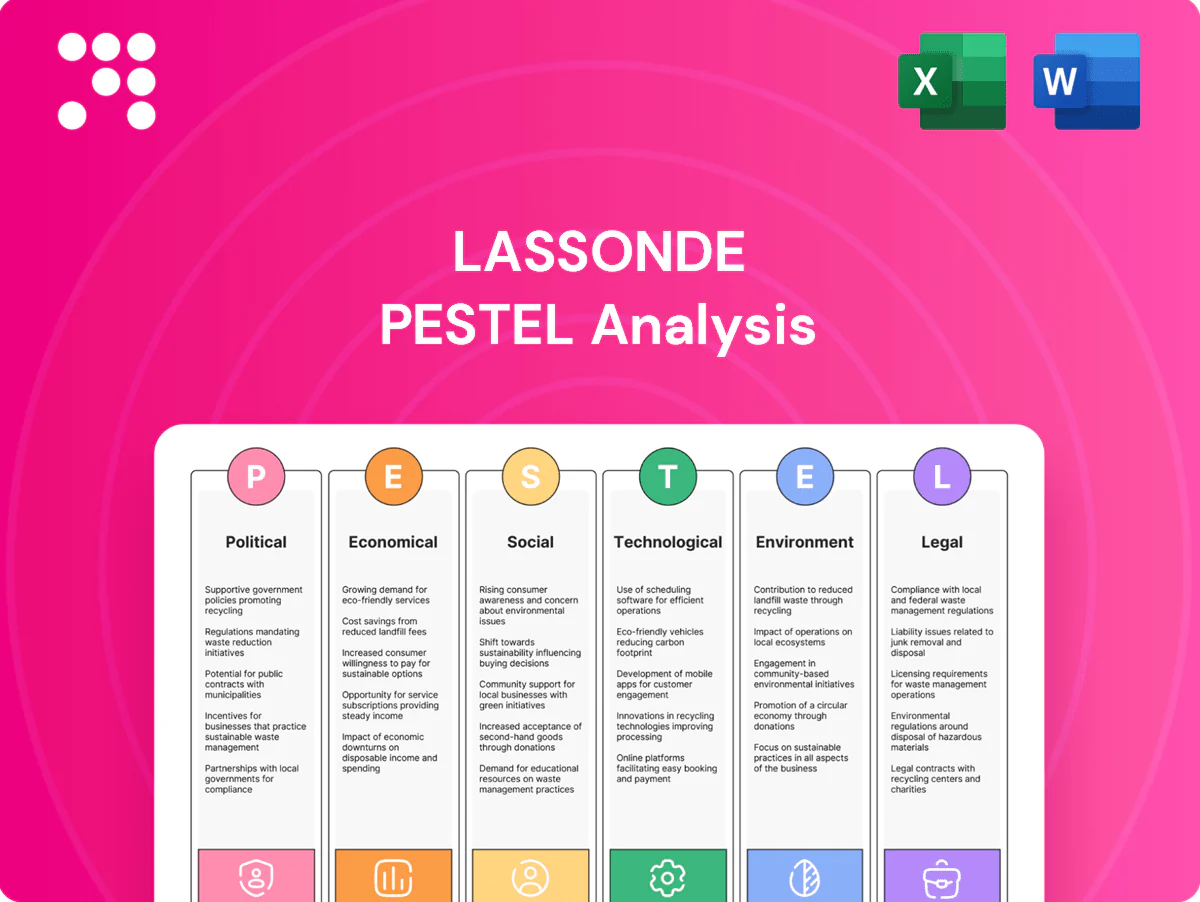

Lassonde PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE analysis of Lassonde—mapping political, economic, social, technological, legal and environmental forces shaping its future. Perfect for investors, consultants and planners, this expert report turns complex trends into actionable recommendations. Purchase the full analysis now for immediately usable insights and editable deliverables.

Political factors

USMCA and trade policy

USMCA, in force since July 1, 2020, governs cross-border flows of juices, concentrates and packaging across North America and sets tariff-rate quotas and dispute mechanisms that directly affect logistics and costs. Changes in enforcement or dispute outcomes can lengthen delivery times and raise input costs, a material risk given roughly 75% of Canadian exports flow to the U.S. market. Renewal talks or retaliatory tariffs could disrupt pricing and sourcing; Lassonde must hedge policy risk with diversified suppliers and higher inventory buffers.

Agricultural subsidies and supports

Farm bills and provincial/state programs shape fruit availability and prices; global production context: apples ~86 million t, tomatoes ~187 million t, cranberries ~1.6 million t, so policy shifts ripple through supply. Subsidies for orchards, crop insurance and disaster relief reduce input-cost volatility for apples, cranberries and tomatoes, while withdrawal of support can tighten supply and raise raw-material costs. Active engagement with grower associations helps anticipate upstream policy shifts and manage procurement risk.

Public health and sugar policy

Governments increasingly target added sugars via taxes, warning labels and school nutrition rules; the US Dietary Guidelines 2020–2025 cap added sugars at <10% of calories and over 40 countries have introduced SSB taxes. Municipal/state soda levies and federal guidance push reformulation and portion-control, shifting demand toward 100% juice, low-sugar or functional drinks. Lassonde must pursue proactive advocacy and rebalance its portfolio mix.

Environmental policy incentives

Environmental policy incentives shape Lassonde operations: Canada’s federal carbon price was C$65/t in 2023 with a legislated rise toward C$170/t by 2030, and US clean-energy Investment Tax Credit offers up to 30% capex support for qualifying projects, lowering transition costs for energy-efficient equipment. Stricter water-extraction and wastewater rules in drought regions increase compliance and capital expenses, forcing site selection and capex planning to incorporate policy trajectories.

- carbon-pricing: Canada C$65/t (2023) → C$170/t (2030 plan)

- clean-energy-credits: US ITC up to 30% capex offset

- water-regs: drought-driven compliance raises capex/OPEX

Geopolitical supply volatility

Geopolitical tensions and sanctions increasingly threaten Lassonde's access to fruit concentrates, citric acid and packaging resins, contributing to episodic price spikes and supply shortfalls; Lassonde reported roughly CAD 1.6 billion revenue in 2024, exposing material input risk to procurement costs. Port congestion and export controls in Latin America, Europe and Asia amplify lead‑time volatility, while instability in harvest regions has driven short-term commodity squeezes.

- Multi-origin sourcing

- Nearshoring to reduce transit risk

- Hedging/long-term contracts

- Inventory buffers for seasonal crops

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

USMCA (since 2020) governs cross-border juice flows and risks affecting ~75% of Canadian exports to the US. Canada carbon price C$65/t (2023) → C$170/t (2030 plan); US ITC up to 30%. Over 40 countries have SSB taxes and US guidelines cap added sugars <10%. Lassonde revenue ~CAD1.6B (2024), exposing procurement to sanctions and port risks.

| Metric | Value |

|---|---|

| US export share | ~75% |

| Revenue 2024 | CAD 1.6B |

| Carbon price | C$65/t → C$170/t (2030) |

| SSB taxes | >40 countries |

What is included in the product

Explores how macro-environmental forces uniquely affect Lassonde across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors.

A concise, PESTLE‑segmented summary of Lassonde’s external environment that’s ready to drop into presentations or planning sessions, enabling quick team alignment and focused discussion on regulatory, economic and market risks.

Economic factors

Input cost inflation

Input-cost inflation hits Lassonde as fruit, sugar, aluminum, PET resin and corrugate remain cyclical and volatile — aluminum rose about 8% in 2024, PET ~12% and global sugar ~7% y/y, while fruit/produce prices spiked ~15% in 2023–24. Weather shocks and energy prices (Brent ~$80–90/barrel in 2024) transmitted through agricultural and packaging markets. Persistent cost inflation compresses margins absent price or mix gains; strategic contracting and value engineering are critical.

FX CAD–USD exposure

Operating in Canada and the U.S. exposes Lassonde to translation and transaction risk: USD/CAD averaged about 1.34 in 2024 and hovered near 1.36 in mid‑2025, so a stronger USD raises costs for imported concentrates and packaging into Canadian plants while boosting translated U.S. revenue. Active hedging policies, plus natural offsets from sourcing and pricing, are essential to manage margin volatility. FX swings also alter cross‑border competitiveness between Canadian and U.S. facilities.

Private label dynamics

Economic slowdowns drive trading-down and lifted private-label volumes, with Canadian private-label penetration reaching about 24% in 2024, benefiting major co-packers like Lassonde via higher unit volumes. Strong retailer consolidation—top chains controlling roughly three-quarters of grocery sales—raises bargaining power and tighter specs, squeezing margins. Lassonde’s balanced mix of branded and private-label contracts helps smooth revenue cycles and reduce volatility.

Interest rates and capex

- Capex cost pressure: higher rates = higher borrowing

- Valuation impact: +100–200 bps discounting

- Optimization: align spend with rate cycles

- Mitigation: use subsidies (≈30% credits) and cash-flow discipline

Logistics and freight costs

Trucking capacity, fuel and driver availability materially affect Lassonde’s delivered cost per case; US on‑highway diesel averaged about 4.15 USD/gal in 2024, ATA estimated a 2024 driver shortfall near 80,000 and DAT spot rates were ~20% below 2022 peaks, pressuring margin volatility. Network optimization, backhauls and modal shifts reduce cost swings while proximity to retailers’ DCs cuts service penalties; dynamic routing and inventory positioning improve on‑time fill and lower unit cost.

- Trucking capacity: ATA driver gap ~80,000 (2024)

- Fuel: US diesel ≈ 4.15 USD/gal (2024, EIA)

- Rates: DAT spot ~20% below 2022 peaks

- Actions: backhauls, modal shift, routing, inventory positioning

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

Input-cost inflation (Al+8% 2024, PET+12%, sugar+7%, fruit+15% 2023–24) and Brent ~$80–90/bbl in 2024 compress margins absent pricing; USD/CAD ~1.34 (2024) and BoC rate 5.00% (mid‑2025) raise FX and financing pressure. Private‑label rose to ~24% (Canada 2024), boosting volumes; diesel ~$4.15/gal and ATA driver gap ~80,000 (2024) increase logistics cost and volatility.

| Metric | Value (2024/2025) |

|---|---|

| Aluminum | +8% |

| PET | +12% |

| Sugar | +7% |

| Fruit | +15% |

| Brent | $80–90/bbl |

| USD/CAD | ~1.34 |

| BoC rate | 5.00% |

| Private‑label (Canada) | 24% |

| Diesel (US) | $4.15/gal |

| ATA driver gap | ~80,000 |

Preview the Actual Deliverable

Lassonde PESTLE Analysis

The Lassonde PESTLE Analysis provides a concise, actionable review of political, economic, social, technological, legal, and environmental factors affecting the company, with strategic implications and recommended responses. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final, downloadable file.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE analysis of Lassonde—mapping political, economic, social, technological, legal and environmental forces shaping its future. Perfect for investors, consultants and planners, this expert report turns complex trends into actionable recommendations. Purchase the full analysis now for immediately usable insights and editable deliverables.

Political factors

USMCA and trade policy

USMCA, in force since July 1, 2020, governs cross-border flows of juices, concentrates and packaging across North America and sets tariff-rate quotas and dispute mechanisms that directly affect logistics and costs. Changes in enforcement or dispute outcomes can lengthen delivery times and raise input costs, a material risk given roughly 75% of Canadian exports flow to the U.S. market. Renewal talks or retaliatory tariffs could disrupt pricing and sourcing; Lassonde must hedge policy risk with diversified suppliers and higher inventory buffers.

Agricultural subsidies and supports

Farm bills and provincial/state programs shape fruit availability and prices; global production context: apples ~86 million t, tomatoes ~187 million t, cranberries ~1.6 million t, so policy shifts ripple through supply. Subsidies for orchards, crop insurance and disaster relief reduce input-cost volatility for apples, cranberries and tomatoes, while withdrawal of support can tighten supply and raise raw-material costs. Active engagement with grower associations helps anticipate upstream policy shifts and manage procurement risk.

Public health and sugar policy

Governments increasingly target added sugars via taxes, warning labels and school nutrition rules; the US Dietary Guidelines 2020–2025 cap added sugars at <10% of calories and over 40 countries have introduced SSB taxes. Municipal/state soda levies and federal guidance push reformulation and portion-control, shifting demand toward 100% juice, low-sugar or functional drinks. Lassonde must pursue proactive advocacy and rebalance its portfolio mix.

Environmental policy incentives

Environmental policy incentives shape Lassonde operations: Canada’s federal carbon price was C$65/t in 2023 with a legislated rise toward C$170/t by 2030, and US clean-energy Investment Tax Credit offers up to 30% capex support for qualifying projects, lowering transition costs for energy-efficient equipment. Stricter water-extraction and wastewater rules in drought regions increase compliance and capital expenses, forcing site selection and capex planning to incorporate policy trajectories.

- carbon-pricing: Canada C$65/t (2023) → C$170/t (2030 plan)

- clean-energy-credits: US ITC up to 30% capex offset

- water-regs: drought-driven compliance raises capex/OPEX

Geopolitical supply volatility

Geopolitical tensions and sanctions increasingly threaten Lassonde's access to fruit concentrates, citric acid and packaging resins, contributing to episodic price spikes and supply shortfalls; Lassonde reported roughly CAD 1.6 billion revenue in 2024, exposing material input risk to procurement costs. Port congestion and export controls in Latin America, Europe and Asia amplify lead‑time volatility, while instability in harvest regions has driven short-term commodity squeezes.

- Multi-origin sourcing

- Nearshoring to reduce transit risk

- Hedging/long-term contracts

- Inventory buffers for seasonal crops

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

USMCA (since 2020) governs cross-border juice flows and risks affecting ~75% of Canadian exports to the US. Canada carbon price C$65/t (2023) → C$170/t (2030 plan); US ITC up to 30%. Over 40 countries have SSB taxes and US guidelines cap added sugars <10%. Lassonde revenue ~CAD1.6B (2024), exposing procurement to sanctions and port risks.

| Metric | Value |

|---|---|

| US export share | ~75% |

| Revenue 2024 | CAD 1.6B |

| Carbon price | C$65/t → C$170/t (2030) |

| SSB taxes | >40 countries |

What is included in the product

Explores how macro-environmental forces uniquely affect Lassonde across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors.

A concise, PESTLE‑segmented summary of Lassonde’s external environment that’s ready to drop into presentations or planning sessions, enabling quick team alignment and focused discussion on regulatory, economic and market risks.

Economic factors

Input cost inflation

Input-cost inflation hits Lassonde as fruit, sugar, aluminum, PET resin and corrugate remain cyclical and volatile — aluminum rose about 8% in 2024, PET ~12% and global sugar ~7% y/y, while fruit/produce prices spiked ~15% in 2023–24. Weather shocks and energy prices (Brent ~$80–90/barrel in 2024) transmitted through agricultural and packaging markets. Persistent cost inflation compresses margins absent price or mix gains; strategic contracting and value engineering are critical.

FX CAD–USD exposure

Operating in Canada and the U.S. exposes Lassonde to translation and transaction risk: USD/CAD averaged about 1.34 in 2024 and hovered near 1.36 in mid‑2025, so a stronger USD raises costs for imported concentrates and packaging into Canadian plants while boosting translated U.S. revenue. Active hedging policies, plus natural offsets from sourcing and pricing, are essential to manage margin volatility. FX swings also alter cross‑border competitiveness between Canadian and U.S. facilities.

Private label dynamics

Economic slowdowns drive trading-down and lifted private-label volumes, with Canadian private-label penetration reaching about 24% in 2024, benefiting major co-packers like Lassonde via higher unit volumes. Strong retailer consolidation—top chains controlling roughly three-quarters of grocery sales—raises bargaining power and tighter specs, squeezing margins. Lassonde’s balanced mix of branded and private-label contracts helps smooth revenue cycles and reduce volatility.

Interest rates and capex

- Capex cost pressure: higher rates = higher borrowing

- Valuation impact: +100–200 bps discounting

- Optimization: align spend with rate cycles

- Mitigation: use subsidies (≈30% credits) and cash-flow discipline

Logistics and freight costs

Trucking capacity, fuel and driver availability materially affect Lassonde’s delivered cost per case; US on‑highway diesel averaged about 4.15 USD/gal in 2024, ATA estimated a 2024 driver shortfall near 80,000 and DAT spot rates were ~20% below 2022 peaks, pressuring margin volatility. Network optimization, backhauls and modal shifts reduce cost swings while proximity to retailers’ DCs cuts service penalties; dynamic routing and inventory positioning improve on‑time fill and lower unit cost.

- Trucking capacity: ATA driver gap ~80,000 (2024)

- Fuel: US diesel ≈ 4.15 USD/gal (2024, EIA)

- Rates: DAT spot ~20% below 2022 peaks

- Actions: backhauls, modal shift, routing, inventory positioning

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

Input-cost inflation (Al+8% 2024, PET+12%, sugar+7%, fruit+15% 2023–24) and Brent ~$80–90/bbl in 2024 compress margins absent pricing; USD/CAD ~1.34 (2024) and BoC rate 5.00% (mid‑2025) raise FX and financing pressure. Private‑label rose to ~24% (Canada 2024), boosting volumes; diesel ~$4.15/gal and ATA driver gap ~80,000 (2024) increase logistics cost and volatility.

| Metric | Value (2024/2025) |

|---|---|

| Aluminum | +8% |

| PET | +12% |

| Sugar | +7% |

| Fruit | +15% |

| Brent | $80–90/bbl |

| USD/CAD | ~1.34 |

| BoC rate | 5.00% |

| Private‑label (Canada) | 24% |

| Diesel (US) | $4.15/gal |

| ATA driver gap | ~80,000 |

Preview the Actual Deliverable

Lassonde PESTLE Analysis

The Lassonde PESTLE Analysis provides a concise, actionable review of political, economic, social, technological, legal, and environmental factors affecting the company, with strategic implications and recommended responses. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final, downloadable file.

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE analysis of Lassonde—mapping political, economic, social, technological, legal and environmental forces shaping its future. Perfect for investors, consultants and planners, this expert report turns complex trends into actionable recommendations. Purchase the full analysis now for immediately usable insights and editable deliverables.

Political factors

USMCA and trade policy

USMCA, in force since July 1, 2020, governs cross-border flows of juices, concentrates and packaging across North America and sets tariff-rate quotas and dispute mechanisms that directly affect logistics and costs. Changes in enforcement or dispute outcomes can lengthen delivery times and raise input costs, a material risk given roughly 75% of Canadian exports flow to the U.S. market. Renewal talks or retaliatory tariffs could disrupt pricing and sourcing; Lassonde must hedge policy risk with diversified suppliers and higher inventory buffers.

Agricultural subsidies and supports

Farm bills and provincial/state programs shape fruit availability and prices; global production context: apples ~86 million t, tomatoes ~187 million t, cranberries ~1.6 million t, so policy shifts ripple through supply. Subsidies for orchards, crop insurance and disaster relief reduce input-cost volatility for apples, cranberries and tomatoes, while withdrawal of support can tighten supply and raise raw-material costs. Active engagement with grower associations helps anticipate upstream policy shifts and manage procurement risk.

Public health and sugar policy

Governments increasingly target added sugars via taxes, warning labels and school nutrition rules; the US Dietary Guidelines 2020–2025 cap added sugars at <10% of calories and over 40 countries have introduced SSB taxes. Municipal/state soda levies and federal guidance push reformulation and portion-control, shifting demand toward 100% juice, low-sugar or functional drinks. Lassonde must pursue proactive advocacy and rebalance its portfolio mix.

Environmental policy incentives

Environmental policy incentives shape Lassonde operations: Canada’s federal carbon price was C$65/t in 2023 with a legislated rise toward C$170/t by 2030, and US clean-energy Investment Tax Credit offers up to 30% capex support for qualifying projects, lowering transition costs for energy-efficient equipment. Stricter water-extraction and wastewater rules in drought regions increase compliance and capital expenses, forcing site selection and capex planning to incorporate policy trajectories.

- carbon-pricing: Canada C$65/t (2023) → C$170/t (2030 plan)

- clean-energy-credits: US ITC up to 30% capex offset

- water-regs: drought-driven compliance raises capex/OPEX

Geopolitical supply volatility

Geopolitical tensions and sanctions increasingly threaten Lassonde's access to fruit concentrates, citric acid and packaging resins, contributing to episodic price spikes and supply shortfalls; Lassonde reported roughly CAD 1.6 billion revenue in 2024, exposing material input risk to procurement costs. Port congestion and export controls in Latin America, Europe and Asia amplify lead‑time volatility, while instability in harvest regions has driven short-term commodity squeezes.

- Multi-origin sourcing

- Nearshoring to reduce transit risk

- Hedging/long-term contracts

- Inventory buffers for seasonal crops

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

USMCA (since 2020) governs cross-border juice flows and risks affecting ~75% of Canadian exports to the US. Canada carbon price C$65/t (2023) → C$170/t (2030 plan); US ITC up to 30%. Over 40 countries have SSB taxes and US guidelines cap added sugars <10%. Lassonde revenue ~CAD1.6B (2024), exposing procurement to sanctions and port risks.

| Metric | Value |

|---|---|

| US export share | ~75% |

| Revenue 2024 | CAD 1.6B |

| Carbon price | C$65/t → C$170/t (2030) |

| SSB taxes | >40 countries |

What is included in the product

Explores how macro-environmental forces uniquely affect Lassonde across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors.

A concise, PESTLE‑segmented summary of Lassonde’s external environment that’s ready to drop into presentations or planning sessions, enabling quick team alignment and focused discussion on regulatory, economic and market risks.

Economic factors

Input cost inflation

Input-cost inflation hits Lassonde as fruit, sugar, aluminum, PET resin and corrugate remain cyclical and volatile — aluminum rose about 8% in 2024, PET ~12% and global sugar ~7% y/y, while fruit/produce prices spiked ~15% in 2023–24. Weather shocks and energy prices (Brent ~$80–90/barrel in 2024) transmitted through agricultural and packaging markets. Persistent cost inflation compresses margins absent price or mix gains; strategic contracting and value engineering are critical.

FX CAD–USD exposure

Operating in Canada and the U.S. exposes Lassonde to translation and transaction risk: USD/CAD averaged about 1.34 in 2024 and hovered near 1.36 in mid‑2025, so a stronger USD raises costs for imported concentrates and packaging into Canadian plants while boosting translated U.S. revenue. Active hedging policies, plus natural offsets from sourcing and pricing, are essential to manage margin volatility. FX swings also alter cross‑border competitiveness between Canadian and U.S. facilities.

Private label dynamics

Economic slowdowns drive trading-down and lifted private-label volumes, with Canadian private-label penetration reaching about 24% in 2024, benefiting major co-packers like Lassonde via higher unit volumes. Strong retailer consolidation—top chains controlling roughly three-quarters of grocery sales—raises bargaining power and tighter specs, squeezing margins. Lassonde’s balanced mix of branded and private-label contracts helps smooth revenue cycles and reduce volatility.

Interest rates and capex

- Capex cost pressure: higher rates = higher borrowing

- Valuation impact: +100–200 bps discounting

- Optimization: align spend with rate cycles

- Mitigation: use subsidies (≈30% credits) and cash-flow discipline

Logistics and freight costs

Trucking capacity, fuel and driver availability materially affect Lassonde’s delivered cost per case; US on‑highway diesel averaged about 4.15 USD/gal in 2024, ATA estimated a 2024 driver shortfall near 80,000 and DAT spot rates were ~20% below 2022 peaks, pressuring margin volatility. Network optimization, backhauls and modal shifts reduce cost swings while proximity to retailers’ DCs cuts service penalties; dynamic routing and inventory positioning improve on‑time fill and lower unit cost.

- Trucking capacity: ATA driver gap ~80,000 (2024)

- Fuel: US diesel ≈ 4.15 USD/gal (2024, EIA)

- Rates: DAT spot ~20% below 2022 peaks

- Actions: backhauls, modal shift, routing, inventory positioning

USMCA, carbon surge to C$170/t and SSB taxes threaten ~75% US-bound juice export flows

Input-cost inflation (Al+8% 2024, PET+12%, sugar+7%, fruit+15% 2023–24) and Brent ~$80–90/bbl in 2024 compress margins absent pricing; USD/CAD ~1.34 (2024) and BoC rate 5.00% (mid‑2025) raise FX and financing pressure. Private‑label rose to ~24% (Canada 2024), boosting volumes; diesel ~$4.15/gal and ATA driver gap ~80,000 (2024) increase logistics cost and volatility.

| Metric | Value (2024/2025) |

|---|---|

| Aluminum | +8% |

| PET | +12% |

| Sugar | +7% |

| Fruit | +15% |

| Brent | $80–90/bbl |

| USD/CAD | ~1.34 |

| BoC rate | 5.00% |

| Private‑label (Canada) | 24% |

| Diesel (US) | $4.15/gal |

| ATA driver gap | ~80,000 |

Preview the Actual Deliverable

Lassonde PESTLE Analysis

The Lassonde PESTLE Analysis provides a concise, actionable review of political, economic, social, technological, legal, and environmental factors affecting the company, with strategic implications and recommended responses. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final, downloadable file.