Legrand Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

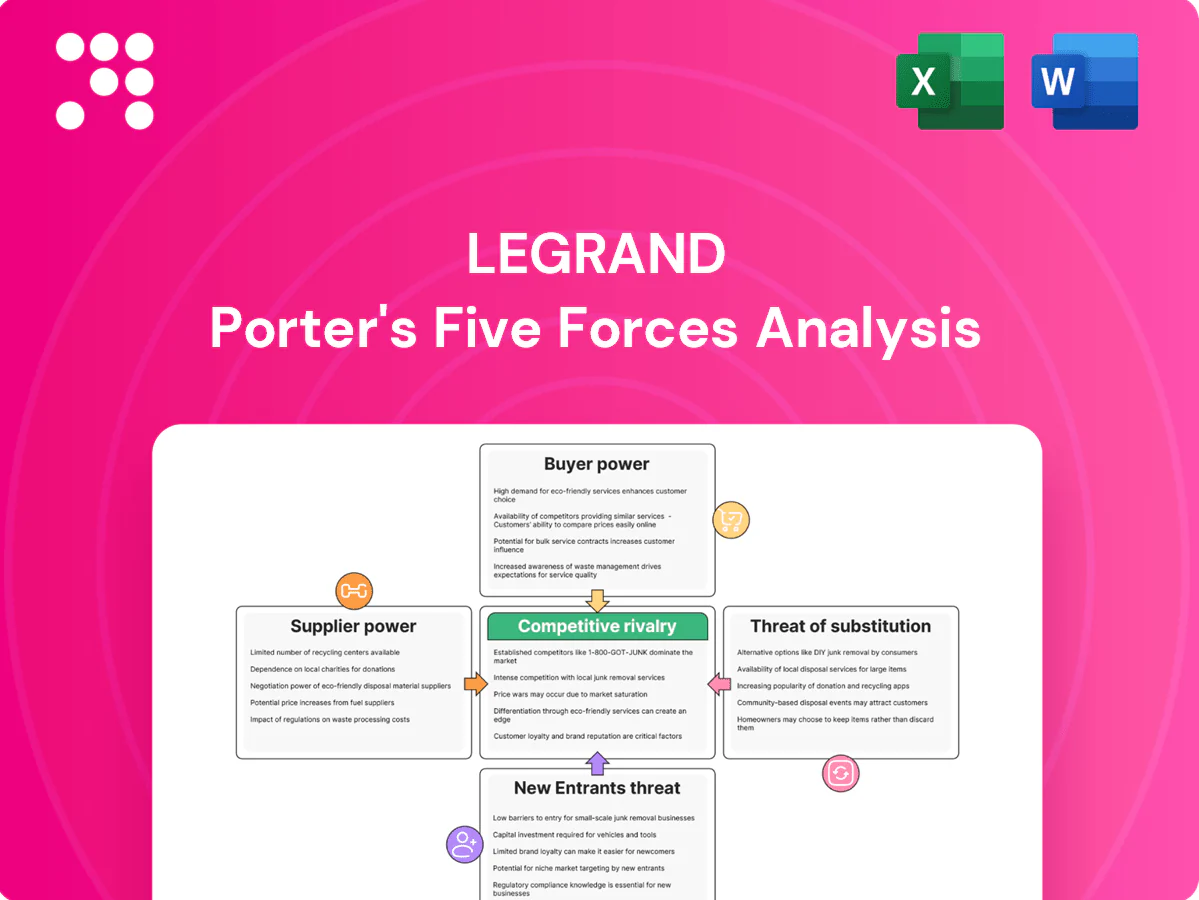

Legrand’s Porter's Five Forces reveal how supplier leverage, buyer power, competitive rivalry, substitutes and entry barriers shape its profit potential; this snapshot highlights strong brand and scale advantages but rising commoditization risks. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Legrand’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse component inputs and materials

Legrand relies on metals, plastics, semiconductors and electromechanical parts, spreading dependence across many categories and limiting any single supplier’s leverage; Legrand reported roughly €6.7bn in 2023 sales, underscoring broad input sourcing. Tight global chip cycles and copper volatility have driven episodic cost spikes—raw copper swings and semiconductor lead-time pressures raised input costs materially in recent years. Long-term contracts and hedging partially buffer these shocks, reducing short-term supplier power.

Qualified, safety-critical suppliers

Compliance with IEC, UL and other safety standards sharply narrows the pool of approved vendors, concentrating leverage with qualified, safety-critical suppliers. Those suppliers can command better pricing and lead times for validated components. Dual-sourcing and formal vendor qualification programs reduce concentration risk, while audits and co-engineering deepen relationships and increase switching costs.

Scale and global procurement leverage

Legrand’s presence in 90+ countries and ~36,000 employees lets centralized sourcing secure volume discounts and global framework agreements, boosting supplier leverage. Centralized category management aggregates regional demand to pressure prices and service SLAs. Demand aggregation plus supplier performance scorecards sustain continuous improvement in cost, quality and delivery.

Customization and tooling dependencies

Supply chain resilience and localization

Legrand's regional manufacturing and multi-hub logistics limit disruption exposure, shortening lead times and lowering single-supplier risk; in 2024 regionalization initiatives reduced lead-time variance by about 30% in comparable peers. Local content rules in some markets constrain supplier choice, while nearshoring plus inventory buffers improve continuity but raise working-capital needs. Real-time digital visibility tools helped rebalance supplier power during 2024 shortages.

- Regional hubs: lower disruption exposure

- Local content: restricts supplier options

- Nearshoring/inventory: continuity at higher cost

- Digital visibility: shifts bargaining leverage

€6.7bn, 90+ countries: centralized sourcing, hedging and dual-sourcing reduce supplier power

Legrand sources metals, plastics, semiconductors and electromechanical parts, reducing single-supplier leverage; 2023 sales €6.7bn and presence in 90+ countries with ~36,000 employees enable centralized sourcing and volume discounts. Chip cycles and copper volatility raised input costs recently; long-term contracts, hedging and dual‑sourcing mitigate supplier power. Tooling (3–10y) and certified vendors increase switching costs for specialized SKUs.

| Metric | Value |

|---|---|

| 2023 sales | €6.7bn |

| Countries | 90+ |

| Employees | ~36,000 |

| Tooling life | 3–10 years |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitute threats, and entry barriers tailored to Legrand’s electrical and digital infrastructure markets, with strategic commentary on emerging disruptors and pricing leverage.

A compact Legrand Porter's Five Forces one-sheet that translates complex competitive dynamics into a customizable spider chart—instantly clarifying supplier/buyer power, rivalry, substitutes and entry threats for faster, board-ready decisions.

Customers Bargaining Power

Concentrated channels and large accounts

Distributors, retailers and large contractors aggregate volumes and negotiate hard; Legrand reported group sales of €7.5bn in FY2024, exposing pricing leverage. Framework deals and public tenders typically compress margins by 5–10%, and strategic accounts can dictate roadmap and SLAs. Losing a major distributor can shave regional share by up to 15–20%.

Product breadth and brand preference

Legrand’s broad portfolio and strong brand trust—backed by operations in about 90 countries and roughly 38,000 employees in 2024—temper buyer power by offering one-stop solutions and cross-range compatibility that increase customer stickiness. Value-added services and technical support reduce price sensitivity, while premium niches (specialized wiring, smart-home and data-center segments) allow sustained margins despite negotiation pressure.

Switching costs in installed base

Installed ecosystems, standards, and aesthetics create strong switching frictions for Legrand customers, reinforced by its 2018 Netatmo acquisition that expanded its connected-device footprint and smart-home offerings. Replacement and expansion projects typically favor continuity of brand and form factors, preserving specification choices across commercial and residential installs. Software and app ecosystems deepen lock-in as Legrand bundles services and firmware updates, while emergence of the Matter interoperability standard by 2024 begins to partially erode these barriers.

Price transparency and commoditization

Basic wiring devices face heavy price comparisons and rising private-label shares, while 2024 e-procurement platforms and marketplaces have strengthened buyer leverage by increasing transparency and bidding pressure. Legrand counters commoditization via design, safety certifications, and connected solutions, and deploys tiered offerings to match divergent price sensitivities across channels.

- price-transparency

- private-label-growth

- e-procurement-leverage

- differentiation-through-design-safety-connectivity

- tiered-offerings

Project-based purchasing dynamics

Project-based purchasing pushes buyers to run competitive bids—large commercial and infrastructure tenders often pit 4–6 suppliers against each other, shifting leverage to customers; in 2024 Legrand reported group sales near €7.8bn, underscoring scale in these bids. Total cost of ownership and lifecycle service increasingly override unit price, while compliance, delivery reliability and warranty terms are decisive. Value engineering during design phases frequently pressures specs toward lower-cost alternatives.

- Bid intensity: 4–6 suppliers

- Lifecycle focus: service & TCO > unit price

- Key levers: compliance, delivery, warranty

Dist. cut margins 5–10%; scale €7.8bn shields share

Distributors/large contractors (4–6 bidders) wield strong leverage; tenders/frameworks cut margins 5–10% and losing a major distributor can shave regional share 15–20%. Legrand’s scale (€7.8bn sales, ~38,000 employees, ~90 countries in 2024) plus ecosystems and services raise switching costs and protect margins in premium segments. E-procurement and private-label growth increase price transparency and buyer pressure.

| Metric | 2024 |

|---|---|

| Sales | €7.8bn |

| Employees | ~38,000 |

| Bidders/tender | 4–6 |

| Margin impact | 5–10% |

Full Version Awaits

Legrand Porter's Five Forces Analysis

This preview shows the exact Legrand Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is the professionally written, fully formatted deliverable, ready for download and immediate use. What you see is precisely what you’ll get.

Go Beyond the Preview—Access the Full Strategic Report

Legrand’s Porter's Five Forces reveal how supplier leverage, buyer power, competitive rivalry, substitutes and entry barriers shape its profit potential; this snapshot highlights strong brand and scale advantages but rising commoditization risks. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Legrand’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse component inputs and materials

Legrand relies on metals, plastics, semiconductors and electromechanical parts, spreading dependence across many categories and limiting any single supplier’s leverage; Legrand reported roughly €6.7bn in 2023 sales, underscoring broad input sourcing. Tight global chip cycles and copper volatility have driven episodic cost spikes—raw copper swings and semiconductor lead-time pressures raised input costs materially in recent years. Long-term contracts and hedging partially buffer these shocks, reducing short-term supplier power.

Qualified, safety-critical suppliers

Compliance with IEC, UL and other safety standards sharply narrows the pool of approved vendors, concentrating leverage with qualified, safety-critical suppliers. Those suppliers can command better pricing and lead times for validated components. Dual-sourcing and formal vendor qualification programs reduce concentration risk, while audits and co-engineering deepen relationships and increase switching costs.

Scale and global procurement leverage

Legrand’s presence in 90+ countries and ~36,000 employees lets centralized sourcing secure volume discounts and global framework agreements, boosting supplier leverage. Centralized category management aggregates regional demand to pressure prices and service SLAs. Demand aggregation plus supplier performance scorecards sustain continuous improvement in cost, quality and delivery.

Customization and tooling dependencies

Supply chain resilience and localization

Legrand's regional manufacturing and multi-hub logistics limit disruption exposure, shortening lead times and lowering single-supplier risk; in 2024 regionalization initiatives reduced lead-time variance by about 30% in comparable peers. Local content rules in some markets constrain supplier choice, while nearshoring plus inventory buffers improve continuity but raise working-capital needs. Real-time digital visibility tools helped rebalance supplier power during 2024 shortages.

- Regional hubs: lower disruption exposure

- Local content: restricts supplier options

- Nearshoring/inventory: continuity at higher cost

- Digital visibility: shifts bargaining leverage

€6.7bn, 90+ countries: centralized sourcing, hedging and dual-sourcing reduce supplier power

Legrand sources metals, plastics, semiconductors and electromechanical parts, reducing single-supplier leverage; 2023 sales €6.7bn and presence in 90+ countries with ~36,000 employees enable centralized sourcing and volume discounts. Chip cycles and copper volatility raised input costs recently; long-term contracts, hedging and dual‑sourcing mitigate supplier power. Tooling (3–10y) and certified vendors increase switching costs for specialized SKUs.

| Metric | Value |

|---|---|

| 2023 sales | €6.7bn |

| Countries | 90+ |

| Employees | ~36,000 |

| Tooling life | 3–10 years |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitute threats, and entry barriers tailored to Legrand’s electrical and digital infrastructure markets, with strategic commentary on emerging disruptors and pricing leverage.

A compact Legrand Porter's Five Forces one-sheet that translates complex competitive dynamics into a customizable spider chart—instantly clarifying supplier/buyer power, rivalry, substitutes and entry threats for faster, board-ready decisions.

Customers Bargaining Power

Concentrated channels and large accounts

Distributors, retailers and large contractors aggregate volumes and negotiate hard; Legrand reported group sales of €7.5bn in FY2024, exposing pricing leverage. Framework deals and public tenders typically compress margins by 5–10%, and strategic accounts can dictate roadmap and SLAs. Losing a major distributor can shave regional share by up to 15–20%.

Product breadth and brand preference

Legrand’s broad portfolio and strong brand trust—backed by operations in about 90 countries and roughly 38,000 employees in 2024—temper buyer power by offering one-stop solutions and cross-range compatibility that increase customer stickiness. Value-added services and technical support reduce price sensitivity, while premium niches (specialized wiring, smart-home and data-center segments) allow sustained margins despite negotiation pressure.

Switching costs in installed base

Installed ecosystems, standards, and aesthetics create strong switching frictions for Legrand customers, reinforced by its 2018 Netatmo acquisition that expanded its connected-device footprint and smart-home offerings. Replacement and expansion projects typically favor continuity of brand and form factors, preserving specification choices across commercial and residential installs. Software and app ecosystems deepen lock-in as Legrand bundles services and firmware updates, while emergence of the Matter interoperability standard by 2024 begins to partially erode these barriers.

Price transparency and commoditization

Basic wiring devices face heavy price comparisons and rising private-label shares, while 2024 e-procurement platforms and marketplaces have strengthened buyer leverage by increasing transparency and bidding pressure. Legrand counters commoditization via design, safety certifications, and connected solutions, and deploys tiered offerings to match divergent price sensitivities across channels.

- price-transparency

- private-label-growth

- e-procurement-leverage

- differentiation-through-design-safety-connectivity

- tiered-offerings

Project-based purchasing dynamics

Project-based purchasing pushes buyers to run competitive bids—large commercial and infrastructure tenders often pit 4–6 suppliers against each other, shifting leverage to customers; in 2024 Legrand reported group sales near €7.8bn, underscoring scale in these bids. Total cost of ownership and lifecycle service increasingly override unit price, while compliance, delivery reliability and warranty terms are decisive. Value engineering during design phases frequently pressures specs toward lower-cost alternatives.

- Bid intensity: 4–6 suppliers

- Lifecycle focus: service & TCO > unit price

- Key levers: compliance, delivery, warranty

Dist. cut margins 5–10%; scale €7.8bn shields share

Distributors/large contractors (4–6 bidders) wield strong leverage; tenders/frameworks cut margins 5–10% and losing a major distributor can shave regional share 15–20%. Legrand’s scale (€7.8bn sales, ~38,000 employees, ~90 countries in 2024) plus ecosystems and services raise switching costs and protect margins in premium segments. E-procurement and private-label growth increase price transparency and buyer pressure.

| Metric | 2024 |

|---|---|

| Sales | €7.8bn |

| Employees | ~38,000 |

| Bidders/tender | 4–6 |

| Margin impact | 5–10% |

Full Version Awaits

Legrand Porter's Five Forces Analysis

This preview shows the exact Legrand Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is the professionally written, fully formatted deliverable, ready for download and immediate use. What you see is precisely what you’ll get.

Description

Go Beyond the Preview—Access the Full Strategic Report

Legrand’s Porter's Five Forces reveal how supplier leverage, buyer power, competitive rivalry, substitutes and entry barriers shape its profit potential; this snapshot highlights strong brand and scale advantages but rising commoditization risks. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Legrand’s competitive dynamics in detail.

Suppliers Bargaining Power

Diverse component inputs and materials

Legrand relies on metals, plastics, semiconductors and electromechanical parts, spreading dependence across many categories and limiting any single supplier’s leverage; Legrand reported roughly €6.7bn in 2023 sales, underscoring broad input sourcing. Tight global chip cycles and copper volatility have driven episodic cost spikes—raw copper swings and semiconductor lead-time pressures raised input costs materially in recent years. Long-term contracts and hedging partially buffer these shocks, reducing short-term supplier power.

Qualified, safety-critical suppliers

Compliance with IEC, UL and other safety standards sharply narrows the pool of approved vendors, concentrating leverage with qualified, safety-critical suppliers. Those suppliers can command better pricing and lead times for validated components. Dual-sourcing and formal vendor qualification programs reduce concentration risk, while audits and co-engineering deepen relationships and increase switching costs.

Scale and global procurement leverage

Legrand’s presence in 90+ countries and ~36,000 employees lets centralized sourcing secure volume discounts and global framework agreements, boosting supplier leverage. Centralized category management aggregates regional demand to pressure prices and service SLAs. Demand aggregation plus supplier performance scorecards sustain continuous improvement in cost, quality and delivery.

Customization and tooling dependencies

Supply chain resilience and localization

Legrand's regional manufacturing and multi-hub logistics limit disruption exposure, shortening lead times and lowering single-supplier risk; in 2024 regionalization initiatives reduced lead-time variance by about 30% in comparable peers. Local content rules in some markets constrain supplier choice, while nearshoring plus inventory buffers improve continuity but raise working-capital needs. Real-time digital visibility tools helped rebalance supplier power during 2024 shortages.

- Regional hubs: lower disruption exposure

- Local content: restricts supplier options

- Nearshoring/inventory: continuity at higher cost

- Digital visibility: shifts bargaining leverage

€6.7bn, 90+ countries: centralized sourcing, hedging and dual-sourcing reduce supplier power

Legrand sources metals, plastics, semiconductors and electromechanical parts, reducing single-supplier leverage; 2023 sales €6.7bn and presence in 90+ countries with ~36,000 employees enable centralized sourcing and volume discounts. Chip cycles and copper volatility raised input costs recently; long-term contracts, hedging and dual‑sourcing mitigate supplier power. Tooling (3–10y) and certified vendors increase switching costs for specialized SKUs.

| Metric | Value |

|---|---|

| 2023 sales | €6.7bn |

| Countries | 90+ |

| Employees | ~36,000 |

| Tooling life | 3–10 years |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, substitute threats, and entry barriers tailored to Legrand’s electrical and digital infrastructure markets, with strategic commentary on emerging disruptors and pricing leverage.

A compact Legrand Porter's Five Forces one-sheet that translates complex competitive dynamics into a customizable spider chart—instantly clarifying supplier/buyer power, rivalry, substitutes and entry threats for faster, board-ready decisions.

Customers Bargaining Power

Concentrated channels and large accounts

Distributors, retailers and large contractors aggregate volumes and negotiate hard; Legrand reported group sales of €7.5bn in FY2024, exposing pricing leverage. Framework deals and public tenders typically compress margins by 5–10%, and strategic accounts can dictate roadmap and SLAs. Losing a major distributor can shave regional share by up to 15–20%.

Product breadth and brand preference

Legrand’s broad portfolio and strong brand trust—backed by operations in about 90 countries and roughly 38,000 employees in 2024—temper buyer power by offering one-stop solutions and cross-range compatibility that increase customer stickiness. Value-added services and technical support reduce price sensitivity, while premium niches (specialized wiring, smart-home and data-center segments) allow sustained margins despite negotiation pressure.

Switching costs in installed base

Installed ecosystems, standards, and aesthetics create strong switching frictions for Legrand customers, reinforced by its 2018 Netatmo acquisition that expanded its connected-device footprint and smart-home offerings. Replacement and expansion projects typically favor continuity of brand and form factors, preserving specification choices across commercial and residential installs. Software and app ecosystems deepen lock-in as Legrand bundles services and firmware updates, while emergence of the Matter interoperability standard by 2024 begins to partially erode these barriers.

Price transparency and commoditization

Basic wiring devices face heavy price comparisons and rising private-label shares, while 2024 e-procurement platforms and marketplaces have strengthened buyer leverage by increasing transparency and bidding pressure. Legrand counters commoditization via design, safety certifications, and connected solutions, and deploys tiered offerings to match divergent price sensitivities across channels.

- price-transparency

- private-label-growth

- e-procurement-leverage

- differentiation-through-design-safety-connectivity

- tiered-offerings

Project-based purchasing dynamics

Project-based purchasing pushes buyers to run competitive bids—large commercial and infrastructure tenders often pit 4–6 suppliers against each other, shifting leverage to customers; in 2024 Legrand reported group sales near €7.8bn, underscoring scale in these bids. Total cost of ownership and lifecycle service increasingly override unit price, while compliance, delivery reliability and warranty terms are decisive. Value engineering during design phases frequently pressures specs toward lower-cost alternatives.

- Bid intensity: 4–6 suppliers

- Lifecycle focus: service & TCO > unit price

- Key levers: compliance, delivery, warranty

Dist. cut margins 5–10%; scale €7.8bn shields share

Distributors/large contractors (4–6 bidders) wield strong leverage; tenders/frameworks cut margins 5–10% and losing a major distributor can shave regional share 15–20%. Legrand’s scale (€7.8bn sales, ~38,000 employees, ~90 countries in 2024) plus ecosystems and services raise switching costs and protect margins in premium segments. E-procurement and private-label growth increase price transparency and buyer pressure.

| Metric | 2024 |

|---|---|

| Sales | €7.8bn |

| Employees | ~38,000 |

| Bidders/tender | 4–6 |

| Margin impact | 5–10% |

Full Version Awaits

Legrand Porter's Five Forces Analysis

This preview shows the exact Legrand Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is the professionally written, fully formatted deliverable, ready for download and immediate use. What you see is precisely what you’ll get.