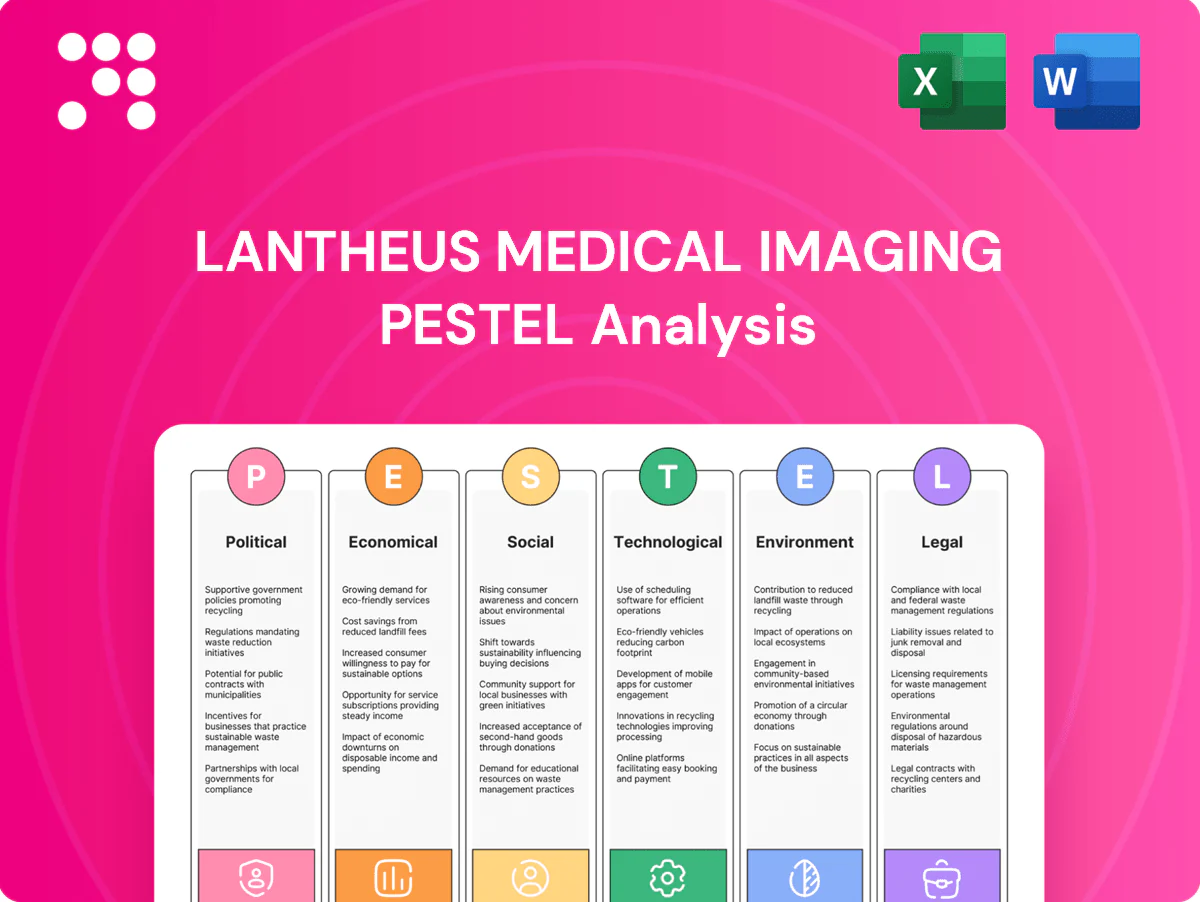

Lantheus Medical Imaging PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how regulatory shifts, reimbursement trends, and imaging technology advances are shaping Lantheus Medical Imaging's strategic outlook. Our concise PESTLE highlights key political, economic, social, technological, legal, and environmental risks and opportunities for investors and strategists. Ready-made and actionable—purchase the full analysis for the complete, editable report.

Political factors

Healthcare policy and reimbursement

Government payers determine coverage, coding and payment rates for imaging and radiopharmaceuticals, directly shaping Lantheus adoption among roughly 66 million Medicare beneficiaries. EU HTA regulation (entered into application Jan 2025) and national formularies can speed or block market access. Value-based care and outcome-based contracting favor agents with measurable clinical impact, while IRA-driven drug price negotiation (starting 2026) and broader cost-containment debate increase pricing scrutiny.

Regulatory approval priorities

Agency focus on diagnostics and theranostics has driven variable review speeds, with 2024 regulators prioritizing novel imaging agents over generic filings. Fast-track or breakthrough pathways materially shorten review windows and can accelerate market access for Lantheus pipeline assets. Rising post-market evidence requirements increase lifecycle compliance costs, while limited global harmonization complicates multi-region filings and labeling.

Nuclear material governance

Nuclear material governance shapes Lantheus supply: policies on isotope production and cross-border movement affect reliability, with five aging reactors historically supplying roughly 70% of global Mo-99. Export controls plus NRC and IAEA oversight add compliance complexity and costs. Geopolitical tensions have intermittently disrupted Mo-99, Lu-177 and scarce Ac-225 chains. Government investments (DOE and USDA grants, public reactor/cyclotron funding) aim to stabilize sourcing.

Trade and tariff exposure

Tariffs on chemicals, APIs and equipment increase COGS for imaging agents; short half-life radiopharmaceuticals such as Tc-99m (half-life ~6 hours) and F-18 (half-life ~110 minutes) make customs delays materially damaging. Localization incentives in EU/US/Japan push regional manufacturing, while trade agreements reduce cross-border frictions for critical market flows.

- Tariffs raise COGS for reagents and kits

- Short half-lives (Tc-99m 6h, F-18 110min) make delays costly

- Localization incentives steer plant placement

- Trade pacts ease EU/US/Japan supply chains

Public health priorities

Oncology and cardiology initiatives increasingly steer public funding toward advanced imaging pathways, with PSMA and cardiac PET uptake accelerated by FDA PSMA agent approvals in 2020–2021; screening and guideline updates directly raise demand for specific radiopharmaceuticals. Pandemic readiness policies reshaped hospital throughput, with elective imaging volumes falling about 50% at COVID peaks, stressing throughput planning. National cancer plans now often explicitly prioritize PSMA and other precision modalities.

- Increased targeted funding: drives demand for PET agents

- Guideline changes: create stepwise volume lifts for specific tracers

- Pandemic impact: ~50% elective imaging decline at peaks

- National plans: prioritize PSMA and precision imaging

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

Government payers (≈66M Medicare beneficiaries) and IRA price negotiation (starts 2026) increase reimbursement and pricing pressure on Lantheus products.

Regulatory fast-track pathways shorten approvals for novel imaging agents while rising post-market evidence and fragmented HTA (EU HTA in force Jan 2025) raise lifecycle costs.

Isotope supply risk remains material: five reactors supply ≈70% of Mo-99; Tc-99m half-life 6h, F-18 110min; elective imaging fell ~50% at COVID peaks.

| Metric | Value |

|---|---|

| Medicare beneficiaries | ≈66M |

| Mo-99 supply | ≈70% from 5 reactors |

| IRA negotiation | Starts 2026 |

| Tc-99m / F-18 half-life | 6h / 110min |

| Elective imaging drop (COVID peaks) | ≈50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Lantheus Medical Imaging across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable implications tailored for executives, investors and strategists aiming to identify risks and growth opportunities.

A concise, visually segmented PESTLE summary of Lantheus Medical Imaging that relieves briefing pain points by delivering clear external risk factors and market positioning for quick insertion into presentations or strategy sessions.

Economic factors

Macro cycles and budgets

Hospital and imaging-center budgets track macro cycles as GDP growth and rate cycles compress capital plans; US policy rates stood at 5.25–5.50% mid-2025, tightening credit and raising funding costs. Higher WACC delays capital and formulary additions, while procedure volumes rebounded to near pre‑pandemic levels by 2024. Recessionary pressure intensifies purchasing and tender price competition, forcing deeper concessions.

Payer mix and pricing power

Shift toward managed care, which covers over 60% of US lives, can compress net pricing for Lantheus as payers demand deeper discounts and capitated contracts. DRG and APC reimbursement structures continue to define site-of-care economics, favoring lower-cost outpatient settings and pressuring hospital-based imaging margins. Robust outcomes and pharmacoeconomic data are increasingly required to defend prices, while international reference pricing used by over 20 countries can echo into export markets.

Supply cost volatility

Isotope feedstock and energy price swings materially pressure margins for Lantheus, since Mo-99/Tc-99m sourcing and plant power can shift COGS; management noted cost-of-goods sold sensitivity to feedstock and utilities in recent filings. Cold-chain and hazmat shipping costs, which rise with jet/diesel fuel, increased transport spend notably during 2022–2023 fuel spikes, raising per-shipment costs. Investments in redundancy—backup generators, alternate suppliers and inventory—limit outage risk but raise fixed operating costs and capex. High vendor concentration for key radionuclide supply amplifies bargaining exposure and pricing pass-through risk.

FX and global exposure

Revenue and costs denominated in multiple currencies expose Lantheus to translation and transaction risk across its US, Europe and APAC operations; hedging programs reduce but do not eliminate quarterly EPS volatility. Price corridors and reimbursement caps in many ex-US markets constrain full pass-through of USD price changes. Rapid emerging market uptake supports volume growth but at materially lower average selling prices, compressing margins.

- FX translation/transaction risk

- Hedging mitigates but not eliminates volatility

- Price corridors limit ex-US pass-through

- Emerging markets = higher volume, lower ASPs

Competition and lifecycle

New imaging agents and biosimilars threaten Lantheus mature franchises; Pylarify (piflufolastat F 18) approval in 2021 shifted focus to growth areas while older diagnostic agents face pricing pressure. Patent cliffs and LOEs force mix shifts and higher rebates, and consolidation among peers alters negotiating leverage. Pipeline successes re-rate growth expectations and capital allocation rapidly.

- Pylarify approval: 2021

- LOE risk: increases rebate pressure and mix shift

- M&A: raises counterparty negotiating power

- Pipeline wins: can materially re-rate valuation

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

High US policy rates (5.25–5.50% mid‑2025) raise WACC, delaying capex and compressing hospital imaging budgets. Managed care covers >60% US lives, pressuring net pricing and margins; DRG/APC shifts favor lower‑cost sites. Mo‑99/Tc‑99m feedstock and fuel volatility raise COGS; FX exposure across US/EU/APAC creates EPS volatility despite hedging.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| Managed care | >60% US lives |

| Mo‑99 supplier concentration | High |

What You See Is What You Get

Lantheus Medical Imaging PESTLE Analysis

This PESTLE analysis of Lantheus Medical Imaging examines political, economic, social, technological, legal, and environmental factors shaping the company’s strategic outlook. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It is the final, ready-to-download file with no placeholders or surprises.

Your Shortcut to Market Insight Starts Here

Discover how regulatory shifts, reimbursement trends, and imaging technology advances are shaping Lantheus Medical Imaging's strategic outlook. Our concise PESTLE highlights key political, economic, social, technological, legal, and environmental risks and opportunities for investors and strategists. Ready-made and actionable—purchase the full analysis for the complete, editable report.

Political factors

Healthcare policy and reimbursement

Government payers determine coverage, coding and payment rates for imaging and radiopharmaceuticals, directly shaping Lantheus adoption among roughly 66 million Medicare beneficiaries. EU HTA regulation (entered into application Jan 2025) and national formularies can speed or block market access. Value-based care and outcome-based contracting favor agents with measurable clinical impact, while IRA-driven drug price negotiation (starting 2026) and broader cost-containment debate increase pricing scrutiny.

Regulatory approval priorities

Agency focus on diagnostics and theranostics has driven variable review speeds, with 2024 regulators prioritizing novel imaging agents over generic filings. Fast-track or breakthrough pathways materially shorten review windows and can accelerate market access for Lantheus pipeline assets. Rising post-market evidence requirements increase lifecycle compliance costs, while limited global harmonization complicates multi-region filings and labeling.

Nuclear material governance

Nuclear material governance shapes Lantheus supply: policies on isotope production and cross-border movement affect reliability, with five aging reactors historically supplying roughly 70% of global Mo-99. Export controls plus NRC and IAEA oversight add compliance complexity and costs. Geopolitical tensions have intermittently disrupted Mo-99, Lu-177 and scarce Ac-225 chains. Government investments (DOE and USDA grants, public reactor/cyclotron funding) aim to stabilize sourcing.

Trade and tariff exposure

Tariffs on chemicals, APIs and equipment increase COGS for imaging agents; short half-life radiopharmaceuticals such as Tc-99m (half-life ~6 hours) and F-18 (half-life ~110 minutes) make customs delays materially damaging. Localization incentives in EU/US/Japan push regional manufacturing, while trade agreements reduce cross-border frictions for critical market flows.

- Tariffs raise COGS for reagents and kits

- Short half-lives (Tc-99m 6h, F-18 110min) make delays costly

- Localization incentives steer plant placement

- Trade pacts ease EU/US/Japan supply chains

Public health priorities

Oncology and cardiology initiatives increasingly steer public funding toward advanced imaging pathways, with PSMA and cardiac PET uptake accelerated by FDA PSMA agent approvals in 2020–2021; screening and guideline updates directly raise demand for specific radiopharmaceuticals. Pandemic readiness policies reshaped hospital throughput, with elective imaging volumes falling about 50% at COVID peaks, stressing throughput planning. National cancer plans now often explicitly prioritize PSMA and other precision modalities.

- Increased targeted funding: drives demand for PET agents

- Guideline changes: create stepwise volume lifts for specific tracers

- Pandemic impact: ~50% elective imaging decline at peaks

- National plans: prioritize PSMA and precision imaging

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

Government payers (≈66M Medicare beneficiaries) and IRA price negotiation (starts 2026) increase reimbursement and pricing pressure on Lantheus products.

Regulatory fast-track pathways shorten approvals for novel imaging agents while rising post-market evidence and fragmented HTA (EU HTA in force Jan 2025) raise lifecycle costs.

Isotope supply risk remains material: five reactors supply ≈70% of Mo-99; Tc-99m half-life 6h, F-18 110min; elective imaging fell ~50% at COVID peaks.

| Metric | Value |

|---|---|

| Medicare beneficiaries | ≈66M |

| Mo-99 supply | ≈70% from 5 reactors |

| IRA negotiation | Starts 2026 |

| Tc-99m / F-18 half-life | 6h / 110min |

| Elective imaging drop (COVID peaks) | ≈50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Lantheus Medical Imaging across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable implications tailored for executives, investors and strategists aiming to identify risks and growth opportunities.

A concise, visually segmented PESTLE summary of Lantheus Medical Imaging that relieves briefing pain points by delivering clear external risk factors and market positioning for quick insertion into presentations or strategy sessions.

Economic factors

Macro cycles and budgets

Hospital and imaging-center budgets track macro cycles as GDP growth and rate cycles compress capital plans; US policy rates stood at 5.25–5.50% mid-2025, tightening credit and raising funding costs. Higher WACC delays capital and formulary additions, while procedure volumes rebounded to near pre‑pandemic levels by 2024. Recessionary pressure intensifies purchasing and tender price competition, forcing deeper concessions.

Payer mix and pricing power

Shift toward managed care, which covers over 60% of US lives, can compress net pricing for Lantheus as payers demand deeper discounts and capitated contracts. DRG and APC reimbursement structures continue to define site-of-care economics, favoring lower-cost outpatient settings and pressuring hospital-based imaging margins. Robust outcomes and pharmacoeconomic data are increasingly required to defend prices, while international reference pricing used by over 20 countries can echo into export markets.

Supply cost volatility

Isotope feedstock and energy price swings materially pressure margins for Lantheus, since Mo-99/Tc-99m sourcing and plant power can shift COGS; management noted cost-of-goods sold sensitivity to feedstock and utilities in recent filings. Cold-chain and hazmat shipping costs, which rise with jet/diesel fuel, increased transport spend notably during 2022–2023 fuel spikes, raising per-shipment costs. Investments in redundancy—backup generators, alternate suppliers and inventory—limit outage risk but raise fixed operating costs and capex. High vendor concentration for key radionuclide supply amplifies bargaining exposure and pricing pass-through risk.

FX and global exposure

Revenue and costs denominated in multiple currencies expose Lantheus to translation and transaction risk across its US, Europe and APAC operations; hedging programs reduce but do not eliminate quarterly EPS volatility. Price corridors and reimbursement caps in many ex-US markets constrain full pass-through of USD price changes. Rapid emerging market uptake supports volume growth but at materially lower average selling prices, compressing margins.

- FX translation/transaction risk

- Hedging mitigates but not eliminates volatility

- Price corridors limit ex-US pass-through

- Emerging markets = higher volume, lower ASPs

Competition and lifecycle

New imaging agents and biosimilars threaten Lantheus mature franchises; Pylarify (piflufolastat F 18) approval in 2021 shifted focus to growth areas while older diagnostic agents face pricing pressure. Patent cliffs and LOEs force mix shifts and higher rebates, and consolidation among peers alters negotiating leverage. Pipeline successes re-rate growth expectations and capital allocation rapidly.

- Pylarify approval: 2021

- LOE risk: increases rebate pressure and mix shift

- M&A: raises counterparty negotiating power

- Pipeline wins: can materially re-rate valuation

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

High US policy rates (5.25–5.50% mid‑2025) raise WACC, delaying capex and compressing hospital imaging budgets. Managed care covers >60% US lives, pressuring net pricing and margins; DRG/APC shifts favor lower‑cost sites. Mo‑99/Tc‑99m feedstock and fuel volatility raise COGS; FX exposure across US/EU/APAC creates EPS volatility despite hedging.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| Managed care | >60% US lives |

| Mo‑99 supplier concentration | High |

What You See Is What You Get

Lantheus Medical Imaging PESTLE Analysis

This PESTLE analysis of Lantheus Medical Imaging examines political, economic, social, technological, legal, and environmental factors shaping the company’s strategic outlook. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It is the final, ready-to-download file with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how regulatory shifts, reimbursement trends, and imaging technology advances are shaping Lantheus Medical Imaging's strategic outlook. Our concise PESTLE highlights key political, economic, social, technological, legal, and environmental risks and opportunities for investors and strategists. Ready-made and actionable—purchase the full analysis for the complete, editable report.

Political factors

Healthcare policy and reimbursement

Government payers determine coverage, coding and payment rates for imaging and radiopharmaceuticals, directly shaping Lantheus adoption among roughly 66 million Medicare beneficiaries. EU HTA regulation (entered into application Jan 2025) and national formularies can speed or block market access. Value-based care and outcome-based contracting favor agents with measurable clinical impact, while IRA-driven drug price negotiation (starting 2026) and broader cost-containment debate increase pricing scrutiny.

Regulatory approval priorities

Agency focus on diagnostics and theranostics has driven variable review speeds, with 2024 regulators prioritizing novel imaging agents over generic filings. Fast-track or breakthrough pathways materially shorten review windows and can accelerate market access for Lantheus pipeline assets. Rising post-market evidence requirements increase lifecycle compliance costs, while limited global harmonization complicates multi-region filings and labeling.

Nuclear material governance

Nuclear material governance shapes Lantheus supply: policies on isotope production and cross-border movement affect reliability, with five aging reactors historically supplying roughly 70% of global Mo-99. Export controls plus NRC and IAEA oversight add compliance complexity and costs. Geopolitical tensions have intermittently disrupted Mo-99, Lu-177 and scarce Ac-225 chains. Government investments (DOE and USDA grants, public reactor/cyclotron funding) aim to stabilize sourcing.

Trade and tariff exposure

Tariffs on chemicals, APIs and equipment increase COGS for imaging agents; short half-life radiopharmaceuticals such as Tc-99m (half-life ~6 hours) and F-18 (half-life ~110 minutes) make customs delays materially damaging. Localization incentives in EU/US/Japan push regional manufacturing, while trade agreements reduce cross-border frictions for critical market flows.

- Tariffs raise COGS for reagents and kits

- Short half-lives (Tc-99m 6h, F-18 110min) make delays costly

- Localization incentives steer plant placement

- Trade pacts ease EU/US/Japan supply chains

Public health priorities

Oncology and cardiology initiatives increasingly steer public funding toward advanced imaging pathways, with PSMA and cardiac PET uptake accelerated by FDA PSMA agent approvals in 2020–2021; screening and guideline updates directly raise demand for specific radiopharmaceuticals. Pandemic readiness policies reshaped hospital throughput, with elective imaging volumes falling about 50% at COVID peaks, stressing throughput planning. National cancer plans now often explicitly prioritize PSMA and other precision modalities.

- Increased targeted funding: drives demand for PET agents

- Guideline changes: create stepwise volume lifts for specific tracers

- Pandemic impact: ~50% elective imaging decline at peaks

- National plans: prioritize PSMA and precision imaging

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

Government payers (≈66M Medicare beneficiaries) and IRA price negotiation (starts 2026) increase reimbursement and pricing pressure on Lantheus products.

Regulatory fast-track pathways shorten approvals for novel imaging agents while rising post-market evidence and fragmented HTA (EU HTA in force Jan 2025) raise lifecycle costs.

Isotope supply risk remains material: five reactors supply ≈70% of Mo-99; Tc-99m half-life 6h, F-18 110min; elective imaging fell ~50% at COVID peaks.

| Metric | Value |

|---|---|

| Medicare beneficiaries | ≈66M |

| Mo-99 supply | ≈70% from 5 reactors |

| IRA negotiation | Starts 2026 |

| Tc-99m / F-18 half-life | 6h / 110min |

| Elective imaging drop (COVID peaks) | ≈50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Lantheus Medical Imaging across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking insights and actionable implications tailored for executives, investors and strategists aiming to identify risks and growth opportunities.

A concise, visually segmented PESTLE summary of Lantheus Medical Imaging that relieves briefing pain points by delivering clear external risk factors and market positioning for quick insertion into presentations or strategy sessions.

Economic factors

Macro cycles and budgets

Hospital and imaging-center budgets track macro cycles as GDP growth and rate cycles compress capital plans; US policy rates stood at 5.25–5.50% mid-2025, tightening credit and raising funding costs. Higher WACC delays capital and formulary additions, while procedure volumes rebounded to near pre‑pandemic levels by 2024. Recessionary pressure intensifies purchasing and tender price competition, forcing deeper concessions.

Payer mix and pricing power

Shift toward managed care, which covers over 60% of US lives, can compress net pricing for Lantheus as payers demand deeper discounts and capitated contracts. DRG and APC reimbursement structures continue to define site-of-care economics, favoring lower-cost outpatient settings and pressuring hospital-based imaging margins. Robust outcomes and pharmacoeconomic data are increasingly required to defend prices, while international reference pricing used by over 20 countries can echo into export markets.

Supply cost volatility

Isotope feedstock and energy price swings materially pressure margins for Lantheus, since Mo-99/Tc-99m sourcing and plant power can shift COGS; management noted cost-of-goods sold sensitivity to feedstock and utilities in recent filings. Cold-chain and hazmat shipping costs, which rise with jet/diesel fuel, increased transport spend notably during 2022–2023 fuel spikes, raising per-shipment costs. Investments in redundancy—backup generators, alternate suppliers and inventory—limit outage risk but raise fixed operating costs and capex. High vendor concentration for key radionuclide supply amplifies bargaining exposure and pricing pass-through risk.

FX and global exposure

Revenue and costs denominated in multiple currencies expose Lantheus to translation and transaction risk across its US, Europe and APAC operations; hedging programs reduce but do not eliminate quarterly EPS volatility. Price corridors and reimbursement caps in many ex-US markets constrain full pass-through of USD price changes. Rapid emerging market uptake supports volume growth but at materially lower average selling prices, compressing margins.

- FX translation/transaction risk

- Hedging mitigates but not eliminates volatility

- Price corridors limit ex-US pass-through

- Emerging markets = higher volume, lower ASPs

Competition and lifecycle

New imaging agents and biosimilars threaten Lantheus mature franchises; Pylarify (piflufolastat F 18) approval in 2021 shifted focus to growth areas while older diagnostic agents face pricing pressure. Patent cliffs and LOEs force mix shifts and higher rebates, and consolidation among peers alters negotiating leverage. Pipeline successes re-rate growth expectations and capital allocation rapidly.

- Pylarify approval: 2021

- LOE risk: increases rebate pressure and mix shift

- M&A: raises counterparty negotiating power

- Pipeline wins: can materially re-rate valuation

Medicare & IRA pricing, faster approvals, and isotope supply risks squeeze imaging margins

High US policy rates (5.25–5.50% mid‑2025) raise WACC, delaying capex and compressing hospital imaging budgets. Managed care covers >60% US lives, pressuring net pricing and margins; DRG/APC shifts favor lower‑cost sites. Mo‑99/Tc‑99m feedstock and fuel volatility raise COGS; FX exposure across US/EU/APAC creates EPS volatility despite hedging.

| Metric | Value |

|---|---|

| US policy rate | 5.25–5.50% (mid‑2025) |

| Managed care | >60% US lives |

| Mo‑99 supplier concentration | High |

What You See Is What You Get

Lantheus Medical Imaging PESTLE Analysis

This PESTLE analysis of Lantheus Medical Imaging examines political, economic, social, technological, legal, and environmental factors shaping the company’s strategic outlook. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It is the final, ready-to-download file with no placeholders or surprises.