Lattice Semiconductor Porter's Five Forces Analysis

Don't Miss the Bigger Picture

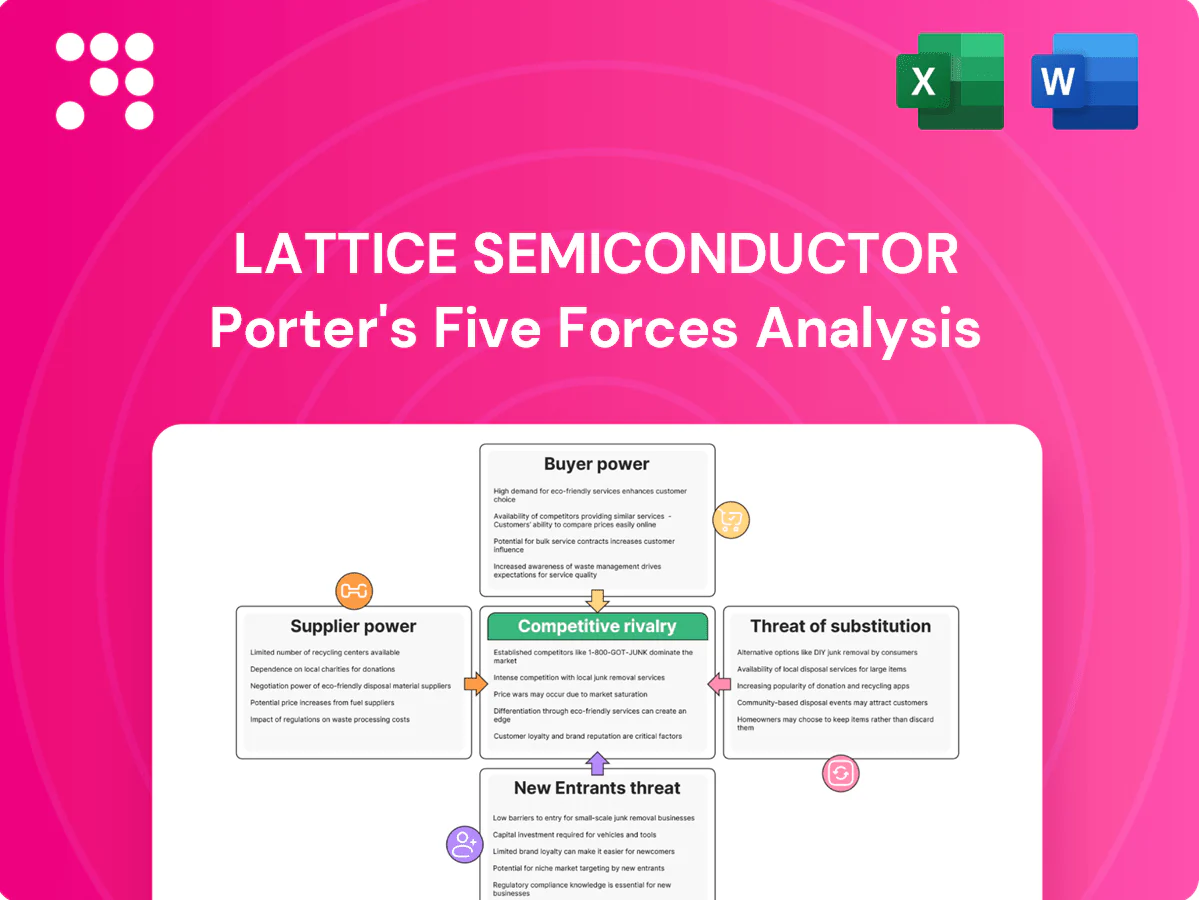

Lattice Semiconductor’s Porter's Five Forces analysis highlights moderate supplier power, growing buyer sophistication, niche barriers limiting new entrants, emerging substitute architectures, and intense rivalry in programmable logic devices. Strategic positioning centers on low-power differentiation and customer intimacy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lattice Semiconductor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry dependence

Lattice depends on a small set of advanced foundries (eg TSMC, UMC) and OSATs (eg ASE, Amkor) for wafers, packaging and test; TSMC held roughly 54% global foundry share in 2023–24, while the top-3 OSATs control ~60% of OSAT capacity (2023). Limited alternative capacity at qualified nodes increases supplier leverage during shortages, though Lattice’s focus on mature, cost-optimized nodes reduces extreme pressure. Multi-sourcing and long-term supply agreements further mitigate risk.

EDA and IP ecosystem reliance

Toolchains and licensed IP from a few major EDA/IP vendors — top three control roughly 80% of the EDA market (2023–24) — create switching frictions and recurring licensing costs, giving suppliers pricing power for signoff-quality tools. Lattice mitigates this by offering its own Lattice toolstack and curated IP to lower external dependency, while co-optimization with partners shifts bargaining leverage back toward Lattice.

Specialty materials and substrates

High-spec substrates, rare gases and ABF laminates can become bottlenecks; when substrate markets tighten suppliers gain leverage and lead times often extend beyond 20 weeks. Lattice’s smaller die sizes and low-power architectures lower material intensity per unit. Exposure persists in cyclical upswings as substrate constraints and price volatility re-emerge.

Geopolitical and export controls

Restrictions on semiconductor equipment and cross-border logistics concentrate supply options; TSMC controls roughly 90% of sub‑7nm capacity (2024), tightening access to advanced tools. Suppliers in targeted regions incur compliance costs that are often passed to fabless customers; Lattice reported FY2024 revenue of about $1.02B, making supplier pass‑throughs meaningful to margins. Lattice diversifies manufacturing geographies to cushion shocks, yet policy volatility can spike supplier power intermittently.

- High concentration: TSMC ~90% sub‑7nm

- Cost passthrough: compliance raises supplier prices

- Mitigation: Lattice multi‑fabrication strategy

- Risk: intermittent policy-driven supplier leverage

Qualification and yield learning

Deep process qualifications and multi-quarter yield ramps create path dependence with incumbent fabs, so switching risks months of delays and performance drift, strengthening supplier positions; as of 2024 Lattice emphasized proven nodes to limit yield volatility. Automotive and industrial certifications often lock designs to specific supply chains for 5–10 years, constraining flexibility.

- Long ramps: 6–18 months to stabilize yields

- Cert duration: 5–10 year supply ties

- Strategy: 2024 focus on proven nodes to reduce volatility

Fabless supplier faces moderate–high supplier power from concentrated fabs, OSATs and EDA/IP duopoly

Lattice faces moderate–high supplier power: concentrated fabs (TSMC ~54% foundry, ~90% sub‑7nm in 2024) and top‑3 OSATs ~60% (2023) limit alternatives, though mature‑node focus, multi‑sourcing and long contracts mitigate risk. EDA/IP top‑3 ~80% raises licensing friction. FY2024 revenue ~$1.02B makes cost pass‑throughs material.

| Metric | Value |

|---|---|

| TSMC share | 54% foundry / 90% sub‑7nm (2024) |

| Top‑3 OSATs | ~60% (2023) |

| EDA top‑3 | ~80% (2023–24) |

| FY2024 Rev | $1.02B |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Lattice Semiconductor, highlighting disruptive rivals, pricing pressures, and strategic defenses shaping its profitability.

Concise Porter's Five Forces for Lattice Semiconductor—clarifies supplier, buyer, rivalry, entrant and substitute pressures to relieve analysis overload and speed strategic decisions. Ready to drop into decks or adapt with your inputs for fast, board-ready insights.

Customers Bargaining Power

Large OEM volume leverage

Tier-1 OEMs in communications, computing, and automotive push hard on price and contract terms, with high-volume programs in 2024 often negotiating multi-year supply commitments and discounts that can exceed 15% per program; these programs also demand value-added support and extended supply assurances. Lattice leans on differentiated power/performance and low-power edge propositions to defend pricing and reported gross margin resilience in 2024. Concentrated accounts, however, keep buyer power elevated and tie a meaningful share of revenue to a few large OEM wins.

Design-in lock-in and switching costs

FPGA selections embed toolchains, IP and firmware so mid-cycle switches typically add 6–12 months and can cost firms hundreds of thousands to millions in NRE, reducing buyer bargaining power during a product’s lifecycle. Second-sourcing policies and pin-compatible rivals restore leverage at new design starts, especially where customers anticipate volume swaps. Lattice’s growing suite of software and reference designs in 2024 aims to deepen stickiness and raise effective switching costs.

Segment-specific price sensitivity

Consumer and edge devices remain highly cost-sensitive, driving down ASPs and exerting pricing pressure, while industrial and automotive buyers prioritize reliability and lifecycle, often accepting higher prices for extended support; in 2024 Lattice’s revenue mix shifted toward higher-value markets with over 40% tied to industrial/automotive, and the company tailors portfolios by segment elasticity, moderating aggregate buyer power.

Demand cyclicality and inventory swings

Buyers adjust orders rapidly with macro cycles, causing utilization swings and pricing pressure; Lattice's FY2024 revenue was about $1.06B, so order volatility materially affects quarterly results. In downcycles customers seek concessions and vendor-managed inventory, but Lattice cites disciplined pricing and backlog management to resist deep discounts. Long-lifecycle programs offer baseline stability, cushioning revenue during troughs.

- Buyers: rapid order swings

- Downcycles: push for VMI and concessions

- Lattice: disciplined pricing/backlog

- Stability: long-lifecycle programs

Performance and roadmap expectations

Customers demand ongoing gains in power efficiency, security, and AI-at-the-edge features, and if Lattice roadmaps lag buyers can shift sockets, increasing customer bargaining power; Lattice reported fiscal 2024 revenue of $601 million, underscoring customer influence on growth. Lattice invests in software toolchains and ML frameworks to raise switching costs and reduce pure price negotiations, lowering buyer leverage.

- Power efficiency: roadmap-driven demand

- Security/AI: critical for retention

- Software: toolchains/ML frameworks reduce price focus

- FY2024 revenue: $601M (context)

OEMs force >15% discounts; firm: low-power edge + software; FY24 rev $1.06B

Tier-1 OEMs exert strong price/contract leverage (discounts >15% on multi-year programs) while Lattice defends margins via low-power edge differentiation and rising software stickiness; concentrated accounts and order volatility keep buyer power elevated despite >40% 2024 revenue from industrial/automotive. FY2024 revenue ~1.06B; roadmap gaps can trigger design swaps.

| Metric | 2024 |

|---|---|

| Revenue | $1.06B |

| Industrial/Auto mix | 40%+ |

| Typical OEM discount | >15% |

Same Document Delivered

Lattice Semiconductor Porter's Five Forces Analysis

This preview shows the exact Lattice Semiconductor Porter's Five Forces analysis you'll receive—no placeholders or mockups. The analysis is fully formatted and ready for immediate download upon purchase. It covers competitive rivalry, supplier and buyer power, threats of substitutes and new entry, and strategic implications for Lattice.

Don't Miss the Bigger Picture

Lattice Semiconductor’s Porter's Five Forces analysis highlights moderate supplier power, growing buyer sophistication, niche barriers limiting new entrants, emerging substitute architectures, and intense rivalry in programmable logic devices. Strategic positioning centers on low-power differentiation and customer intimacy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lattice Semiconductor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry dependence

Lattice depends on a small set of advanced foundries (eg TSMC, UMC) and OSATs (eg ASE, Amkor) for wafers, packaging and test; TSMC held roughly 54% global foundry share in 2023–24, while the top-3 OSATs control ~60% of OSAT capacity (2023). Limited alternative capacity at qualified nodes increases supplier leverage during shortages, though Lattice’s focus on mature, cost-optimized nodes reduces extreme pressure. Multi-sourcing and long-term supply agreements further mitigate risk.

EDA and IP ecosystem reliance

Toolchains and licensed IP from a few major EDA/IP vendors — top three control roughly 80% of the EDA market (2023–24) — create switching frictions and recurring licensing costs, giving suppliers pricing power for signoff-quality tools. Lattice mitigates this by offering its own Lattice toolstack and curated IP to lower external dependency, while co-optimization with partners shifts bargaining leverage back toward Lattice.

Specialty materials and substrates

High-spec substrates, rare gases and ABF laminates can become bottlenecks; when substrate markets tighten suppliers gain leverage and lead times often extend beyond 20 weeks. Lattice’s smaller die sizes and low-power architectures lower material intensity per unit. Exposure persists in cyclical upswings as substrate constraints and price volatility re-emerge.

Geopolitical and export controls

Restrictions on semiconductor equipment and cross-border logistics concentrate supply options; TSMC controls roughly 90% of sub‑7nm capacity (2024), tightening access to advanced tools. Suppliers in targeted regions incur compliance costs that are often passed to fabless customers; Lattice reported FY2024 revenue of about $1.02B, making supplier pass‑throughs meaningful to margins. Lattice diversifies manufacturing geographies to cushion shocks, yet policy volatility can spike supplier power intermittently.

- High concentration: TSMC ~90% sub‑7nm

- Cost passthrough: compliance raises supplier prices

- Mitigation: Lattice multi‑fabrication strategy

- Risk: intermittent policy-driven supplier leverage

Qualification and yield learning

Deep process qualifications and multi-quarter yield ramps create path dependence with incumbent fabs, so switching risks months of delays and performance drift, strengthening supplier positions; as of 2024 Lattice emphasized proven nodes to limit yield volatility. Automotive and industrial certifications often lock designs to specific supply chains for 5–10 years, constraining flexibility.

- Long ramps: 6–18 months to stabilize yields

- Cert duration: 5–10 year supply ties

- Strategy: 2024 focus on proven nodes to reduce volatility

Fabless supplier faces moderate–high supplier power from concentrated fabs, OSATs and EDA/IP duopoly

Lattice faces moderate–high supplier power: concentrated fabs (TSMC ~54% foundry, ~90% sub‑7nm in 2024) and top‑3 OSATs ~60% (2023) limit alternatives, though mature‑node focus, multi‑sourcing and long contracts mitigate risk. EDA/IP top‑3 ~80% raises licensing friction. FY2024 revenue ~$1.02B makes cost pass‑throughs material.

| Metric | Value |

|---|---|

| TSMC share | 54% foundry / 90% sub‑7nm (2024) |

| Top‑3 OSATs | ~60% (2023) |

| EDA top‑3 | ~80% (2023–24) |

| FY2024 Rev | $1.02B |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Lattice Semiconductor, highlighting disruptive rivals, pricing pressures, and strategic defenses shaping its profitability.

Concise Porter's Five Forces for Lattice Semiconductor—clarifies supplier, buyer, rivalry, entrant and substitute pressures to relieve analysis overload and speed strategic decisions. Ready to drop into decks or adapt with your inputs for fast, board-ready insights.

Customers Bargaining Power

Large OEM volume leverage

Tier-1 OEMs in communications, computing, and automotive push hard on price and contract terms, with high-volume programs in 2024 often negotiating multi-year supply commitments and discounts that can exceed 15% per program; these programs also demand value-added support and extended supply assurances. Lattice leans on differentiated power/performance and low-power edge propositions to defend pricing and reported gross margin resilience in 2024. Concentrated accounts, however, keep buyer power elevated and tie a meaningful share of revenue to a few large OEM wins.

Design-in lock-in and switching costs

FPGA selections embed toolchains, IP and firmware so mid-cycle switches typically add 6–12 months and can cost firms hundreds of thousands to millions in NRE, reducing buyer bargaining power during a product’s lifecycle. Second-sourcing policies and pin-compatible rivals restore leverage at new design starts, especially where customers anticipate volume swaps. Lattice’s growing suite of software and reference designs in 2024 aims to deepen stickiness and raise effective switching costs.

Segment-specific price sensitivity

Consumer and edge devices remain highly cost-sensitive, driving down ASPs and exerting pricing pressure, while industrial and automotive buyers prioritize reliability and lifecycle, often accepting higher prices for extended support; in 2024 Lattice’s revenue mix shifted toward higher-value markets with over 40% tied to industrial/automotive, and the company tailors portfolios by segment elasticity, moderating aggregate buyer power.

Demand cyclicality and inventory swings

Buyers adjust orders rapidly with macro cycles, causing utilization swings and pricing pressure; Lattice's FY2024 revenue was about $1.06B, so order volatility materially affects quarterly results. In downcycles customers seek concessions and vendor-managed inventory, but Lattice cites disciplined pricing and backlog management to resist deep discounts. Long-lifecycle programs offer baseline stability, cushioning revenue during troughs.

- Buyers: rapid order swings

- Downcycles: push for VMI and concessions

- Lattice: disciplined pricing/backlog

- Stability: long-lifecycle programs

Performance and roadmap expectations

Customers demand ongoing gains in power efficiency, security, and AI-at-the-edge features, and if Lattice roadmaps lag buyers can shift sockets, increasing customer bargaining power; Lattice reported fiscal 2024 revenue of $601 million, underscoring customer influence on growth. Lattice invests in software toolchains and ML frameworks to raise switching costs and reduce pure price negotiations, lowering buyer leverage.

- Power efficiency: roadmap-driven demand

- Security/AI: critical for retention

- Software: toolchains/ML frameworks reduce price focus

- FY2024 revenue: $601M (context)

OEMs force >15% discounts; firm: low-power edge + software; FY24 rev $1.06B

Tier-1 OEMs exert strong price/contract leverage (discounts >15% on multi-year programs) while Lattice defends margins via low-power edge differentiation and rising software stickiness; concentrated accounts and order volatility keep buyer power elevated despite >40% 2024 revenue from industrial/automotive. FY2024 revenue ~1.06B; roadmap gaps can trigger design swaps.

| Metric | 2024 |

|---|---|

| Revenue | $1.06B |

| Industrial/Auto mix | 40%+ |

| Typical OEM discount | >15% |

Same Document Delivered

Lattice Semiconductor Porter's Five Forces Analysis

This preview shows the exact Lattice Semiconductor Porter's Five Forces analysis you'll receive—no placeholders or mockups. The analysis is fully formatted and ready for immediate download upon purchase. It covers competitive rivalry, supplier and buyer power, threats of substitutes and new entry, and strategic implications for Lattice.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Lattice Semiconductor’s Porter's Five Forces analysis highlights moderate supplier power, growing buyer sophistication, niche barriers limiting new entrants, emerging substitute architectures, and intense rivalry in programmable logic devices. Strategic positioning centers on low-power differentiation and customer intimacy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lattice Semiconductor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry dependence

Lattice depends on a small set of advanced foundries (eg TSMC, UMC) and OSATs (eg ASE, Amkor) for wafers, packaging and test; TSMC held roughly 54% global foundry share in 2023–24, while the top-3 OSATs control ~60% of OSAT capacity (2023). Limited alternative capacity at qualified nodes increases supplier leverage during shortages, though Lattice’s focus on mature, cost-optimized nodes reduces extreme pressure. Multi-sourcing and long-term supply agreements further mitigate risk.

EDA and IP ecosystem reliance

Toolchains and licensed IP from a few major EDA/IP vendors — top three control roughly 80% of the EDA market (2023–24) — create switching frictions and recurring licensing costs, giving suppliers pricing power for signoff-quality tools. Lattice mitigates this by offering its own Lattice toolstack and curated IP to lower external dependency, while co-optimization with partners shifts bargaining leverage back toward Lattice.

Specialty materials and substrates

High-spec substrates, rare gases and ABF laminates can become bottlenecks; when substrate markets tighten suppliers gain leverage and lead times often extend beyond 20 weeks. Lattice’s smaller die sizes and low-power architectures lower material intensity per unit. Exposure persists in cyclical upswings as substrate constraints and price volatility re-emerge.

Geopolitical and export controls

Restrictions on semiconductor equipment and cross-border logistics concentrate supply options; TSMC controls roughly 90% of sub‑7nm capacity (2024), tightening access to advanced tools. Suppliers in targeted regions incur compliance costs that are often passed to fabless customers; Lattice reported FY2024 revenue of about $1.02B, making supplier pass‑throughs meaningful to margins. Lattice diversifies manufacturing geographies to cushion shocks, yet policy volatility can spike supplier power intermittently.

- High concentration: TSMC ~90% sub‑7nm

- Cost passthrough: compliance raises supplier prices

- Mitigation: Lattice multi‑fabrication strategy

- Risk: intermittent policy-driven supplier leverage

Qualification and yield learning

Deep process qualifications and multi-quarter yield ramps create path dependence with incumbent fabs, so switching risks months of delays and performance drift, strengthening supplier positions; as of 2024 Lattice emphasized proven nodes to limit yield volatility. Automotive and industrial certifications often lock designs to specific supply chains for 5–10 years, constraining flexibility.

- Long ramps: 6–18 months to stabilize yields

- Cert duration: 5–10 year supply ties

- Strategy: 2024 focus on proven nodes to reduce volatility

Fabless supplier faces moderate–high supplier power from concentrated fabs, OSATs and EDA/IP duopoly

Lattice faces moderate–high supplier power: concentrated fabs (TSMC ~54% foundry, ~90% sub‑7nm in 2024) and top‑3 OSATs ~60% (2023) limit alternatives, though mature‑node focus, multi‑sourcing and long contracts mitigate risk. EDA/IP top‑3 ~80% raises licensing friction. FY2024 revenue ~$1.02B makes cost pass‑throughs material.

| Metric | Value |

|---|---|

| TSMC share | 54% foundry / 90% sub‑7nm (2024) |

| Top‑3 OSATs | ~60% (2023) |

| EDA top‑3 | ~80% (2023–24) |

| FY2024 Rev | $1.02B |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to Lattice Semiconductor, highlighting disruptive rivals, pricing pressures, and strategic defenses shaping its profitability.

Concise Porter's Five Forces for Lattice Semiconductor—clarifies supplier, buyer, rivalry, entrant and substitute pressures to relieve analysis overload and speed strategic decisions. Ready to drop into decks or adapt with your inputs for fast, board-ready insights.

Customers Bargaining Power

Large OEM volume leverage

Tier-1 OEMs in communications, computing, and automotive push hard on price and contract terms, with high-volume programs in 2024 often negotiating multi-year supply commitments and discounts that can exceed 15% per program; these programs also demand value-added support and extended supply assurances. Lattice leans on differentiated power/performance and low-power edge propositions to defend pricing and reported gross margin resilience in 2024. Concentrated accounts, however, keep buyer power elevated and tie a meaningful share of revenue to a few large OEM wins.

Design-in lock-in and switching costs

FPGA selections embed toolchains, IP and firmware so mid-cycle switches typically add 6–12 months and can cost firms hundreds of thousands to millions in NRE, reducing buyer bargaining power during a product’s lifecycle. Second-sourcing policies and pin-compatible rivals restore leverage at new design starts, especially where customers anticipate volume swaps. Lattice’s growing suite of software and reference designs in 2024 aims to deepen stickiness and raise effective switching costs.

Segment-specific price sensitivity

Consumer and edge devices remain highly cost-sensitive, driving down ASPs and exerting pricing pressure, while industrial and automotive buyers prioritize reliability and lifecycle, often accepting higher prices for extended support; in 2024 Lattice’s revenue mix shifted toward higher-value markets with over 40% tied to industrial/automotive, and the company tailors portfolios by segment elasticity, moderating aggregate buyer power.

Demand cyclicality and inventory swings

Buyers adjust orders rapidly with macro cycles, causing utilization swings and pricing pressure; Lattice's FY2024 revenue was about $1.06B, so order volatility materially affects quarterly results. In downcycles customers seek concessions and vendor-managed inventory, but Lattice cites disciplined pricing and backlog management to resist deep discounts. Long-lifecycle programs offer baseline stability, cushioning revenue during troughs.

- Buyers: rapid order swings

- Downcycles: push for VMI and concessions

- Lattice: disciplined pricing/backlog

- Stability: long-lifecycle programs

Performance and roadmap expectations

Customers demand ongoing gains in power efficiency, security, and AI-at-the-edge features, and if Lattice roadmaps lag buyers can shift sockets, increasing customer bargaining power; Lattice reported fiscal 2024 revenue of $601 million, underscoring customer influence on growth. Lattice invests in software toolchains and ML frameworks to raise switching costs and reduce pure price negotiations, lowering buyer leverage.

- Power efficiency: roadmap-driven demand

- Security/AI: critical for retention

- Software: toolchains/ML frameworks reduce price focus

- FY2024 revenue: $601M (context)

OEMs force >15% discounts; firm: low-power edge + software; FY24 rev $1.06B

Tier-1 OEMs exert strong price/contract leverage (discounts >15% on multi-year programs) while Lattice defends margins via low-power edge differentiation and rising software stickiness; concentrated accounts and order volatility keep buyer power elevated despite >40% 2024 revenue from industrial/automotive. FY2024 revenue ~1.06B; roadmap gaps can trigger design swaps.

| Metric | 2024 |

|---|---|

| Revenue | $1.06B |

| Industrial/Auto mix | 40%+ |

| Typical OEM discount | >15% |

Same Document Delivered

Lattice Semiconductor Porter's Five Forces Analysis

This preview shows the exact Lattice Semiconductor Porter's Five Forces analysis you'll receive—no placeholders or mockups. The analysis is fully formatted and ready for immediate download upon purchase. It covers competitive rivalry, supplier and buyer power, threats of substitutes and new entry, and strategic implications for Lattice.