LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

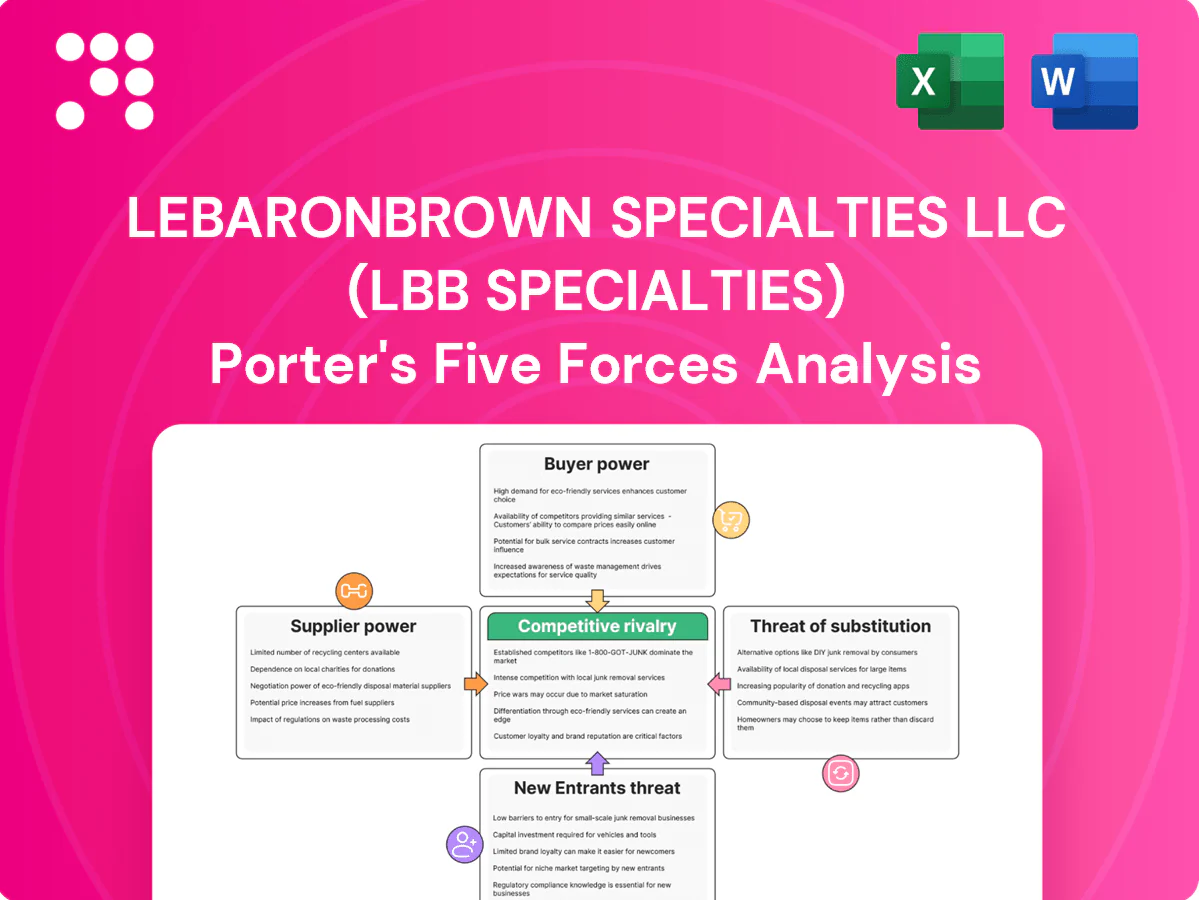

LeBaronBrown Specialties LLC (LBB Specialties) faces moderate supplier power, rising buyer expectations, and niche rivalry that compresses margins while new entrants and substitutes pose targeted threats to select product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LeBaronBrown Specialties LLC (LBB Specialties)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty principals

LBB Specialties sources from a limited set of high-spec chemical and ingredient producers, many global and increasingly concentrated, allowing suppliers leverage over pricing, allocation and exclusivity. Their brand equity and end-customer qualification status further strengthen negotiating power. This concentration raises LBB’s dependency risk in key verticals and supply shocks can materially affect margins in 2024.

Exclusive territory agreements

Distribution for LBB Specialties relies on exclusive, territory-based contracts that protect volume but concentrate dependence on specific principals and renewal terms. In 2024 suppliers have leveraged exclusivity to renegotiate margins or reassign territories, increasing supplier bargaining power. LBB must sustain technical demand creation and measurable sales support to retain exclusivity and mitigate margin compression.

Capacity and allocation constraints

Specialty chemicals face batch production limits and tight capacity planning, with industry capacity utilization exceeding 85% in 2024, tightening lead times. During shortages suppliers prioritize strategic accounts, strengthening their bargaining power and causing allocations that can compress distributor margins by double-digit percentages. LBB Specialties must pursue diversified sourcing and safety-stock programs to mitigate allocation risk and margin erosion.

Regulatory and compliance burden

Suppliers control SDS, REACH, food-grade and cosmetic certifications, making compliance documentation the primary gatekeeper for market access; in 2024 REACH amendments tightened reporting timelines, increasing supplier influence. Any delay or change in certification can immediately disrupt LBB Specialties sales pipelines. LBB mitigates risk through robust QA/QC and centralized documentation management.

- 2024: REACH amendments tightened reporting

- Gatekeeper: SDS/food/cosmetic certs

- Risk: delays = disrupted sales

- Mitigation: strong QA/QC + doc management

Switching and requalification costs

Changing principals triggers customer requalification, reformulation, and validation costs, creating friction that gives incumbents leverage over distributors; suppliers can thus preserve pricing terms or push higher minimums. LBB mitigates this by building multi-principal portfolios and operating application labs that shorten validation cycles and reduce perceived switching pain.

- Incumbent leverage via requalification

- LBB mitigation: multi-principal sourcing

- LBB mitigation: in-house application labs

Supplier-driven allocations and >85% capacity squeeze distributor margins

LBB Specialties faces strong supplier bargaining power from concentrated, high-spec chemical producers and exclusive distribution principals, raising dependency and requalification friction. 2024 trends—REACH reporting tightening, industry capacity utilization >85% and supplier-driven allocations—have driven double-digit distributor margin compression. LBB mitigates via multi-principal sourcing, in-house labs and QA/document centralization.

| Metric | 2024 Status |

|---|---|

| Capacity utilization | >85% |

| Regulatory change | REACH reporting tightened |

| Allocation impact | Double-digit margin compression |

What is included in the product

Tailored Porter's Five Forces analysis for LeBaronBrown Specialties LLC (LBB Specialties) that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for LBB Specialties that instantly highlights competitive pressure points with an editable spider chart—easy to customize, copy into pitch decks, and integrate into broader dashboards to relieve strategic decision-making pain.

Customers Bargaining Power

Diverse but knowledgeable buyers

Customers span three sectors—personal care, food & nutrition and industrial—and often employ skilled formulators whose technical knowledge enables price benchmarking and alternative sourcing. With the global specialty chemicals market near $1.2 trillion in 2024, this raises negotiation leverage on commoditizing SKUs. LBB Specialties’ application support shifts buyer focus from price to performance, protecting margin on differentiated products.

Volume concentration in key accounts

Large CPGs and contract manufacturers concentrate purchasing power, exemplified by major retailers like Walmart capturing roughly 24% of US grocery sales in 2023–24, enabling competitive bids and extended payment terms that compress distributor margins.

LBB Specialties faces this volume concentration pressure but offsets margin squeeze through bundled solutions, exclusive SKUs and strict service SLAs backed by measured fill rates and on-time metrics.

Qualification lock-in moderates power

Once a formulation is validated, buyers face 3–12 months of requalification and tens–hundreds of thousands USD in switching costs, reducing immediate price sensitivity for qualified materials. This qualification lock-in gives LBB Specialties room to maintain margins on critical SKUs without immediate competitive erosion. Robust technical service and on-site support further deepen stickiness by lowering requalification risk and increasing customer reliance on LBB expertise.

Multisourcing and e-procurement

- Multisourcing: increases buyer leverage

- Digital RFQs: wider supplier set, faster price discovery

- Near-commodity: strongest buyer power, margin squeeze

- LBB response: differentiation + self-service + technical support

Service and speed expectations

Buyers now view short lead times, smaller MOQs, and documentation-on-demand as baseline expectations, shifting bargaining power toward distributors that can solve complexity and mitigate supply risk.

Superior logistics and inventory positioning reduce buyer leverage by ensuring continuity, while LBB Specialties’ value-added services—kitting, quality inspections, and technical support—justify premium pricing and customer stickiness.

- Short lead times

- Smaller MOQs

- Documentation-on-demand

- Logistics/inventory = lower buyer power

- LBB value-added services = premium pricing

Specialty chemicals $1.2T (2024): 60% e-procurement, qualification lock-in preserves margins

Customers across personal care, food & nutrition and industrial use in-house formulators and benchmarking, pressuring price on commoditized SKUs; global specialty chemicals ≈ $1.2T (2024). Large buyers concentrate spend (Walmart ≈ 24% US grocery share 2023–24), increasing leverage; qualification lock-in (3–12 months, >$100k) preserves margin on validated SKUs. Rising e-RFQs and multisourcing (≈60% e-procurement adoption 2024) raise price transparency; LBB counters with differentiation, SLAs and logistics.

| Metric | Value |

|---|---|

| Global market (2024) | $1.2T |

| Walmart US grocery share (2023–24) | 24% |

| E-procurement adoption (2024) | ≈60% |

| Near-commodity margins | 3–5% |

| Qualification lead time/cost | 3–12 months; >$100k |

Preview Before You Purchase

LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for LeBaronBrown Specialties LLC you'll receive immediately after purchase—no placeholders or mockups. It provides a professional, fully formatted assessment of competitive rivalry, buyer and supplier power, and threats of substitutes and new entrants, with clear strategic implications. Once purchased, you’ll get instant access to this identical file, ready to download and use.

Go Beyond the Preview—Access the Full Strategic Report

LeBaronBrown Specialties LLC (LBB Specialties) faces moderate supplier power, rising buyer expectations, and niche rivalry that compresses margins while new entrants and substitutes pose targeted threats to select product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LeBaronBrown Specialties LLC (LBB Specialties)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty principals

LBB Specialties sources from a limited set of high-spec chemical and ingredient producers, many global and increasingly concentrated, allowing suppliers leverage over pricing, allocation and exclusivity. Their brand equity and end-customer qualification status further strengthen negotiating power. This concentration raises LBB’s dependency risk in key verticals and supply shocks can materially affect margins in 2024.

Exclusive territory agreements

Distribution for LBB Specialties relies on exclusive, territory-based contracts that protect volume but concentrate dependence on specific principals and renewal terms. In 2024 suppliers have leveraged exclusivity to renegotiate margins or reassign territories, increasing supplier bargaining power. LBB must sustain technical demand creation and measurable sales support to retain exclusivity and mitigate margin compression.

Capacity and allocation constraints

Specialty chemicals face batch production limits and tight capacity planning, with industry capacity utilization exceeding 85% in 2024, tightening lead times. During shortages suppliers prioritize strategic accounts, strengthening their bargaining power and causing allocations that can compress distributor margins by double-digit percentages. LBB Specialties must pursue diversified sourcing and safety-stock programs to mitigate allocation risk and margin erosion.

Regulatory and compliance burden

Suppliers control SDS, REACH, food-grade and cosmetic certifications, making compliance documentation the primary gatekeeper for market access; in 2024 REACH amendments tightened reporting timelines, increasing supplier influence. Any delay or change in certification can immediately disrupt LBB Specialties sales pipelines. LBB mitigates risk through robust QA/QC and centralized documentation management.

- 2024: REACH amendments tightened reporting

- Gatekeeper: SDS/food/cosmetic certs

- Risk: delays = disrupted sales

- Mitigation: strong QA/QC + doc management

Switching and requalification costs

Changing principals triggers customer requalification, reformulation, and validation costs, creating friction that gives incumbents leverage over distributors; suppliers can thus preserve pricing terms or push higher minimums. LBB mitigates this by building multi-principal portfolios and operating application labs that shorten validation cycles and reduce perceived switching pain.

- Incumbent leverage via requalification

- LBB mitigation: multi-principal sourcing

- LBB mitigation: in-house application labs

Supplier-driven allocations and >85% capacity squeeze distributor margins

LBB Specialties faces strong supplier bargaining power from concentrated, high-spec chemical producers and exclusive distribution principals, raising dependency and requalification friction. 2024 trends—REACH reporting tightening, industry capacity utilization >85% and supplier-driven allocations—have driven double-digit distributor margin compression. LBB mitigates via multi-principal sourcing, in-house labs and QA/document centralization.

| Metric | 2024 Status |

|---|---|

| Capacity utilization | >85% |

| Regulatory change | REACH reporting tightened |

| Allocation impact | Double-digit margin compression |

What is included in the product

Tailored Porter's Five Forces analysis for LeBaronBrown Specialties LLC (LBB Specialties) that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for LBB Specialties that instantly highlights competitive pressure points with an editable spider chart—easy to customize, copy into pitch decks, and integrate into broader dashboards to relieve strategic decision-making pain.

Customers Bargaining Power

Diverse but knowledgeable buyers

Customers span three sectors—personal care, food & nutrition and industrial—and often employ skilled formulators whose technical knowledge enables price benchmarking and alternative sourcing. With the global specialty chemicals market near $1.2 trillion in 2024, this raises negotiation leverage on commoditizing SKUs. LBB Specialties’ application support shifts buyer focus from price to performance, protecting margin on differentiated products.

Volume concentration in key accounts

Large CPGs and contract manufacturers concentrate purchasing power, exemplified by major retailers like Walmart capturing roughly 24% of US grocery sales in 2023–24, enabling competitive bids and extended payment terms that compress distributor margins.

LBB Specialties faces this volume concentration pressure but offsets margin squeeze through bundled solutions, exclusive SKUs and strict service SLAs backed by measured fill rates and on-time metrics.

Qualification lock-in moderates power

Once a formulation is validated, buyers face 3–12 months of requalification and tens–hundreds of thousands USD in switching costs, reducing immediate price sensitivity for qualified materials. This qualification lock-in gives LBB Specialties room to maintain margins on critical SKUs without immediate competitive erosion. Robust technical service and on-site support further deepen stickiness by lowering requalification risk and increasing customer reliance on LBB expertise.

Multisourcing and e-procurement

- Multisourcing: increases buyer leverage

- Digital RFQs: wider supplier set, faster price discovery

- Near-commodity: strongest buyer power, margin squeeze

- LBB response: differentiation + self-service + technical support

Service and speed expectations

Buyers now view short lead times, smaller MOQs, and documentation-on-demand as baseline expectations, shifting bargaining power toward distributors that can solve complexity and mitigate supply risk.

Superior logistics and inventory positioning reduce buyer leverage by ensuring continuity, while LBB Specialties’ value-added services—kitting, quality inspections, and technical support—justify premium pricing and customer stickiness.

- Short lead times

- Smaller MOQs

- Documentation-on-demand

- Logistics/inventory = lower buyer power

- LBB value-added services = premium pricing

Specialty chemicals $1.2T (2024): 60% e-procurement, qualification lock-in preserves margins

Customers across personal care, food & nutrition and industrial use in-house formulators and benchmarking, pressuring price on commoditized SKUs; global specialty chemicals ≈ $1.2T (2024). Large buyers concentrate spend (Walmart ≈ 24% US grocery share 2023–24), increasing leverage; qualification lock-in (3–12 months, >$100k) preserves margin on validated SKUs. Rising e-RFQs and multisourcing (≈60% e-procurement adoption 2024) raise price transparency; LBB counters with differentiation, SLAs and logistics.

| Metric | Value |

|---|---|

| Global market (2024) | $1.2T |

| Walmart US grocery share (2023–24) | 24% |

| E-procurement adoption (2024) | ≈60% |

| Near-commodity margins | 3–5% |

| Qualification lead time/cost | 3–12 months; >$100k |

Preview Before You Purchase

LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for LeBaronBrown Specialties LLC you'll receive immediately after purchase—no placeholders or mockups. It provides a professional, fully formatted assessment of competitive rivalry, buyer and supplier power, and threats of substitutes and new entrants, with clear strategic implications. Once purchased, you’ll get instant access to this identical file, ready to download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

LeBaronBrown Specialties LLC (LBB Specialties) faces moderate supplier power, rising buyer expectations, and niche rivalry that compresses margins while new entrants and substitutes pose targeted threats to select product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore LeBaronBrown Specialties LLC (LBB Specialties)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialty principals

LBB Specialties sources from a limited set of high-spec chemical and ingredient producers, many global and increasingly concentrated, allowing suppliers leverage over pricing, allocation and exclusivity. Their brand equity and end-customer qualification status further strengthen negotiating power. This concentration raises LBB’s dependency risk in key verticals and supply shocks can materially affect margins in 2024.

Exclusive territory agreements

Distribution for LBB Specialties relies on exclusive, territory-based contracts that protect volume but concentrate dependence on specific principals and renewal terms. In 2024 suppliers have leveraged exclusivity to renegotiate margins or reassign territories, increasing supplier bargaining power. LBB must sustain technical demand creation and measurable sales support to retain exclusivity and mitigate margin compression.

Capacity and allocation constraints

Specialty chemicals face batch production limits and tight capacity planning, with industry capacity utilization exceeding 85% in 2024, tightening lead times. During shortages suppliers prioritize strategic accounts, strengthening their bargaining power and causing allocations that can compress distributor margins by double-digit percentages. LBB Specialties must pursue diversified sourcing and safety-stock programs to mitigate allocation risk and margin erosion.

Regulatory and compliance burden

Suppliers control SDS, REACH, food-grade and cosmetic certifications, making compliance documentation the primary gatekeeper for market access; in 2024 REACH amendments tightened reporting timelines, increasing supplier influence. Any delay or change in certification can immediately disrupt LBB Specialties sales pipelines. LBB mitigates risk through robust QA/QC and centralized documentation management.

- 2024: REACH amendments tightened reporting

- Gatekeeper: SDS/food/cosmetic certs

- Risk: delays = disrupted sales

- Mitigation: strong QA/QC + doc management

Switching and requalification costs

Changing principals triggers customer requalification, reformulation, and validation costs, creating friction that gives incumbents leverage over distributors; suppliers can thus preserve pricing terms or push higher minimums. LBB mitigates this by building multi-principal portfolios and operating application labs that shorten validation cycles and reduce perceived switching pain.

- Incumbent leverage via requalification

- LBB mitigation: multi-principal sourcing

- LBB mitigation: in-house application labs

Supplier-driven allocations and >85% capacity squeeze distributor margins

LBB Specialties faces strong supplier bargaining power from concentrated, high-spec chemical producers and exclusive distribution principals, raising dependency and requalification friction. 2024 trends—REACH reporting tightening, industry capacity utilization >85% and supplier-driven allocations—have driven double-digit distributor margin compression. LBB mitigates via multi-principal sourcing, in-house labs and QA/document centralization.

| Metric | 2024 Status |

|---|---|

| Capacity utilization | >85% |

| Regulatory change | REACH reporting tightened |

| Allocation impact | Double-digit margin compression |

What is included in the product

Tailored Porter's Five Forces analysis for LeBaronBrown Specialties LLC (LBB Specialties) that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for LBB Specialties that instantly highlights competitive pressure points with an editable spider chart—easy to customize, copy into pitch decks, and integrate into broader dashboards to relieve strategic decision-making pain.

Customers Bargaining Power

Diverse but knowledgeable buyers

Customers span three sectors—personal care, food & nutrition and industrial—and often employ skilled formulators whose technical knowledge enables price benchmarking and alternative sourcing. With the global specialty chemicals market near $1.2 trillion in 2024, this raises negotiation leverage on commoditizing SKUs. LBB Specialties’ application support shifts buyer focus from price to performance, protecting margin on differentiated products.

Volume concentration in key accounts

Large CPGs and contract manufacturers concentrate purchasing power, exemplified by major retailers like Walmart capturing roughly 24% of US grocery sales in 2023–24, enabling competitive bids and extended payment terms that compress distributor margins.

LBB Specialties faces this volume concentration pressure but offsets margin squeeze through bundled solutions, exclusive SKUs and strict service SLAs backed by measured fill rates and on-time metrics.

Qualification lock-in moderates power

Once a formulation is validated, buyers face 3–12 months of requalification and tens–hundreds of thousands USD in switching costs, reducing immediate price sensitivity for qualified materials. This qualification lock-in gives LBB Specialties room to maintain margins on critical SKUs without immediate competitive erosion. Robust technical service and on-site support further deepen stickiness by lowering requalification risk and increasing customer reliance on LBB expertise.

Multisourcing and e-procurement

- Multisourcing: increases buyer leverage

- Digital RFQs: wider supplier set, faster price discovery

- Near-commodity: strongest buyer power, margin squeeze

- LBB response: differentiation + self-service + technical support

Service and speed expectations

Buyers now view short lead times, smaller MOQs, and documentation-on-demand as baseline expectations, shifting bargaining power toward distributors that can solve complexity and mitigate supply risk.

Superior logistics and inventory positioning reduce buyer leverage by ensuring continuity, while LBB Specialties’ value-added services—kitting, quality inspections, and technical support—justify premium pricing and customer stickiness.

- Short lead times

- Smaller MOQs

- Documentation-on-demand

- Logistics/inventory = lower buyer power

- LBB value-added services = premium pricing

Specialty chemicals $1.2T (2024): 60% e-procurement, qualification lock-in preserves margins

Customers across personal care, food & nutrition and industrial use in-house formulators and benchmarking, pressuring price on commoditized SKUs; global specialty chemicals ≈ $1.2T (2024). Large buyers concentrate spend (Walmart ≈ 24% US grocery share 2023–24), increasing leverage; qualification lock-in (3–12 months, >$100k) preserves margin on validated SKUs. Rising e-RFQs and multisourcing (≈60% e-procurement adoption 2024) raise price transparency; LBB counters with differentiation, SLAs and logistics.

| Metric | Value |

|---|---|

| Global market (2024) | $1.2T |

| Walmart US grocery share (2023–24) | 24% |

| E-procurement adoption (2024) | ≈60% |

| Near-commodity margins | 3–5% |

| Qualification lead time/cost | 3–12 months; >$100k |

Preview Before You Purchase

LeBaronBrown Specialties LLC (LBB Specialties) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for LeBaronBrown Specialties LLC you'll receive immediately after purchase—no placeholders or mockups. It provides a professional, fully formatted assessment of competitive rivalry, buyer and supplier power, and threats of substitutes and new entrants, with clear strategic implications. Once purchased, you’ll get instant access to this identical file, ready to download and use.