LACROIX Porter's Five Forces Analysis

From Overview to Strategy Blueprint

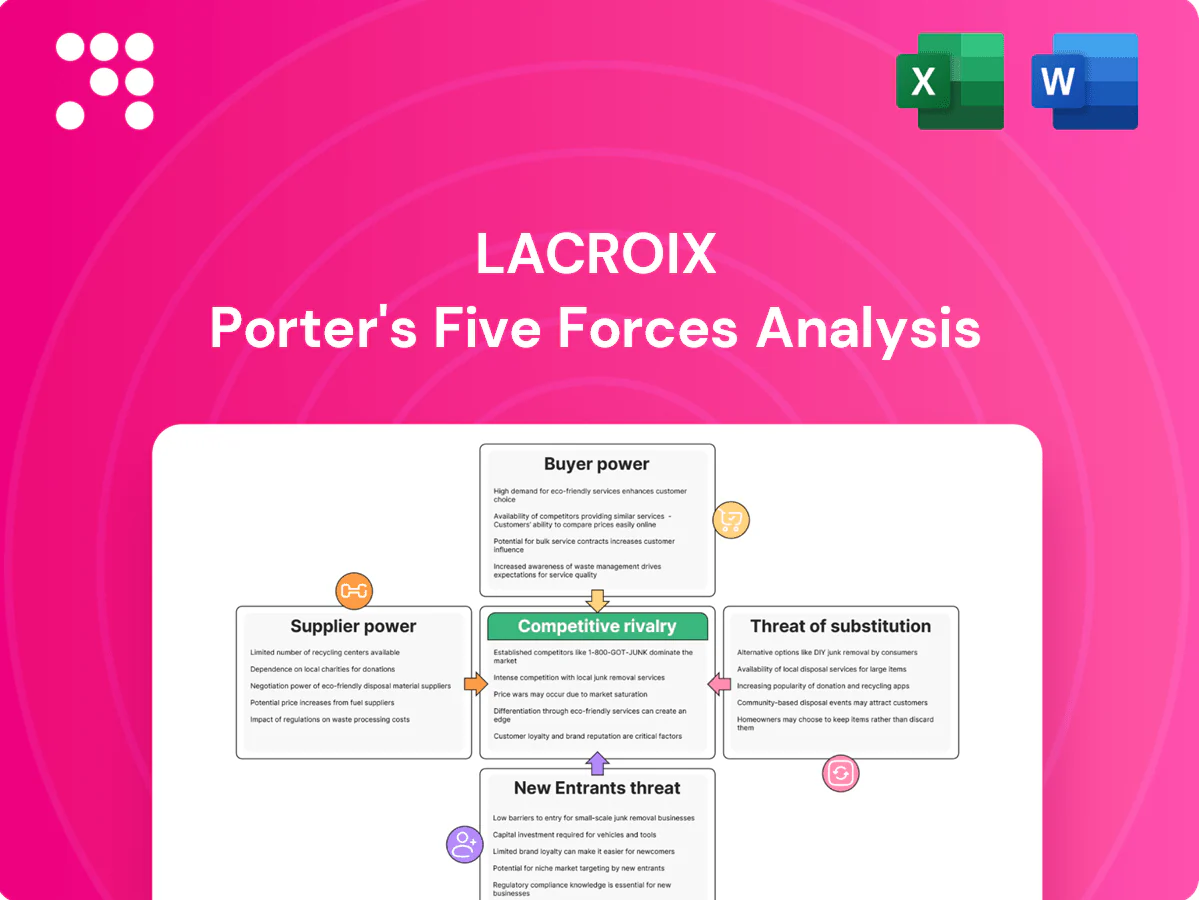

LACROIX faces moderate supplier power, rising buyer demands, niche entry barriers, substitute threats from electronics consolidation, and intense rivalry driven by rapid tech innovation. This snapshot highlights where margins and strategy are most exposed and where management can act. Ready to move beyond the basics? Get a full strategic breakdown of LACROIX’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentrated chip suppliers

Semiconductor and MCU sourcing is highly concentrated—TSMC held about 52% of the pure‑play foundry market in 2024 and the top 3 IDMs supply over 60% of MCUs; allocation cycles and lead times can jump from typical 4–8 weeks to 20+ weeks, shifting power to suppliers. LACROIX must dual‑source and redesign around shortages; strategic supply agreements and 3–4 month inventory buffers partially mitigate risk.

Specialized components

Industrial sensors, RF modules and safety-certified parts are niche with few substitutes, giving suppliers leverage; qualification and compliance testing commonly exceed $50,000 and can take months, raising switching barriers. In tight markets suppliers have historically charged premiums of 10–25% on specialized SKUs. Long-term contracts and approved-vendor lists, used widely in 2024 procurement, dampen short-term price swings.

Manufacturing equipment vendors

SMT lines (~€2–3M each in 2024), AOI systems (€0.2–0.8M) and test equipment come from a handful of OEMs, concentrating supplier power. Upgrades and maintenance create technical lock‑in, with service agreements typically 8–15% of equipment value annually, adding recurring OPEX. Bulk purchases can secure 5–15% discounts but demand significant capex commitment, limiting bargaining flexibility for LACROIX.

Software and cloud stack

OS, middleware and cloud providers (AWS ~32%, Azure ~23%, GCP ~10% in 2024) underpin LACROIX’s IoT stack, so API or licensing shifts can quickly reallocate margins and service revenue; platform fees and licensing changes have altered vendor take in adjacent markets by double-digit points. Widespread containerization (CNCF 2023: ~92% adoption) and multicloud strategies (Flexera 2024: ~92% multicloud use) reduce supplier lock-in, and growing open standards adoption strengthens LACROIX’s negotiating stance.

- OS/middleware dependency: high

- Top-cloud concentration: AWS/Azure/GCP ~65%

- Containerization: ~92% adoption

- Multicloud: ~92% enterprises

- Open standards: increases supplier leverage for LACROIX

Telecom and connectivity

Operators for LTE-M, NB-IoT and 5G private networks materially drive recurring costs and SLA terms; as of 2024 LTE-M/NB-IoT represented over 50% of new cellular IoT connections (GSMA 2024), shaping pricing power. Coverage gaps in Latin America and parts of EMEA limit substitute options regionally. MVNO models and LPWAN rivals (LoRaWAN, Sigfox) increase supplier leverage, while volume commitments can win tariff discounts and 99.9%+ uptime SLAs.

- Operators: recurring costs, SLAs

- 2024: LTE-M/NB-IoT >50% new connections

- Coverage limits substitutes regionally

- MVNO/LPWAN add leverage

- Volume commitments → better tariffs, 99.9%+ uptime

Foundry power 52%, top-3 MCUs >60%, cloud concentrated

Supplier power is high: TSMC ~52% foundry share (2024) and top‑3 IDMs >60% MCUs, causing long lead times and premium pricing. Niche sensors/RF parts have few substitutes; qualification costs >€50k. SMT/AOI OEM concentration drives technical lock‑in (SMT €2–3M). Cloud (AWS 32%, Azure 23%, GCP 10%) and operators (LTE‑M/NB‑IoT >50% new connections) create recurring leverage.

| Item | 2024 stat |

|---|---|

| Foundry share | TSMC 52% |

| MCUs | Top‑3 >60% |

| SMT cost | €2–3M |

| Cloud | AWS32%/AZ23%/GCP10% |

| Cellular IoT | LTE‑M/NB‑IoT >50% |

What is included in the product

Tailored Porter's Five Forces analysis for LACROIX, uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks that shape pricing and profitability. Actionable insights identify disruptive threats and protective market dynamics, suitable for investor decks, strategy plans, or editable Word reports.

A clear, one-sheet LACROIX Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart and customizable force levels—ideal for rapid decision-making, slide-ready reporting, and non-technical users.

Customers Bargaining Power

Municipal and utility tenders

Public procurement in the EU represented roughly 14% of GDP in 2024, making municipal and utility tenders highly price-competitive and transparent. Buyers commonly issue multi-year RFPs (typically 3–5 years), intensifying sustained price pressure. Total cost of ownership and compliance scoring allow LACROIX to submit value-based bids beyond headline price. References and pilot projects are decisive, often tipping awards toward proven suppliers.

Industrial OEMs and Tier-1s

Industrial OEMs and Tier-1s aggregate large volumes and negotiate aggressively, often enforcing dual-sourcing that typically limits any single supplier to about a 50/50 share; PPAP, 100% traceability and strict KPI regimes (on-time delivery, defect ppm <100) are standard. Co-development contracts can embed LACROIX into product lifecycles, raising switching costs and protecting a increasing portion of recurring revenue.

Switching and integration costs

Embedded firmware, proprietary protocols and certification needs make switching LACROIX systems non-trivial, driving high integration costs for buyers. Field-deployed assets create physical replacement frictions and logistics hurdles, especially given typical renewal cycles of 3–5 years. Buyers nonetheless use renewal windows to pressure pricing, while LACROIXs 2024 long-term service and upgrade paths materially reduce churn.

Outcome-driven procurement

Clients now demand SLAs of 99.9%+ uptime, 15–30% energy savings and payback under 3 years; performance-linked pricing (up to 20% of contract value) raises buyer leverage while shifting risk to suppliers. Data ownership clauses and residency are deal-breakers; strong analytics and cybersecurity offerings reduce pure price competition and support premium pricing.

- SLAs: 99.9%+

- Energy savings: 15–30%

- ROI/payback: <3 years

- Performance pricing: up to 20%

- Key terms: data ownership & residency

- Differentiators: analytics, cybersecurity

Global alternatives

Buyers can source from EMS firms in lower-cost regions in 2024, while nearshoring trends partially balance this by shifting contracts back to Europe; security, sovereignty and ESG requirements increasingly favor European providers; currency volatility in 2024 (EUR, USD fluctuations) continues to influence sourcing timing and contract terms.

- Global sourcing pressure in 2024

- Nearshoring moderates leverage

- Security/ESG favors Europe

- Currency moves alter decisions

EU procurement power: 14% GDP, dual-sourcing, SLAs drive nearshoring

Public procurement ~14% of EU GDP in 2024 drives transparent, price-competitive multi-year RFPs (3–5y). OEMs enforce dual-sourcing (~50/50) with strict KPIs (ppm <100) raising buyer leverage. SLAs 99.9%+, performance pricing up to 20% and data residency demands tilt negotiations toward value over headline price. Nearshoring and ESG tilt sourcing back to Europe despite low-cost EMS competition.

| Metric | 2024 |

|---|---|

| Public procurement | ~14% GDP |

| RFP length | 3–5 years |

| Dual-sourcing | ~50/50 |

| SLAs | 99.9%+ |

| Performance pricing | up to 20% |

Preview the Actual Deliverable

LACROIX Porter's Five Forces Analysis

This preview shows the exact LACROIX Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete file shown here, available instantly after payment.

From Overview to Strategy Blueprint

LACROIX faces moderate supplier power, rising buyer demands, niche entry barriers, substitute threats from electronics consolidation, and intense rivalry driven by rapid tech innovation. This snapshot highlights where margins and strategy are most exposed and where management can act. Ready to move beyond the basics? Get a full strategic breakdown of LACROIX’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentrated chip suppliers

Semiconductor and MCU sourcing is highly concentrated—TSMC held about 52% of the pure‑play foundry market in 2024 and the top 3 IDMs supply over 60% of MCUs; allocation cycles and lead times can jump from typical 4–8 weeks to 20+ weeks, shifting power to suppliers. LACROIX must dual‑source and redesign around shortages; strategic supply agreements and 3–4 month inventory buffers partially mitigate risk.

Specialized components

Industrial sensors, RF modules and safety-certified parts are niche with few substitutes, giving suppliers leverage; qualification and compliance testing commonly exceed $50,000 and can take months, raising switching barriers. In tight markets suppliers have historically charged premiums of 10–25% on specialized SKUs. Long-term contracts and approved-vendor lists, used widely in 2024 procurement, dampen short-term price swings.

Manufacturing equipment vendors

SMT lines (~€2–3M each in 2024), AOI systems (€0.2–0.8M) and test equipment come from a handful of OEMs, concentrating supplier power. Upgrades and maintenance create technical lock‑in, with service agreements typically 8–15% of equipment value annually, adding recurring OPEX. Bulk purchases can secure 5–15% discounts but demand significant capex commitment, limiting bargaining flexibility for LACROIX.

Software and cloud stack

OS, middleware and cloud providers (AWS ~32%, Azure ~23%, GCP ~10% in 2024) underpin LACROIX’s IoT stack, so API or licensing shifts can quickly reallocate margins and service revenue; platform fees and licensing changes have altered vendor take in adjacent markets by double-digit points. Widespread containerization (CNCF 2023: ~92% adoption) and multicloud strategies (Flexera 2024: ~92% multicloud use) reduce supplier lock-in, and growing open standards adoption strengthens LACROIX’s negotiating stance.

- OS/middleware dependency: high

- Top-cloud concentration: AWS/Azure/GCP ~65%

- Containerization: ~92% adoption

- Multicloud: ~92% enterprises

- Open standards: increases supplier leverage for LACROIX

Telecom and connectivity

Operators for LTE-M, NB-IoT and 5G private networks materially drive recurring costs and SLA terms; as of 2024 LTE-M/NB-IoT represented over 50% of new cellular IoT connections (GSMA 2024), shaping pricing power. Coverage gaps in Latin America and parts of EMEA limit substitute options regionally. MVNO models and LPWAN rivals (LoRaWAN, Sigfox) increase supplier leverage, while volume commitments can win tariff discounts and 99.9%+ uptime SLAs.

- Operators: recurring costs, SLAs

- 2024: LTE-M/NB-IoT >50% new connections

- Coverage limits substitutes regionally

- MVNO/LPWAN add leverage

- Volume commitments → better tariffs, 99.9%+ uptime

Foundry power 52%, top-3 MCUs >60%, cloud concentrated

Supplier power is high: TSMC ~52% foundry share (2024) and top‑3 IDMs >60% MCUs, causing long lead times and premium pricing. Niche sensors/RF parts have few substitutes; qualification costs >€50k. SMT/AOI OEM concentration drives technical lock‑in (SMT €2–3M). Cloud (AWS 32%, Azure 23%, GCP 10%) and operators (LTE‑M/NB‑IoT >50% new connections) create recurring leverage.

| Item | 2024 stat |

|---|---|

| Foundry share | TSMC 52% |

| MCUs | Top‑3 >60% |

| SMT cost | €2–3M |

| Cloud | AWS32%/AZ23%/GCP10% |

| Cellular IoT | LTE‑M/NB‑IoT >50% |

What is included in the product

Tailored Porter's Five Forces analysis for LACROIX, uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks that shape pricing and profitability. Actionable insights identify disruptive threats and protective market dynamics, suitable for investor decks, strategy plans, or editable Word reports.

A clear, one-sheet LACROIX Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart and customizable force levels—ideal for rapid decision-making, slide-ready reporting, and non-technical users.

Customers Bargaining Power

Municipal and utility tenders

Public procurement in the EU represented roughly 14% of GDP in 2024, making municipal and utility tenders highly price-competitive and transparent. Buyers commonly issue multi-year RFPs (typically 3–5 years), intensifying sustained price pressure. Total cost of ownership and compliance scoring allow LACROIX to submit value-based bids beyond headline price. References and pilot projects are decisive, often tipping awards toward proven suppliers.

Industrial OEMs and Tier-1s

Industrial OEMs and Tier-1s aggregate large volumes and negotiate aggressively, often enforcing dual-sourcing that typically limits any single supplier to about a 50/50 share; PPAP, 100% traceability and strict KPI regimes (on-time delivery, defect ppm <100) are standard. Co-development contracts can embed LACROIX into product lifecycles, raising switching costs and protecting a increasing portion of recurring revenue.

Switching and integration costs

Embedded firmware, proprietary protocols and certification needs make switching LACROIX systems non-trivial, driving high integration costs for buyers. Field-deployed assets create physical replacement frictions and logistics hurdles, especially given typical renewal cycles of 3–5 years. Buyers nonetheless use renewal windows to pressure pricing, while LACROIXs 2024 long-term service and upgrade paths materially reduce churn.

Outcome-driven procurement

Clients now demand SLAs of 99.9%+ uptime, 15–30% energy savings and payback under 3 years; performance-linked pricing (up to 20% of contract value) raises buyer leverage while shifting risk to suppliers. Data ownership clauses and residency are deal-breakers; strong analytics and cybersecurity offerings reduce pure price competition and support premium pricing.

- SLAs: 99.9%+

- Energy savings: 15–30%

- ROI/payback: <3 years

- Performance pricing: up to 20%

- Key terms: data ownership & residency

- Differentiators: analytics, cybersecurity

Global alternatives

Buyers can source from EMS firms in lower-cost regions in 2024, while nearshoring trends partially balance this by shifting contracts back to Europe; security, sovereignty and ESG requirements increasingly favor European providers; currency volatility in 2024 (EUR, USD fluctuations) continues to influence sourcing timing and contract terms.

- Global sourcing pressure in 2024

- Nearshoring moderates leverage

- Security/ESG favors Europe

- Currency moves alter decisions

EU procurement power: 14% GDP, dual-sourcing, SLAs drive nearshoring

Public procurement ~14% of EU GDP in 2024 drives transparent, price-competitive multi-year RFPs (3–5y). OEMs enforce dual-sourcing (~50/50) with strict KPIs (ppm <100) raising buyer leverage. SLAs 99.9%+, performance pricing up to 20% and data residency demands tilt negotiations toward value over headline price. Nearshoring and ESG tilt sourcing back to Europe despite low-cost EMS competition.

| Metric | 2024 |

|---|---|

| Public procurement | ~14% GDP |

| RFP length | 3–5 years |

| Dual-sourcing | ~50/50 |

| SLAs | 99.9%+ |

| Performance pricing | up to 20% |

Preview the Actual Deliverable

LACROIX Porter's Five Forces Analysis

This preview shows the exact LACROIX Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete file shown here, available instantly after payment.

Description

From Overview to Strategy Blueprint

LACROIX faces moderate supplier power, rising buyer demands, niche entry barriers, substitute threats from electronics consolidation, and intense rivalry driven by rapid tech innovation. This snapshot highlights where margins and strategy are most exposed and where management can act. Ready to move beyond the basics? Get a full strategic breakdown of LACROIX’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentrated chip suppliers

Semiconductor and MCU sourcing is highly concentrated—TSMC held about 52% of the pure‑play foundry market in 2024 and the top 3 IDMs supply over 60% of MCUs; allocation cycles and lead times can jump from typical 4–8 weeks to 20+ weeks, shifting power to suppliers. LACROIX must dual‑source and redesign around shortages; strategic supply agreements and 3–4 month inventory buffers partially mitigate risk.

Specialized components

Industrial sensors, RF modules and safety-certified parts are niche with few substitutes, giving suppliers leverage; qualification and compliance testing commonly exceed $50,000 and can take months, raising switching barriers. In tight markets suppliers have historically charged premiums of 10–25% on specialized SKUs. Long-term contracts and approved-vendor lists, used widely in 2024 procurement, dampen short-term price swings.

Manufacturing equipment vendors

SMT lines (~€2–3M each in 2024), AOI systems (€0.2–0.8M) and test equipment come from a handful of OEMs, concentrating supplier power. Upgrades and maintenance create technical lock‑in, with service agreements typically 8–15% of equipment value annually, adding recurring OPEX. Bulk purchases can secure 5–15% discounts but demand significant capex commitment, limiting bargaining flexibility for LACROIX.

Software and cloud stack

OS, middleware and cloud providers (AWS ~32%, Azure ~23%, GCP ~10% in 2024) underpin LACROIX’s IoT stack, so API or licensing shifts can quickly reallocate margins and service revenue; platform fees and licensing changes have altered vendor take in adjacent markets by double-digit points. Widespread containerization (CNCF 2023: ~92% adoption) and multicloud strategies (Flexera 2024: ~92% multicloud use) reduce supplier lock-in, and growing open standards adoption strengthens LACROIX’s negotiating stance.

- OS/middleware dependency: high

- Top-cloud concentration: AWS/Azure/GCP ~65%

- Containerization: ~92% adoption

- Multicloud: ~92% enterprises

- Open standards: increases supplier leverage for LACROIX

Telecom and connectivity

Operators for LTE-M, NB-IoT and 5G private networks materially drive recurring costs and SLA terms; as of 2024 LTE-M/NB-IoT represented over 50% of new cellular IoT connections (GSMA 2024), shaping pricing power. Coverage gaps in Latin America and parts of EMEA limit substitute options regionally. MVNO models and LPWAN rivals (LoRaWAN, Sigfox) increase supplier leverage, while volume commitments can win tariff discounts and 99.9%+ uptime SLAs.

- Operators: recurring costs, SLAs

- 2024: LTE-M/NB-IoT >50% new connections

- Coverage limits substitutes regionally

- MVNO/LPWAN add leverage

- Volume commitments → better tariffs, 99.9%+ uptime

Foundry power 52%, top-3 MCUs >60%, cloud concentrated

Supplier power is high: TSMC ~52% foundry share (2024) and top‑3 IDMs >60% MCUs, causing long lead times and premium pricing. Niche sensors/RF parts have few substitutes; qualification costs >€50k. SMT/AOI OEM concentration drives technical lock‑in (SMT €2–3M). Cloud (AWS 32%, Azure 23%, GCP 10%) and operators (LTE‑M/NB‑IoT >50% new connections) create recurring leverage.

| Item | 2024 stat |

|---|---|

| Foundry share | TSMC 52% |

| MCUs | Top‑3 >60% |

| SMT cost | €2–3M |

| Cloud | AWS32%/AZ23%/GCP10% |

| Cellular IoT | LTE‑M/NB‑IoT >50% |

What is included in the product

Tailored Porter's Five Forces analysis for LACROIX, uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks that shape pricing and profitability. Actionable insights identify disruptive threats and protective market dynamics, suitable for investor decks, strategy plans, or editable Word reports.

A clear, one-sheet LACROIX Porter's Five Forces summary that visualizes strategic pressure with an editable spider chart and customizable force levels—ideal for rapid decision-making, slide-ready reporting, and non-technical users.

Customers Bargaining Power

Municipal and utility tenders

Public procurement in the EU represented roughly 14% of GDP in 2024, making municipal and utility tenders highly price-competitive and transparent. Buyers commonly issue multi-year RFPs (typically 3–5 years), intensifying sustained price pressure. Total cost of ownership and compliance scoring allow LACROIX to submit value-based bids beyond headline price. References and pilot projects are decisive, often tipping awards toward proven suppliers.

Industrial OEMs and Tier-1s

Industrial OEMs and Tier-1s aggregate large volumes and negotiate aggressively, often enforcing dual-sourcing that typically limits any single supplier to about a 50/50 share; PPAP, 100% traceability and strict KPI regimes (on-time delivery, defect ppm <100) are standard. Co-development contracts can embed LACROIX into product lifecycles, raising switching costs and protecting a increasing portion of recurring revenue.

Switching and integration costs

Embedded firmware, proprietary protocols and certification needs make switching LACROIX systems non-trivial, driving high integration costs for buyers. Field-deployed assets create physical replacement frictions and logistics hurdles, especially given typical renewal cycles of 3–5 years. Buyers nonetheless use renewal windows to pressure pricing, while LACROIXs 2024 long-term service and upgrade paths materially reduce churn.

Outcome-driven procurement

Clients now demand SLAs of 99.9%+ uptime, 15–30% energy savings and payback under 3 years; performance-linked pricing (up to 20% of contract value) raises buyer leverage while shifting risk to suppliers. Data ownership clauses and residency are deal-breakers; strong analytics and cybersecurity offerings reduce pure price competition and support premium pricing.

- SLAs: 99.9%+

- Energy savings: 15–30%

- ROI/payback: <3 years

- Performance pricing: up to 20%

- Key terms: data ownership & residency

- Differentiators: analytics, cybersecurity

Global alternatives

Buyers can source from EMS firms in lower-cost regions in 2024, while nearshoring trends partially balance this by shifting contracts back to Europe; security, sovereignty and ESG requirements increasingly favor European providers; currency volatility in 2024 (EUR, USD fluctuations) continues to influence sourcing timing and contract terms.

- Global sourcing pressure in 2024

- Nearshoring moderates leverage

- Security/ESG favors Europe

- Currency moves alter decisions

EU procurement power: 14% GDP, dual-sourcing, SLAs drive nearshoring

Public procurement ~14% of EU GDP in 2024 drives transparent, price-competitive multi-year RFPs (3–5y). OEMs enforce dual-sourcing (~50/50) with strict KPIs (ppm <100) raising buyer leverage. SLAs 99.9%+, performance pricing up to 20% and data residency demands tilt negotiations toward value over headline price. Nearshoring and ESG tilt sourcing back to Europe despite low-cost EMS competition.

| Metric | 2024 |

|---|---|

| Public procurement | ~14% GDP |

| RFP length | 3–5 years |

| Dual-sourcing | ~50/50 |

| SLAs | 99.9%+ |

| Performance pricing | up to 20% |

Preview the Actual Deliverable

LACROIX Porter's Five Forces Analysis

This preview shows the exact LACROIX Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted, professionally written, and ready for download the moment you buy. You're getting the same complete file shown here, available instantly after payment.