Lee Enterprises Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

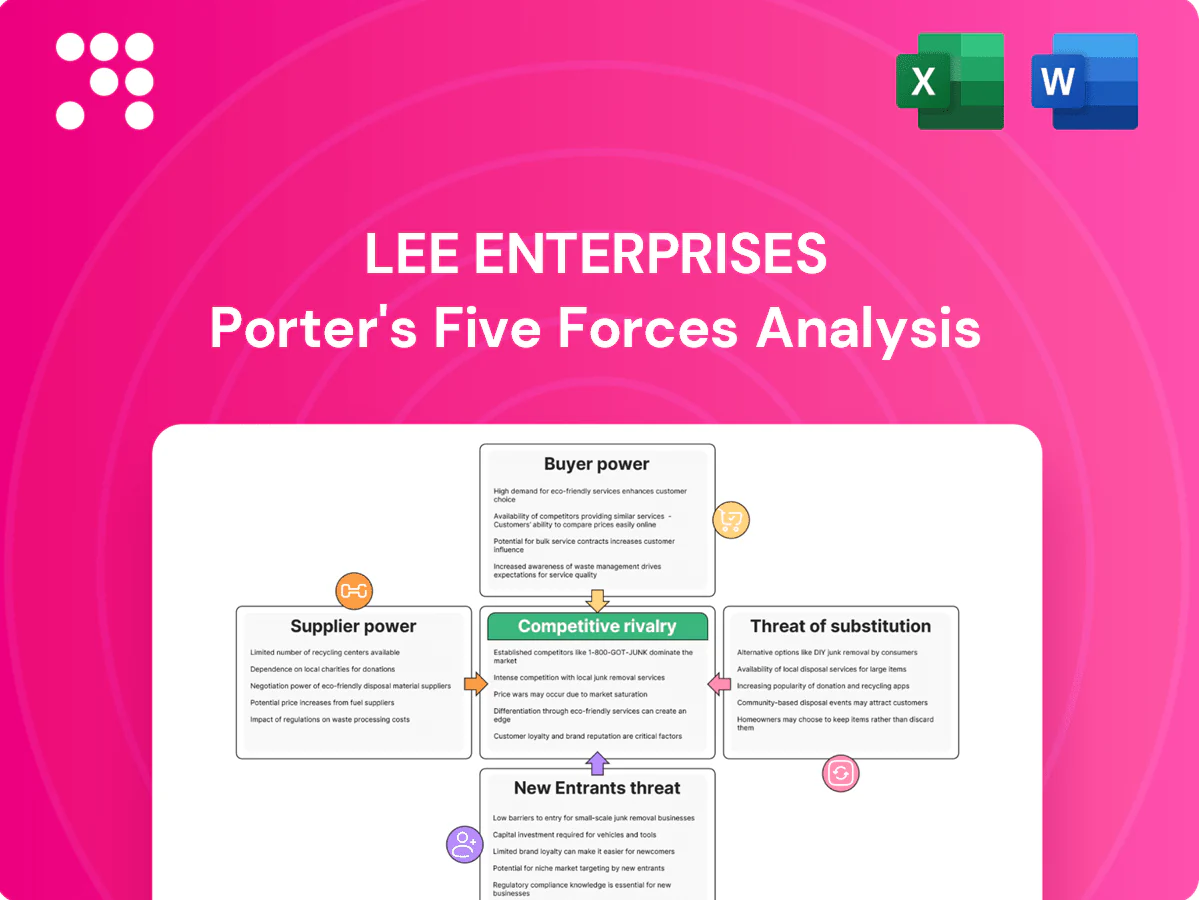

Lee Enterprises faces high buyer and advertiser pressure, a moderate threat from digital substitutes, and scale-driven barriers to entry amid industry consolidation. This snapshot flags strategic risks and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Consolidated newsprint and ink vendors

Consolidation among newsprint and ink vendors has increased suppliers’ pricing leverage over declining but essential inputs, and volatile pulp and logistics costs frequently pass through to publishers, squeezing margins. Lee mitigates risk with multi‑year supply contracts and inventory management to smooth spikes, yet falling print volumes weaken its negotiating clout. Ongoing digital mix shift reduces print dependency over time, dampening supplier power.

Printing, distribution, and USPS dependencies

Third‑party printers, delivery contractors and USPS exert strong leverage over Lee Enterprises’ last‑mile distribution, with shrinking route density increasing per‑unit print and delivery costs and limiting alternative providers. Contract renegotiations or USPS service disruptions can delay distribution and raise fulfillment expenses. Consolidating print sites lowers unit costs but concentrates operational risk and lengthens backup recovery times.

Content wires and syndicated providers

AP, syndicated columns, sports rights and real-time data feeds are specialized inputs with few equivalents; AP alone serves 1,300+ news outlets, and Lee operates 77 daily newspapers, so these feeds materially expand breadth and timeliness. Price hikes or tighter licensing can create content gaps or raise costs, forcing layoffs or paid substitutes. Lee offsets risk with proprietary local reporting but continues to rely on diverse wire partners for scale and sports coverage.

Adtech, martech, and platform ecosystems

Dependence on ad servers, SSPs, analytics, paywall/CMS vendors and app stores creates material switching costs for Lee; Google and Meta together accounted for about 61% of US digital ad spend in 2024, while app store commissions range 15–30% and programmatic stacks can levy 10–25% in fees, so fee or policy shifts and privacy rules compress yields and raise supplier power; vendor consolidation and walled gardens amplify this, while building first‑party data and in‑house stack reduces exposure over time.

- High platform share: Google+Meta ≈61% US ad spend (2024)

- App store commissions: 15–30%

- Programmatic/adtech fees: ~10–25%

- Mitigation: first‑party data + in‑house ad/CMS lowers supplier risk

Freelancers and specialized local talent

Skilled reporters, photographers and niche contributors are scarce across several of Lee Enterprises’ 77 daily markets in 2024, raising supplier leverage as quality local journalism is hard to substitute without audience loss. Tight labor pools and increased newsroom union activity have elevated compensation demands, pressuring margins. Long‑term relationships and talent pipelines partially moderate turnover and cost volatility.

- Scarcity: 77 daily newspapers (2024)

- Substitutability: high audience sensitivity to local talent

- Cost pressure: union-driven wage increases

- Mitigant: established talent pipelines and long relationships

Supplier leverage rises as print decline and platform fees (61%, 15–30%) squeeze margins

Concentrated inputs (newsprint, ink, pulp) and logistics volatility raise supplier leverage, while falling print volumes weaken Lee’s negotiating clout. Digital ad platforms (Google+Meta ≈61% US ad spend, 2024) and app stores (15–30% fees) create persistent fee risk. Specialized content feeds (AP ~1,300 outlets) and scarce local talent across 77 dailies (2024) further constrain margins.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Ad platforms | Google+Meta ≈61% | Fee/policy risk |

| Print inputs | Volatile pulp/logistics | Cost pass-through |

| Content/talent | AP ~1,300; 77 dailies | Coverage/cost pressure |

What is included in the product

Tailored Porter's Five Forces for Lee Enterprises, assessing competitive rivalry, buyer/supplier power, threat of entrants and substitutes, and disruptive digital shifts—actionable insights to inform strategy and investor materials.

A concise, one-sheet Porter's Five Forces for Lee Enterprises that instantly visualizes competitive pressure with a customizable spider chart—no macros, easy to edit, and ready to drop into pitch decks or board reports to speed strategic decisions.

Customers Bargaining Power

Local advertisers with ample alternatives

SMBs can reallocate budgets across search, social, CTV and retail media, driving price sensitivity—about 73% of SMBs used social ads in 2023. Self‑serve tools from Google and Meta—which together account for roughly 60% of US digital ad spend—reduce dependence on local publishers. Easy multi‑homing across channels raises bargaining power and churn risk. Packaging measurable, ROI‑driven marketing services helps defend share.

Digital readers face low switching costs

As of 2024 digital readers face low switching costs—local updates are available via apps, social groups, and TV sites at minimal expense. Paywalls add friction but introductory offers and competitor promotions commonly undercut retention. Strong brand trust and exclusive local reporting limit defection, while personalization and targeted newsletters deepen engagement and reduce buyer power.

Programmatic buyers demand performance

Programmatic now represents about 85% of US display ad spend in 2024, and agency/DSP buyers routinely optimize to CPM/CPC/CPA benchmarks, commoditizing open‑auction inventory. Viewability (≈55% average), brand safety and first‑party data quality create price deltas, with consented audiences commanding roughly 1.5–2x premiums. Privacy shifts reducing third‑party targeting have moved leverage to sellers with permissioned data, while direct deals and sponsorships reduce auction dependence.

Print subscribers are price sensitive

Print cohorts skew older and show high sensitivity to frequency and delivery changes; industry trends show U.S. weekday print circulation down roughly 10% into 2024, meaning price hikes can spark accelerated cancellations in an already shrinking base. Habit persistence among older readers gives Lee Enterprises short‑term pricing room, but long‑run retention depends on managing tiered offers and controlled migration to digital to preserve lifetime value.

- Age skew: older subscribers

- Price sensitivity: cancellation risk on hikes

- Trend: ~10% print decline into 2024

- Strategy: tiered offers + digital migration to protect LTV

Regional and national buyers negotiate scale

Regional and national buyers press for multi‑market packages and volume discounts, enabling them to benchmark Lee’s CPMs across publishers and compress margins.

Cross‑platform bundles and unified performance reporting strengthen Lee’s negotiating stance by tying digital, print and events into measurable outcomes.

Partnerships and JOA‑style collaborations help unlock inventory scale and offer buyers broader reach without sole reliance on Lee’s standalone footprint.

- Larger advertisers: multi‑market deals

- Benchmarking: tighter CPMs

- Cross‑platform reporting: improved leverage

- JOA/partnerships: inventory scale

High buyer leverage: 73% SMBs on social, programmatic ~85%; defend with bundles & 1st-party data

Buyers have high leverage: 73% of SMBs used social ads in 2023 and programmatic is ~85% of US display spend in 2024, enabling easy multi‑homing and price sensitivity. Print decline ~10% into 2024 raises churn risk on price hikes while older cohorts give short‑term pricing room. Bundles, first‑party data and cross‑platform ROI reporting are key defenses.

| Metric | Value |

|---|---|

| SMB social ad use (2023) | 73% |

| Programmatic share (2024) | ~85% |

| Print decline (to 2024) | ~10% |

| Consented audience CPM premium | 1.5–2x |

Preview the Actual Deliverable

Lee Enterprises Porter's Five Forces Analysis

This preview shows the exact Lee Enterprises Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy. You're viewing the actual deliverable and will get instant access to this identical document upon payment.

A Must-Have Tool for Decision-Makers

Lee Enterprises faces high buyer and advertiser pressure, a moderate threat from digital substitutes, and scale-driven barriers to entry amid industry consolidation. This snapshot flags strategic risks and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Consolidated newsprint and ink vendors

Consolidation among newsprint and ink vendors has increased suppliers’ pricing leverage over declining but essential inputs, and volatile pulp and logistics costs frequently pass through to publishers, squeezing margins. Lee mitigates risk with multi‑year supply contracts and inventory management to smooth spikes, yet falling print volumes weaken its negotiating clout. Ongoing digital mix shift reduces print dependency over time, dampening supplier power.

Printing, distribution, and USPS dependencies

Third‑party printers, delivery contractors and USPS exert strong leverage over Lee Enterprises’ last‑mile distribution, with shrinking route density increasing per‑unit print and delivery costs and limiting alternative providers. Contract renegotiations or USPS service disruptions can delay distribution and raise fulfillment expenses. Consolidating print sites lowers unit costs but concentrates operational risk and lengthens backup recovery times.

Content wires and syndicated providers

AP, syndicated columns, sports rights and real-time data feeds are specialized inputs with few equivalents; AP alone serves 1,300+ news outlets, and Lee operates 77 daily newspapers, so these feeds materially expand breadth and timeliness. Price hikes or tighter licensing can create content gaps or raise costs, forcing layoffs or paid substitutes. Lee offsets risk with proprietary local reporting but continues to rely on diverse wire partners for scale and sports coverage.

Adtech, martech, and platform ecosystems

Dependence on ad servers, SSPs, analytics, paywall/CMS vendors and app stores creates material switching costs for Lee; Google and Meta together accounted for about 61% of US digital ad spend in 2024, while app store commissions range 15–30% and programmatic stacks can levy 10–25% in fees, so fee or policy shifts and privacy rules compress yields and raise supplier power; vendor consolidation and walled gardens amplify this, while building first‑party data and in‑house stack reduces exposure over time.

- High platform share: Google+Meta ≈61% US ad spend (2024)

- App store commissions: 15–30%

- Programmatic/adtech fees: ~10–25%

- Mitigation: first‑party data + in‑house ad/CMS lowers supplier risk

Freelancers and specialized local talent

Skilled reporters, photographers and niche contributors are scarce across several of Lee Enterprises’ 77 daily markets in 2024, raising supplier leverage as quality local journalism is hard to substitute without audience loss. Tight labor pools and increased newsroom union activity have elevated compensation demands, pressuring margins. Long‑term relationships and talent pipelines partially moderate turnover and cost volatility.

- Scarcity: 77 daily newspapers (2024)

- Substitutability: high audience sensitivity to local talent

- Cost pressure: union-driven wage increases

- Mitigant: established talent pipelines and long relationships

Supplier leverage rises as print decline and platform fees (61%, 15–30%) squeeze margins

Concentrated inputs (newsprint, ink, pulp) and logistics volatility raise supplier leverage, while falling print volumes weaken Lee’s negotiating clout. Digital ad platforms (Google+Meta ≈61% US ad spend, 2024) and app stores (15–30% fees) create persistent fee risk. Specialized content feeds (AP ~1,300 outlets) and scarce local talent across 77 dailies (2024) further constrain margins.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Ad platforms | Google+Meta ≈61% | Fee/policy risk |

| Print inputs | Volatile pulp/logistics | Cost pass-through |

| Content/talent | AP ~1,300; 77 dailies | Coverage/cost pressure |

What is included in the product

Tailored Porter's Five Forces for Lee Enterprises, assessing competitive rivalry, buyer/supplier power, threat of entrants and substitutes, and disruptive digital shifts—actionable insights to inform strategy and investor materials.

A concise, one-sheet Porter's Five Forces for Lee Enterprises that instantly visualizes competitive pressure with a customizable spider chart—no macros, easy to edit, and ready to drop into pitch decks or board reports to speed strategic decisions.

Customers Bargaining Power

Local advertisers with ample alternatives

SMBs can reallocate budgets across search, social, CTV and retail media, driving price sensitivity—about 73% of SMBs used social ads in 2023. Self‑serve tools from Google and Meta—which together account for roughly 60% of US digital ad spend—reduce dependence on local publishers. Easy multi‑homing across channels raises bargaining power and churn risk. Packaging measurable, ROI‑driven marketing services helps defend share.

Digital readers face low switching costs

As of 2024 digital readers face low switching costs—local updates are available via apps, social groups, and TV sites at minimal expense. Paywalls add friction but introductory offers and competitor promotions commonly undercut retention. Strong brand trust and exclusive local reporting limit defection, while personalization and targeted newsletters deepen engagement and reduce buyer power.

Programmatic buyers demand performance

Programmatic now represents about 85% of US display ad spend in 2024, and agency/DSP buyers routinely optimize to CPM/CPC/CPA benchmarks, commoditizing open‑auction inventory. Viewability (≈55% average), brand safety and first‑party data quality create price deltas, with consented audiences commanding roughly 1.5–2x premiums. Privacy shifts reducing third‑party targeting have moved leverage to sellers with permissioned data, while direct deals and sponsorships reduce auction dependence.

Print subscribers are price sensitive

Print cohorts skew older and show high sensitivity to frequency and delivery changes; industry trends show U.S. weekday print circulation down roughly 10% into 2024, meaning price hikes can spark accelerated cancellations in an already shrinking base. Habit persistence among older readers gives Lee Enterprises short‑term pricing room, but long‑run retention depends on managing tiered offers and controlled migration to digital to preserve lifetime value.

- Age skew: older subscribers

- Price sensitivity: cancellation risk on hikes

- Trend: ~10% print decline into 2024

- Strategy: tiered offers + digital migration to protect LTV

Regional and national buyers negotiate scale

Regional and national buyers press for multi‑market packages and volume discounts, enabling them to benchmark Lee’s CPMs across publishers and compress margins.

Cross‑platform bundles and unified performance reporting strengthen Lee’s negotiating stance by tying digital, print and events into measurable outcomes.

Partnerships and JOA‑style collaborations help unlock inventory scale and offer buyers broader reach without sole reliance on Lee’s standalone footprint.

- Larger advertisers: multi‑market deals

- Benchmarking: tighter CPMs

- Cross‑platform reporting: improved leverage

- JOA/partnerships: inventory scale

High buyer leverage: 73% SMBs on social, programmatic ~85%; defend with bundles & 1st-party data

Buyers have high leverage: 73% of SMBs used social ads in 2023 and programmatic is ~85% of US display spend in 2024, enabling easy multi‑homing and price sensitivity. Print decline ~10% into 2024 raises churn risk on price hikes while older cohorts give short‑term pricing room. Bundles, first‑party data and cross‑platform ROI reporting are key defenses.

| Metric | Value |

|---|---|

| SMB social ad use (2023) | 73% |

| Programmatic share (2024) | ~85% |

| Print decline (to 2024) | ~10% |

| Consented audience CPM premium | 1.5–2x |

Preview the Actual Deliverable

Lee Enterprises Porter's Five Forces Analysis

This preview shows the exact Lee Enterprises Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy. You're viewing the actual deliverable and will get instant access to this identical document upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lee Enterprises faces high buyer and advertiser pressure, a moderate threat from digital substitutes, and scale-driven barriers to entry amid industry consolidation. This snapshot flags strategic risks and strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Consolidated newsprint and ink vendors

Consolidation among newsprint and ink vendors has increased suppliers’ pricing leverage over declining but essential inputs, and volatile pulp and logistics costs frequently pass through to publishers, squeezing margins. Lee mitigates risk with multi‑year supply contracts and inventory management to smooth spikes, yet falling print volumes weaken its negotiating clout. Ongoing digital mix shift reduces print dependency over time, dampening supplier power.

Printing, distribution, and USPS dependencies

Third‑party printers, delivery contractors and USPS exert strong leverage over Lee Enterprises’ last‑mile distribution, with shrinking route density increasing per‑unit print and delivery costs and limiting alternative providers. Contract renegotiations or USPS service disruptions can delay distribution and raise fulfillment expenses. Consolidating print sites lowers unit costs but concentrates operational risk and lengthens backup recovery times.

Content wires and syndicated providers

AP, syndicated columns, sports rights and real-time data feeds are specialized inputs with few equivalents; AP alone serves 1,300+ news outlets, and Lee operates 77 daily newspapers, so these feeds materially expand breadth and timeliness. Price hikes or tighter licensing can create content gaps or raise costs, forcing layoffs or paid substitutes. Lee offsets risk with proprietary local reporting but continues to rely on diverse wire partners for scale and sports coverage.

Adtech, martech, and platform ecosystems

Dependence on ad servers, SSPs, analytics, paywall/CMS vendors and app stores creates material switching costs for Lee; Google and Meta together accounted for about 61% of US digital ad spend in 2024, while app store commissions range 15–30% and programmatic stacks can levy 10–25% in fees, so fee or policy shifts and privacy rules compress yields and raise supplier power; vendor consolidation and walled gardens amplify this, while building first‑party data and in‑house stack reduces exposure over time.

- High platform share: Google+Meta ≈61% US ad spend (2024)

- App store commissions: 15–30%

- Programmatic/adtech fees: ~10–25%

- Mitigation: first‑party data + in‑house ad/CMS lowers supplier risk

Freelancers and specialized local talent

Skilled reporters, photographers and niche contributors are scarce across several of Lee Enterprises’ 77 daily markets in 2024, raising supplier leverage as quality local journalism is hard to substitute without audience loss. Tight labor pools and increased newsroom union activity have elevated compensation demands, pressuring margins. Long‑term relationships and talent pipelines partially moderate turnover and cost volatility.

- Scarcity: 77 daily newspapers (2024)

- Substitutability: high audience sensitivity to local talent

- Cost pressure: union-driven wage increases

- Mitigant: established talent pipelines and long relationships

Supplier leverage rises as print decline and platform fees (61%, 15–30%) squeeze margins

Concentrated inputs (newsprint, ink, pulp) and logistics volatility raise supplier leverage, while falling print volumes weaken Lee’s negotiating clout. Digital ad platforms (Google+Meta ≈61% US ad spend, 2024) and app stores (15–30% fees) create persistent fee risk. Specialized content feeds (AP ~1,300 outlets) and scarce local talent across 77 dailies (2024) further constrain margins.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Ad platforms | Google+Meta ≈61% | Fee/policy risk |

| Print inputs | Volatile pulp/logistics | Cost pass-through |

| Content/talent | AP ~1,300; 77 dailies | Coverage/cost pressure |

What is included in the product

Tailored Porter's Five Forces for Lee Enterprises, assessing competitive rivalry, buyer/supplier power, threat of entrants and substitutes, and disruptive digital shifts—actionable insights to inform strategy and investor materials.

A concise, one-sheet Porter's Five Forces for Lee Enterprises that instantly visualizes competitive pressure with a customizable spider chart—no macros, easy to edit, and ready to drop into pitch decks or board reports to speed strategic decisions.

Customers Bargaining Power

Local advertisers with ample alternatives

SMBs can reallocate budgets across search, social, CTV and retail media, driving price sensitivity—about 73% of SMBs used social ads in 2023. Self‑serve tools from Google and Meta—which together account for roughly 60% of US digital ad spend—reduce dependence on local publishers. Easy multi‑homing across channels raises bargaining power and churn risk. Packaging measurable, ROI‑driven marketing services helps defend share.

Digital readers face low switching costs

As of 2024 digital readers face low switching costs—local updates are available via apps, social groups, and TV sites at minimal expense. Paywalls add friction but introductory offers and competitor promotions commonly undercut retention. Strong brand trust and exclusive local reporting limit defection, while personalization and targeted newsletters deepen engagement and reduce buyer power.

Programmatic buyers demand performance

Programmatic now represents about 85% of US display ad spend in 2024, and agency/DSP buyers routinely optimize to CPM/CPC/CPA benchmarks, commoditizing open‑auction inventory. Viewability (≈55% average), brand safety and first‑party data quality create price deltas, with consented audiences commanding roughly 1.5–2x premiums. Privacy shifts reducing third‑party targeting have moved leverage to sellers with permissioned data, while direct deals and sponsorships reduce auction dependence.

Print subscribers are price sensitive

Print cohorts skew older and show high sensitivity to frequency and delivery changes; industry trends show U.S. weekday print circulation down roughly 10% into 2024, meaning price hikes can spark accelerated cancellations in an already shrinking base. Habit persistence among older readers gives Lee Enterprises short‑term pricing room, but long‑run retention depends on managing tiered offers and controlled migration to digital to preserve lifetime value.

- Age skew: older subscribers

- Price sensitivity: cancellation risk on hikes

- Trend: ~10% print decline into 2024

- Strategy: tiered offers + digital migration to protect LTV

Regional and national buyers negotiate scale

Regional and national buyers press for multi‑market packages and volume discounts, enabling them to benchmark Lee’s CPMs across publishers and compress margins.

Cross‑platform bundles and unified performance reporting strengthen Lee’s negotiating stance by tying digital, print and events into measurable outcomes.

Partnerships and JOA‑style collaborations help unlock inventory scale and offer buyers broader reach without sole reliance on Lee’s standalone footprint.

- Larger advertisers: multi‑market deals

- Benchmarking: tighter CPMs

- Cross‑platform reporting: improved leverage

- JOA/partnerships: inventory scale

High buyer leverage: 73% SMBs on social, programmatic ~85%; defend with bundles & 1st-party data

Buyers have high leverage: 73% of SMBs used social ads in 2023 and programmatic is ~85% of US display spend in 2024, enabling easy multi‑homing and price sensitivity. Print decline ~10% into 2024 raises churn risk on price hikes while older cohorts give short‑term pricing room. Bundles, first‑party data and cross‑platform ROI reporting are key defenses.

| Metric | Value |

|---|---|

| SMB social ad use (2023) | 73% |

| Programmatic share (2024) | ~85% |

| Print decline (to 2024) | ~10% |

| Consented audience CPM premium | 1.5–2x |

Preview the Actual Deliverable

Lee Enterprises Porter's Five Forces Analysis

This preview shows the exact Lee Enterprises Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted and ready for download and use the moment you buy. You're viewing the actual deliverable and will get instant access to this identical document upon payment.