Leadcorp Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

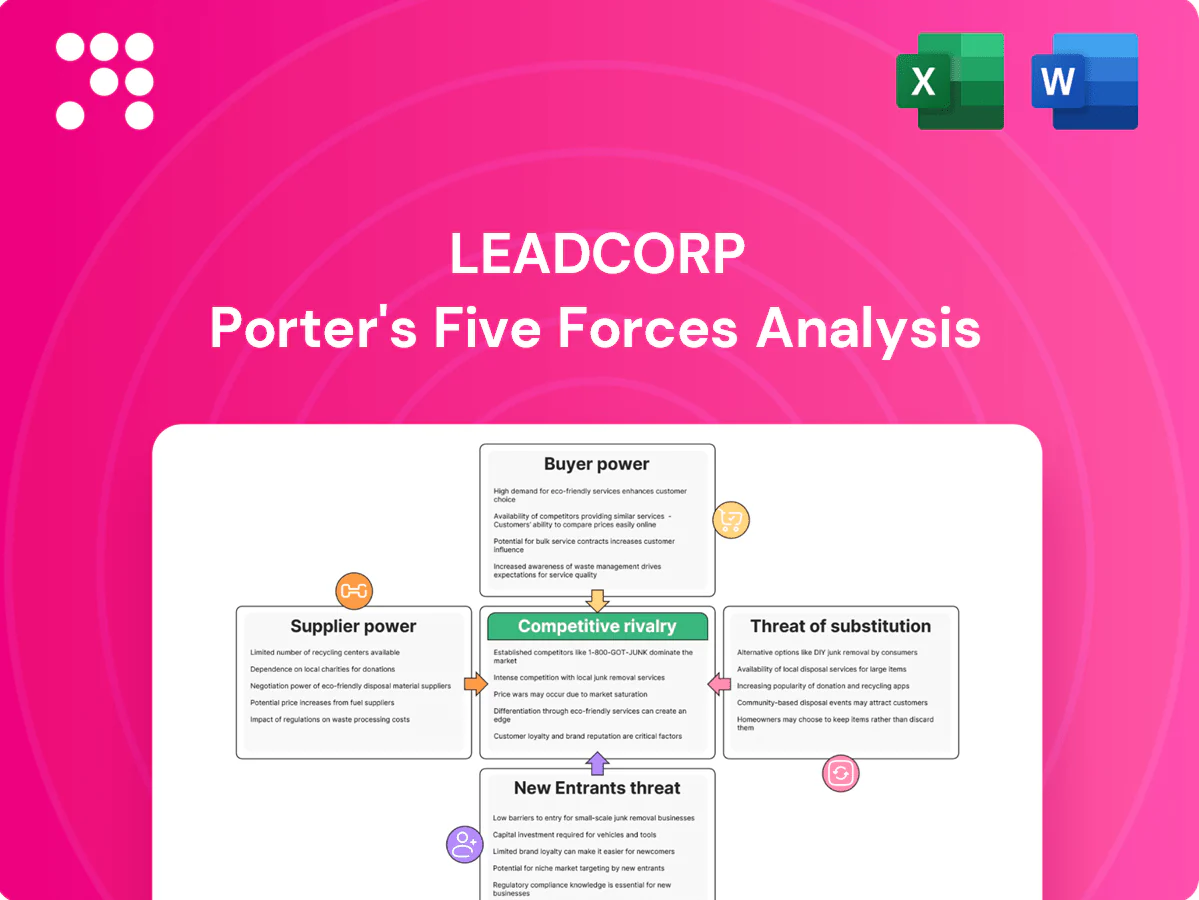

Leadcorp’s Porter's Five Forces snapshot highlights key pressures—from buyer bargaining to competitive rivalry—and hints at strategic levers management can use. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated crude and refinery sources

Japan imports over 90% of its crude and supply is concentrated among a few major refiners and trading houses, with ENEOS Holdings the largest domestic refiner. Contract terms and refinery utilization rates directly affect wholesale allocations and pricing. 2024 OPEC+ adjustments and geopolitical shocks lifted Brent to roughly mid-$80s/bbl, exposing Leadcorp’s petroleum margins to upstream concentration.

NEXCO concessions and landlords

Highway rest stations operate under concession and lease frameworks set by NEXCO East/Central/West and local authorities, with terms—rent, service standards, investment obligations—dictating operating margins; as of 2024 NEXCO comprises three regional companies managing Japan’s roughly 9,000 km expressway network. Limited alternative roadside sites heighten landlord bargaining power, and renewal risk can compress projected cash flows and complicate capital planning for operators.

Fuel equipment and maintenance vendors

Pump, POS and safety system suppliers require vendor-specific certifications and recertification; switching causes downtime, retraining and compliance testing often spanning days to weeks, reducing station uptime. Spare-parts lead times drive bargaining leverage; multi-year service contracts (commonly 3–5 years) lock pricing and limit short-term renegotiation.

Funding providers for consumer credit

Funding providers for consumer credit determine lending spreads through the cost and availability of wholesale funding; the US federal funds rate ended 2024 at 5.25–5.50%, tightening wholesale funding and lifting spreads. Rising rates and tighter covenants increase providers' bargaining power, while issuer ratings and ABS/securitization market conditions shape pricing and access. Diversifying across banks and instruments reduces concentration risk and weakens supplier power.

- Wholesale funding cost: fed funds 5.25–5.50% (Dec 2024)

- Ratings/securitization: primary determinants of terms

- Diversification: multiple banks/instruments mitigates concentration

Data, networks, and IT providers

Data, networks and IT vendors — credit bureaus (Experian, Equifax, TransUnion cover ~300M US consumers), payment networks, KYC/AML tools and cloud providers are critical inputs for Leadcorp. Compliance and integration create switching frictions; outages or price hikes (top cloud providers hold ~70% share in 2024) can disrupt operations and risk controls. Vendor diversification and in-house tooling reduce exposure.

- Credit bureaus: ~300M US consumers

- Cloud concentration: ~70% by top 3 (2024)

- Mitigants: vendor diversification, in-house tooling

Suppliers exert high power: crude >90% imports, Brent mid-$80s, expressways constrain sites

Suppliers exert high bargaining power: crude imports >90% (ENEOS dominant), Brent ~mid-$80s/bbl (2024) compresses margins; NEXCO controls ~9,000 km expressways, limiting site options and raising lease power; vendors (cloud top3 ~70%, credit bureaus ~300M records) create switching frictions—diversification and multiyear contracts are primary mitigants.

| Metric | 2024 |

|---|---|

| Crude import share | >90% |

| Brent | mid-$80s/bbl |

| Expressway km | ~9,000 |

| Cloud top3 | ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Leadcorp that uncovers key drivers of competition, buyer and supplier power, substitutes and entry risks, and identifies emerging threats to market share. Delivered in fully editable Word format for easy customization and inclusion in investor decks or strategic plans.

One-sheet Leadcorp Porter’s Five Forces—instantly visualizes competitive pressure with an editable spider chart, simple layout for decks, and plug-and-play data fields so teams can assess scenarios without complex tools.

Customers Bargaining Power

Price-sensitive fuel consumers

Fuel buyers compare posted prices and apps in real time, making local demand highly elastic: studies in 2024 show volume shifts from price gaps as small as $0.02–$0.05 per liter. Loyalty schemes can reduce churn by roughly 10% but are easily replicated by competitors. Convenience, forecourt services and bundled retail can command a 3–5 cent per liter premium, partly offsetting pure price sensitivity.

Highway travelers with convenience needs

On-expressway customers prioritize speed, cleanliness and amenities; NACS 2024 notes convenience stores capture roughly 70% of U.S. motor fuel sales and an average in-store basket of about $6.50, so captive traffic reduces price sensitivity versus off-highway options. Service expectations are high and a poor experience often prompts detours to rival service areas, while bundled offers (fuel+food+services) measurably raise basket size and lower switching.

Credit customers shopping APR and fees

Consumers actively shop APRs and fees—average US credit card APRs were about 20–23% in 2024 while BNPL and fintech often advertise 0–36% equivalent APRs, pushing price competition. With ~30% of US shoppers using BNPL in 2024 and digital onboarding cutting approval to under 10 minutes, switching costs are modest. Clear disclosures increase sensitivity to total cost of credit, though rewards and wide merchant acceptance help defend pricing.

Corporate and fleet accounts

Corporate and fleet buyers extract volume discounts and strict service-level terms, driving margin pressure and operational commitments; contract renewals trigger competitive bidding that can compress rates. Payment terms and granular data reporting (usage/fuel/miles) are often decisive purchasing levers. Losing a single large account can cut volumes by 10% or more for comparable mobility providers in 2024.

- Volume discounts / SLAs

- Renewals = competitive bids

- Payment terms & data reporting = differentiators

- Single-account loss >10% volume risk (2024)

Multi-homing and channel transparency

Customers increasingly multi-home: 2024 surveys show around 64% of motorists use multiple credit lines and compare 2–3 fuel providers per trip, reducing dependency on any single supplier.

Channel transparency via apps and aggregators amplifies offer comparison, driving price and loyalty sensitivity for Leadcorp.

Leadcorp must sustain consistent value propositions and targeted incentives to protect share of wallet and limit churn.

- multi-homing: high (≈64% in 2024)

- comparability: apps enable instant price checks

- risk: share-of-wallet erosion

Drivers switch on $0.02–$0.05/L, convenience adds 3–5¢/L

Customers are highly price-sensitive—volume shifts from $0.02–$0.05/L gaps—while loyalty cuts churn ~10% and convenience can add a 3–5¢/L premium. Convenience stores capture ~70% of US fuel sales, creating captive demand, yet 64% of motorists multi-home and apps enable instant comparisons. Corporate/fleet contracts drive volume discounts; losing one account can cut volumes >10%.

| Metric | 2024 Value |

|---|---|

| Price gap sensitivity | $0.02–$0.05/L |

| Loyalty churn reduction | ≈10% |

| Convenience premium | 3–5¢/L |

| Multi-homing | 64% |

| Convenience share | 70% |

Preview the Actual Deliverable

Leadcorp Porter's Five Forces Analysis

This preview shows the exact Leadcorp Porter's Five Forces analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical document.

Go Beyond the Preview—Access the Full Strategic Report

Leadcorp’s Porter's Five Forces snapshot highlights key pressures—from buyer bargaining to competitive rivalry—and hints at strategic levers management can use. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated crude and refinery sources

Japan imports over 90% of its crude and supply is concentrated among a few major refiners and trading houses, with ENEOS Holdings the largest domestic refiner. Contract terms and refinery utilization rates directly affect wholesale allocations and pricing. 2024 OPEC+ adjustments and geopolitical shocks lifted Brent to roughly mid-$80s/bbl, exposing Leadcorp’s petroleum margins to upstream concentration.

NEXCO concessions and landlords

Highway rest stations operate under concession and lease frameworks set by NEXCO East/Central/West and local authorities, with terms—rent, service standards, investment obligations—dictating operating margins; as of 2024 NEXCO comprises three regional companies managing Japan’s roughly 9,000 km expressway network. Limited alternative roadside sites heighten landlord bargaining power, and renewal risk can compress projected cash flows and complicate capital planning for operators.

Fuel equipment and maintenance vendors

Pump, POS and safety system suppliers require vendor-specific certifications and recertification; switching causes downtime, retraining and compliance testing often spanning days to weeks, reducing station uptime. Spare-parts lead times drive bargaining leverage; multi-year service contracts (commonly 3–5 years) lock pricing and limit short-term renegotiation.

Funding providers for consumer credit

Funding providers for consumer credit determine lending spreads through the cost and availability of wholesale funding; the US federal funds rate ended 2024 at 5.25–5.50%, tightening wholesale funding and lifting spreads. Rising rates and tighter covenants increase providers' bargaining power, while issuer ratings and ABS/securitization market conditions shape pricing and access. Diversifying across banks and instruments reduces concentration risk and weakens supplier power.

- Wholesale funding cost: fed funds 5.25–5.50% (Dec 2024)

- Ratings/securitization: primary determinants of terms

- Diversification: multiple banks/instruments mitigates concentration

Data, networks, and IT providers

Data, networks and IT vendors — credit bureaus (Experian, Equifax, TransUnion cover ~300M US consumers), payment networks, KYC/AML tools and cloud providers are critical inputs for Leadcorp. Compliance and integration create switching frictions; outages or price hikes (top cloud providers hold ~70% share in 2024) can disrupt operations and risk controls. Vendor diversification and in-house tooling reduce exposure.

- Credit bureaus: ~300M US consumers

- Cloud concentration: ~70% by top 3 (2024)

- Mitigants: vendor diversification, in-house tooling

Suppliers exert high power: crude >90% imports, Brent mid-$80s, expressways constrain sites

Suppliers exert high bargaining power: crude imports >90% (ENEOS dominant), Brent ~mid-$80s/bbl (2024) compresses margins; NEXCO controls ~9,000 km expressways, limiting site options and raising lease power; vendors (cloud top3 ~70%, credit bureaus ~300M records) create switching frictions—diversification and multiyear contracts are primary mitigants.

| Metric | 2024 |

|---|---|

| Crude import share | >90% |

| Brent | mid-$80s/bbl |

| Expressway km | ~9,000 |

| Cloud top3 | ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Leadcorp that uncovers key drivers of competition, buyer and supplier power, substitutes and entry risks, and identifies emerging threats to market share. Delivered in fully editable Word format for easy customization and inclusion in investor decks or strategic plans.

One-sheet Leadcorp Porter’s Five Forces—instantly visualizes competitive pressure with an editable spider chart, simple layout for decks, and plug-and-play data fields so teams can assess scenarios without complex tools.

Customers Bargaining Power

Price-sensitive fuel consumers

Fuel buyers compare posted prices and apps in real time, making local demand highly elastic: studies in 2024 show volume shifts from price gaps as small as $0.02–$0.05 per liter. Loyalty schemes can reduce churn by roughly 10% but are easily replicated by competitors. Convenience, forecourt services and bundled retail can command a 3–5 cent per liter premium, partly offsetting pure price sensitivity.

Highway travelers with convenience needs

On-expressway customers prioritize speed, cleanliness and amenities; NACS 2024 notes convenience stores capture roughly 70% of U.S. motor fuel sales and an average in-store basket of about $6.50, so captive traffic reduces price sensitivity versus off-highway options. Service expectations are high and a poor experience often prompts detours to rival service areas, while bundled offers (fuel+food+services) measurably raise basket size and lower switching.

Credit customers shopping APR and fees

Consumers actively shop APRs and fees—average US credit card APRs were about 20–23% in 2024 while BNPL and fintech often advertise 0–36% equivalent APRs, pushing price competition. With ~30% of US shoppers using BNPL in 2024 and digital onboarding cutting approval to under 10 minutes, switching costs are modest. Clear disclosures increase sensitivity to total cost of credit, though rewards and wide merchant acceptance help defend pricing.

Corporate and fleet accounts

Corporate and fleet buyers extract volume discounts and strict service-level terms, driving margin pressure and operational commitments; contract renewals trigger competitive bidding that can compress rates. Payment terms and granular data reporting (usage/fuel/miles) are often decisive purchasing levers. Losing a single large account can cut volumes by 10% or more for comparable mobility providers in 2024.

- Volume discounts / SLAs

- Renewals = competitive bids

- Payment terms & data reporting = differentiators

- Single-account loss >10% volume risk (2024)

Multi-homing and channel transparency

Customers increasingly multi-home: 2024 surveys show around 64% of motorists use multiple credit lines and compare 2–3 fuel providers per trip, reducing dependency on any single supplier.

Channel transparency via apps and aggregators amplifies offer comparison, driving price and loyalty sensitivity for Leadcorp.

Leadcorp must sustain consistent value propositions and targeted incentives to protect share of wallet and limit churn.

- multi-homing: high (≈64% in 2024)

- comparability: apps enable instant price checks

- risk: share-of-wallet erosion

Drivers switch on $0.02–$0.05/L, convenience adds 3–5¢/L

Customers are highly price-sensitive—volume shifts from $0.02–$0.05/L gaps—while loyalty cuts churn ~10% and convenience can add a 3–5¢/L premium. Convenience stores capture ~70% of US fuel sales, creating captive demand, yet 64% of motorists multi-home and apps enable instant comparisons. Corporate/fleet contracts drive volume discounts; losing one account can cut volumes >10%.

| Metric | 2024 Value |

|---|---|

| Price gap sensitivity | $0.02–$0.05/L |

| Loyalty churn reduction | ≈10% |

| Convenience premium | 3–5¢/L |

| Multi-homing | 64% |

| Convenience share | 70% |

Preview the Actual Deliverable

Leadcorp Porter's Five Forces Analysis

This preview shows the exact Leadcorp Porter's Five Forces analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical document.

Description

Go Beyond the Preview—Access the Full Strategic Report

Leadcorp’s Porter's Five Forces snapshot highlights key pressures—from buyer bargaining to competitive rivalry—and hints at strategic levers management can use. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated crude and refinery sources

Japan imports over 90% of its crude and supply is concentrated among a few major refiners and trading houses, with ENEOS Holdings the largest domestic refiner. Contract terms and refinery utilization rates directly affect wholesale allocations and pricing. 2024 OPEC+ adjustments and geopolitical shocks lifted Brent to roughly mid-$80s/bbl, exposing Leadcorp’s petroleum margins to upstream concentration.

NEXCO concessions and landlords

Highway rest stations operate under concession and lease frameworks set by NEXCO East/Central/West and local authorities, with terms—rent, service standards, investment obligations—dictating operating margins; as of 2024 NEXCO comprises three regional companies managing Japan’s roughly 9,000 km expressway network. Limited alternative roadside sites heighten landlord bargaining power, and renewal risk can compress projected cash flows and complicate capital planning for operators.

Fuel equipment and maintenance vendors

Pump, POS and safety system suppliers require vendor-specific certifications and recertification; switching causes downtime, retraining and compliance testing often spanning days to weeks, reducing station uptime. Spare-parts lead times drive bargaining leverage; multi-year service contracts (commonly 3–5 years) lock pricing and limit short-term renegotiation.

Funding providers for consumer credit

Funding providers for consumer credit determine lending spreads through the cost and availability of wholesale funding; the US federal funds rate ended 2024 at 5.25–5.50%, tightening wholesale funding and lifting spreads. Rising rates and tighter covenants increase providers' bargaining power, while issuer ratings and ABS/securitization market conditions shape pricing and access. Diversifying across banks and instruments reduces concentration risk and weakens supplier power.

- Wholesale funding cost: fed funds 5.25–5.50% (Dec 2024)

- Ratings/securitization: primary determinants of terms

- Diversification: multiple banks/instruments mitigates concentration

Data, networks, and IT providers

Data, networks and IT vendors — credit bureaus (Experian, Equifax, TransUnion cover ~300M US consumers), payment networks, KYC/AML tools and cloud providers are critical inputs for Leadcorp. Compliance and integration create switching frictions; outages or price hikes (top cloud providers hold ~70% share in 2024) can disrupt operations and risk controls. Vendor diversification and in-house tooling reduce exposure.

- Credit bureaus: ~300M US consumers

- Cloud concentration: ~70% by top 3 (2024)

- Mitigants: vendor diversification, in-house tooling

Suppliers exert high power: crude >90% imports, Brent mid-$80s, expressways constrain sites

Suppliers exert high bargaining power: crude imports >90% (ENEOS dominant), Brent ~mid-$80s/bbl (2024) compresses margins; NEXCO controls ~9,000 km expressways, limiting site options and raising lease power; vendors (cloud top3 ~70%, credit bureaus ~300M records) create switching frictions—diversification and multiyear contracts are primary mitigants.

| Metric | 2024 |

|---|---|

| Crude import share | >90% |

| Brent | mid-$80s/bbl |

| Expressway km | ~9,000 |

| Cloud top3 | ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Leadcorp that uncovers key drivers of competition, buyer and supplier power, substitutes and entry risks, and identifies emerging threats to market share. Delivered in fully editable Word format for easy customization and inclusion in investor decks or strategic plans.

One-sheet Leadcorp Porter’s Five Forces—instantly visualizes competitive pressure with an editable spider chart, simple layout for decks, and plug-and-play data fields so teams can assess scenarios without complex tools.

Customers Bargaining Power

Price-sensitive fuel consumers

Fuel buyers compare posted prices and apps in real time, making local demand highly elastic: studies in 2024 show volume shifts from price gaps as small as $0.02–$0.05 per liter. Loyalty schemes can reduce churn by roughly 10% but are easily replicated by competitors. Convenience, forecourt services and bundled retail can command a 3–5 cent per liter premium, partly offsetting pure price sensitivity.

Highway travelers with convenience needs

On-expressway customers prioritize speed, cleanliness and amenities; NACS 2024 notes convenience stores capture roughly 70% of U.S. motor fuel sales and an average in-store basket of about $6.50, so captive traffic reduces price sensitivity versus off-highway options. Service expectations are high and a poor experience often prompts detours to rival service areas, while bundled offers (fuel+food+services) measurably raise basket size and lower switching.

Credit customers shopping APR and fees

Consumers actively shop APRs and fees—average US credit card APRs were about 20–23% in 2024 while BNPL and fintech often advertise 0–36% equivalent APRs, pushing price competition. With ~30% of US shoppers using BNPL in 2024 and digital onboarding cutting approval to under 10 minutes, switching costs are modest. Clear disclosures increase sensitivity to total cost of credit, though rewards and wide merchant acceptance help defend pricing.

Corporate and fleet accounts

Corporate and fleet buyers extract volume discounts and strict service-level terms, driving margin pressure and operational commitments; contract renewals trigger competitive bidding that can compress rates. Payment terms and granular data reporting (usage/fuel/miles) are often decisive purchasing levers. Losing a single large account can cut volumes by 10% or more for comparable mobility providers in 2024.

- Volume discounts / SLAs

- Renewals = competitive bids

- Payment terms & data reporting = differentiators

- Single-account loss >10% volume risk (2024)

Multi-homing and channel transparency

Customers increasingly multi-home: 2024 surveys show around 64% of motorists use multiple credit lines and compare 2–3 fuel providers per trip, reducing dependency on any single supplier.

Channel transparency via apps and aggregators amplifies offer comparison, driving price and loyalty sensitivity for Leadcorp.

Leadcorp must sustain consistent value propositions and targeted incentives to protect share of wallet and limit churn.

- multi-homing: high (≈64% in 2024)

- comparability: apps enable instant price checks

- risk: share-of-wallet erosion

Drivers switch on $0.02–$0.05/L, convenience adds 3–5¢/L

Customers are highly price-sensitive—volume shifts from $0.02–$0.05/L gaps—while loyalty cuts churn ~10% and convenience can add a 3–5¢/L premium. Convenience stores capture ~70% of US fuel sales, creating captive demand, yet 64% of motorists multi-home and apps enable instant comparisons. Corporate/fleet contracts drive volume discounts; losing one account can cut volumes >10%.

| Metric | 2024 Value |

|---|---|

| Price gap sensitivity | $0.02–$0.05/L |

| Loyalty churn reduction | ≈10% |

| Convenience premium | 3–5¢/L |

| Multi-homing | 64% |

| Convenience share | 70% |

Preview the Actual Deliverable

Leadcorp Porter's Five Forces Analysis

This preview shows the exact Leadcorp Porter's Five Forces analysis you’ll receive after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for immediate download and use. Purchase grants instant access to this identical document.