Lear PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, market cycles, and tech disruption are reshaping Lear’s strategy in our expert PESTLE Analysis. This concise briefing highlights risks and opportunities—buy the full report to access detailed, ready-to-use insights and actionable recommendations.

Political factors

Trade policy volatility

Shifts in US–China tariff regimes, including Section 301 duties of up to 25% on roughly $300 billion of Chinese goods, can quickly raise costs for wiring, electronics and seat components and force rerouting of supply chains. Lear must hedge import-duty exposure through tariff engineering, sourcing agreements and duty drawback strategies. Diversifying regional production across North America, Europe and Asia mitigates tariff shocks, while proactive trade compliance preserves delivery reliability to global OEMs.

Industrial policy and EV incentives

Government subsidies and local-content rules—driven by the US Inflation Reduction Act (IRA) which mobilized about $369 billion and includes a clean vehicle tax credit up to $7,500 with domestic content bonuses—are reshaping E-Systems demand and plant footprints. Battery and electronics tax credits in key markets favor regionalized manufacturing, prompting Lear to align investments to policy-rich geographies. Rapid policy reversals, however, risk stranded capacity and capital write-offs.

Geopolitical tensions and sanctions

Conflicts and sanction regimes (eg Russia/Ukraine, tightened US export controls 2022–24) have repeatedly disrupted suppliers and logistics lanes, raising lead times for auto parts and electronics. Critical minerals — DRC supplies ~70% of mined cobalt and China processes >80% of refined battery materials — and semiconductors face export controls. Lear needs multi-source strategies for high-risk inputs. Scenario planning supports uninterrupted OEM supply.

Labor and industrial relations

Minimum wage trajectories and union talks affect Lear's cost and flexibility: US federal wage remains $7.25/hr while California reached $16/hr in 2024; UAW 2023 contracts yielded roughly 20% wage gains, raising supplier wage pressure. Cross-border minima (e.g., Germany €12/hr) complicate capacity planning; stable relations support quality and delivery; localization eases political scrutiny.

- Minimums: US $7.25, CA $16 (2024); UAW +~20% (2023)

- Cross-border variance: Germany €12/hr

- Impact: stability reduces disruptions; localization lowers political risk

Public procurement and standards influence

States shape OEM safety, sustainability and connectivity norms; public procurement drives requirements for over-the-air updates, cybersecurity and ISO/SAE interfaces, with EVs reaching about 14% of global new-car sales in 2023 (IEA). Large public fleets and procurement programs—supported by US Infrastructure Law EV charger funding of 7.5 billion USD—can force OEMs into advanced E-System architectures. Engagement with standards bodies (ISO, SAE, CEN) sets technical specs while advocacy steers regulatory roadmaps.

- Policy impact: public procurement mandates

- Fleet catalyst: forces EV e-system design

- Standards: ISO/SAE/CEN shape specs

- Advocacy: aligns product roadmaps with regs

Tariffs 25%, IRA $369B, DRC 70%

Trade tariffs (eg Section 301 up to 25% on ~$300B goods) and IRA incentives ($369B; EV credit up to $7,500) force Lear to regionalize sourcing and align investments. Sanctions, export controls and concentrated mineral processing (DRC ~70% cobalt; China >80% refined materials) require multi-source risk plans. Labor costs and union settlements (UAW +~20% 2023; US $7.25; CA $16 2024; DE €12) affect location and margin decisions.

| Risk | Key data |

|---|---|

| Tariffs | Section 301 25% on ~$300B |

| Incentives | IRA $369B; EV credit $7,500 |

| Critical minerals | DRC ~70% cobalt; China >80% refining |

| Labor | UAW +20% (2023); US $7.25; CA $16; DE €12 |

What is included in the product

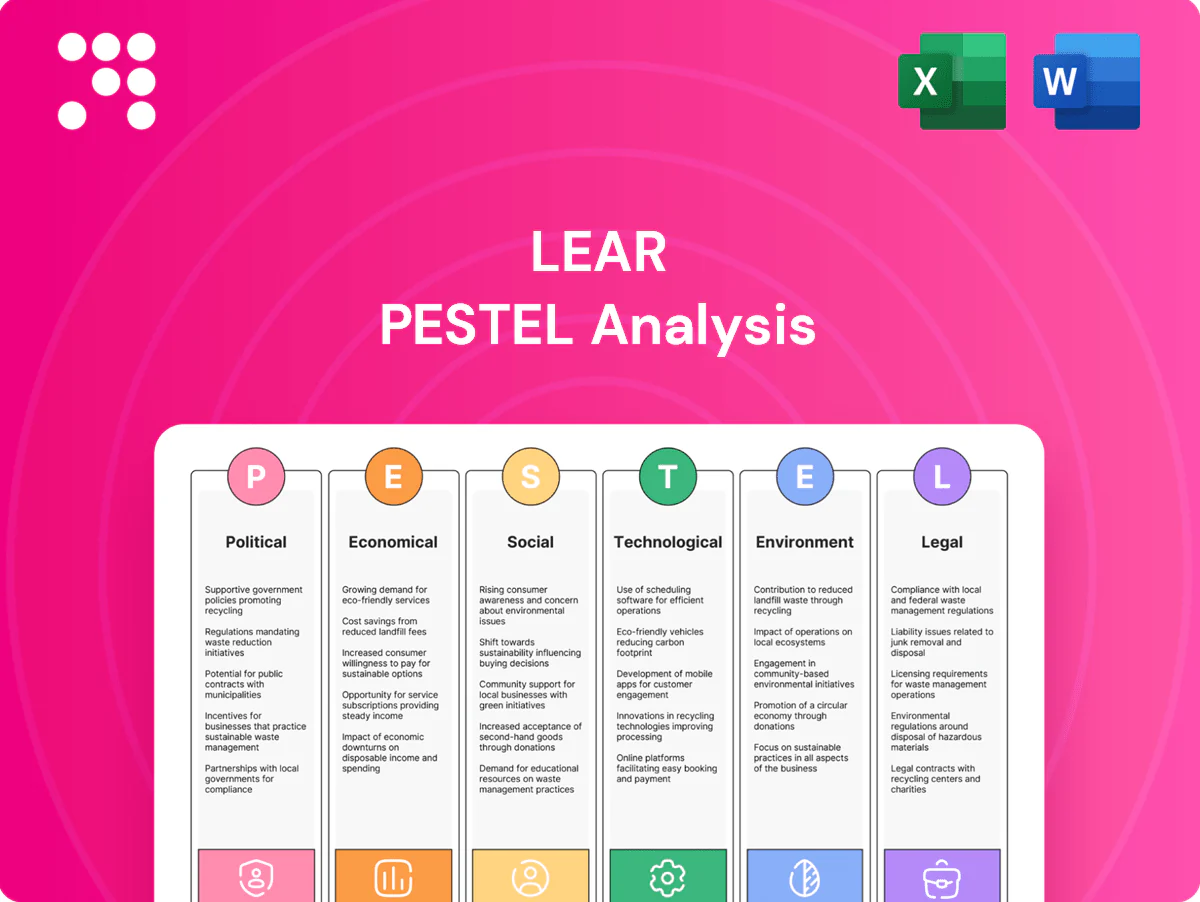

Explores how external macro-environmental factors uniquely affect Lear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section supported by current data and industry trends to reveal specific threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategy.

Concise, visually segmented Lear PESTLE summary that distills external risks and opportunities into an easily editable, shareable format—ideal for quick insertion into presentations, team alignment, and strategy sessions.

Economic factors

Auto demand cyclicality

OEM build schedules swing with GDP, employment and consumer confidence—US light‑vehicle sales were about 15.3M units in 2024 and global production ran near 78M, driving order volatility for suppliers. Seating volumes and E‑Systems orders closely mirror production levels, while Lear's flexible cost structure (shiftable production, variable labor) helps weather downturns. Rising content‑per‑vehicle—roughly a 3% annual electronics content CAGR—offsets unit volatility.

Commodity and input price swings

Copper, aluminum, steel, resins and rare earths drive Lear’s BOM — market moves in 2024 showed copper +12% YoY, aluminum +8%, steel +10%, resins +15% and select rare earths up ~25%, materially pressuring margins. Wiring‑grade copper supply tightness has tightened premiums and squeezed margins in 2024–H1 2025. Index‑linked pricing and hedging programs have dampened volatility, while design‑to‑cost and material substitution initiatives further protect profitability.

FX and regional mix

Lear operates with revenues and costs across USD, EUR, CNY and MXN; mid‑2025 FX levels were roughly EUR/USD 1.09, CNY/USD 7.25 and MXN/USD 17.5, creating translation and transaction risk. Currency mismatches have materially compressed supplier margins in past FX swings. Natural hedging via local sourcing and production footprint reduces exposure. Where possible, pricing clauses with OEMs shift part of FX risk back to customers.

Logistics and supply chain resilience

Freight rates, which fell roughly 60–70% from 2021 peaks into 2024, and lead times (now ~30–40 days for many routes) continue to strain just-in-time operations at Lear, raising stockout risk and cost variability. Nearshoring and dual sourcing—reflected in rising Mexico and US parts flows—cut disruption exposure, while many OEMs hold ~8–12 weeks of chips/connectors as buffers. Increased adoption of digital visibility and control towers (≈35% of large manufacturers by 2024) speeds corrective actions and reduces recovery time.

- Freight rates down 60–70% vs 2021

- Lead times ~30–40 days

- Chip/connectors buffers ~8–12 weeks

- Control tower adoption ≈35% (2024)

- Nearshoring/dual sourcing rising

Interest rates and credit availability

- Fed peak 5.25–5.50% (2023–24)

- Auto APR ~9–10% in 2024

- Lear FY2024 interest expense pressured capex timing

- Rate easing 2024–25 helped demand recovery

Tariffs 25%, IRA $369B, DRC 70%

OEM build tracks GDP — US light‑vehicle sales ~15.3M (2024) and global production ~78M driving order volatility; rising electronics content (~3% CAGR) offsets unit swings. 2024 commodity moves (copper +12%, aluminum +8%, steel +10%, resins +15%, select rare earths ~+25%) pressured margins. Mid‑2025 FX EUR/USD 1.09, CNY/USD 7.25, MXN/USD 17.5; Fed peak 5.25–5.50% (2023–24), auto APR ~9–10% (2024).

| Metric | Value |

|---|---|

| US sales 2024 | 15.3M |

| Global production 2024 | ~78M |

| Copper YoY 2024 | +12% |

| EUR/USD mid‑2025 | 1.09 |

| Fed peak | 5.25–5.50% |

Preview the Actual Deliverable

Lear PESTLE Analysis

The preview shown here is the exact Lear PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use. The content, layout, and structure visible are identical to the file you’ll download. No placeholders or teasers—this is the final product.

Skip the Research. Get the Strategy.

Discover how political shifts, market cycles, and tech disruption are reshaping Lear’s strategy in our expert PESTLE Analysis. This concise briefing highlights risks and opportunities—buy the full report to access detailed, ready-to-use insights and actionable recommendations.

Political factors

Trade policy volatility

Shifts in US–China tariff regimes, including Section 301 duties of up to 25% on roughly $300 billion of Chinese goods, can quickly raise costs for wiring, electronics and seat components and force rerouting of supply chains. Lear must hedge import-duty exposure through tariff engineering, sourcing agreements and duty drawback strategies. Diversifying regional production across North America, Europe and Asia mitigates tariff shocks, while proactive trade compliance preserves delivery reliability to global OEMs.

Industrial policy and EV incentives

Government subsidies and local-content rules—driven by the US Inflation Reduction Act (IRA) which mobilized about $369 billion and includes a clean vehicle tax credit up to $7,500 with domestic content bonuses—are reshaping E-Systems demand and plant footprints. Battery and electronics tax credits in key markets favor regionalized manufacturing, prompting Lear to align investments to policy-rich geographies. Rapid policy reversals, however, risk stranded capacity and capital write-offs.

Geopolitical tensions and sanctions

Conflicts and sanction regimes (eg Russia/Ukraine, tightened US export controls 2022–24) have repeatedly disrupted suppliers and logistics lanes, raising lead times for auto parts and electronics. Critical minerals — DRC supplies ~70% of mined cobalt and China processes >80% of refined battery materials — and semiconductors face export controls. Lear needs multi-source strategies for high-risk inputs. Scenario planning supports uninterrupted OEM supply.

Labor and industrial relations

Minimum wage trajectories and union talks affect Lear's cost and flexibility: US federal wage remains $7.25/hr while California reached $16/hr in 2024; UAW 2023 contracts yielded roughly 20% wage gains, raising supplier wage pressure. Cross-border minima (e.g., Germany €12/hr) complicate capacity planning; stable relations support quality and delivery; localization eases political scrutiny.

- Minimums: US $7.25, CA $16 (2024); UAW +~20% (2023)

- Cross-border variance: Germany €12/hr

- Impact: stability reduces disruptions; localization lowers political risk

Public procurement and standards influence

States shape OEM safety, sustainability and connectivity norms; public procurement drives requirements for over-the-air updates, cybersecurity and ISO/SAE interfaces, with EVs reaching about 14% of global new-car sales in 2023 (IEA). Large public fleets and procurement programs—supported by US Infrastructure Law EV charger funding of 7.5 billion USD—can force OEMs into advanced E-System architectures. Engagement with standards bodies (ISO, SAE, CEN) sets technical specs while advocacy steers regulatory roadmaps.

- Policy impact: public procurement mandates

- Fleet catalyst: forces EV e-system design

- Standards: ISO/SAE/CEN shape specs

- Advocacy: aligns product roadmaps with regs

Tariffs 25%, IRA $369B, DRC 70%

Trade tariffs (eg Section 301 up to 25% on ~$300B goods) and IRA incentives ($369B; EV credit up to $7,500) force Lear to regionalize sourcing and align investments. Sanctions, export controls and concentrated mineral processing (DRC ~70% cobalt; China >80% refined materials) require multi-source risk plans. Labor costs and union settlements (UAW +~20% 2023; US $7.25; CA $16 2024; DE €12) affect location and margin decisions.

| Risk | Key data |

|---|---|

| Tariffs | Section 301 25% on ~$300B |

| Incentives | IRA $369B; EV credit $7,500 |

| Critical minerals | DRC ~70% cobalt; China >80% refining |

| Labor | UAW +20% (2023); US $7.25; CA $16; DE €12 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section supported by current data and industry trends to reveal specific threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategy.

Concise, visually segmented Lear PESTLE summary that distills external risks and opportunities into an easily editable, shareable format—ideal for quick insertion into presentations, team alignment, and strategy sessions.

Economic factors

Auto demand cyclicality

OEM build schedules swing with GDP, employment and consumer confidence—US light‑vehicle sales were about 15.3M units in 2024 and global production ran near 78M, driving order volatility for suppliers. Seating volumes and E‑Systems orders closely mirror production levels, while Lear's flexible cost structure (shiftable production, variable labor) helps weather downturns. Rising content‑per‑vehicle—roughly a 3% annual electronics content CAGR—offsets unit volatility.

Commodity and input price swings

Copper, aluminum, steel, resins and rare earths drive Lear’s BOM — market moves in 2024 showed copper +12% YoY, aluminum +8%, steel +10%, resins +15% and select rare earths up ~25%, materially pressuring margins. Wiring‑grade copper supply tightness has tightened premiums and squeezed margins in 2024–H1 2025. Index‑linked pricing and hedging programs have dampened volatility, while design‑to‑cost and material substitution initiatives further protect profitability.

FX and regional mix

Lear operates with revenues and costs across USD, EUR, CNY and MXN; mid‑2025 FX levels were roughly EUR/USD 1.09, CNY/USD 7.25 and MXN/USD 17.5, creating translation and transaction risk. Currency mismatches have materially compressed supplier margins in past FX swings. Natural hedging via local sourcing and production footprint reduces exposure. Where possible, pricing clauses with OEMs shift part of FX risk back to customers.

Logistics and supply chain resilience

Freight rates, which fell roughly 60–70% from 2021 peaks into 2024, and lead times (now ~30–40 days for many routes) continue to strain just-in-time operations at Lear, raising stockout risk and cost variability. Nearshoring and dual sourcing—reflected in rising Mexico and US parts flows—cut disruption exposure, while many OEMs hold ~8–12 weeks of chips/connectors as buffers. Increased adoption of digital visibility and control towers (≈35% of large manufacturers by 2024) speeds corrective actions and reduces recovery time.

- Freight rates down 60–70% vs 2021

- Lead times ~30–40 days

- Chip/connectors buffers ~8–12 weeks

- Control tower adoption ≈35% (2024)

- Nearshoring/dual sourcing rising

Interest rates and credit availability

- Fed peak 5.25–5.50% (2023–24)

- Auto APR ~9–10% in 2024

- Lear FY2024 interest expense pressured capex timing

- Rate easing 2024–25 helped demand recovery

Tariffs 25%, IRA $369B, DRC 70%

OEM build tracks GDP — US light‑vehicle sales ~15.3M (2024) and global production ~78M driving order volatility; rising electronics content (~3% CAGR) offsets unit swings. 2024 commodity moves (copper +12%, aluminum +8%, steel +10%, resins +15%, select rare earths ~+25%) pressured margins. Mid‑2025 FX EUR/USD 1.09, CNY/USD 7.25, MXN/USD 17.5; Fed peak 5.25–5.50% (2023–24), auto APR ~9–10% (2024).

| Metric | Value |

|---|---|

| US sales 2024 | 15.3M |

| Global production 2024 | ~78M |

| Copper YoY 2024 | +12% |

| EUR/USD mid‑2025 | 1.09 |

| Fed peak | 5.25–5.50% |

Preview the Actual Deliverable

Lear PESTLE Analysis

The preview shown here is the exact Lear PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use. The content, layout, and structure visible are identical to the file you’ll download. No placeholders or teasers—this is the final product.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political shifts, market cycles, and tech disruption are reshaping Lear’s strategy in our expert PESTLE Analysis. This concise briefing highlights risks and opportunities—buy the full report to access detailed, ready-to-use insights and actionable recommendations.

Political factors

Trade policy volatility

Shifts in US–China tariff regimes, including Section 301 duties of up to 25% on roughly $300 billion of Chinese goods, can quickly raise costs for wiring, electronics and seat components and force rerouting of supply chains. Lear must hedge import-duty exposure through tariff engineering, sourcing agreements and duty drawback strategies. Diversifying regional production across North America, Europe and Asia mitigates tariff shocks, while proactive trade compliance preserves delivery reliability to global OEMs.

Industrial policy and EV incentives

Government subsidies and local-content rules—driven by the US Inflation Reduction Act (IRA) which mobilized about $369 billion and includes a clean vehicle tax credit up to $7,500 with domestic content bonuses—are reshaping E-Systems demand and plant footprints. Battery and electronics tax credits in key markets favor regionalized manufacturing, prompting Lear to align investments to policy-rich geographies. Rapid policy reversals, however, risk stranded capacity and capital write-offs.

Geopolitical tensions and sanctions

Conflicts and sanction regimes (eg Russia/Ukraine, tightened US export controls 2022–24) have repeatedly disrupted suppliers and logistics lanes, raising lead times for auto parts and electronics. Critical minerals — DRC supplies ~70% of mined cobalt and China processes >80% of refined battery materials — and semiconductors face export controls. Lear needs multi-source strategies for high-risk inputs. Scenario planning supports uninterrupted OEM supply.

Labor and industrial relations

Minimum wage trajectories and union talks affect Lear's cost and flexibility: US federal wage remains $7.25/hr while California reached $16/hr in 2024; UAW 2023 contracts yielded roughly 20% wage gains, raising supplier wage pressure. Cross-border minima (e.g., Germany €12/hr) complicate capacity planning; stable relations support quality and delivery; localization eases political scrutiny.

- Minimums: US $7.25, CA $16 (2024); UAW +~20% (2023)

- Cross-border variance: Germany €12/hr

- Impact: stability reduces disruptions; localization lowers political risk

Public procurement and standards influence

States shape OEM safety, sustainability and connectivity norms; public procurement drives requirements for over-the-air updates, cybersecurity and ISO/SAE interfaces, with EVs reaching about 14% of global new-car sales in 2023 (IEA). Large public fleets and procurement programs—supported by US Infrastructure Law EV charger funding of 7.5 billion USD—can force OEMs into advanced E-System architectures. Engagement with standards bodies (ISO, SAE, CEN) sets technical specs while advocacy steers regulatory roadmaps.

- Policy impact: public procurement mandates

- Fleet catalyst: forces EV e-system design

- Standards: ISO/SAE/CEN shape specs

- Advocacy: aligns product roadmaps with regs

Tariffs 25%, IRA $369B, DRC 70%

Trade tariffs (eg Section 301 up to 25% on ~$300B goods) and IRA incentives ($369B; EV credit up to $7,500) force Lear to regionalize sourcing and align investments. Sanctions, export controls and concentrated mineral processing (DRC ~70% cobalt; China >80% refined materials) require multi-source risk plans. Labor costs and union settlements (UAW +~20% 2023; US $7.25; CA $16 2024; DE €12) affect location and margin decisions.

| Risk | Key data |

|---|---|

| Tariffs | Section 301 25% on ~$300B |

| Incentives | IRA $369B; EV credit $7,500 |

| Critical minerals | DRC ~70% cobalt; China >80% refining |

| Labor | UAW +20% (2023); US $7.25; CA $16; DE €12 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Lear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with each section supported by current data and industry trends to reveal specific threats and opportunities. Designed for executives and investors, it offers forward-looking insights for scenario planning and strategy.

Concise, visually segmented Lear PESTLE summary that distills external risks and opportunities into an easily editable, shareable format—ideal for quick insertion into presentations, team alignment, and strategy sessions.

Economic factors

Auto demand cyclicality

OEM build schedules swing with GDP, employment and consumer confidence—US light‑vehicle sales were about 15.3M units in 2024 and global production ran near 78M, driving order volatility for suppliers. Seating volumes and E‑Systems orders closely mirror production levels, while Lear's flexible cost structure (shiftable production, variable labor) helps weather downturns. Rising content‑per‑vehicle—roughly a 3% annual electronics content CAGR—offsets unit volatility.

Commodity and input price swings

Copper, aluminum, steel, resins and rare earths drive Lear’s BOM — market moves in 2024 showed copper +12% YoY, aluminum +8%, steel +10%, resins +15% and select rare earths up ~25%, materially pressuring margins. Wiring‑grade copper supply tightness has tightened premiums and squeezed margins in 2024–H1 2025. Index‑linked pricing and hedging programs have dampened volatility, while design‑to‑cost and material substitution initiatives further protect profitability.

FX and regional mix

Lear operates with revenues and costs across USD, EUR, CNY and MXN; mid‑2025 FX levels were roughly EUR/USD 1.09, CNY/USD 7.25 and MXN/USD 17.5, creating translation and transaction risk. Currency mismatches have materially compressed supplier margins in past FX swings. Natural hedging via local sourcing and production footprint reduces exposure. Where possible, pricing clauses with OEMs shift part of FX risk back to customers.

Logistics and supply chain resilience

Freight rates, which fell roughly 60–70% from 2021 peaks into 2024, and lead times (now ~30–40 days for many routes) continue to strain just-in-time operations at Lear, raising stockout risk and cost variability. Nearshoring and dual sourcing—reflected in rising Mexico and US parts flows—cut disruption exposure, while many OEMs hold ~8–12 weeks of chips/connectors as buffers. Increased adoption of digital visibility and control towers (≈35% of large manufacturers by 2024) speeds corrective actions and reduces recovery time.

- Freight rates down 60–70% vs 2021

- Lead times ~30–40 days

- Chip/connectors buffers ~8–12 weeks

- Control tower adoption ≈35% (2024)

- Nearshoring/dual sourcing rising

Interest rates and credit availability

- Fed peak 5.25–5.50% (2023–24)

- Auto APR ~9–10% in 2024

- Lear FY2024 interest expense pressured capex timing

- Rate easing 2024–25 helped demand recovery

Tariffs 25%, IRA $369B, DRC 70%

OEM build tracks GDP — US light‑vehicle sales ~15.3M (2024) and global production ~78M driving order volatility; rising electronics content (~3% CAGR) offsets unit swings. 2024 commodity moves (copper +12%, aluminum +8%, steel +10%, resins +15%, select rare earths ~+25%) pressured margins. Mid‑2025 FX EUR/USD 1.09, CNY/USD 7.25, MXN/USD 17.5; Fed peak 5.25–5.50% (2023–24), auto APR ~9–10% (2024).

| Metric | Value |

|---|---|

| US sales 2024 | 15.3M |

| Global production 2024 | ~78M |

| Copper YoY 2024 | +12% |

| EUR/USD mid‑2025 | 1.09 |

| Fed peak | 5.25–5.50% |

Preview the Actual Deliverable

Lear PESTLE Analysis

The preview shown here is the exact Lear PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use. The content, layout, and structure visible are identical to the file you’ll download. No placeholders or teasers—this is the final product.