capital droughts

- Mitigants: flexible capacity, modular services

M&A and industry consolidation

M&A and consolidation let Labcorp capture scale: broader test menus and procurement savings that can boost margins in a diagnostics market valued at about 92 billion USD in 2023. Integration risk and cultural mismatches can erode synergies and raise costs. Heightened antitrust review (often 6–12 months) affects deal timing and structure. Portfolio pruning focuses capital on higher-ROIC assets.

- Scale: procurement savings, menu breadth

- Risk: integration can erode synergies

- Antitrust: 6–12 month review impacts deals

- Capital: pruning to improve ROIC

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Employment and 49% employer-sponsored coverage (2023, KFF) plus 3.7% US unemployment (2024, BLS) drive routine volumes; diversification into Labcorp Drug Development smooths volatility. Medicare enrollment ~67M (2024) and payer consolidation compress reimbursement. Lab tech shortages (335,800; median $57,800, May 2022) raise labor costs; diagnostics market ~$92B (2023) favors scale.

| Metric | Value |

|---|---|

| Unemployment (2024) | 3.7% |

| Employer coverage (2023) | 49% |

| Medicare (2024) | ~67M |

| Diagnostics market (2023) | $92B |

Preview the Actual Deliverable

Labcorp PESTLE Analysis

The Labcorp PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting Labcorp. It includes actionable insights for investors and strategic decision‑makers. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic pressure, and rapid tech advances are reshaping Labcorp’s strategic outlook in this concise PESTLE snapshot. Our full analysis delivers the detailed risks and opportunities behind these trends, refined for investors and strategists. Purchase the complete report to access actionable insights and ready-to-use recommendations.

Political factors

Healthcare policy and reimbursement

Government healthcare priorities shape coverage and test utilization, with Medicare covering about 66 million and Medicaid/CHIP roughly 82 million beneficiaries in 2024, directly influencing Labcorp volumes. Shifts in Medicare/Medicaid reimbursement rules can materially alter pricing and throughput. Policy moves toward value-based care favor diagnostics that show clear clinical utility and cost-effectiveness. Labcorp must align test menus and evidence dossiers with evolving payer expectations.

Public health funding and preparedness

National and local public health budgets directly drive demand for infectious disease testing and surveillance, influencing Labcorp’s contracted testing volumes and reimbursement rates. Emergency funding during outbreaks has historically produced rapid volume spikes and capacity strain, then post-crisis normalization creates revenue volatility for lab operators. Strategic partnerships with federal and state health agencies improve pipeline visibility and can stabilize demand through multi-year contracts and preparedness programs.

Global regulatory harmonization

Differences between U.S. and EU review clocks—FDA PDUFA ~10 months versus EMA centralized review 210 days—plus divergent emerging-market rules extend trial timelines and complicate Labcorp’s lab operations. Harmonization efforts can lower compliance burden but require proactive alignment of global SOPs and IT systems. Active participation in ICH and regional standard-setting helps shape favorable pathways as fragmentation raises costs and delays market entry.

Geopolitical risk and supply chains

Tariffs, sanctions, and export controls can disrupt flows of reagents and instrumentation to Labcorp, raising procurement costs and causing substitution or retrofit needs. Political instability along transit corridors increases logistics costs and lead times for lab supplies and trial materials. Dual-sourcing, regional inventory buffers, and nearshoring have been adopted to mitigate exposure, while cross-border data restrictions complicate global trial data sharing and compliance.

- Tariffs/sanctions: disrupt reagent and instrument imports

- Logistics: instability increases costs and lead times

- Mitigation: dual-sourcing and regional buffers

- Data: cross-border restrictions complicate trial management

Government pricing pressure

Government payers, led by Medicare and Medicaid, negotiate aggressively and their fee schedules effectively anchor many commercial lab rates, pressuring Labcorp margins.

Price-transparency rules (CMS hospital rule in force since 2021) and 2024 enforcement trends are compressing negotiated spreads; reference pricing in markets like the UK/EU can echo into multinational contracts.

Political emphasis on outcomes means Labcorp must demonstrate cost-offsets with real-world evidence to protect reimbursement and secure value-based deals.

- Public payers anchor commercial rates

- Transparency rules tighten margins (heightened enforcement 2024)

- Reference pricing abroad impacts multinational contracts

- Outcomes data critical for value-based reimbursement

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Government payers (Medicare ~66M, Medicaid/CHIP ~82M in 2024) anchor pricing and drive volumes; 2024 enforcement of CMS price-transparency compresses spreads. Regulatory divergence (FDA PDUFA ~10 months vs EMA 210 days) and trade controls raise time-to-market and reagent costs. Labcorp mitigates via dual-sourcing, regional buffers and value-evidence for payers.

| Metric | 2024/2025 |

|---|---|

| Medicare beneficiaries | ~66M (2024) |

| Medicaid/CHIP | ~82M (2024) |

| FDA vs EMA review | PDUFA ~10 mo / EMA 210 days |

| CMS enforcement | Heightened (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — uniquely affect Labcorp, with data-backed trends, specific sub-point examples, and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios for planning and funding.

A concise, visually segmented PESTLE summary of Labcorp that can be dropped into presentations, shared across teams, and annotated for local business lines—streamlining external risk discussions and strategic planning.

Economic factors

Macroeconomic cycles and testing demand

Employment levels and employer-sponsored insurance (49% of US population in 2023, KFF) drive routine test volumes; US unemployment was 3.7% in 2024 (BLS). Recessions historically compress discretionary screening and wellness panels, while counter-cyclical infectious-disease spikes (eg COVID testing surges) can partially offset volume declines. Diversification into Labcorp Drug Development smooths revenue volatility.

Payer mix and reimbursement rates

Shifts toward government programs — Medicare enrollment of about 67 million in 2024 — and expanded Medicaid pressure average reimbursement, lowering margins on high-volume testing. Private payer consolidation (large insurers and pharmacy benefit managers) increases negotiating leverage, compressing price per test. Denial management and revenue-cycle optimization have become key profit levers, while contracting must balance volume with sustainable pricing to protect EBITDA.

Labor costs and talent scarcity

Medical technologist shortages—BLS reports 335,800 clinical laboratory technologists and technicians employed in May 2022 with a median annual wage of $57,800—inflate wages and overtime costs for Labcorp. Recruiting and retention compete directly with hospital labs and peers, raising labor expense pressure. Investment in automation and workflow redesign can lower per-test labor costs, while partnerships with training programs and schools build longer-term pipelines.

Biopharma funding and pipeline health

Biopharma funding and capital markets drive Labcorp test volumes as drug development revenues track venture flows; strong oncology and rare-disease pipelines particularly lift demand for specialized diagnostics and biomarker services. Trial delays or funding droughts compress utilization and pressure margins, while flexible capacity and modular services let Labcorp reallocate resources and preserve utilization.

- Market sensitivity: ties to VC and public biotech funding

- Demand drivers: oncology and rare-disease pipelines

- Risks: trial delays, capital droughts

- Mitigants: flexible capacity, modular services

M&A and industry consolidation

M&A and consolidation let Labcorp capture scale: broader test menus and procurement savings that can boost margins in a diagnostics market valued at about 92 billion USD in 2023. Integration risk and cultural mismatches can erode synergies and raise costs. Heightened antitrust review (often 6–12 months) affects deal timing and structure. Portfolio pruning focuses capital on higher-ROIC assets.

- Scale: procurement savings, menu breadth

- Risk: integration can erode synergies

- Antitrust: 6–12 month review impacts deals

- Capital: pruning to improve ROIC

Government payers set pricing; Medicare ~66M, Medicaid/CHIP ~82M

Employment and 49% employer-sponsored coverage (2023, KFF) plus 3.7% US unemployment (2024, BLS) drive routine volumes; diversification into Labcorp Drug Development smooths volatility. Medicare enrollment ~67M (2024) and payer consolidation compress reimbursement. Lab tech shortages (335,800; median $57,800, May 2022) raise labor costs; diagnostics market ~$92B (2023) favors scale.

| Metric | Value |

|---|---|

| Unemployment (2024) | 3.7% |

| Employer coverage (2023) | 49% |

| Medicare (2024) | ~67M |

| Diagnostics market (2023) | $92B |

Preview the Actual Deliverable

Labcorp PESTLE Analysis

The Labcorp PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal and environmental factors affecting Labcorp. It includes actionable insights for investors and strategic decision‑makers. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.