Leidos Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Leidos operates in a high-stakes defense and IT services market where buyer concentration, government contracting, and technological shifts shape profitability. Supplier power is moderate while regulatory and bidding barriers limit new entrants. Competitive rivalry is intense across specialty segments. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Leidos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component vendors

Leidos depends on niche hardware, sensors and secure-communications components with few qualified suppliers, and in 2024 many such parts faced lead times exceeding 12 months. Export/ITAR controls and limited substitutes amplify vendor leverage, forcing schedule or pricing concessions. Dual-sourcing is feasible but typically adds lengthy qualification timelines and multi-million-dollar certification costs.

Cloud and OEM dependence

Mission systems increasingly rely on hyperscale clouds and OEM stacks, with AWS, Microsoft Azure and Google Cloud holding roughly 65% combined market share in 2024, so certification, proprietary tooling and restrictive EULAs materially raise switching costs. Volume discounts blunt supplier power, but feature lock-in and proprietary APIs keep migration expensive. Outages or price shifts at hyperscalers can immediately ripple through program budgets and timelines.

Skilled labor as supplier

Clearable STEM talent and TS/SCI-cleared engineers act as a critical supplier for Leidos, with the firm drawing from a constrained pool amid an industry where cleared personnel remain scarce; Leidos' workforce is roughly 40,000–50,000 employees (2024). Tight 2024 labor markets gave staffing firms and cleared employees leverage, driving wage inflation and retention bonuses (industry pay growth around 4–6% in 2024) that press margins; non-competes and talent pipelines mitigate but do not eliminate this risk.

Data and classified access

Access to proprietary datasets, models and classified ranges is highly concentrated, enabling owners to set pricing and delivery terms. Owners of ranges or classified environments can dictate contract conditions and timelines. Switching is constrained by accreditation and need-to-know, creating localized supplier power despite Leidos scale; Leidos reported about 45,000 employees in 2024.

- Concentration: limited range/dataset owners

- Control: owners dictate terms

- Barrier: accreditation & need-to-know

- Impact: localized supplier power

Integration and certification costs

Once a component is ATO’d and integrated, replacement triggers recertification that can add months and significant cost; Leidos reported $14.4B revenue in FY2024, highlighting scale-dependent sustainment exposure. Rework, testing and schedule risk raise effective switching costs, while suppliers use renewal cycles to extract better terms. Long-term sustainment contracts (often 5+ years) entrench dependencies and limit buyer leverage.

Suppliers, hyperscalers and cleared STEM talent squeeze defense IT margins

Suppliers hold strong leverage over Leidos due to scarce niche hardware with >12-month 2024 lead times, ITAR/export limits and costly ATO recertification. Hyperscalers (AWS/Microsoft/Google ~65% 2024) and cleared STEM talent (Leidos ~45,000–50,000 employees; industry pay growth 4–6% 2024) raise switching costs and wage-driven margin pressure. Long sustainment contracts (5+ years) and concentrated range/dataset owners enable price and term extraction.

| Metric | 2024 |

|---|---|

| Leidos revenue | $14.4B |

| Hyperscaler share | ~65% |

| Employees (est) | 45k–50k |

| Lead times | >12 months |

| Industry pay growth | 4–6% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Leidos, with detailed analysis of each force supported by industry data and strategic commentary. Identifies disruptive threats, substitutes, and buyer/supplier power that shape pricing and profitability, delivered in a fully editable format for use in reports, investor decks, or academic projects.

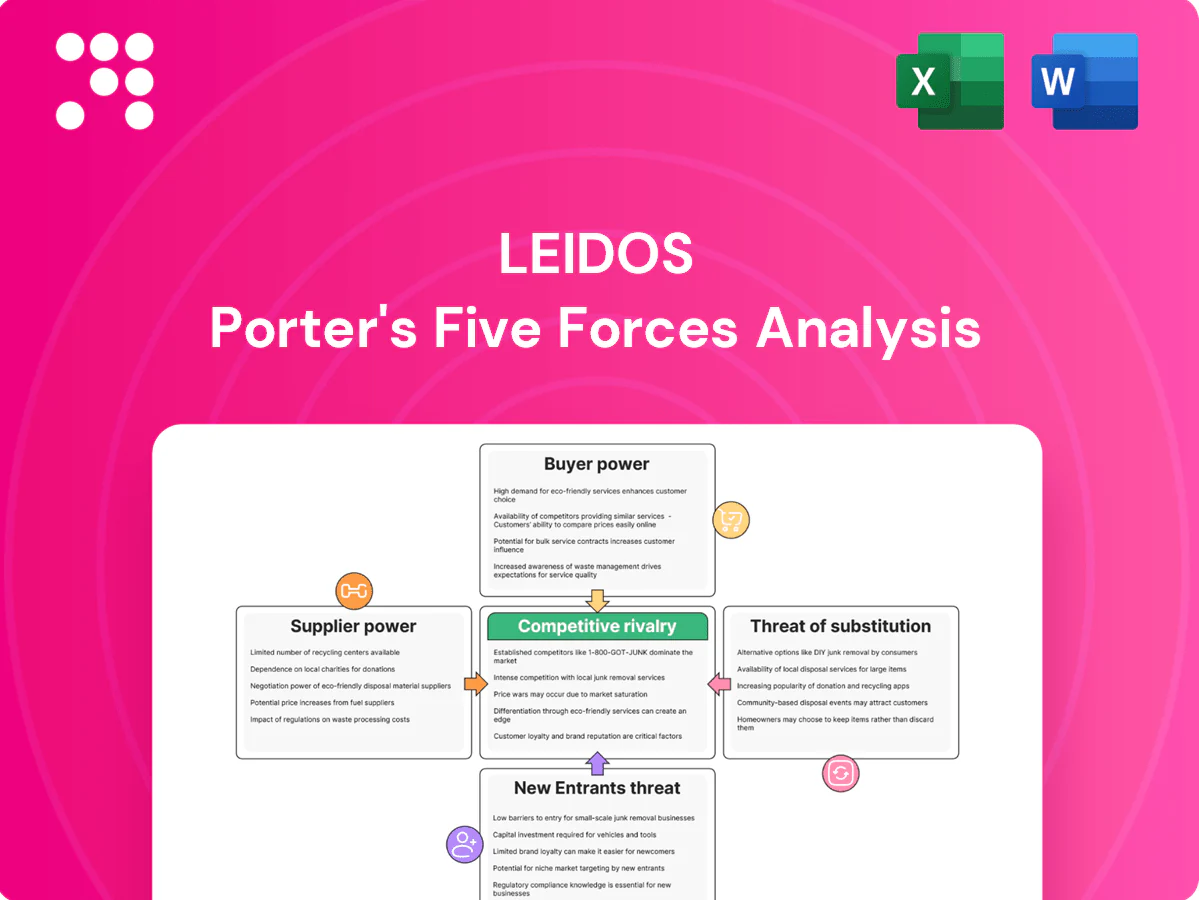

A concise one-sheet Porter's Five Forces for Leidos that visualizes competitive pressure with a radar chart and lets you customize force levels and swap in your own data—ready for pitch decks, dashboards, or boardroom slides without macros.

Customers Bargaining Power

Concentrated government buyers

US federal agencies, led by the DoD whose FY2024 budget was about 858 billion, and a handful of allied governments dominate Leidos demand, giving buyers concentrated leverage. Their scale and explicit budget authority enable strong price and contract-negotiation power. Program offices routinely define scope and technical baselines that favor incumbents or force concessions. Agency strategies to diversify vendors via multiple-award IDIQs further intensify pricing and margin pressure.

Procurement rigor and price pressure

Competitive RFPs, LPTA and cost-reimbursable awards constrain Leidos margins as buyers force rate cards and ceiling rates across task orders; should-cost reviews and audits in 2024 increased pricing transparency, pressuring bid marks. Bid protests and debriefs sharpen competition and raise proposal costs. Leidos, with roughly 42,000 employees and about $14 billion revenue in 2024, faces compressed win margins.

Past performance leverage

Agencies weigh CPARS ratings and incumbency—Leidos reported $14.7 billion revenue in FY2024—yet buyers still extract concessions during option exercises and recompetes, which reset commercial terms. Missed SLAs can trigger contractually defined withholds and penalties tied to performance metrics. Strong past performance improves win probability but does not materially weaken federal buyer leverage.

Contract vehicles and modular buys

GWACs and IDIQs (for example Alliant 2 with a $50B ceiling) enable rapid tasking and switching among vendors, while modular open systems approaches reduce vendor lock-in and let agencies disaggregate work across multiple suppliers. Buyers can split scopes and award smaller task orders, increasing competition and elevating customer bargaining power against prime contractors like Leidos. This fragmentation amplifies price pressure and leverage in negotiations.

- GWAC/IDIQ scale: Alliant 2 $50B+

- Modularity lowers switching costs

- Disaggregation increases buyer leverage

Shift to outcomes and OTA

Outcome-based metrics shift delivery risk to vendors, forcing Leidos and peers to guarantee performance and absorb cost overruns; OTAs accelerate awards while keeping buyer options, prompting faster entry to competitions. Pilots and down-selects create bake-offs on capability and price, and vendors must invest upfront to win, strengthening buyer leverage.

- Outcome risk borne by vendors

- OTAs shorten cycles

- Pilots enable direct comparisons

- Upfront vendor investment increases buyer leverage

Federal buying power, GWACs and OTAs intensify price pressure and margin compression

Federal buyers (DoD FY2024 ~$858B) concentrate demand and wield strong price/contract leverage over Leidos (FY2024 revenue $14.7B; ~42,000 employees). GWACs/IDIQs (Alliant 2 $50B+) and modular contracting lower switching costs, intensifying price pressure and margin compression via LPTA, should-cost reviews and CPARS-based selections. Outcome-based metrics and OTAs shift risk to vendors, raising upfront investment and strengthening buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| DoD budget | $858B |

| Leidos revenue | $14.7B |

| Employees | ~42,000 |

| Alliant 2 ceiling | $50B+ |

What You See Is What You Get

Leidos Porter's Five Forces Analysis

This Leidos Porter's Five Forces analysis offers a concise, professional assessment of competitive rivalry, buyer and supplier power, threat of entrants, and substitute pressures specific to Leidos' markets. You're looking at the actual document—once purchased you’ll get instant access to this exact file. It's fully formatted and ready for strategic use.

Go Beyond the Preview—Access the Full Strategic Report

Leidos operates in a high-stakes defense and IT services market where buyer concentration, government contracting, and technological shifts shape profitability. Supplier power is moderate while regulatory and bidding barriers limit new entrants. Competitive rivalry is intense across specialty segments. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Leidos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component vendors

Leidos depends on niche hardware, sensors and secure-communications components with few qualified suppliers, and in 2024 many such parts faced lead times exceeding 12 months. Export/ITAR controls and limited substitutes amplify vendor leverage, forcing schedule or pricing concessions. Dual-sourcing is feasible but typically adds lengthy qualification timelines and multi-million-dollar certification costs.

Cloud and OEM dependence

Mission systems increasingly rely on hyperscale clouds and OEM stacks, with AWS, Microsoft Azure and Google Cloud holding roughly 65% combined market share in 2024, so certification, proprietary tooling and restrictive EULAs materially raise switching costs. Volume discounts blunt supplier power, but feature lock-in and proprietary APIs keep migration expensive. Outages or price shifts at hyperscalers can immediately ripple through program budgets and timelines.

Skilled labor as supplier

Clearable STEM talent and TS/SCI-cleared engineers act as a critical supplier for Leidos, with the firm drawing from a constrained pool amid an industry where cleared personnel remain scarce; Leidos' workforce is roughly 40,000–50,000 employees (2024). Tight 2024 labor markets gave staffing firms and cleared employees leverage, driving wage inflation and retention bonuses (industry pay growth around 4–6% in 2024) that press margins; non-competes and talent pipelines mitigate but do not eliminate this risk.

Data and classified access

Access to proprietary datasets, models and classified ranges is highly concentrated, enabling owners to set pricing and delivery terms. Owners of ranges or classified environments can dictate contract conditions and timelines. Switching is constrained by accreditation and need-to-know, creating localized supplier power despite Leidos scale; Leidos reported about 45,000 employees in 2024.

- Concentration: limited range/dataset owners

- Control: owners dictate terms

- Barrier: accreditation & need-to-know

- Impact: localized supplier power

Integration and certification costs

Once a component is ATO’d and integrated, replacement triggers recertification that can add months and significant cost; Leidos reported $14.4B revenue in FY2024, highlighting scale-dependent sustainment exposure. Rework, testing and schedule risk raise effective switching costs, while suppliers use renewal cycles to extract better terms. Long-term sustainment contracts (often 5+ years) entrench dependencies and limit buyer leverage.

Suppliers, hyperscalers and cleared STEM talent squeeze defense IT margins

Suppliers hold strong leverage over Leidos due to scarce niche hardware with >12-month 2024 lead times, ITAR/export limits and costly ATO recertification. Hyperscalers (AWS/Microsoft/Google ~65% 2024) and cleared STEM talent (Leidos ~45,000–50,000 employees; industry pay growth 4–6% 2024) raise switching costs and wage-driven margin pressure. Long sustainment contracts (5+ years) and concentrated range/dataset owners enable price and term extraction.

| Metric | 2024 |

|---|---|

| Leidos revenue | $14.4B |

| Hyperscaler share | ~65% |

| Employees (est) | 45k–50k |

| Lead times | >12 months |

| Industry pay growth | 4–6% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Leidos, with detailed analysis of each force supported by industry data and strategic commentary. Identifies disruptive threats, substitutes, and buyer/supplier power that shape pricing and profitability, delivered in a fully editable format for use in reports, investor decks, or academic projects.

A concise one-sheet Porter's Five Forces for Leidos that visualizes competitive pressure with a radar chart and lets you customize force levels and swap in your own data—ready for pitch decks, dashboards, or boardroom slides without macros.

Customers Bargaining Power

Concentrated government buyers

US federal agencies, led by the DoD whose FY2024 budget was about 858 billion, and a handful of allied governments dominate Leidos demand, giving buyers concentrated leverage. Their scale and explicit budget authority enable strong price and contract-negotiation power. Program offices routinely define scope and technical baselines that favor incumbents or force concessions. Agency strategies to diversify vendors via multiple-award IDIQs further intensify pricing and margin pressure.

Procurement rigor and price pressure

Competitive RFPs, LPTA and cost-reimbursable awards constrain Leidos margins as buyers force rate cards and ceiling rates across task orders; should-cost reviews and audits in 2024 increased pricing transparency, pressuring bid marks. Bid protests and debriefs sharpen competition and raise proposal costs. Leidos, with roughly 42,000 employees and about $14 billion revenue in 2024, faces compressed win margins.

Past performance leverage

Agencies weigh CPARS ratings and incumbency—Leidos reported $14.7 billion revenue in FY2024—yet buyers still extract concessions during option exercises and recompetes, which reset commercial terms. Missed SLAs can trigger contractually defined withholds and penalties tied to performance metrics. Strong past performance improves win probability but does not materially weaken federal buyer leverage.

Contract vehicles and modular buys

GWACs and IDIQs (for example Alliant 2 with a $50B ceiling) enable rapid tasking and switching among vendors, while modular open systems approaches reduce vendor lock-in and let agencies disaggregate work across multiple suppliers. Buyers can split scopes and award smaller task orders, increasing competition and elevating customer bargaining power against prime contractors like Leidos. This fragmentation amplifies price pressure and leverage in negotiations.

- GWAC/IDIQ scale: Alliant 2 $50B+

- Modularity lowers switching costs

- Disaggregation increases buyer leverage

Shift to outcomes and OTA

Outcome-based metrics shift delivery risk to vendors, forcing Leidos and peers to guarantee performance and absorb cost overruns; OTAs accelerate awards while keeping buyer options, prompting faster entry to competitions. Pilots and down-selects create bake-offs on capability and price, and vendors must invest upfront to win, strengthening buyer leverage.

- Outcome risk borne by vendors

- OTAs shorten cycles

- Pilots enable direct comparisons

- Upfront vendor investment increases buyer leverage

Federal buying power, GWACs and OTAs intensify price pressure and margin compression

Federal buyers (DoD FY2024 ~$858B) concentrate demand and wield strong price/contract leverage over Leidos (FY2024 revenue $14.7B; ~42,000 employees). GWACs/IDIQs (Alliant 2 $50B+) and modular contracting lower switching costs, intensifying price pressure and margin compression via LPTA, should-cost reviews and CPARS-based selections. Outcome-based metrics and OTAs shift risk to vendors, raising upfront investment and strengthening buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| DoD budget | $858B |

| Leidos revenue | $14.7B |

| Employees | ~42,000 |

| Alliant 2 ceiling | $50B+ |

What You See Is What You Get

Leidos Porter's Five Forces Analysis

This Leidos Porter's Five Forces analysis offers a concise, professional assessment of competitive rivalry, buyer and supplier power, threat of entrants, and substitute pressures specific to Leidos' markets. You're looking at the actual document—once purchased you’ll get instant access to this exact file. It's fully formatted and ready for strategic use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Leidos operates in a high-stakes defense and IT services market where buyer concentration, government contracting, and technological shifts shape profitability. Supplier power is moderate while regulatory and bidding barriers limit new entrants. Competitive rivalry is intense across specialty segments. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Leidos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component vendors

Leidos depends on niche hardware, sensors and secure-communications components with few qualified suppliers, and in 2024 many such parts faced lead times exceeding 12 months. Export/ITAR controls and limited substitutes amplify vendor leverage, forcing schedule or pricing concessions. Dual-sourcing is feasible but typically adds lengthy qualification timelines and multi-million-dollar certification costs.

Cloud and OEM dependence

Mission systems increasingly rely on hyperscale clouds and OEM stacks, with AWS, Microsoft Azure and Google Cloud holding roughly 65% combined market share in 2024, so certification, proprietary tooling and restrictive EULAs materially raise switching costs. Volume discounts blunt supplier power, but feature lock-in and proprietary APIs keep migration expensive. Outages or price shifts at hyperscalers can immediately ripple through program budgets and timelines.

Skilled labor as supplier

Clearable STEM talent and TS/SCI-cleared engineers act as a critical supplier for Leidos, with the firm drawing from a constrained pool amid an industry where cleared personnel remain scarce; Leidos' workforce is roughly 40,000–50,000 employees (2024). Tight 2024 labor markets gave staffing firms and cleared employees leverage, driving wage inflation and retention bonuses (industry pay growth around 4–6% in 2024) that press margins; non-competes and talent pipelines mitigate but do not eliminate this risk.

Data and classified access

Access to proprietary datasets, models and classified ranges is highly concentrated, enabling owners to set pricing and delivery terms. Owners of ranges or classified environments can dictate contract conditions and timelines. Switching is constrained by accreditation and need-to-know, creating localized supplier power despite Leidos scale; Leidos reported about 45,000 employees in 2024.

- Concentration: limited range/dataset owners

- Control: owners dictate terms

- Barrier: accreditation & need-to-know

- Impact: localized supplier power

Integration and certification costs

Once a component is ATO’d and integrated, replacement triggers recertification that can add months and significant cost; Leidos reported $14.4B revenue in FY2024, highlighting scale-dependent sustainment exposure. Rework, testing and schedule risk raise effective switching costs, while suppliers use renewal cycles to extract better terms. Long-term sustainment contracts (often 5+ years) entrench dependencies and limit buyer leverage.

Suppliers, hyperscalers and cleared STEM talent squeeze defense IT margins

Suppliers hold strong leverage over Leidos due to scarce niche hardware with >12-month 2024 lead times, ITAR/export limits and costly ATO recertification. Hyperscalers (AWS/Microsoft/Google ~65% 2024) and cleared STEM talent (Leidos ~45,000–50,000 employees; industry pay growth 4–6% 2024) raise switching costs and wage-driven margin pressure. Long sustainment contracts (5+ years) and concentrated range/dataset owners enable price and term extraction.

| Metric | 2024 |

|---|---|

| Leidos revenue | $14.4B |

| Hyperscaler share | ~65% |

| Employees (est) | 45k–50k |

| Lead times | >12 months |

| Industry pay growth | 4–6% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to Leidos, with detailed analysis of each force supported by industry data and strategic commentary. Identifies disruptive threats, substitutes, and buyer/supplier power that shape pricing and profitability, delivered in a fully editable format for use in reports, investor decks, or academic projects.

A concise one-sheet Porter's Five Forces for Leidos that visualizes competitive pressure with a radar chart and lets you customize force levels and swap in your own data—ready for pitch decks, dashboards, or boardroom slides without macros.

Customers Bargaining Power

Concentrated government buyers

US federal agencies, led by the DoD whose FY2024 budget was about 858 billion, and a handful of allied governments dominate Leidos demand, giving buyers concentrated leverage. Their scale and explicit budget authority enable strong price and contract-negotiation power. Program offices routinely define scope and technical baselines that favor incumbents or force concessions. Agency strategies to diversify vendors via multiple-award IDIQs further intensify pricing and margin pressure.

Procurement rigor and price pressure

Competitive RFPs, LPTA and cost-reimbursable awards constrain Leidos margins as buyers force rate cards and ceiling rates across task orders; should-cost reviews and audits in 2024 increased pricing transparency, pressuring bid marks. Bid protests and debriefs sharpen competition and raise proposal costs. Leidos, with roughly 42,000 employees and about $14 billion revenue in 2024, faces compressed win margins.

Past performance leverage

Agencies weigh CPARS ratings and incumbency—Leidos reported $14.7 billion revenue in FY2024—yet buyers still extract concessions during option exercises and recompetes, which reset commercial terms. Missed SLAs can trigger contractually defined withholds and penalties tied to performance metrics. Strong past performance improves win probability but does not materially weaken federal buyer leverage.

Contract vehicles and modular buys

GWACs and IDIQs (for example Alliant 2 with a $50B ceiling) enable rapid tasking and switching among vendors, while modular open systems approaches reduce vendor lock-in and let agencies disaggregate work across multiple suppliers. Buyers can split scopes and award smaller task orders, increasing competition and elevating customer bargaining power against prime contractors like Leidos. This fragmentation amplifies price pressure and leverage in negotiations.

- GWAC/IDIQ scale: Alliant 2 $50B+

- Modularity lowers switching costs

- Disaggregation increases buyer leverage

Shift to outcomes and OTA

Outcome-based metrics shift delivery risk to vendors, forcing Leidos and peers to guarantee performance and absorb cost overruns; OTAs accelerate awards while keeping buyer options, prompting faster entry to competitions. Pilots and down-selects create bake-offs on capability and price, and vendors must invest upfront to win, strengthening buyer leverage.

- Outcome risk borne by vendors

- OTAs shorten cycles

- Pilots enable direct comparisons

- Upfront vendor investment increases buyer leverage

Federal buying power, GWACs and OTAs intensify price pressure and margin compression

Federal buyers (DoD FY2024 ~$858B) concentrate demand and wield strong price/contract leverage over Leidos (FY2024 revenue $14.7B; ~42,000 employees). GWACs/IDIQs (Alliant 2 $50B+) and modular contracting lower switching costs, intensifying price pressure and margin compression via LPTA, should-cost reviews and CPARS-based selections. Outcome-based metrics and OTAs shift risk to vendors, raising upfront investment and strengthening buyer bargaining power.

| Metric | Value (2024) |

|---|---|

| DoD budget | $858B |

| Leidos revenue | $14.7B |

| Employees | ~42,000 |

| Alliant 2 ceiling | $50B+ |

What You See Is What You Get

Leidos Porter's Five Forces Analysis

This Leidos Porter's Five Forces analysis offers a concise, professional assessment of competitive rivalry, buyer and supplier power, threat of entrants, and substitute pressures specific to Leidos' markets. You're looking at the actual document—once purchased you’ll get instant access to this exact file. It's fully formatted and ready for strategic use.