Lakeland Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Lakeland Bank—three to five concise sections revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Ideal for investors and strategists, this report translates external risks into actionable insights. Purchase the full analysis to download the complete, editable version and make data-driven decisions confidently.

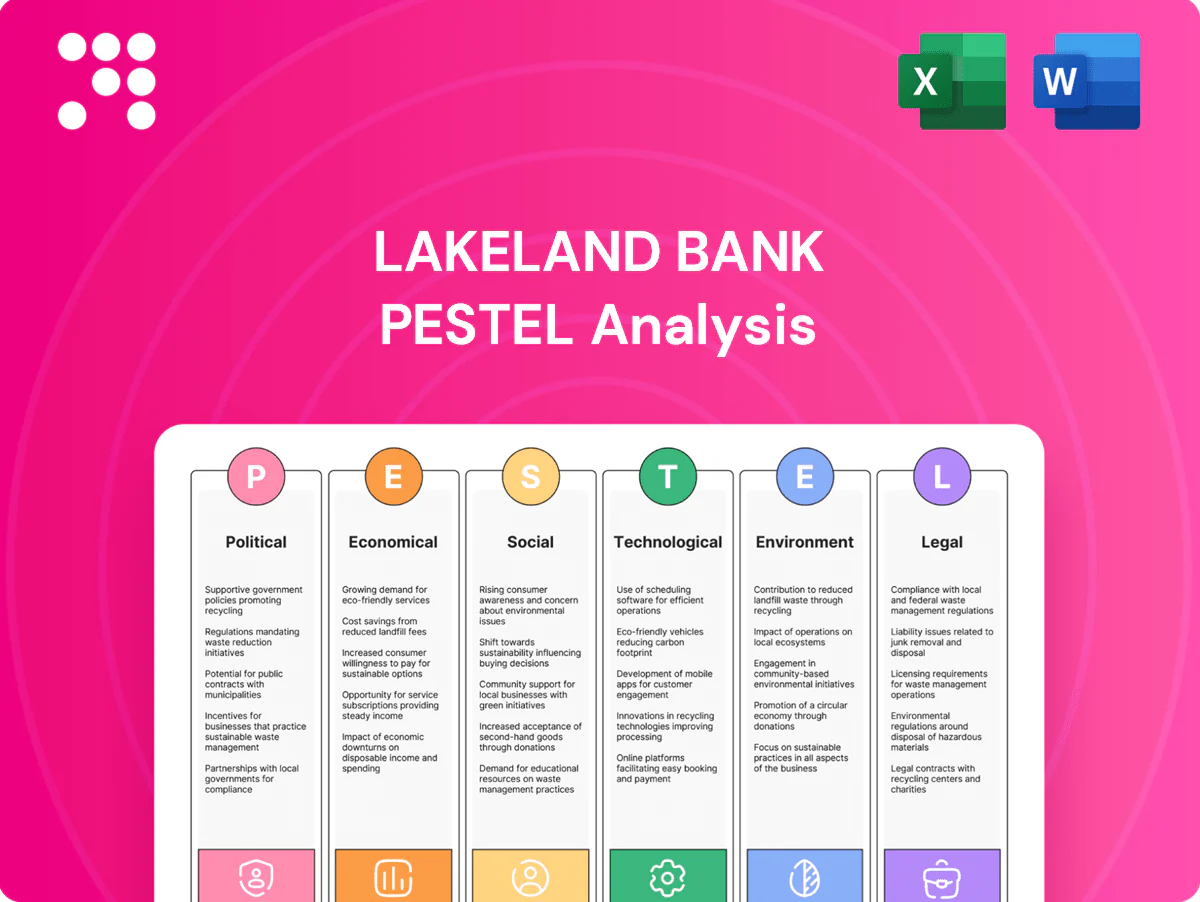

Political factors

State banking policy alignment

New Jersey’s banking priorities—shaped by the 1977 Community Reinvestment Act framework and state agencies—directly affect community bank operations, grant access, and CRA expectations in a state of about 9.3 million residents. Alignment with NJEDA and municipal economic agendas can unlock small-business lending partnerships; small businesses represent roughly 99.9% of US firms. Misalignment can slow approvals or program access, so Lakeland Bank should keep proactive dialogue with state agencies and municipal leaders.

Municipal relationships and public deposits

Winning or retaining public sector deposits hinges on local political relationships and procurement processes, particularly in New Jersey where 565 municipalities compete for banking services. Policy shifts on collateralization or bidding standards can reallocate municipal and school balances rapidly. Transparent, competitive proposals reduce rotation risk and ease procurement scrutiny. Active community engagement and regular outreach strengthen standing with towns and school districts.

Infrastructure and transit funding

Federal Bipartisan Infrastructure Law totals $1.2 trillion nationally and continued FY2024/2025 federal and New Jersey capital programs boost demand for contractor and supplier lending, creating opportunities for Lakeland Bank's construction portfolio. Political delays or state budget impasses can stall pipelines and cash flow. Banks with specialized construction lending capture upside from timely execution. Monitoring appropriations cycles aids resource planning.

Housing and zoning priorities

Local zoning decisions shape Lakeland Bank’s residential and mixed-use lending pipeline; a U.S. housing shortfall of about 3.8 million units (Harvard JCHS, 2024) intensifies demand for mortgages and construction loans. Pro-housing stances in service areas expand origination and construction financing opportunities, while restrictive zoning limits deal flow and can depress appraisal values. Active participation in planning forums gives Lakeland early visibility into projects and pricing.

- Zoning impact on pipeline

- Pro-housing = more mortgage/construction loans

- Restrictive zoning reduces appraisal values

- Planning forums provide early project visibility

Cross-border regional dynamics

Tri-state political coordination (NJ-NY-PA) shapes labor mobility and business formation across a combined population of about 41.8 million (2023 Census estimates), affecting deposit and small-business loan demand; changes in state taxes or incentives have redirected capital and workforce in recent regional relocations. Advocacy on regional competitiveness influences community bank growth, so Lakeland Bank should monitor interstate policy differentials closely.

- Population: 41.8M (2023)

- Labor mobility: cross-border commuting alters deposit flows

- Tax/incentive shifts can move loan originations

- Advocacy affects regulatory environment for community banks

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

NJ political priorities and CRA expectations affect Lakeland Bank operations in a state of 9.3M residents. Municipal deposit wins depend on procurement across 565 NJ towns and school districts. Fed/state infrastructure funding ($1.2T national) and a 3.8M US housing shortfall boost construction and mortgage demand. Tri-state (41.8M) tax shifts alter deposit and loan flows.

| Metric | Value |

|---|---|

| NJ population | 9.3M |

| Tri-state pop | 41.8M |

| Housing shortfall | 3.8M |

| Infra funding (US) | $1.2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lakeland Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, using region-specific data and current trends. Designed for executives and investors, it highlights actionable threats, opportunities and forward-looking scenario insights ready for reports or decks.

A concise, visually segmented PESTLE summary for Lakeland Bank that distills external risks and opportunities into clear language, easily dropped into presentations or shared across teams; editable notes let users tailor insights to their region or business line for faster alignment and decision-making.

Economic factors

Interest rate cycle sensitivity

Net interest margin at Lakeland Bank is highly sensitive to Fed policy (federal funds ~5.25–5.50% in 2024–25) and deposit beta in a competitive New Jersey market (industry deposit betas commonly 40–60%), with rapid hikes compressing fixed-rate securities valuations and slowing loan originations while cuts raise deposit retention pressure. Balance-sheet hedging and disciplined loan/deposit pricing, supported by granular repricing analytics, are critical to protect margins.

SMB health in core counties

Local SMB vitality drives C&I lending, treasury services and deposits; New Jersey had about 672,000 small businesses in 2023 and small firms account for roughly 47.5% of private-sector employment (SBA). Retail, healthcare, logistics and professional services dominate many NJ submarkets. Recessions raise credit costs and downgrade risks; sector diversification and relationship banking bolster resilience.

Commercial real estate exposure

Commercial real estate exposure materially affects Lakeland Bank credit quality as office, multifamily and mixed-use performance diverge; national office vacancy was about 17% in Q4 2024 while industrial vacancy remained near 4% (CoStar, Q4 2024). Suburban office softness raises vacancy and refinance risk; conservative LTVs, rigorous tenant analysis and proactive borrower engagement improve workout outcomes.

Labor costs and productivity

Tight New Jersey labor markets (NJ average unemployment 3.9% in 2024, BLS) are elevating compensation for branch and tech talent while average hourly earnings rose ~4.1% y/y in 2024 (BLS), pressuring margins unless digital adoption offsets wage inflation; targeted automation could replace or augment up to ~30% of routine banking tasks (McKinsey 2024), and retention programs cut recruiting friction and service disruption.

- Labor tightness: NJ unemployment 3.9% (2024, BLS)

- Wage pressure: avg hourly earnings +4.1% y/y (2024, BLS)

- Automation potential: ~30% routine tasks (McKinsey 2024)

- Retention lowers hiring costs and service gaps

Household wealth and migration

Affluent suburbs around Lakeland Bank have median household incomes often above $100,000 (2022 ACS), supporting deposits, mortgages and wealth-management revenue. Continued domestic outmigration from New Jersey (Census trend 2010–2023) can erode local demand, though in-migration to transit-rich towns such as Hoboken and Jersey City has sustained housing and banking activity. Tailored mover and first-time-buyer products can capture churn.

- Affluent suburbs: median HH income >$100,000 (2022 ACS)

- Net NJ domestic outflow: Census trend 2010–2023

- Transit towns growth: Hoboken/Jersey City population gains

- Opportunity: mover and first-time-buyer products

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

Fed policy (fed funds 5.25–5.50% 2024–25) and deposit beta (40–60%) drive NIM sensitivity; hedging and repricing analytics are essential. NJ economy: unemployment 3.9% (2024) and 672,000 small businesses (2023) support C&I but raise wage pressure. CRE split: office vacancy ~17% Q4 2024 vs industrial ~4%, stressing selective underwriting.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| NJ unemployment | 3.9% (2024) |

| Small businesses | 672,000 (2023) |

| Office/Industrial | 17% / 4% (Q4 2024) |

| Median HH income | >$100,000 (2022) |

What You See Is What You Get

Lakeland Bank PESTLE Analysis

The preview shown here is the exact Lakeland Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, structure, and data visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Lakeland Bank—three to five concise sections revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Ideal for investors and strategists, this report translates external risks into actionable insights. Purchase the full analysis to download the complete, editable version and make data-driven decisions confidently.

Political factors

State banking policy alignment

New Jersey’s banking priorities—shaped by the 1977 Community Reinvestment Act framework and state agencies—directly affect community bank operations, grant access, and CRA expectations in a state of about 9.3 million residents. Alignment with NJEDA and municipal economic agendas can unlock small-business lending partnerships; small businesses represent roughly 99.9% of US firms. Misalignment can slow approvals or program access, so Lakeland Bank should keep proactive dialogue with state agencies and municipal leaders.

Municipal relationships and public deposits

Winning or retaining public sector deposits hinges on local political relationships and procurement processes, particularly in New Jersey where 565 municipalities compete for banking services. Policy shifts on collateralization or bidding standards can reallocate municipal and school balances rapidly. Transparent, competitive proposals reduce rotation risk and ease procurement scrutiny. Active community engagement and regular outreach strengthen standing with towns and school districts.

Infrastructure and transit funding

Federal Bipartisan Infrastructure Law totals $1.2 trillion nationally and continued FY2024/2025 federal and New Jersey capital programs boost demand for contractor and supplier lending, creating opportunities for Lakeland Bank's construction portfolio. Political delays or state budget impasses can stall pipelines and cash flow. Banks with specialized construction lending capture upside from timely execution. Monitoring appropriations cycles aids resource planning.

Housing and zoning priorities

Local zoning decisions shape Lakeland Bank’s residential and mixed-use lending pipeline; a U.S. housing shortfall of about 3.8 million units (Harvard JCHS, 2024) intensifies demand for mortgages and construction loans. Pro-housing stances in service areas expand origination and construction financing opportunities, while restrictive zoning limits deal flow and can depress appraisal values. Active participation in planning forums gives Lakeland early visibility into projects and pricing.

- Zoning impact on pipeline

- Pro-housing = more mortgage/construction loans

- Restrictive zoning reduces appraisal values

- Planning forums provide early project visibility

Cross-border regional dynamics

Tri-state political coordination (NJ-NY-PA) shapes labor mobility and business formation across a combined population of about 41.8 million (2023 Census estimates), affecting deposit and small-business loan demand; changes in state taxes or incentives have redirected capital and workforce in recent regional relocations. Advocacy on regional competitiveness influences community bank growth, so Lakeland Bank should monitor interstate policy differentials closely.

- Population: 41.8M (2023)

- Labor mobility: cross-border commuting alters deposit flows

- Tax/incentive shifts can move loan originations

- Advocacy affects regulatory environment for community banks

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

NJ political priorities and CRA expectations affect Lakeland Bank operations in a state of 9.3M residents. Municipal deposit wins depend on procurement across 565 NJ towns and school districts. Fed/state infrastructure funding ($1.2T national) and a 3.8M US housing shortfall boost construction and mortgage demand. Tri-state (41.8M) tax shifts alter deposit and loan flows.

| Metric | Value |

|---|---|

| NJ population | 9.3M |

| Tri-state pop | 41.8M |

| Housing shortfall | 3.8M |

| Infra funding (US) | $1.2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lakeland Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, using region-specific data and current trends. Designed for executives and investors, it highlights actionable threats, opportunities and forward-looking scenario insights ready for reports or decks.

A concise, visually segmented PESTLE summary for Lakeland Bank that distills external risks and opportunities into clear language, easily dropped into presentations or shared across teams; editable notes let users tailor insights to their region or business line for faster alignment and decision-making.

Economic factors

Interest rate cycle sensitivity

Net interest margin at Lakeland Bank is highly sensitive to Fed policy (federal funds ~5.25–5.50% in 2024–25) and deposit beta in a competitive New Jersey market (industry deposit betas commonly 40–60%), with rapid hikes compressing fixed-rate securities valuations and slowing loan originations while cuts raise deposit retention pressure. Balance-sheet hedging and disciplined loan/deposit pricing, supported by granular repricing analytics, are critical to protect margins.

SMB health in core counties

Local SMB vitality drives C&I lending, treasury services and deposits; New Jersey had about 672,000 small businesses in 2023 and small firms account for roughly 47.5% of private-sector employment (SBA). Retail, healthcare, logistics and professional services dominate many NJ submarkets. Recessions raise credit costs and downgrade risks; sector diversification and relationship banking bolster resilience.

Commercial real estate exposure

Commercial real estate exposure materially affects Lakeland Bank credit quality as office, multifamily and mixed-use performance diverge; national office vacancy was about 17% in Q4 2024 while industrial vacancy remained near 4% (CoStar, Q4 2024). Suburban office softness raises vacancy and refinance risk; conservative LTVs, rigorous tenant analysis and proactive borrower engagement improve workout outcomes.

Labor costs and productivity

Tight New Jersey labor markets (NJ average unemployment 3.9% in 2024, BLS) are elevating compensation for branch and tech talent while average hourly earnings rose ~4.1% y/y in 2024 (BLS), pressuring margins unless digital adoption offsets wage inflation; targeted automation could replace or augment up to ~30% of routine banking tasks (McKinsey 2024), and retention programs cut recruiting friction and service disruption.

- Labor tightness: NJ unemployment 3.9% (2024, BLS)

- Wage pressure: avg hourly earnings +4.1% y/y (2024, BLS)

- Automation potential: ~30% routine tasks (McKinsey 2024)

- Retention lowers hiring costs and service gaps

Household wealth and migration

Affluent suburbs around Lakeland Bank have median household incomes often above $100,000 (2022 ACS), supporting deposits, mortgages and wealth-management revenue. Continued domestic outmigration from New Jersey (Census trend 2010–2023) can erode local demand, though in-migration to transit-rich towns such as Hoboken and Jersey City has sustained housing and banking activity. Tailored mover and first-time-buyer products can capture churn.

- Affluent suburbs: median HH income >$100,000 (2022 ACS)

- Net NJ domestic outflow: Census trend 2010–2023

- Transit towns growth: Hoboken/Jersey City population gains

- Opportunity: mover and first-time-buyer products

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

Fed policy (fed funds 5.25–5.50% 2024–25) and deposit beta (40–60%) drive NIM sensitivity; hedging and repricing analytics are essential. NJ economy: unemployment 3.9% (2024) and 672,000 small businesses (2023) support C&I but raise wage pressure. CRE split: office vacancy ~17% Q4 2024 vs industrial ~4%, stressing selective underwriting.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| NJ unemployment | 3.9% (2024) |

| Small businesses | 672,000 (2023) |

| Office/Industrial | 17% / 4% (Q4 2024) |

| Median HH income | >$100,000 (2022) |

What You See Is What You Get

Lakeland Bank PESTLE Analysis

The preview shown here is the exact Lakeland Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, structure, and data visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic advantage with our PESTLE Analysis of Lakeland Bank—three to five concise sections revealing how political, economic, social, technological, legal, and environmental forces shape its prospects. Ideal for investors and strategists, this report translates external risks into actionable insights. Purchase the full analysis to download the complete, editable version and make data-driven decisions confidently.

Political factors

State banking policy alignment

New Jersey’s banking priorities—shaped by the 1977 Community Reinvestment Act framework and state agencies—directly affect community bank operations, grant access, and CRA expectations in a state of about 9.3 million residents. Alignment with NJEDA and municipal economic agendas can unlock small-business lending partnerships; small businesses represent roughly 99.9% of US firms. Misalignment can slow approvals or program access, so Lakeland Bank should keep proactive dialogue with state agencies and municipal leaders.

Municipal relationships and public deposits

Winning or retaining public sector deposits hinges on local political relationships and procurement processes, particularly in New Jersey where 565 municipalities compete for banking services. Policy shifts on collateralization or bidding standards can reallocate municipal and school balances rapidly. Transparent, competitive proposals reduce rotation risk and ease procurement scrutiny. Active community engagement and regular outreach strengthen standing with towns and school districts.

Infrastructure and transit funding

Federal Bipartisan Infrastructure Law totals $1.2 trillion nationally and continued FY2024/2025 federal and New Jersey capital programs boost demand for contractor and supplier lending, creating opportunities for Lakeland Bank's construction portfolio. Political delays or state budget impasses can stall pipelines and cash flow. Banks with specialized construction lending capture upside from timely execution. Monitoring appropriations cycles aids resource planning.

Housing and zoning priorities

Local zoning decisions shape Lakeland Bank’s residential and mixed-use lending pipeline; a U.S. housing shortfall of about 3.8 million units (Harvard JCHS, 2024) intensifies demand for mortgages and construction loans. Pro-housing stances in service areas expand origination and construction financing opportunities, while restrictive zoning limits deal flow and can depress appraisal values. Active participation in planning forums gives Lakeland early visibility into projects and pricing.

- Zoning impact on pipeline

- Pro-housing = more mortgage/construction loans

- Restrictive zoning reduces appraisal values

- Planning forums provide early project visibility

Cross-border regional dynamics

Tri-state political coordination (NJ-NY-PA) shapes labor mobility and business formation across a combined population of about 41.8 million (2023 Census estimates), affecting deposit and small-business loan demand; changes in state taxes or incentives have redirected capital and workforce in recent regional relocations. Advocacy on regional competitiveness influences community bank growth, so Lakeland Bank should monitor interstate policy differentials closely.

- Population: 41.8M (2023)

- Labor mobility: cross-border commuting alters deposit flows

- Tax/incentive shifts can move loan originations

- Advocacy affects regulatory environment for community banks

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

NJ political priorities and CRA expectations affect Lakeland Bank operations in a state of 9.3M residents. Municipal deposit wins depend on procurement across 565 NJ towns and school districts. Fed/state infrastructure funding ($1.2T national) and a 3.8M US housing shortfall boost construction and mortgage demand. Tri-state (41.8M) tax shifts alter deposit and loan flows.

| Metric | Value |

|---|---|

| NJ population | 9.3M |

| Tri-state pop | 41.8M |

| Housing shortfall | 3.8M |

| Infra funding (US) | $1.2T |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lakeland Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, using region-specific data and current trends. Designed for executives and investors, it highlights actionable threats, opportunities and forward-looking scenario insights ready for reports or decks.

A concise, visually segmented PESTLE summary for Lakeland Bank that distills external risks and opportunities into clear language, easily dropped into presentations or shared across teams; editable notes let users tailor insights to their region or business line for faster alignment and decision-making.

Economic factors

Interest rate cycle sensitivity

Net interest margin at Lakeland Bank is highly sensitive to Fed policy (federal funds ~5.25–5.50% in 2024–25) and deposit beta in a competitive New Jersey market (industry deposit betas commonly 40–60%), with rapid hikes compressing fixed-rate securities valuations and slowing loan originations while cuts raise deposit retention pressure. Balance-sheet hedging and disciplined loan/deposit pricing, supported by granular repricing analytics, are critical to protect margins.

SMB health in core counties

Local SMB vitality drives C&I lending, treasury services and deposits; New Jersey had about 672,000 small businesses in 2023 and small firms account for roughly 47.5% of private-sector employment (SBA). Retail, healthcare, logistics and professional services dominate many NJ submarkets. Recessions raise credit costs and downgrade risks; sector diversification and relationship banking bolster resilience.

Commercial real estate exposure

Commercial real estate exposure materially affects Lakeland Bank credit quality as office, multifamily and mixed-use performance diverge; national office vacancy was about 17% in Q4 2024 while industrial vacancy remained near 4% (CoStar, Q4 2024). Suburban office softness raises vacancy and refinance risk; conservative LTVs, rigorous tenant analysis and proactive borrower engagement improve workout outcomes.

Labor costs and productivity

Tight New Jersey labor markets (NJ average unemployment 3.9% in 2024, BLS) are elevating compensation for branch and tech talent while average hourly earnings rose ~4.1% y/y in 2024 (BLS), pressuring margins unless digital adoption offsets wage inflation; targeted automation could replace or augment up to ~30% of routine banking tasks (McKinsey 2024), and retention programs cut recruiting friction and service disruption.

- Labor tightness: NJ unemployment 3.9% (2024, BLS)

- Wage pressure: avg hourly earnings +4.1% y/y (2024, BLS)

- Automation potential: ~30% routine tasks (McKinsey 2024)

- Retention lowers hiring costs and service gaps

Household wealth and migration

Affluent suburbs around Lakeland Bank have median household incomes often above $100,000 (2022 ACS), supporting deposits, mortgages and wealth-management revenue. Continued domestic outmigration from New Jersey (Census trend 2010–2023) can erode local demand, though in-migration to transit-rich towns such as Hoboken and Jersey City has sustained housing and banking activity. Tailored mover and first-time-buyer products can capture churn.

- Affluent suburbs: median HH income >$100,000 (2022 ACS)

- Net NJ domestic outflow: Census trend 2010–2023

- Transit towns growth: Hoboken/Jersey City population gains

- Opportunity: mover and first-time-buyer products

NJ policy, procurement and tri-state tax shifts reshape deposits, mortgages and building

Fed policy (fed funds 5.25–5.50% 2024–25) and deposit beta (40–60%) drive NIM sensitivity; hedging and repricing analytics are essential. NJ economy: unemployment 3.9% (2024) and 672,000 small businesses (2023) support C&I but raise wage pressure. CRE split: office vacancy ~17% Q4 2024 vs industrial ~4%, stressing selective underwriting.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| NJ unemployment | 3.9% (2024) |

| Small businesses | 672,000 (2023) |

| Office/Industrial | 17% / 4% (Q4 2024) |

| Median HH income | >$100,000 (2022) |

What You See Is What You Get

Lakeland Bank PESTLE Analysis

The preview shown here is the exact Lakeland Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, structure, and data visible are identical to the downloadable file. No placeholders or teasers—this is the final, professionally structured document.