Lassonde Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

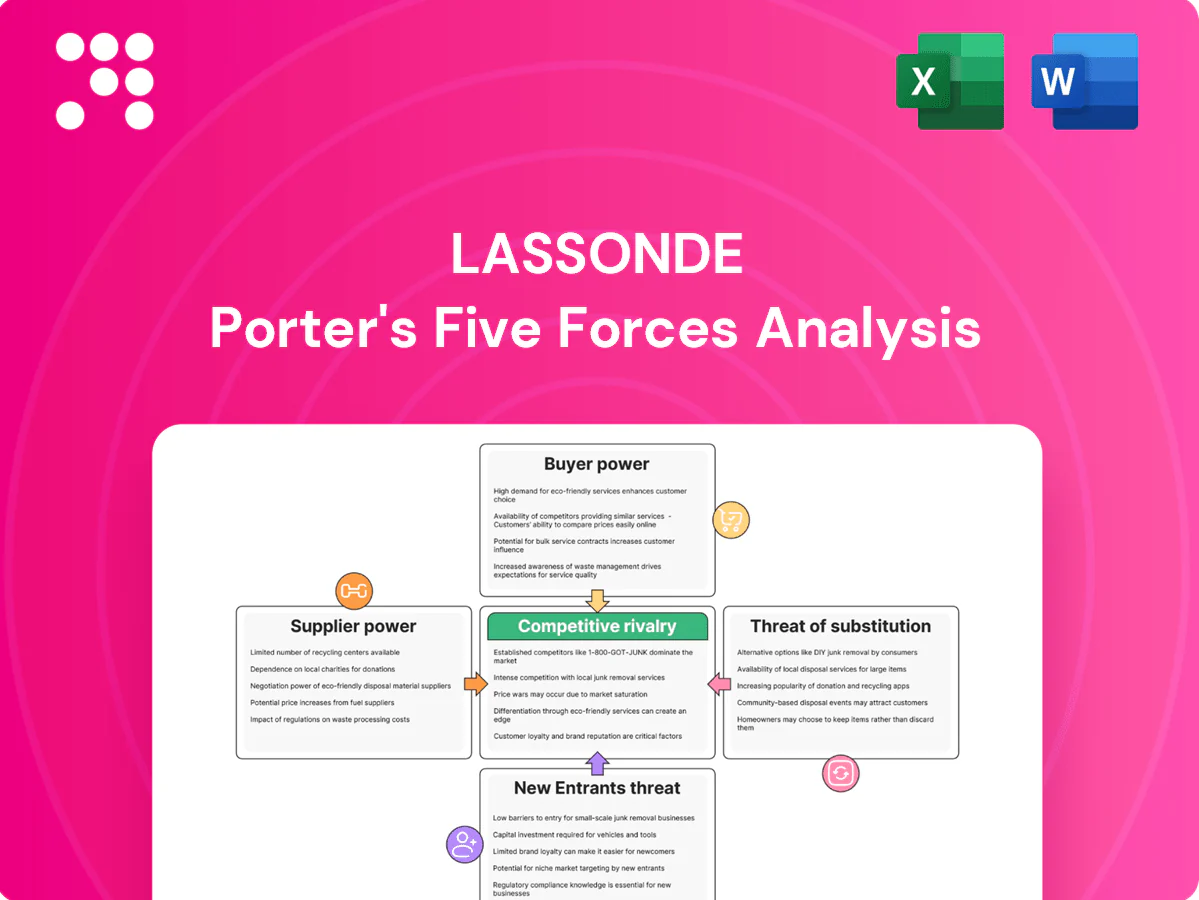

Lassonde’s Porter's Five Forces snapshot highlights supplier and buyer power, substitute threats, new entrant risks, and competitive rivalry shaping its beverage and juice market. This concise view frames key pressures but leaves nuance and data-driven implications unexplored. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic recommendations tailored to Lassonde.

Suppliers Bargaining Power

Fragmented agri-suppliers limit leverage

Most fruit and vegetable inputs come from a broad global base of growers and processors, so no single supplier holds major sway over Lassonde. In 2024 Lassonde continued to multi-source concentrates and pulps across regions and seasons, which limits supplier leverage. Crop cycles and weather shocks can temporarily concentrate supply and raise costs. Diversified sourcing and scale in private-label production strengthen Lassonde’s negotiating position.

Commodity volatility pressures margins

Input costs for fruit concentrates, sugar and edible oils remain volatile: global sugar futures climbed ~15% in 2024 while energy-driven freight and processing costs rose, and CAD/USD moved about 5% vs 2023, compressing margins before list prices adjust. Price spikes can shave operating margins quickly; Lassonde reported roughly CA$1.25bn revenue in 2024, using hedges and forward contracts to mitigate but not eliminate exposure. Hedging covers near-term needs yet residual volatility persists, while Lassonde’s broad product mix enables selective pricing to offset some input swings.

Packaging suppliers hold moderate power

Packaging for PET (eg Indorama), aseptic cartons (Tetra Pak, SIG), glass (O-I, Ardagh) and aluminum cans (Ball) is supplied by a relatively small set of specialists, so suppliers have moderate power; switching formats requires capex and line changeovers, raising short-run switching costs, while long-term contracts and volume commitments limit suppliers’ pricing power, and recyclability/sustainability specs further narrow qualified vendors.

Logistics and co-packing dependencies

Logistics and co-packing dependencies create localized supplier reliance through cold-chain, warehousing, and specialized fillers; the global cold chain market was valued at about 244.3 billion USD in 2023, highlighting scale and concentration. Disruptions from labor, fuel, or capacity shortages can quickly raise costs and degrade service levels, while Lassonde’s multi-plant North American footprint and strategic co-packer relationships provide redundancy and reduce bottleneck risk.

- Cold-chain market size: 244.3B USD (2023)

- Localized reliance: cold storage, fillers, warehousing

- Disruption vectors: labor, fuel, capacity

- Mitigants: multi-plant footprint, strategic co-packers

Quality and safety standards raise vendor bar

Moderate supplier power; hedges help but exposure to sugar, FX and cold-chain shocks

Supplier power is moderate: broad global fruit sourcing and multi-plant/private-label scale limit leverage, but weather-driven crop shocks and volatile inputs raise short-term supplier influence. Packaging and cold-chain providers are concentrated, creating switching costs and pickup in bargaining power. Lassonde used hedges and forward contracts in 2024 but remained exposed to input swings.

| Metric | Value (date) |

|---|---|

| Revenue | CA$1.25bn (2024) |

| Sugar futures move | +15% (2024) |

| CAD/USD vs 2023 | ~5% (2024) |

| Cold-chain market | $244.3B (2023) |

What is included in the product

Applies Porter's Five Forces to Lassonde, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and industry-specific dynamics that shape pricing and profitability; includes strategic implications and actionable insights to defend market share and anticipate disruptive threats.

Lassonde Porter's Five Forces delivers a concise one-sheet summary with customizable pressure levels and an instant radar chart to pinpoint strategic pressure, making boardroom-ready visuals and quick decisions effortless.

Customers Bargaining Power

Retail giants exert high bargaining power

Concentrated chains (big-box, club, grocery) wield strong bargaining power—Canada’s top four grocers account for roughly 70–80% of grocery sales in 2024, forcing trade terms, slotting and promotional funding demands. Rising private-label penetration (~26% in 2024) boosts retailer leverage, yet Lassonde’s private-label capability aligns interests and mitigates risk; losing a major account could reduce volumes by over 10%.

Private label heightens price sensitivity

Retailers increasingly pit national brands against house brands as private-label penetration in North American grocery climbed to roughly 20% in 2024, tightening pricing leverage over suppliers.

Lassonde benefits as a major private-label contract manufacturer but still faces margin pressure when buyers demand price parity or lower-cost SKUs.

Value-tier shoppers switch rapidly when price gaps exceed single-digit percentages, so operational efficiency and scale are critical to sustain economics.

Low consumer switching costs

Juice buyers readily switch among brands, flavors, and formats, with promotional cycles and end-cap visibility driving purchase decisions more than brand loyalty; industry data in 2024 shows roughly 58% of shoppers reported switching juice brands within a 3-month period. Differentiation via low-sugar, organic, or functional claims lowers churn—products with such claims grew share by double digits in 2024. Packaging convenience, like single-serve or resealable formats, further shifts choice toward more portable SKUs.

Foodservice and institutional buyers negotiate hard

Foodservice and institutional buyers wield strong bargaining power: large-volume contracts for hospitality and schools are competitively bid, with price, pack-size, and delivery reliability driving award decisions, while multi-year agreements stabilize volumes but limit upside and transfer margin pressure to suppliers. Service KPIs such as fill rate and on-time delivery are pivotal to renewals and penalties.

- Competitive bids dominate

- Price, pack-size, reliability win awards

- Multi-year deals cap upside

- Service KPIs determine renewals

Data-driven category management expectations

Retailers increasingly demand data-driven category management: suppliers must deliver actionable insights, velocity lifts, and planogram support to secure shelf space. Customers award space to suppliers who fund promotions and demonstrate measurable ROI, while underperformance can lead to delisting. Lassonde’s breadth across branded and private-label lines enables joint business planning and tailored promotional funding.

- insights-driven assortment

- promotion funding + proven ROI

- joint business planning via brand & private label

- underperformance → delisting risk

Grocer concentration raises trade pressure; private labels and promos drive juice wins

Concentrated retailers hold high leverage—Canada’s top four grocers = 70–80% of sales in 2024, pressuring trade terms and slotting. Private-label share ~26% (2024) increases buyer power, though Lassonde's co-manufacturing mitigates risk; loss of a major account could cut volumes >10%. Shopper churn high—~58% switched juice brands within 3 months in 2024, so promo funding and SKU convenience drive wins.

| Metric | 2024 |

|---|---|

| Top-4 grocer share (Canada) | 70–80% |

| Private-label share | ~26% |

| 3-month juice brand switch | ~58% |

| Major-account volume risk | >10% |

Preview Before You Purchase

Lassonde Porter's Five Forces Analysis

This Lassonde Porter’s Five Forces Analysis delivers a concise, professionally formatted assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. This preview is the exact document you’ll receive instantly after purchase—no placeholders, ready for immediate use.

A Must-Have Tool for Decision-Makers

Lassonde’s Porter's Five Forces snapshot highlights supplier and buyer power, substitute threats, new entrant risks, and competitive rivalry shaping its beverage and juice market. This concise view frames key pressures but leaves nuance and data-driven implications unexplored. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic recommendations tailored to Lassonde.

Suppliers Bargaining Power

Fragmented agri-suppliers limit leverage

Most fruit and vegetable inputs come from a broad global base of growers and processors, so no single supplier holds major sway over Lassonde. In 2024 Lassonde continued to multi-source concentrates and pulps across regions and seasons, which limits supplier leverage. Crop cycles and weather shocks can temporarily concentrate supply and raise costs. Diversified sourcing and scale in private-label production strengthen Lassonde’s negotiating position.

Commodity volatility pressures margins

Input costs for fruit concentrates, sugar and edible oils remain volatile: global sugar futures climbed ~15% in 2024 while energy-driven freight and processing costs rose, and CAD/USD moved about 5% vs 2023, compressing margins before list prices adjust. Price spikes can shave operating margins quickly; Lassonde reported roughly CA$1.25bn revenue in 2024, using hedges and forward contracts to mitigate but not eliminate exposure. Hedging covers near-term needs yet residual volatility persists, while Lassonde’s broad product mix enables selective pricing to offset some input swings.

Packaging suppliers hold moderate power

Packaging for PET (eg Indorama), aseptic cartons (Tetra Pak, SIG), glass (O-I, Ardagh) and aluminum cans (Ball) is supplied by a relatively small set of specialists, so suppliers have moderate power; switching formats requires capex and line changeovers, raising short-run switching costs, while long-term contracts and volume commitments limit suppliers’ pricing power, and recyclability/sustainability specs further narrow qualified vendors.

Logistics and co-packing dependencies

Logistics and co-packing dependencies create localized supplier reliance through cold-chain, warehousing, and specialized fillers; the global cold chain market was valued at about 244.3 billion USD in 2023, highlighting scale and concentration. Disruptions from labor, fuel, or capacity shortages can quickly raise costs and degrade service levels, while Lassonde’s multi-plant North American footprint and strategic co-packer relationships provide redundancy and reduce bottleneck risk.

- Cold-chain market size: 244.3B USD (2023)

- Localized reliance: cold storage, fillers, warehousing

- Disruption vectors: labor, fuel, capacity

- Mitigants: multi-plant footprint, strategic co-packers

Quality and safety standards raise vendor bar

Moderate supplier power; hedges help but exposure to sugar, FX and cold-chain shocks

Supplier power is moderate: broad global fruit sourcing and multi-plant/private-label scale limit leverage, but weather-driven crop shocks and volatile inputs raise short-term supplier influence. Packaging and cold-chain providers are concentrated, creating switching costs and pickup in bargaining power. Lassonde used hedges and forward contracts in 2024 but remained exposed to input swings.

| Metric | Value (date) |

|---|---|

| Revenue | CA$1.25bn (2024) |

| Sugar futures move | +15% (2024) |

| CAD/USD vs 2023 | ~5% (2024) |

| Cold-chain market | $244.3B (2023) |

What is included in the product

Applies Porter's Five Forces to Lassonde, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and industry-specific dynamics that shape pricing and profitability; includes strategic implications and actionable insights to defend market share and anticipate disruptive threats.

Lassonde Porter's Five Forces delivers a concise one-sheet summary with customizable pressure levels and an instant radar chart to pinpoint strategic pressure, making boardroom-ready visuals and quick decisions effortless.

Customers Bargaining Power

Retail giants exert high bargaining power

Concentrated chains (big-box, club, grocery) wield strong bargaining power—Canada’s top four grocers account for roughly 70–80% of grocery sales in 2024, forcing trade terms, slotting and promotional funding demands. Rising private-label penetration (~26% in 2024) boosts retailer leverage, yet Lassonde’s private-label capability aligns interests and mitigates risk; losing a major account could reduce volumes by over 10%.

Private label heightens price sensitivity

Retailers increasingly pit national brands against house brands as private-label penetration in North American grocery climbed to roughly 20% in 2024, tightening pricing leverage over suppliers.

Lassonde benefits as a major private-label contract manufacturer but still faces margin pressure when buyers demand price parity or lower-cost SKUs.

Value-tier shoppers switch rapidly when price gaps exceed single-digit percentages, so operational efficiency and scale are critical to sustain economics.

Low consumer switching costs

Juice buyers readily switch among brands, flavors, and formats, with promotional cycles and end-cap visibility driving purchase decisions more than brand loyalty; industry data in 2024 shows roughly 58% of shoppers reported switching juice brands within a 3-month period. Differentiation via low-sugar, organic, or functional claims lowers churn—products with such claims grew share by double digits in 2024. Packaging convenience, like single-serve or resealable formats, further shifts choice toward more portable SKUs.

Foodservice and institutional buyers negotiate hard

Foodservice and institutional buyers wield strong bargaining power: large-volume contracts for hospitality and schools are competitively bid, with price, pack-size, and delivery reliability driving award decisions, while multi-year agreements stabilize volumes but limit upside and transfer margin pressure to suppliers. Service KPIs such as fill rate and on-time delivery are pivotal to renewals and penalties.

- Competitive bids dominate

- Price, pack-size, reliability win awards

- Multi-year deals cap upside

- Service KPIs determine renewals

Data-driven category management expectations

Retailers increasingly demand data-driven category management: suppliers must deliver actionable insights, velocity lifts, and planogram support to secure shelf space. Customers award space to suppliers who fund promotions and demonstrate measurable ROI, while underperformance can lead to delisting. Lassonde’s breadth across branded and private-label lines enables joint business planning and tailored promotional funding.

- insights-driven assortment

- promotion funding + proven ROI

- joint business planning via brand & private label

- underperformance → delisting risk

Grocer concentration raises trade pressure; private labels and promos drive juice wins

Concentrated retailers hold high leverage—Canada’s top four grocers = 70–80% of sales in 2024, pressuring trade terms and slotting. Private-label share ~26% (2024) increases buyer power, though Lassonde's co-manufacturing mitigates risk; loss of a major account could cut volumes >10%. Shopper churn high—~58% switched juice brands within 3 months in 2024, so promo funding and SKU convenience drive wins.

| Metric | 2024 |

|---|---|

| Top-4 grocer share (Canada) | 70–80% |

| Private-label share | ~26% |

| 3-month juice brand switch | ~58% |

| Major-account volume risk | >10% |

Preview Before You Purchase

Lassonde Porter's Five Forces Analysis

This Lassonde Porter’s Five Forces Analysis delivers a concise, professionally formatted assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. This preview is the exact document you’ll receive instantly after purchase—no placeholders, ready for immediate use.

Description

A Must-Have Tool for Decision-Makers

Lassonde’s Porter's Five Forces snapshot highlights supplier and buyer power, substitute threats, new entrant risks, and competitive rivalry shaping its beverage and juice market. This concise view frames key pressures but leaves nuance and data-driven implications unexplored. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and strategic recommendations tailored to Lassonde.

Suppliers Bargaining Power

Fragmented agri-suppliers limit leverage

Most fruit and vegetable inputs come from a broad global base of growers and processors, so no single supplier holds major sway over Lassonde. In 2024 Lassonde continued to multi-source concentrates and pulps across regions and seasons, which limits supplier leverage. Crop cycles and weather shocks can temporarily concentrate supply and raise costs. Diversified sourcing and scale in private-label production strengthen Lassonde’s negotiating position.

Commodity volatility pressures margins

Input costs for fruit concentrates, sugar and edible oils remain volatile: global sugar futures climbed ~15% in 2024 while energy-driven freight and processing costs rose, and CAD/USD moved about 5% vs 2023, compressing margins before list prices adjust. Price spikes can shave operating margins quickly; Lassonde reported roughly CA$1.25bn revenue in 2024, using hedges and forward contracts to mitigate but not eliminate exposure. Hedging covers near-term needs yet residual volatility persists, while Lassonde’s broad product mix enables selective pricing to offset some input swings.

Packaging suppliers hold moderate power

Packaging for PET (eg Indorama), aseptic cartons (Tetra Pak, SIG), glass (O-I, Ardagh) and aluminum cans (Ball) is supplied by a relatively small set of specialists, so suppliers have moderate power; switching formats requires capex and line changeovers, raising short-run switching costs, while long-term contracts and volume commitments limit suppliers’ pricing power, and recyclability/sustainability specs further narrow qualified vendors.

Logistics and co-packing dependencies

Logistics and co-packing dependencies create localized supplier reliance through cold-chain, warehousing, and specialized fillers; the global cold chain market was valued at about 244.3 billion USD in 2023, highlighting scale and concentration. Disruptions from labor, fuel, or capacity shortages can quickly raise costs and degrade service levels, while Lassonde’s multi-plant North American footprint and strategic co-packer relationships provide redundancy and reduce bottleneck risk.

- Cold-chain market size: 244.3B USD (2023)

- Localized reliance: cold storage, fillers, warehousing

- Disruption vectors: labor, fuel, capacity

- Mitigants: multi-plant footprint, strategic co-packers

Quality and safety standards raise vendor bar

Moderate supplier power; hedges help but exposure to sugar, FX and cold-chain shocks

Supplier power is moderate: broad global fruit sourcing and multi-plant/private-label scale limit leverage, but weather-driven crop shocks and volatile inputs raise short-term supplier influence. Packaging and cold-chain providers are concentrated, creating switching costs and pickup in bargaining power. Lassonde used hedges and forward contracts in 2024 but remained exposed to input swings.

| Metric | Value (date) |

|---|---|

| Revenue | CA$1.25bn (2024) |

| Sugar futures move | +15% (2024) |

| CAD/USD vs 2023 | ~5% (2024) |

| Cold-chain market | $244.3B (2023) |

What is included in the product

Applies Porter's Five Forces to Lassonde, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and industry-specific dynamics that shape pricing and profitability; includes strategic implications and actionable insights to defend market share and anticipate disruptive threats.

Lassonde Porter's Five Forces delivers a concise one-sheet summary with customizable pressure levels and an instant radar chart to pinpoint strategic pressure, making boardroom-ready visuals and quick decisions effortless.

Customers Bargaining Power

Retail giants exert high bargaining power

Concentrated chains (big-box, club, grocery) wield strong bargaining power—Canada’s top four grocers account for roughly 70–80% of grocery sales in 2024, forcing trade terms, slotting and promotional funding demands. Rising private-label penetration (~26% in 2024) boosts retailer leverage, yet Lassonde’s private-label capability aligns interests and mitigates risk; losing a major account could reduce volumes by over 10%.

Private label heightens price sensitivity

Retailers increasingly pit national brands against house brands as private-label penetration in North American grocery climbed to roughly 20% in 2024, tightening pricing leverage over suppliers.

Lassonde benefits as a major private-label contract manufacturer but still faces margin pressure when buyers demand price parity or lower-cost SKUs.

Value-tier shoppers switch rapidly when price gaps exceed single-digit percentages, so operational efficiency and scale are critical to sustain economics.

Low consumer switching costs

Juice buyers readily switch among brands, flavors, and formats, with promotional cycles and end-cap visibility driving purchase decisions more than brand loyalty; industry data in 2024 shows roughly 58% of shoppers reported switching juice brands within a 3-month period. Differentiation via low-sugar, organic, or functional claims lowers churn—products with such claims grew share by double digits in 2024. Packaging convenience, like single-serve or resealable formats, further shifts choice toward more portable SKUs.

Foodservice and institutional buyers negotiate hard

Foodservice and institutional buyers wield strong bargaining power: large-volume contracts for hospitality and schools are competitively bid, with price, pack-size, and delivery reliability driving award decisions, while multi-year agreements stabilize volumes but limit upside and transfer margin pressure to suppliers. Service KPIs such as fill rate and on-time delivery are pivotal to renewals and penalties.

- Competitive bids dominate

- Price, pack-size, reliability win awards

- Multi-year deals cap upside

- Service KPIs determine renewals

Data-driven category management expectations

Retailers increasingly demand data-driven category management: suppliers must deliver actionable insights, velocity lifts, and planogram support to secure shelf space. Customers award space to suppliers who fund promotions and demonstrate measurable ROI, while underperformance can lead to delisting. Lassonde’s breadth across branded and private-label lines enables joint business planning and tailored promotional funding.

- insights-driven assortment

- promotion funding + proven ROI

- joint business planning via brand & private label

- underperformance → delisting risk

Grocer concentration raises trade pressure; private labels and promos drive juice wins

Concentrated retailers hold high leverage—Canada’s top four grocers = 70–80% of sales in 2024, pressuring trade terms and slotting. Private-label share ~26% (2024) increases buyer power, though Lassonde's co-manufacturing mitigates risk; loss of a major account could cut volumes >10%. Shopper churn high—~58% switched juice brands within 3 months in 2024, so promo funding and SKU convenience drive wins.

| Metric | 2024 |

|---|---|

| Top-4 grocer share (Canada) | 70–80% |

| Private-label share | ~26% |

| 3-month juice brand switch | ~58% |

| Major-account volume risk | >10% |

Preview Before You Purchase

Lassonde Porter's Five Forces Analysis

This Lassonde Porter’s Five Forces Analysis delivers a concise, professionally formatted assessment of industry rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. This preview is the exact document you’ll receive instantly after purchase—no placeholders, ready for immediate use.