Lecta SA Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

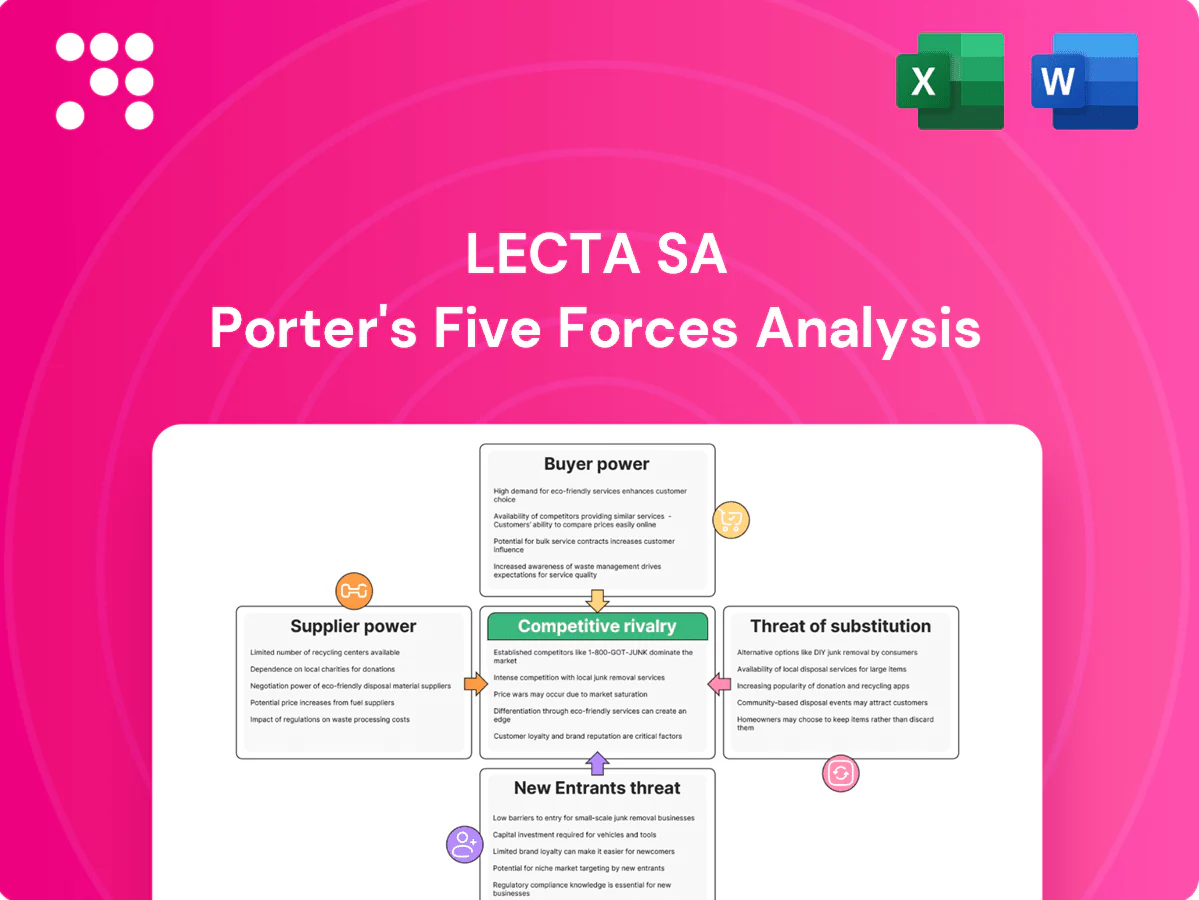

Lecta SA faces nuanced competitive pressures from raw material suppliers, shifting buyer demands, and rising substitute materials, while regulatory and capital barriers shape entry threats; our snapshot highlights key strategic levers and vulnerabilities. This brief teaser only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Lecta SA.

Suppliers Bargaining Power

Fiber sourcing concentration

Lecta depends on wood pulp, chemicals and energy supplied by a concentrated set of global pulp producers such as Suzano, Sappi, UPM, Stora Enso and International Paper, which increases supplier bargaining power. Limited sources of FSC/PEFC-certified sustainable fiber further tighten availability and can push input costs higher. Long-term contracts and multi-sourcing mitigate supply shocks but constrain operational flexibility. Certification requirements narrow the viable supplier pool and raise switching costs.

Energy and utilities volatility

Paper mills are highly energy‑intensive, exposing Lecta to European gas and power price swings. Geopolitical disruptions drove TTF gas up to about €345/MWh in Aug 2022, squeezing margins. Hedging and efficiency upgrades mitigate but cannot fully offset volatility. EU ETS prices near €90–100/tCO2 in 2024 add compliance costs and potential supply constraints.

Specialty chemicals dependence

Coatings, adhesives and specialty chemicals for paper are concentrated suppliers, with the global specialty chemicals market estimated at >$700 billion in 2024, giving vendors pricing and delivery leverage; supply disruptions can halt production or degrade quality at converters like Lecta, while vendor qualification cycles often extend beyond six months, and strategic partnerships secure innovation but create switching costs and lock-in.

Logistics and packaging inputs

Transport, pallets and packaging films create additional supplier exposure for Lecta SA; container spot rates fell roughly 70% from 2021 peaks to 2024 but volatility persists, keeping freight cost risk elevated. Port congestion and an estimated 400,000 EU truck-driver shortfall in 2024 can delay shipments and raise spot freight. Regional distribution mitigates but cross-border bottlenecks and just-in-time models increase disruption vulnerability.

- Transport volatility: spot rates down ~70% vs 2021

- Trucking shortage: ~400,000 drivers EU (2024)

- Pallets/films: limited supplier concentration

- JIT risk: higher sensitivity to delays

Currency and import exposure

Pulp and key chemicals for Lecta are commonly priced in USD while sales are invoiced in EUR, exposing margins to FX swings; the FOEX pulp index averaged about 900 USD/tonne in 2024 and EUR/USD averaged ~1.09, amplifying supplier pricing power during depreciation of EUR. Financial hedges cut volatility but incur premiums and margin cost. Localizing inputs where feasible reduces this supplier leverage.

- USD pricing vs EUR sales: FX mismatch

- FOEX pulp ~900 USD/t (2024)

- EUR/USD ~1.09 (2024 avg)

- Hedging reduces volatility but adds cost

- Local sourcing lowers supplier power

Concentrated suppliers, high CO2 costs (~90–100 €/t) and FOEX ~900 USD/t compress margins

Lecta faces high supplier power from concentrated pulp, chemicals and energy vendors, amplified by limited certified fiber and specialty-chemical concentration. Energy and CO2 costs (EU ETS ~90–100 €/tCO2 in 2024) and FX mismatch (FOEX ~900 USD/t; EUR/USD ~1.09 in 2024) squeeze margins despite hedging. Transport volatility (spot rates -~70% vs 2021) and ~400,000 EU truck-driver shortfall add disruption risk.

| Metric | 2024 value |

|---|---|

| FOEX pulp | ~900 USD/t |

| EUR/USD | ~1.09 |

| EU ETS | ~90–100 €/tCO2 |

| Truck-driver gap EU | ~400,000 |

| Container spot rates vs 2021 | ~-70% |

What is included in the product

Analyzes competitive drivers, buyer and supplier power, threat of substitutes and new entrants for Lecta SA, highlighting industry-specific pressures, disruptive threats, pricing influence on margins, and barriers that protect incumbents while providing strategic insights for investors and management.

A concise, one-sheet Porter's Five Forces for Lecta SA that highlights competitive pressures and relieves decision fatigue by visualizing supplier/buyer power, entry threats, substitutes, and rivalry—ready to drop into decks or model scenarios without macros.

Customers Bargaining Power

Consolidated converters and printers

Large label converters, packaging firms and publishing printers buy at scale and negotiate aggressively, with industry reports showing the top five customers often concentrating roughly 30–50% of purchase volumes for speciality paper suppliers. Volume concentration compresses pricing and service terms and framework agreements frequently lock multi-year discounts (commonly 2–5 years). Losing a top account can cut plant utilization materially, often by double-digit percentage points.

High product comparability

For many coated and uncoated grades specifications are largely interchangeable, enabling buyers to run quick tenders and multi-sourcing to pressure margins; certification parity is high, with FSC and PEFC covering over 500 million hectares globally by 2024, which further lowers switching costs; true differentiation for Lecta must therefore come from superior service, shorter lead times, and specialty features or coatings.

Demand cyclicality

In 2024 publishing end-markets remain structurally declining while packaging demand shows pronounced cyclicality, increasing Lecta buyers' price sensitivity. During downturns customers press for concessions and extend payment terms, squeezing working capital. Inventory destocking compresses order volumes and shifts bargaining power to buyers. Recoveries partially restore volumes but do not fully reverse concession trends.

Technical qualification switching costs

Specialty label and flexible-packaging papers require press trials and approvals, creating moderate technical-qualification switching costs that temper buyer power; however large converters retain backup specs to maintain leverage and performance failures typically trigger rapid re-sourcing. Global flexible packaging market ≈USD 213 billion in 2024, keeping buyer negotiation power significant.

- Press trials and approvals raise switching friction

- Backup specs by large converters preserve leverage

- Performance failures prompt quick re-sourcing

Sustainability and compliance demands

Buyers increasingly demand traceability, low-carbon footprints and recyclability, and since CSRD phased in from 2024 more procurement teams require verified disclosures; meeting these specs raises input costs and narrows material choices. Non-compliance can cost tenders despite lower prices, while verified ESG credentials win premium accounts and dampen price sensitivity.

- CSRD 2024: stronger disclosure expectations

- Higher compliance costs, constrained suppliers

- Verified ESG → premium, lower price pressure

Top buyers (30–50%) and USD 213B market amplify buyer leverage and utilization risk

Large buyers concentrate 30–50% of volumes, driving multi-year discounts and double-digit utilization risk if lost. Specification parity and FSC/PEFC coverage ~500M ha in 2024 lower switching costs, while press trials create moderate friction. CSRD from 2024 raises disclosure demands; flexible packaging market ≈USD 213B in 2024, keeping buyer leverage high.

| Metric | 2024 |

|---|---|

| Top-5 buyer share | 30–50% |

| FSC/PEFC area | ~500M ha |

| Flexible packaging market | USD 213B |

Preview the Actual Deliverable

Lecta SA Porter's Five Forces Analysis

This preview shows the exact Lecta SA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted analysis, ready to download and use the moment you complete payment. What you see is what you get.

A Must-Have Tool for Decision-Makers

Lecta SA faces nuanced competitive pressures from raw material suppliers, shifting buyer demands, and rising substitute materials, while regulatory and capital barriers shape entry threats; our snapshot highlights key strategic levers and vulnerabilities. This brief teaser only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Lecta SA.

Suppliers Bargaining Power

Fiber sourcing concentration

Lecta depends on wood pulp, chemicals and energy supplied by a concentrated set of global pulp producers such as Suzano, Sappi, UPM, Stora Enso and International Paper, which increases supplier bargaining power. Limited sources of FSC/PEFC-certified sustainable fiber further tighten availability and can push input costs higher. Long-term contracts and multi-sourcing mitigate supply shocks but constrain operational flexibility. Certification requirements narrow the viable supplier pool and raise switching costs.

Energy and utilities volatility

Paper mills are highly energy‑intensive, exposing Lecta to European gas and power price swings. Geopolitical disruptions drove TTF gas up to about €345/MWh in Aug 2022, squeezing margins. Hedging and efficiency upgrades mitigate but cannot fully offset volatility. EU ETS prices near €90–100/tCO2 in 2024 add compliance costs and potential supply constraints.

Specialty chemicals dependence

Coatings, adhesives and specialty chemicals for paper are concentrated suppliers, with the global specialty chemicals market estimated at >$700 billion in 2024, giving vendors pricing and delivery leverage; supply disruptions can halt production or degrade quality at converters like Lecta, while vendor qualification cycles often extend beyond six months, and strategic partnerships secure innovation but create switching costs and lock-in.

Logistics and packaging inputs

Transport, pallets and packaging films create additional supplier exposure for Lecta SA; container spot rates fell roughly 70% from 2021 peaks to 2024 but volatility persists, keeping freight cost risk elevated. Port congestion and an estimated 400,000 EU truck-driver shortfall in 2024 can delay shipments and raise spot freight. Regional distribution mitigates but cross-border bottlenecks and just-in-time models increase disruption vulnerability.

- Transport volatility: spot rates down ~70% vs 2021

- Trucking shortage: ~400,000 drivers EU (2024)

- Pallets/films: limited supplier concentration

- JIT risk: higher sensitivity to delays

Currency and import exposure

Pulp and key chemicals for Lecta are commonly priced in USD while sales are invoiced in EUR, exposing margins to FX swings; the FOEX pulp index averaged about 900 USD/tonne in 2024 and EUR/USD averaged ~1.09, amplifying supplier pricing power during depreciation of EUR. Financial hedges cut volatility but incur premiums and margin cost. Localizing inputs where feasible reduces this supplier leverage.

- USD pricing vs EUR sales: FX mismatch

- FOEX pulp ~900 USD/t (2024)

- EUR/USD ~1.09 (2024 avg)

- Hedging reduces volatility but adds cost

- Local sourcing lowers supplier power

Concentrated suppliers, high CO2 costs (~90–100 €/t) and FOEX ~900 USD/t compress margins

Lecta faces high supplier power from concentrated pulp, chemicals and energy vendors, amplified by limited certified fiber and specialty-chemical concentration. Energy and CO2 costs (EU ETS ~90–100 €/tCO2 in 2024) and FX mismatch (FOEX ~900 USD/t; EUR/USD ~1.09 in 2024) squeeze margins despite hedging. Transport volatility (spot rates -~70% vs 2021) and ~400,000 EU truck-driver shortfall add disruption risk.

| Metric | 2024 value |

|---|---|

| FOEX pulp | ~900 USD/t |

| EUR/USD | ~1.09 |

| EU ETS | ~90–100 €/tCO2 |

| Truck-driver gap EU | ~400,000 |

| Container spot rates vs 2021 | ~-70% |

What is included in the product

Analyzes competitive drivers, buyer and supplier power, threat of substitutes and new entrants for Lecta SA, highlighting industry-specific pressures, disruptive threats, pricing influence on margins, and barriers that protect incumbents while providing strategic insights for investors and management.

A concise, one-sheet Porter's Five Forces for Lecta SA that highlights competitive pressures and relieves decision fatigue by visualizing supplier/buyer power, entry threats, substitutes, and rivalry—ready to drop into decks or model scenarios without macros.

Customers Bargaining Power

Consolidated converters and printers

Large label converters, packaging firms and publishing printers buy at scale and negotiate aggressively, with industry reports showing the top five customers often concentrating roughly 30–50% of purchase volumes for speciality paper suppliers. Volume concentration compresses pricing and service terms and framework agreements frequently lock multi-year discounts (commonly 2–5 years). Losing a top account can cut plant utilization materially, often by double-digit percentage points.

High product comparability

For many coated and uncoated grades specifications are largely interchangeable, enabling buyers to run quick tenders and multi-sourcing to pressure margins; certification parity is high, with FSC and PEFC covering over 500 million hectares globally by 2024, which further lowers switching costs; true differentiation for Lecta must therefore come from superior service, shorter lead times, and specialty features or coatings.

Demand cyclicality

In 2024 publishing end-markets remain structurally declining while packaging demand shows pronounced cyclicality, increasing Lecta buyers' price sensitivity. During downturns customers press for concessions and extend payment terms, squeezing working capital. Inventory destocking compresses order volumes and shifts bargaining power to buyers. Recoveries partially restore volumes but do not fully reverse concession trends.

Technical qualification switching costs

Specialty label and flexible-packaging papers require press trials and approvals, creating moderate technical-qualification switching costs that temper buyer power; however large converters retain backup specs to maintain leverage and performance failures typically trigger rapid re-sourcing. Global flexible packaging market ≈USD 213 billion in 2024, keeping buyer negotiation power significant.

- Press trials and approvals raise switching friction

- Backup specs by large converters preserve leverage

- Performance failures prompt quick re-sourcing

Sustainability and compliance demands

Buyers increasingly demand traceability, low-carbon footprints and recyclability, and since CSRD phased in from 2024 more procurement teams require verified disclosures; meeting these specs raises input costs and narrows material choices. Non-compliance can cost tenders despite lower prices, while verified ESG credentials win premium accounts and dampen price sensitivity.

- CSRD 2024: stronger disclosure expectations

- Higher compliance costs, constrained suppliers

- Verified ESG → premium, lower price pressure

Top buyers (30–50%) and USD 213B market amplify buyer leverage and utilization risk

Large buyers concentrate 30–50% of volumes, driving multi-year discounts and double-digit utilization risk if lost. Specification parity and FSC/PEFC coverage ~500M ha in 2024 lower switching costs, while press trials create moderate friction. CSRD from 2024 raises disclosure demands; flexible packaging market ≈USD 213B in 2024, keeping buyer leverage high.

| Metric | 2024 |

|---|---|

| Top-5 buyer share | 30–50% |

| FSC/PEFC area | ~500M ha |

| Flexible packaging market | USD 213B |

Preview the Actual Deliverable

Lecta SA Porter's Five Forces Analysis

This preview shows the exact Lecta SA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted analysis, ready to download and use the moment you complete payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lecta SA faces nuanced competitive pressures from raw material suppliers, shifting buyer demands, and rising substitute materials, while regulatory and capital barriers shape entry threats; our snapshot highlights key strategic levers and vulnerabilities. This brief teaser only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Lecta SA.

Suppliers Bargaining Power

Fiber sourcing concentration

Lecta depends on wood pulp, chemicals and energy supplied by a concentrated set of global pulp producers such as Suzano, Sappi, UPM, Stora Enso and International Paper, which increases supplier bargaining power. Limited sources of FSC/PEFC-certified sustainable fiber further tighten availability and can push input costs higher. Long-term contracts and multi-sourcing mitigate supply shocks but constrain operational flexibility. Certification requirements narrow the viable supplier pool and raise switching costs.

Energy and utilities volatility

Paper mills are highly energy‑intensive, exposing Lecta to European gas and power price swings. Geopolitical disruptions drove TTF gas up to about €345/MWh in Aug 2022, squeezing margins. Hedging and efficiency upgrades mitigate but cannot fully offset volatility. EU ETS prices near €90–100/tCO2 in 2024 add compliance costs and potential supply constraints.

Specialty chemicals dependence

Coatings, adhesives and specialty chemicals for paper are concentrated suppliers, with the global specialty chemicals market estimated at >$700 billion in 2024, giving vendors pricing and delivery leverage; supply disruptions can halt production or degrade quality at converters like Lecta, while vendor qualification cycles often extend beyond six months, and strategic partnerships secure innovation but create switching costs and lock-in.

Logistics and packaging inputs

Transport, pallets and packaging films create additional supplier exposure for Lecta SA; container spot rates fell roughly 70% from 2021 peaks to 2024 but volatility persists, keeping freight cost risk elevated. Port congestion and an estimated 400,000 EU truck-driver shortfall in 2024 can delay shipments and raise spot freight. Regional distribution mitigates but cross-border bottlenecks and just-in-time models increase disruption vulnerability.

- Transport volatility: spot rates down ~70% vs 2021

- Trucking shortage: ~400,000 drivers EU (2024)

- Pallets/films: limited supplier concentration

- JIT risk: higher sensitivity to delays

Currency and import exposure

Pulp and key chemicals for Lecta are commonly priced in USD while sales are invoiced in EUR, exposing margins to FX swings; the FOEX pulp index averaged about 900 USD/tonne in 2024 and EUR/USD averaged ~1.09, amplifying supplier pricing power during depreciation of EUR. Financial hedges cut volatility but incur premiums and margin cost. Localizing inputs where feasible reduces this supplier leverage.

- USD pricing vs EUR sales: FX mismatch

- FOEX pulp ~900 USD/t (2024)

- EUR/USD ~1.09 (2024 avg)

- Hedging reduces volatility but adds cost

- Local sourcing lowers supplier power

Concentrated suppliers, high CO2 costs (~90–100 €/t) and FOEX ~900 USD/t compress margins

Lecta faces high supplier power from concentrated pulp, chemicals and energy vendors, amplified by limited certified fiber and specialty-chemical concentration. Energy and CO2 costs (EU ETS ~90–100 €/tCO2 in 2024) and FX mismatch (FOEX ~900 USD/t; EUR/USD ~1.09 in 2024) squeeze margins despite hedging. Transport volatility (spot rates -~70% vs 2021) and ~400,000 EU truck-driver shortfall add disruption risk.

| Metric | 2024 value |

|---|---|

| FOEX pulp | ~900 USD/t |

| EUR/USD | ~1.09 |

| EU ETS | ~90–100 €/tCO2 |

| Truck-driver gap EU | ~400,000 |

| Container spot rates vs 2021 | ~-70% |

What is included in the product

Analyzes competitive drivers, buyer and supplier power, threat of substitutes and new entrants for Lecta SA, highlighting industry-specific pressures, disruptive threats, pricing influence on margins, and barriers that protect incumbents while providing strategic insights for investors and management.

A concise, one-sheet Porter's Five Forces for Lecta SA that highlights competitive pressures and relieves decision fatigue by visualizing supplier/buyer power, entry threats, substitutes, and rivalry—ready to drop into decks or model scenarios without macros.

Customers Bargaining Power

Consolidated converters and printers

Large label converters, packaging firms and publishing printers buy at scale and negotiate aggressively, with industry reports showing the top five customers often concentrating roughly 30–50% of purchase volumes for speciality paper suppliers. Volume concentration compresses pricing and service terms and framework agreements frequently lock multi-year discounts (commonly 2–5 years). Losing a top account can cut plant utilization materially, often by double-digit percentage points.

High product comparability

For many coated and uncoated grades specifications are largely interchangeable, enabling buyers to run quick tenders and multi-sourcing to pressure margins; certification parity is high, with FSC and PEFC covering over 500 million hectares globally by 2024, which further lowers switching costs; true differentiation for Lecta must therefore come from superior service, shorter lead times, and specialty features or coatings.

Demand cyclicality

In 2024 publishing end-markets remain structurally declining while packaging demand shows pronounced cyclicality, increasing Lecta buyers' price sensitivity. During downturns customers press for concessions and extend payment terms, squeezing working capital. Inventory destocking compresses order volumes and shifts bargaining power to buyers. Recoveries partially restore volumes but do not fully reverse concession trends.

Technical qualification switching costs

Specialty label and flexible-packaging papers require press trials and approvals, creating moderate technical-qualification switching costs that temper buyer power; however large converters retain backup specs to maintain leverage and performance failures typically trigger rapid re-sourcing. Global flexible packaging market ≈USD 213 billion in 2024, keeping buyer negotiation power significant.

- Press trials and approvals raise switching friction

- Backup specs by large converters preserve leverage

- Performance failures prompt quick re-sourcing

Sustainability and compliance demands

Buyers increasingly demand traceability, low-carbon footprints and recyclability, and since CSRD phased in from 2024 more procurement teams require verified disclosures; meeting these specs raises input costs and narrows material choices. Non-compliance can cost tenders despite lower prices, while verified ESG credentials win premium accounts and dampen price sensitivity.

- CSRD 2024: stronger disclosure expectations

- Higher compliance costs, constrained suppliers

- Verified ESG → premium, lower price pressure

Top buyers (30–50%) and USD 213B market amplify buyer leverage and utilization risk

Large buyers concentrate 30–50% of volumes, driving multi-year discounts and double-digit utilization risk if lost. Specification parity and FSC/PEFC coverage ~500M ha in 2024 lower switching costs, while press trials create moderate friction. CSRD from 2024 raises disclosure demands; flexible packaging market ≈USD 213B in 2024, keeping buyer leverage high.

| Metric | 2024 |

|---|---|

| Top-5 buyer share | 30–50% |

| FSC/PEFC area | ~500M ha |

| Flexible packaging market | USD 213B |

Preview the Actual Deliverable

Lecta SA Porter's Five Forces Analysis

This preview shows the exact Lecta SA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or sample excerpts. The file is the full, professionally formatted analysis, ready to download and use the moment you complete payment. What you see is what you get.