Leggett & Platt Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

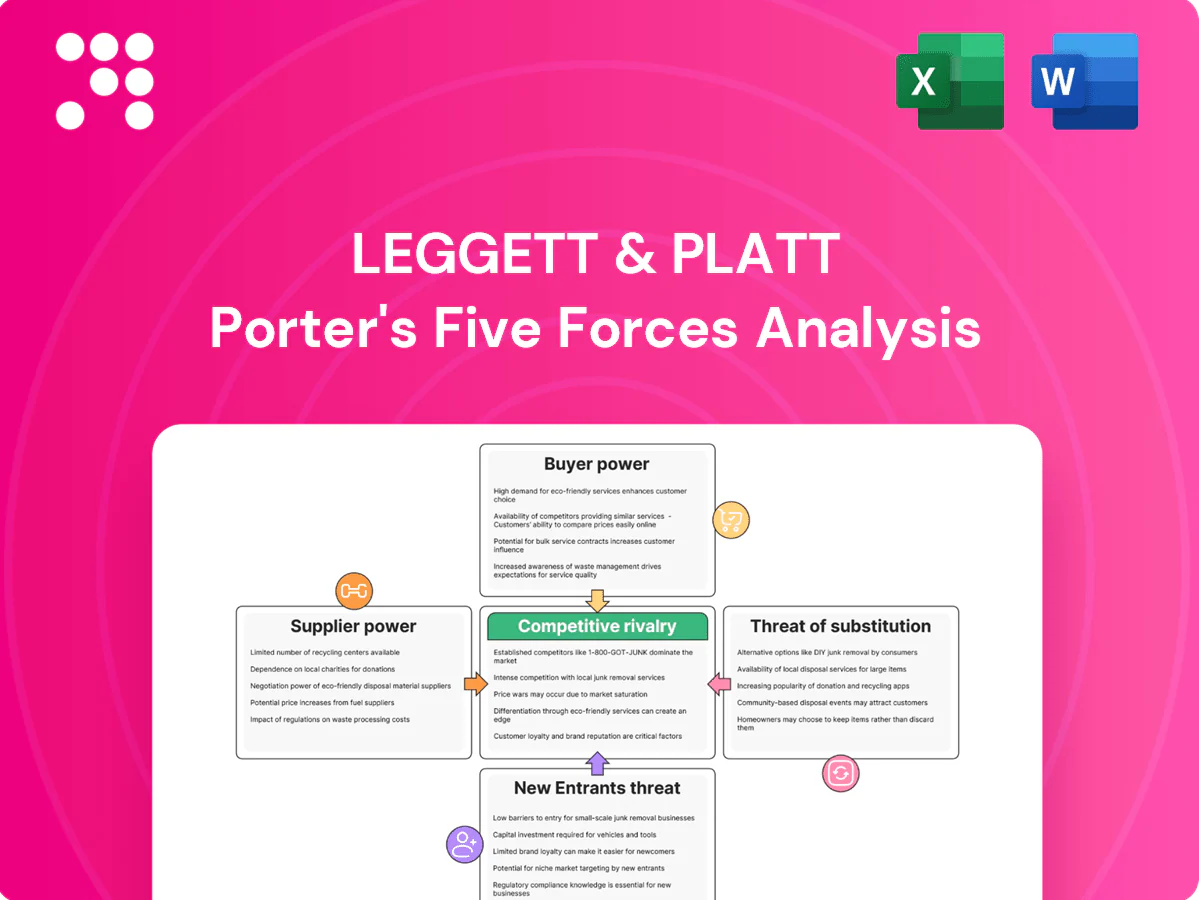

Leggett & Platt faces moderate rivalry driven by diversified product lines and global peers, while supplier power is constrained by commodity inputs and scale advantages; buyer power varies across retail and industrial channels, and barriers to entry are moderate given manufacturing know-how. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Leggett & Platt’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials (steel, chemicals)

Leggett & Platt depends on wire rod, steel strip, polyols/isocyanates, textiles and specialty foams supplied by a handful of global chemical and steel producers, giving suppliers elevated leverage; short-term price passthrough is imperfect, leaving margins exposed to raw-material spikes. L&P limits risk via multi-sourcing and commodity hedging, but supplier concentration sustains moderate bargaining power.

Commodity price volatility and surcharges

Commodity price volatility, with benchmark hot-rolled coil and ethylene/naphtha costs posting double-digit swings in 2023–24, drives supplier surcharges and contract repricing that hit Leggett & Platt’s input base. Timing gaps between input inflation and customer price adjustments compress gross margins. Volatility complicates inventory and working-capital planning and gives suppliers negotiating leverage during tight markets.

Switching costs and qualification

Substituting a steel grade, foam chemistry, or adhesive typically requires requalification and customer approval, adding months of testing and validation that raise effective switching costs for Leggett & Platt.

In automotive applications PPAP submissions and supplier quality audits further entrench incumbents by creating formal barriers to change.

These operational frictions increase suppliers’ bargaining power despite nominal input fungibility.

Global logistics and capacity constraints

Ocean freight bottlenecks and regional outages in 2024 tightened supply, and force majeure events have intermittently reduced available capacity. Suppliers can prioritize larger or higher‑margin buyers, pushing smaller L&P orders back despite the company’s global footprint. Diversified plants mitigate site risk, yet transport constraints and longer lead times still shift bargaining power upstream.

- 2024: capacity volatility favored large buyers

- Global footprint offsets but does not eliminate risk

- Transport and lead-time pressures persist

Countervailing scale and long-term contracts

Leggett & Platt’s large volumes and long-term relationships drive volume rebates and indexed contracts—in 2024 L&P reported about $3.6 billion in net sales, underpinning purchasing leverage versus smaller rivals.

Vendor-managed inventory and co-development agreements have embedded suppliers into L&P’s supply chain, improving terms and continuity, though indexation does not remove short-term raw‑material price spikes.

- Scale: ~3.6B net sales 2024

- Mechanisms: volume rebates, indexed contracts, VMI, co-development

- Effect: lowers supplier power vs smaller peers

- Limit: indexation ≠ protection from short-term price pressure

Supplier leverage persists despite $3.6B, price swings, long qual cycles

Suppliers of steel, polyols and textiles exert moderate bargaining power due to concentration, input-price volatility and lengthy requalification; L&P’s $3.6B 2024 scale, multi-sourcing and indexed contracts reduce but do not eliminate exposure. Ocean freight and capacity tightness in 2024 amplified supplier leverage during spikes. Long OEM qual cycles raise effective switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Net sales | $3.6B | Purchase leverage |

| Input volatility | Double-digit swings 2023–24 | Margin exposure |

| Lead times | Extended vs pre-2023 | Supplier leverage |

What is included in the product

Tailored exclusively for Leggett & Platt, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks while identifying disruptive substitutes and emerging threats to market share; fully editable for investor materials, strategy decks, or business plans.

A one-sheet Porter's Five Forces for Leggett & Platt that visually maps competitive pressure and risk, with adjustable inputs for scenario planning—ideal for quick boardroom decisions and pitch decks.

Customers Bargaining Power

Large OEMs and retailers exert leverage

Large automotive Tier-1s/OEMs and big-box bedding retailers wield high buyer power over Leggett & Platt, leveraging procurement scale to push pricing and demand cost-downs while enforcing strict service levels; in 2024 L&P reported roughly $3.0 billion in net sales, with key OEM/retailer contracts representing an outsized share of orders, and widespread dual-sourcing increasing price sensitivity across core segments.

Specification lock-in moderates switching

Many L&P components are engineered into customer designs with certifications and testing, and requalification plus tooling changes often take 6–18 months and commonly exceed $1M in auto seating programs. This spec-in status makes mid-program switching costly and slow, reducing buyer optionality and materially tempering buyer power once awards are made, especially in automotive seating systems.

Product differentiation and value-add

Comfort systems, advanced mechanisms, and specialty foams deliver measurable performance in durability, noise reduction, and weight savings, shifting buyer focus beyond price. When customers prioritize these attributes, substitutability falls and engineered offerings support premium pricing. That reduced substitutability and pricing power lower buyer bargaining power in Leggett & Platt’s engineered niches.

Demand cyclicality and inventory dynamics

Service, logistics, and customization

Just-in-time delivery, short lead times, and customization increase switching frictions for Leggett & Platt; operational ties to regional plants and kitting embed buyers in its supply chain, meaning abrupt transitions risk disruption. In 2024 L&P reported approximately $3.9 billion in net sales, underscoring scale that supports integrated logistics and reduces pure price vulnerability.

- Regional plants: embedded ops

- Kitting: reduces buyer churn

- JIT/short lead times: raise switching cost

- Operational integration: limits buyer price leverage

OEM price squeeze, but $3.9B scale and tooling >$1M raise switching costs

Large Tier-1 OEMs and big-box retailers exert strong price and terms pressure on Leggett & Platt, though 2024 net sales of $3.9 billion reflect scale that supports integrated logistics; engineering-spec components (requalifications 6–18 months, tooling often >$1M) raise switching costs and blunt buyer power, while 2024 cyclicality increased concessions and extended payment terms.

| Metric | 2024 |

|---|---|

| Net sales | $3.9B |

| Requalification time | 6–18 months |

| Typical tooling cost | >$1M |

Full Version Awaits

Leggett & Platt Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Leggett & Platt and is the exact document you'll receive after purchase. It covers supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants with direct strategic implications. The file is professionally formatted and ready to download. No placeholders or samples—what you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Leggett & Platt faces moderate rivalry driven by diversified product lines and global peers, while supplier power is constrained by commodity inputs and scale advantages; buyer power varies across retail and industrial channels, and barriers to entry are moderate given manufacturing know-how. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Leggett & Platt’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials (steel, chemicals)

Leggett & Platt depends on wire rod, steel strip, polyols/isocyanates, textiles and specialty foams supplied by a handful of global chemical and steel producers, giving suppliers elevated leverage; short-term price passthrough is imperfect, leaving margins exposed to raw-material spikes. L&P limits risk via multi-sourcing and commodity hedging, but supplier concentration sustains moderate bargaining power.

Commodity price volatility and surcharges

Commodity price volatility, with benchmark hot-rolled coil and ethylene/naphtha costs posting double-digit swings in 2023–24, drives supplier surcharges and contract repricing that hit Leggett & Platt’s input base. Timing gaps between input inflation and customer price adjustments compress gross margins. Volatility complicates inventory and working-capital planning and gives suppliers negotiating leverage during tight markets.

Switching costs and qualification

Substituting a steel grade, foam chemistry, or adhesive typically requires requalification and customer approval, adding months of testing and validation that raise effective switching costs for Leggett & Platt.

In automotive applications PPAP submissions and supplier quality audits further entrench incumbents by creating formal barriers to change.

These operational frictions increase suppliers’ bargaining power despite nominal input fungibility.

Global logistics and capacity constraints

Ocean freight bottlenecks and regional outages in 2024 tightened supply, and force majeure events have intermittently reduced available capacity. Suppliers can prioritize larger or higher‑margin buyers, pushing smaller L&P orders back despite the company’s global footprint. Diversified plants mitigate site risk, yet transport constraints and longer lead times still shift bargaining power upstream.

- 2024: capacity volatility favored large buyers

- Global footprint offsets but does not eliminate risk

- Transport and lead-time pressures persist

Countervailing scale and long-term contracts

Leggett & Platt’s large volumes and long-term relationships drive volume rebates and indexed contracts—in 2024 L&P reported about $3.6 billion in net sales, underpinning purchasing leverage versus smaller rivals.

Vendor-managed inventory and co-development agreements have embedded suppliers into L&P’s supply chain, improving terms and continuity, though indexation does not remove short-term raw‑material price spikes.

- Scale: ~3.6B net sales 2024

- Mechanisms: volume rebates, indexed contracts, VMI, co-development

- Effect: lowers supplier power vs smaller peers

- Limit: indexation ≠ protection from short-term price pressure

Supplier leverage persists despite $3.6B, price swings, long qual cycles

Suppliers of steel, polyols and textiles exert moderate bargaining power due to concentration, input-price volatility and lengthy requalification; L&P’s $3.6B 2024 scale, multi-sourcing and indexed contracts reduce but do not eliminate exposure. Ocean freight and capacity tightness in 2024 amplified supplier leverage during spikes. Long OEM qual cycles raise effective switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Net sales | $3.6B | Purchase leverage |

| Input volatility | Double-digit swings 2023–24 | Margin exposure |

| Lead times | Extended vs pre-2023 | Supplier leverage |

What is included in the product

Tailored exclusively for Leggett & Platt, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks while identifying disruptive substitutes and emerging threats to market share; fully editable for investor materials, strategy decks, or business plans.

A one-sheet Porter's Five Forces for Leggett & Platt that visually maps competitive pressure and risk, with adjustable inputs for scenario planning—ideal for quick boardroom decisions and pitch decks.

Customers Bargaining Power

Large OEMs and retailers exert leverage

Large automotive Tier-1s/OEMs and big-box bedding retailers wield high buyer power over Leggett & Platt, leveraging procurement scale to push pricing and demand cost-downs while enforcing strict service levels; in 2024 L&P reported roughly $3.0 billion in net sales, with key OEM/retailer contracts representing an outsized share of orders, and widespread dual-sourcing increasing price sensitivity across core segments.

Specification lock-in moderates switching

Many L&P components are engineered into customer designs with certifications and testing, and requalification plus tooling changes often take 6–18 months and commonly exceed $1M in auto seating programs. This spec-in status makes mid-program switching costly and slow, reducing buyer optionality and materially tempering buyer power once awards are made, especially in automotive seating systems.

Product differentiation and value-add

Comfort systems, advanced mechanisms, and specialty foams deliver measurable performance in durability, noise reduction, and weight savings, shifting buyer focus beyond price. When customers prioritize these attributes, substitutability falls and engineered offerings support premium pricing. That reduced substitutability and pricing power lower buyer bargaining power in Leggett & Platt’s engineered niches.

Demand cyclicality and inventory dynamics

Service, logistics, and customization

Just-in-time delivery, short lead times, and customization increase switching frictions for Leggett & Platt; operational ties to regional plants and kitting embed buyers in its supply chain, meaning abrupt transitions risk disruption. In 2024 L&P reported approximately $3.9 billion in net sales, underscoring scale that supports integrated logistics and reduces pure price vulnerability.

- Regional plants: embedded ops

- Kitting: reduces buyer churn

- JIT/short lead times: raise switching cost

- Operational integration: limits buyer price leverage

OEM price squeeze, but $3.9B scale and tooling >$1M raise switching costs

Large Tier-1 OEMs and big-box retailers exert strong price and terms pressure on Leggett & Platt, though 2024 net sales of $3.9 billion reflect scale that supports integrated logistics; engineering-spec components (requalifications 6–18 months, tooling often >$1M) raise switching costs and blunt buyer power, while 2024 cyclicality increased concessions and extended payment terms.

| Metric | 2024 |

|---|---|

| Net sales | $3.9B |

| Requalification time | 6–18 months |

| Typical tooling cost | >$1M |

Full Version Awaits

Leggett & Platt Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Leggett & Platt and is the exact document you'll receive after purchase. It covers supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants with direct strategic implications. The file is professionally formatted and ready to download. No placeholders or samples—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Leggett & Platt faces moderate rivalry driven by diversified product lines and global peers, while supplier power is constrained by commodity inputs and scale advantages; buyer power varies across retail and industrial channels, and barriers to entry are moderate given manufacturing know-how. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Leggett & Platt’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials (steel, chemicals)

Leggett & Platt depends on wire rod, steel strip, polyols/isocyanates, textiles and specialty foams supplied by a handful of global chemical and steel producers, giving suppliers elevated leverage; short-term price passthrough is imperfect, leaving margins exposed to raw-material spikes. L&P limits risk via multi-sourcing and commodity hedging, but supplier concentration sustains moderate bargaining power.

Commodity price volatility and surcharges

Commodity price volatility, with benchmark hot-rolled coil and ethylene/naphtha costs posting double-digit swings in 2023–24, drives supplier surcharges and contract repricing that hit Leggett & Platt’s input base. Timing gaps between input inflation and customer price adjustments compress gross margins. Volatility complicates inventory and working-capital planning and gives suppliers negotiating leverage during tight markets.

Switching costs and qualification

Substituting a steel grade, foam chemistry, or adhesive typically requires requalification and customer approval, adding months of testing and validation that raise effective switching costs for Leggett & Platt.

In automotive applications PPAP submissions and supplier quality audits further entrench incumbents by creating formal barriers to change.

These operational frictions increase suppliers’ bargaining power despite nominal input fungibility.

Global logistics and capacity constraints

Ocean freight bottlenecks and regional outages in 2024 tightened supply, and force majeure events have intermittently reduced available capacity. Suppliers can prioritize larger or higher‑margin buyers, pushing smaller L&P orders back despite the company’s global footprint. Diversified plants mitigate site risk, yet transport constraints and longer lead times still shift bargaining power upstream.

- 2024: capacity volatility favored large buyers

- Global footprint offsets but does not eliminate risk

- Transport and lead-time pressures persist

Countervailing scale and long-term contracts

Leggett & Platt’s large volumes and long-term relationships drive volume rebates and indexed contracts—in 2024 L&P reported about $3.6 billion in net sales, underpinning purchasing leverage versus smaller rivals.

Vendor-managed inventory and co-development agreements have embedded suppliers into L&P’s supply chain, improving terms and continuity, though indexation does not remove short-term raw‑material price spikes.

- Scale: ~3.6B net sales 2024

- Mechanisms: volume rebates, indexed contracts, VMI, co-development

- Effect: lowers supplier power vs smaller peers

- Limit: indexation ≠ protection from short-term price pressure

Supplier leverage persists despite $3.6B, price swings, long qual cycles

Suppliers of steel, polyols and textiles exert moderate bargaining power due to concentration, input-price volatility and lengthy requalification; L&P’s $3.6B 2024 scale, multi-sourcing and indexed contracts reduce but do not eliminate exposure. Ocean freight and capacity tightness in 2024 amplified supplier leverage during spikes. Long OEM qual cycles raise effective switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Net sales | $3.6B | Purchase leverage |

| Input volatility | Double-digit swings 2023–24 | Margin exposure |

| Lead times | Extended vs pre-2023 | Supplier leverage |

What is included in the product

Tailored exclusively for Leggett & Platt, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market entry risks while identifying disruptive substitutes and emerging threats to market share; fully editable for investor materials, strategy decks, or business plans.

A one-sheet Porter's Five Forces for Leggett & Platt that visually maps competitive pressure and risk, with adjustable inputs for scenario planning—ideal for quick boardroom decisions and pitch decks.

Customers Bargaining Power

Large OEMs and retailers exert leverage

Large automotive Tier-1s/OEMs and big-box bedding retailers wield high buyer power over Leggett & Platt, leveraging procurement scale to push pricing and demand cost-downs while enforcing strict service levels; in 2024 L&P reported roughly $3.0 billion in net sales, with key OEM/retailer contracts representing an outsized share of orders, and widespread dual-sourcing increasing price sensitivity across core segments.

Specification lock-in moderates switching

Many L&P components are engineered into customer designs with certifications and testing, and requalification plus tooling changes often take 6–18 months and commonly exceed $1M in auto seating programs. This spec-in status makes mid-program switching costly and slow, reducing buyer optionality and materially tempering buyer power once awards are made, especially in automotive seating systems.

Product differentiation and value-add

Comfort systems, advanced mechanisms, and specialty foams deliver measurable performance in durability, noise reduction, and weight savings, shifting buyer focus beyond price. When customers prioritize these attributes, substitutability falls and engineered offerings support premium pricing. That reduced substitutability and pricing power lower buyer bargaining power in Leggett & Platt’s engineered niches.

Demand cyclicality and inventory dynamics

Service, logistics, and customization

Just-in-time delivery, short lead times, and customization increase switching frictions for Leggett & Platt; operational ties to regional plants and kitting embed buyers in its supply chain, meaning abrupt transitions risk disruption. In 2024 L&P reported approximately $3.9 billion in net sales, underscoring scale that supports integrated logistics and reduces pure price vulnerability.

- Regional plants: embedded ops

- Kitting: reduces buyer churn

- JIT/short lead times: raise switching cost

- Operational integration: limits buyer price leverage

OEM price squeeze, but $3.9B scale and tooling >$1M raise switching costs

Large Tier-1 OEMs and big-box retailers exert strong price and terms pressure on Leggett & Platt, though 2024 net sales of $3.9 billion reflect scale that supports integrated logistics; engineering-spec components (requalifications 6–18 months, tooling often >$1M) raise switching costs and blunt buyer power, while 2024 cyclicality increased concessions and extended payment terms.

| Metric | 2024 |

|---|---|

| Net sales | $3.9B |

| Requalification time | 6–18 months |

| Typical tooling cost | >$1M |

Full Version Awaits

Leggett & Platt Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Leggett & Platt and is the exact document you'll receive after purchase. It covers supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants with direct strategic implications. The file is professionally formatted and ready to download. No placeholders or samples—what you see is what you get.