Lalique Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Lalique Group faces nuanced competitive dynamics—brand prestige offsets supplier leverage, while niche luxury positioning limits price sensitivity but heightens substitution risks as market tastes shift. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Lalique’s market pressures, force-by-force ratings, and strategic implications in detail. Get instant access to a consultant-grade report with visuals and Excel/Word deliverables to inform investment or strategy.

Suppliers Bargaining Power

Artisanal crystal inputs scarcity

In 2024 Lalique's artisanal crystal production depends on a handful of qualified suppliers for high-purity silica, specialty ashes, metals and colorants, while heritage-grade molds and kiln components remain niche and hard to substitute. This concentration raises switching costs and lead-time risk, often stretching procurement cycles. Suppliers thus retain leverage over quality specifications, delivery timelines and minimum order terms.

Master craftsmen and design talent

Lalique depends on scarce glassmakers, engravers and designers whose specialized skills are hard to replace, giving suppliers and talent significant leverage. Mobility of master craftsmen across luxury houses increases upward pressure on wages and scheduling flexibility. Union presence and regional labor dynamics in France and Europe can further strengthen bargaining positions. Preserving signature artistry requires above-market compensation and ongoing training investments.

Fragrance raw materials and perfumers

Major aroma suppliers such as Givaudan, Firmenich, IFF, Symrise and Mane dominate fragrance raw materials and captive molecules, concentrating bargaining power over Lalique Group. Star perfumers and specialist labs command premium fees and IP constraints that limit switching and raise formulation costs. Supply shocks in naturals (2023–24 jasmine and sandalwood shortages) increased price volatility and input costs. Exclusivity and allocation clauses in contracts further strengthen supplier influence.

Packaging, glass, and bottling partners

Packaging, glass, and bottling partners for Lalique supply luxury-grade flacons, caps, and decorative finishes that require precision vendors with limited global capacity, making suppliers strategically powerful.

Customization, MOQs (commonly 10,000–50,000 units) and tooling cycles (typical lead times 12–18 months) increase dependency and switching costs for Lalique.

Any quality deviation directly harms brand equity, amplifying vendor power; dual-sourcing is feasible but adds significant cost and time to qualify alternate vendors.

- Limited suppliers

- MOQs 10,000–50,000

- Tooling 12–18 months

- High switching costs

Hospitality F&B and property services

Premium food, wine, linens and specialist maintenance contractors materially inflate hotel and restaurant cost structures for Lalique-linked hospitality, with service-level agreements commonly spanning 3–5 years and limiting rapid renegotiation. Local supplier concentration and strong seasonality reduce sourcing flexibility and can push spot prices higher during peak periods. Energy and utilities represent roughly 5% of hotel operating costs, adding fixed-cost leverage.

- SLAs: 3–5 years

- Energy share: ~5% of operating costs

- Seasonality: raises spot prices during peaks

- Local monopolies: reduce supplier bargaining power

High supplier leverage: concentrated perfumers, large MOQs, long tooling and SLAs raise input risk

Lalique faces high supplier leverage: concentrated high-purity materials and top perfumers (Givaudan/IFF etc.) raise input risk; MOQs 10,000–50,000 and tooling 12–18 months amplify switching costs; SLAs (3–5 yrs) and energy ~5% of hotel Opex constrain renegotiation and raise cost volatility.

| Metric | Value |

|---|---|

| Top fragrance suppliers | 5 (Givaudan, IFF, Firmenich, Symrise, Mane) |

| MOQs | 10,000–50,000 |

| Tooling lead time | 12–18 months |

| SLAs | 3–5 years |

| Energy share (hotel) | ~5% |

What is included in the product

Concise Porter's Five Forces analysis for Lalique Group, uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers that influence pricing, margins, and long-term brand resilience.

A concise one-sheet Porter's Five Forces for Lalique Group that instantly visualizes competitive pressures via a spider chart, perfect for quick strategic decisions; customize force levels for new trends or scenarios and drop it straight into pitch decks or boardroom slides—no macros, easy for non-finance users.

Customers Bargaining Power

Affluent individual collectors

Affluent collectors exhibit low price sensitivity due to high willingness to pay, yet they are highly discerning on provenance and design, demanding museum-quality authenticity and limited editions. Switching to peer maisons is feasible when uniqueness is lacking, increasing competitive pressure. Personalized service expectations raise Lalique’s cost-to-serve, while word-of-mouth and the pre-owned luxury market (about $32bn in 2023, rising toward $50bn by 2025) amplify buyers’ leverage.

Retailers, distributors, travel retail

Channel partners aggregate demand to negotiate margins (typically 25–40%), payment terms and co‑op marketing; Lalique faces shelf‑space trades that can drive discounts up to ~30%. Consolidated retailers—top chains controlling about 50% of fragrance shelf in key markets—increase negotiating leverage. Performance‑based rebates and returns clauses commonly erode 5–15% of invoiced value, pressuring profitability.

Hospitality guests and event clients

Luxury guests compare boutique properties on experience and brand story, with OTAs and review platforms driving transparency as OTAs account for roughly 50% of online bookings in hospitality; online reviews now shape purchase decisions at scale. Corporate events, which can represent up to 20% of hotel revenue, push for bespoke packages and rate concessions. Occupancy volatility—often dropping into off-peak single digits for some properties—gives buyers clear leverage.

Corporate gifting and B2B décor

Corporate gifting and B2B décor buyers exert strong bargaining power: bulk orders for gifts or interior projects drive price negotiation and customization demands, with corporate procurement often enforcing competitive bids and budget-cycle timing that favor suppliers meeting formal RFPs. Lead-time and logistics reliability are decisive—lost deadlines cost large contracts—while value-added engraving or co-branding can justify premiums and offset typical discount pressure.

- Bulk orders: leverage for 10–25% discounts

- Procurement: formal RFPs, quarterly/annual cycles

- Logistics: on-time delivery wins 70% of repeat B2B contracts

- Value-add: co-branding/engraving raises perceived value

Fragrance and beauty consumers

Fragrance and beauty consumers wield strong comparison power as the category is crowded across mass, prestige and niche tiers; e-commerce penetration (~30% of beauty sales in 2024) amplifies price and feature transparency. High trialability from sampling and continual product launches raises switching rates, while online reviews and sampling platforms expand perceived choice. Competitor bundle promotions compress perceived value, forcing Lalique to defend margins and differentiation.

- High e-commerce transparency — ~30% beauty online (2024)

- Frequent launches increase switching

- Bundles erode price premium

HNW need provenance; 30% online and $32bn market raise buyer leverage

High-net-worth collectors show low price sensitivity but demand provenance and limited editions, raising switching risk if uniqueness falters. Retail partners and B2B buyers exert margin pressure (retailer discounts up to 30%, bulk B2B discounts 10–25%), while e-commerce transparency (~30% beauty online in 2024) and a $32bn pre-owned market (2023) amplify buyer leverage.

| Metric | Value |

|---|---|

| Beauty e‑commerce (2024) | ~30% |

| Pre‑owned luxury (2023) | $32bn |

| Retailer discounts | up to 30% |

| Bulk B2B discounts | 10–25% |

Full Version Awaits

Lalique Group Porter's Five Forces Analysis

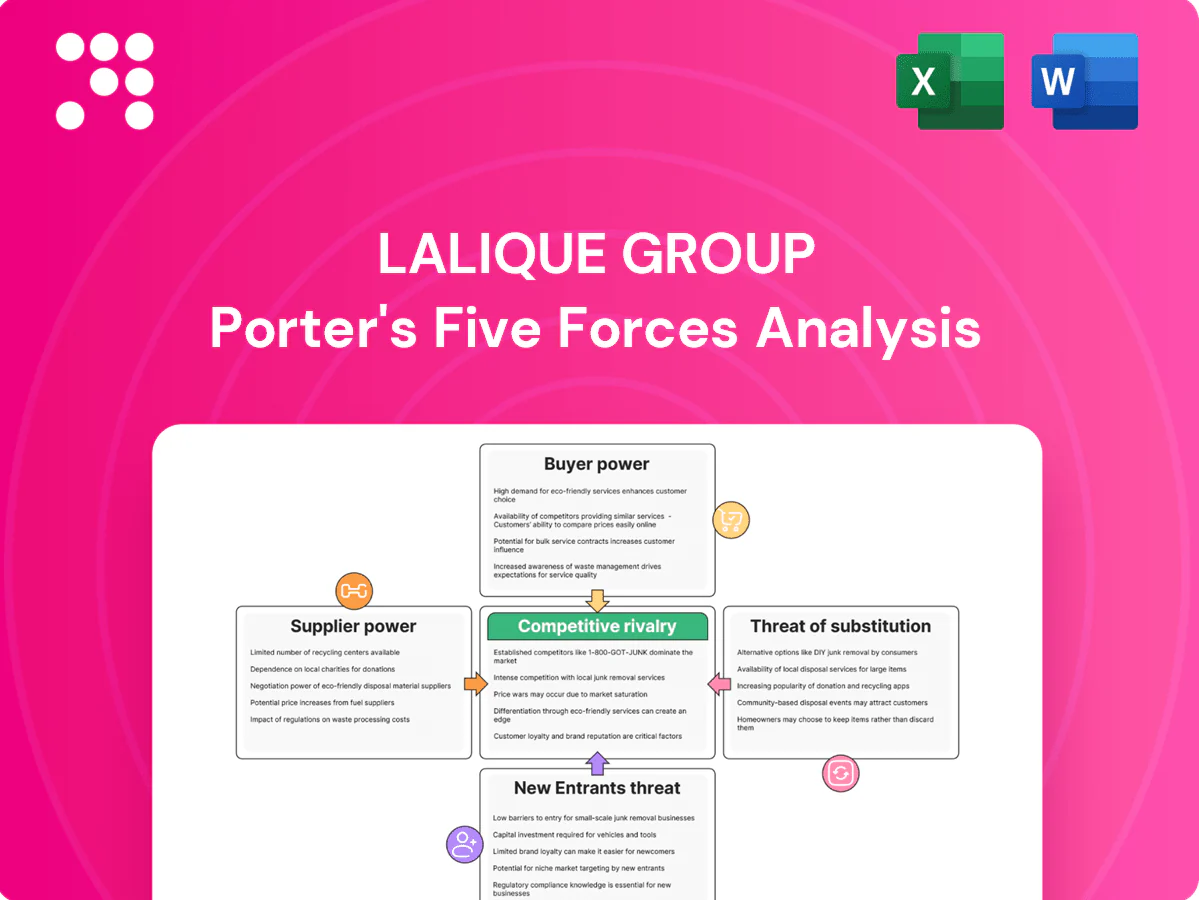

The Porter's Five Forces analysis examines Lalique Group's supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and the impact of brand heritage across its crystal, perfume and luxury segments. It evaluates margins, distribution channels, and barriers to entry to quantify bargaining dynamics and strategic risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

A Must-Have Tool for Decision-Makers

Lalique Group faces nuanced competitive dynamics—brand prestige offsets supplier leverage, while niche luxury positioning limits price sensitivity but heightens substitution risks as market tastes shift. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Lalique’s market pressures, force-by-force ratings, and strategic implications in detail. Get instant access to a consultant-grade report with visuals and Excel/Word deliverables to inform investment or strategy.

Suppliers Bargaining Power

Artisanal crystal inputs scarcity

In 2024 Lalique's artisanal crystal production depends on a handful of qualified suppliers for high-purity silica, specialty ashes, metals and colorants, while heritage-grade molds and kiln components remain niche and hard to substitute. This concentration raises switching costs and lead-time risk, often stretching procurement cycles. Suppliers thus retain leverage over quality specifications, delivery timelines and minimum order terms.

Master craftsmen and design talent

Lalique depends on scarce glassmakers, engravers and designers whose specialized skills are hard to replace, giving suppliers and talent significant leverage. Mobility of master craftsmen across luxury houses increases upward pressure on wages and scheduling flexibility. Union presence and regional labor dynamics in France and Europe can further strengthen bargaining positions. Preserving signature artistry requires above-market compensation and ongoing training investments.

Fragrance raw materials and perfumers

Major aroma suppliers such as Givaudan, Firmenich, IFF, Symrise and Mane dominate fragrance raw materials and captive molecules, concentrating bargaining power over Lalique Group. Star perfumers and specialist labs command premium fees and IP constraints that limit switching and raise formulation costs. Supply shocks in naturals (2023–24 jasmine and sandalwood shortages) increased price volatility and input costs. Exclusivity and allocation clauses in contracts further strengthen supplier influence.

Packaging, glass, and bottling partners

Packaging, glass, and bottling partners for Lalique supply luxury-grade flacons, caps, and decorative finishes that require precision vendors with limited global capacity, making suppliers strategically powerful.

Customization, MOQs (commonly 10,000–50,000 units) and tooling cycles (typical lead times 12–18 months) increase dependency and switching costs for Lalique.

Any quality deviation directly harms brand equity, amplifying vendor power; dual-sourcing is feasible but adds significant cost and time to qualify alternate vendors.

- Limited suppliers

- MOQs 10,000–50,000

- Tooling 12–18 months

- High switching costs

Hospitality F&B and property services

Premium food, wine, linens and specialist maintenance contractors materially inflate hotel and restaurant cost structures for Lalique-linked hospitality, with service-level agreements commonly spanning 3–5 years and limiting rapid renegotiation. Local supplier concentration and strong seasonality reduce sourcing flexibility and can push spot prices higher during peak periods. Energy and utilities represent roughly 5% of hotel operating costs, adding fixed-cost leverage.

- SLAs: 3–5 years

- Energy share: ~5% of operating costs

- Seasonality: raises spot prices during peaks

- Local monopolies: reduce supplier bargaining power

High supplier leverage: concentrated perfumers, large MOQs, long tooling and SLAs raise input risk

Lalique faces high supplier leverage: concentrated high-purity materials and top perfumers (Givaudan/IFF etc.) raise input risk; MOQs 10,000–50,000 and tooling 12–18 months amplify switching costs; SLAs (3–5 yrs) and energy ~5% of hotel Opex constrain renegotiation and raise cost volatility.

| Metric | Value |

|---|---|

| Top fragrance suppliers | 5 (Givaudan, IFF, Firmenich, Symrise, Mane) |

| MOQs | 10,000–50,000 |

| Tooling lead time | 12–18 months |

| SLAs | 3–5 years |

| Energy share (hotel) | ~5% |

What is included in the product

Concise Porter's Five Forces analysis for Lalique Group, uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers that influence pricing, margins, and long-term brand resilience.

A concise one-sheet Porter's Five Forces for Lalique Group that instantly visualizes competitive pressures via a spider chart, perfect for quick strategic decisions; customize force levels for new trends or scenarios and drop it straight into pitch decks or boardroom slides—no macros, easy for non-finance users.

Customers Bargaining Power

Affluent individual collectors

Affluent collectors exhibit low price sensitivity due to high willingness to pay, yet they are highly discerning on provenance and design, demanding museum-quality authenticity and limited editions. Switching to peer maisons is feasible when uniqueness is lacking, increasing competitive pressure. Personalized service expectations raise Lalique’s cost-to-serve, while word-of-mouth and the pre-owned luxury market (about $32bn in 2023, rising toward $50bn by 2025) amplify buyers’ leverage.

Retailers, distributors, travel retail

Channel partners aggregate demand to negotiate margins (typically 25–40%), payment terms and co‑op marketing; Lalique faces shelf‑space trades that can drive discounts up to ~30%. Consolidated retailers—top chains controlling about 50% of fragrance shelf in key markets—increase negotiating leverage. Performance‑based rebates and returns clauses commonly erode 5–15% of invoiced value, pressuring profitability.

Hospitality guests and event clients

Luxury guests compare boutique properties on experience and brand story, with OTAs and review platforms driving transparency as OTAs account for roughly 50% of online bookings in hospitality; online reviews now shape purchase decisions at scale. Corporate events, which can represent up to 20% of hotel revenue, push for bespoke packages and rate concessions. Occupancy volatility—often dropping into off-peak single digits for some properties—gives buyers clear leverage.

Corporate gifting and B2B décor

Corporate gifting and B2B décor buyers exert strong bargaining power: bulk orders for gifts or interior projects drive price negotiation and customization demands, with corporate procurement often enforcing competitive bids and budget-cycle timing that favor suppliers meeting formal RFPs. Lead-time and logistics reliability are decisive—lost deadlines cost large contracts—while value-added engraving or co-branding can justify premiums and offset typical discount pressure.

- Bulk orders: leverage for 10–25% discounts

- Procurement: formal RFPs, quarterly/annual cycles

- Logistics: on-time delivery wins 70% of repeat B2B contracts

- Value-add: co-branding/engraving raises perceived value

Fragrance and beauty consumers

Fragrance and beauty consumers wield strong comparison power as the category is crowded across mass, prestige and niche tiers; e-commerce penetration (~30% of beauty sales in 2024) amplifies price and feature transparency. High trialability from sampling and continual product launches raises switching rates, while online reviews and sampling platforms expand perceived choice. Competitor bundle promotions compress perceived value, forcing Lalique to defend margins and differentiation.

- High e-commerce transparency — ~30% beauty online (2024)

- Frequent launches increase switching

- Bundles erode price premium

HNW need provenance; 30% online and $32bn market raise buyer leverage

High-net-worth collectors show low price sensitivity but demand provenance and limited editions, raising switching risk if uniqueness falters. Retail partners and B2B buyers exert margin pressure (retailer discounts up to 30%, bulk B2B discounts 10–25%), while e-commerce transparency (~30% beauty online in 2024) and a $32bn pre-owned market (2023) amplify buyer leverage.

| Metric | Value |

|---|---|

| Beauty e‑commerce (2024) | ~30% |

| Pre‑owned luxury (2023) | $32bn |

| Retailer discounts | up to 30% |

| Bulk B2B discounts | 10–25% |

Full Version Awaits

Lalique Group Porter's Five Forces Analysis

The Porter's Five Forces analysis examines Lalique Group's supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and the impact of brand heritage across its crystal, perfume and luxury segments. It evaluates margins, distribution channels, and barriers to entry to quantify bargaining dynamics and strategic risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Description

A Must-Have Tool for Decision-Makers

Lalique Group faces nuanced competitive dynamics—brand prestige offsets supplier leverage, while niche luxury positioning limits price sensitivity but heightens substitution risks as market tastes shift. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Lalique’s market pressures, force-by-force ratings, and strategic implications in detail. Get instant access to a consultant-grade report with visuals and Excel/Word deliverables to inform investment or strategy.

Suppliers Bargaining Power

Artisanal crystal inputs scarcity

In 2024 Lalique's artisanal crystal production depends on a handful of qualified suppliers for high-purity silica, specialty ashes, metals and colorants, while heritage-grade molds and kiln components remain niche and hard to substitute. This concentration raises switching costs and lead-time risk, often stretching procurement cycles. Suppliers thus retain leverage over quality specifications, delivery timelines and minimum order terms.

Master craftsmen and design talent

Lalique depends on scarce glassmakers, engravers and designers whose specialized skills are hard to replace, giving suppliers and talent significant leverage. Mobility of master craftsmen across luxury houses increases upward pressure on wages and scheduling flexibility. Union presence and regional labor dynamics in France and Europe can further strengthen bargaining positions. Preserving signature artistry requires above-market compensation and ongoing training investments.

Fragrance raw materials and perfumers

Major aroma suppliers such as Givaudan, Firmenich, IFF, Symrise and Mane dominate fragrance raw materials and captive molecules, concentrating bargaining power over Lalique Group. Star perfumers and specialist labs command premium fees and IP constraints that limit switching and raise formulation costs. Supply shocks in naturals (2023–24 jasmine and sandalwood shortages) increased price volatility and input costs. Exclusivity and allocation clauses in contracts further strengthen supplier influence.

Packaging, glass, and bottling partners

Packaging, glass, and bottling partners for Lalique supply luxury-grade flacons, caps, and decorative finishes that require precision vendors with limited global capacity, making suppliers strategically powerful.

Customization, MOQs (commonly 10,000–50,000 units) and tooling cycles (typical lead times 12–18 months) increase dependency and switching costs for Lalique.

Any quality deviation directly harms brand equity, amplifying vendor power; dual-sourcing is feasible but adds significant cost and time to qualify alternate vendors.

- Limited suppliers

- MOQs 10,000–50,000

- Tooling 12–18 months

- High switching costs

Hospitality F&B and property services

Premium food, wine, linens and specialist maintenance contractors materially inflate hotel and restaurant cost structures for Lalique-linked hospitality, with service-level agreements commonly spanning 3–5 years and limiting rapid renegotiation. Local supplier concentration and strong seasonality reduce sourcing flexibility and can push spot prices higher during peak periods. Energy and utilities represent roughly 5% of hotel operating costs, adding fixed-cost leverage.

- SLAs: 3–5 years

- Energy share: ~5% of operating costs

- Seasonality: raises spot prices during peaks

- Local monopolies: reduce supplier bargaining power

High supplier leverage: concentrated perfumers, large MOQs, long tooling and SLAs raise input risk

Lalique faces high supplier leverage: concentrated high-purity materials and top perfumers (Givaudan/IFF etc.) raise input risk; MOQs 10,000–50,000 and tooling 12–18 months amplify switching costs; SLAs (3–5 yrs) and energy ~5% of hotel Opex constrain renegotiation and raise cost volatility.

| Metric | Value |

|---|---|

| Top fragrance suppliers | 5 (Givaudan, IFF, Firmenich, Symrise, Mane) |

| MOQs | 10,000–50,000 |

| Tooling lead time | 12–18 months |

| SLAs | 3–5 years |

| Energy share (hotel) | ~5% |

What is included in the product

Concise Porter's Five Forces analysis for Lalique Group, uncovering competitive intensity, supplier and buyer power, threats from substitutes and new entrants, and strategic levers that influence pricing, margins, and long-term brand resilience.

A concise one-sheet Porter's Five Forces for Lalique Group that instantly visualizes competitive pressures via a spider chart, perfect for quick strategic decisions; customize force levels for new trends or scenarios and drop it straight into pitch decks or boardroom slides—no macros, easy for non-finance users.

Customers Bargaining Power

Affluent individual collectors

Affluent collectors exhibit low price sensitivity due to high willingness to pay, yet they are highly discerning on provenance and design, demanding museum-quality authenticity and limited editions. Switching to peer maisons is feasible when uniqueness is lacking, increasing competitive pressure. Personalized service expectations raise Lalique’s cost-to-serve, while word-of-mouth and the pre-owned luxury market (about $32bn in 2023, rising toward $50bn by 2025) amplify buyers’ leverage.

Retailers, distributors, travel retail

Channel partners aggregate demand to negotiate margins (typically 25–40%), payment terms and co‑op marketing; Lalique faces shelf‑space trades that can drive discounts up to ~30%. Consolidated retailers—top chains controlling about 50% of fragrance shelf in key markets—increase negotiating leverage. Performance‑based rebates and returns clauses commonly erode 5–15% of invoiced value, pressuring profitability.

Hospitality guests and event clients

Luxury guests compare boutique properties on experience and brand story, with OTAs and review platforms driving transparency as OTAs account for roughly 50% of online bookings in hospitality; online reviews now shape purchase decisions at scale. Corporate events, which can represent up to 20% of hotel revenue, push for bespoke packages and rate concessions. Occupancy volatility—often dropping into off-peak single digits for some properties—gives buyers clear leverage.

Corporate gifting and B2B décor

Corporate gifting and B2B décor buyers exert strong bargaining power: bulk orders for gifts or interior projects drive price negotiation and customization demands, with corporate procurement often enforcing competitive bids and budget-cycle timing that favor suppliers meeting formal RFPs. Lead-time and logistics reliability are decisive—lost deadlines cost large contracts—while value-added engraving or co-branding can justify premiums and offset typical discount pressure.

- Bulk orders: leverage for 10–25% discounts

- Procurement: formal RFPs, quarterly/annual cycles

- Logistics: on-time delivery wins 70% of repeat B2B contracts

- Value-add: co-branding/engraving raises perceived value

Fragrance and beauty consumers

Fragrance and beauty consumers wield strong comparison power as the category is crowded across mass, prestige and niche tiers; e-commerce penetration (~30% of beauty sales in 2024) amplifies price and feature transparency. High trialability from sampling and continual product launches raises switching rates, while online reviews and sampling platforms expand perceived choice. Competitor bundle promotions compress perceived value, forcing Lalique to defend margins and differentiation.

- High e-commerce transparency — ~30% beauty online (2024)

- Frequent launches increase switching

- Bundles erode price premium

HNW need provenance; 30% online and $32bn market raise buyer leverage

High-net-worth collectors show low price sensitivity but demand provenance and limited editions, raising switching risk if uniqueness falters. Retail partners and B2B buyers exert margin pressure (retailer discounts up to 30%, bulk B2B discounts 10–25%), while e-commerce transparency (~30% beauty online in 2024) and a $32bn pre-owned market (2023) amplify buyer leverage.

| Metric | Value |

|---|---|

| Beauty e‑commerce (2024) | ~30% |

| Pre‑owned luxury (2023) | $32bn |

| Retailer discounts | up to 30% |

| Bulk B2B discounts | 10–25% |

Full Version Awaits

Lalique Group Porter's Five Forces Analysis

The Porter's Five Forces analysis examines Lalique Group's supplier and buyer power, competitive rivalry, threats of new entrants and substitutes, and the impact of brand heritage across its crystal, perfume and luxury segments. It evaluates margins, distribution channels, and barriers to entry to quantify bargaining dynamics and strategic risks. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.