LeMaitre Vascular Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

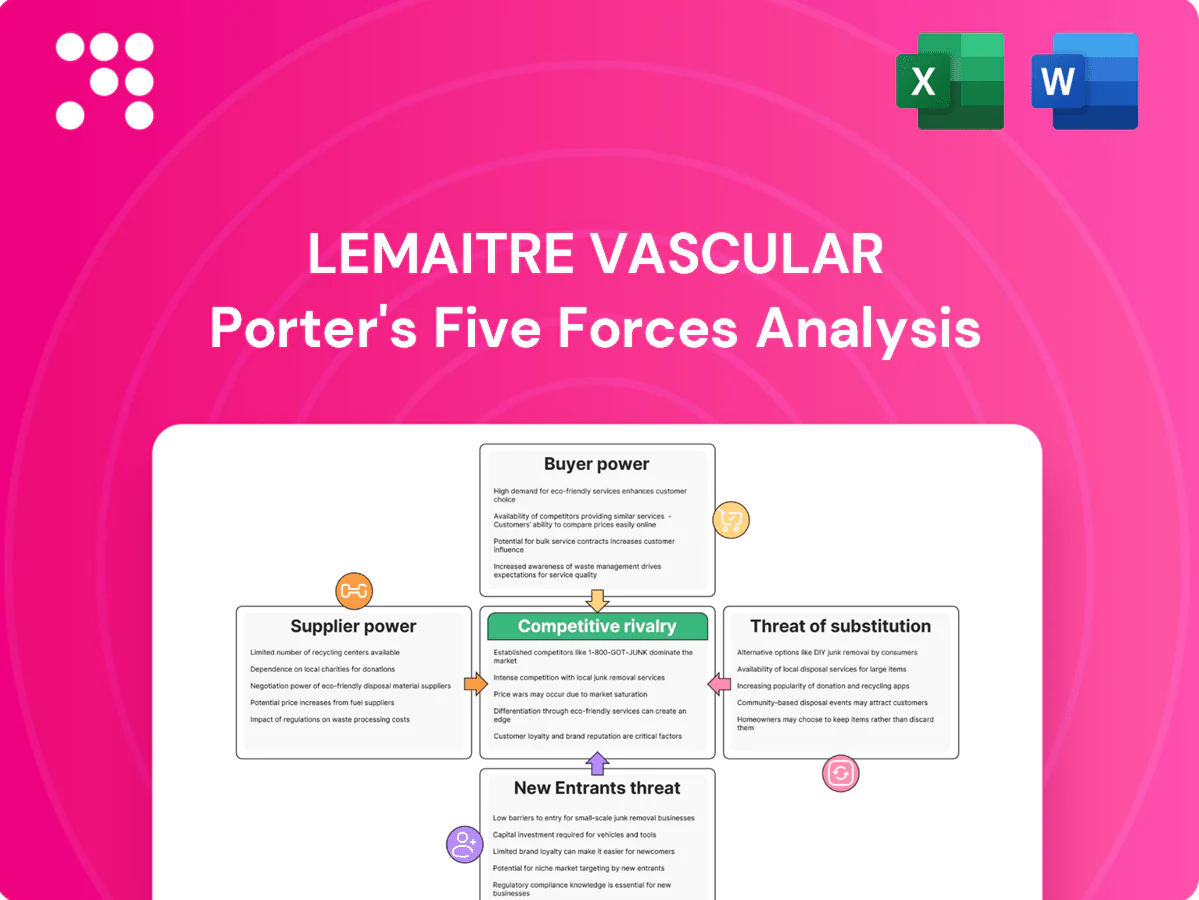

LeMaitre Vascular faces moderate supplier power, niche buyer dynamics, and evolving substitute risks driven by minimally invasive trends, while regulatory barriers and capital intensity temper new entrants—creating a nuanced competitive landscape. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Specialized biomaterials concentration

Core inputs such as ePTFE, polyester, nitinol and heparin coatings are supplied by a narrow pool of qualified vendors, increasing supplier leverage and price sensitivity. Any supplier disruption or quality lapse can stop production because strict device validation and traceability requirements mean replacements must be extensively requalified. Dual-sourcing and safety stocks reduce risk but add substantial qualification cost and inventory expense under regulatory constraints.

Regulatory revalidation switching costs

Changing a material or component in vascular devices typically triggers design changes, revalidation and regulatory filings, often adding 6–24 months and hundreds of thousands to millions of dollars in cost, which raises switching costs and strengthens supplier leverage. Hospitals and regulators demand documented equivalence, slowing transitions; suppliers exploit this to negotiate favorable terms, increasing their bargaining power over LeMaitre Vascular.

Sterilization and contract manufacturing bottlenecks

In 2024 third-party sterilizers and specialized contract manufacturers remained capacity constrained, giving a small set of approved sites scheduling and pricing power over LeMaitre Vascular supply chains. Lead-time volatility from bottlenecks has pushed device makers toward higher safety-stock levels and elevated working capital. Long-term volume commitments with vendors mitigate shortages but lock LeMaitre into reduced operational flexibility.

Quality and compliance criticality

- Compliance: ISO 13485 + FDA 21 CFR Part 820

- Financial exposure: 2024 net sales 124.0M USD

- Risk: audit failures → recalls

- Mitigation: supplier development requires sustained investment

Counter-leverage via scale and design

Standardizing platforms and designing for manufacturability broadens qualified sources and reduces unit cost; LeMaitre Vascular reported fiscal 2024 revenue of $162.4 million, enabling scale-based sourcing and negotiation. Volume bundling and multi-year contracts secure pricing and priority from suppliers, while early supplier involvement cuts post-approval change orders. Niche components, however, can remain single-source despite these levers.

- Scale: use volume to gain 3–10% supplier discounts

- Design: modular platforms widen qualified suppliers

- Contracts: multi-year deals lock priority

- Risk: specialty parts often stay single-source

High supplier power: narrow vendor pool, 6–24 month switches, $100k–$1M changeover

LeMaitre faces strong supplier bargaining power due to a narrow qualified vendor pool for ePTFE, nitinol and coatings, high switching costs (6–24 months, >$100k–$1M) and capacity-constrained CMOs in 2024. With reported 2024 net sales 124.0M USD and modular design/volume levers, the company secures 3–10% supplier discounts but specialty parts often remain single-source.

| Metric | Value (2024) |

|---|---|

| Net sales | 124.0M USD |

| Switching time | 6–24 months |

| Switching cost | $100k–$1M+ |

| Supplier discount | 3–10% |

| Risk | Single-source specialty parts |

What is included in the product

Tailored Porter’s Five Forces analysis for LeMaitre Vascular highlighting competitive rivalry, buyer/supplier power, substitution threats, and entry barriers shaping pricing and profit potential. Includes strategic insights on emerging disruptors and defensive positioning.

A single-sheet Porter's Five Forces for LeMaitre Vascular that clarifies competitive pressures—supplier/buyer power, substitutes, new entrants and rivalry—so teams can instantly spot strategic pain points and craft investor-ready responses for pricing, sourcing and M&A decisions.

Customers Bargaining Power

GPOs and IDNs price pressure

Large US IDNs and GPOs (over 95% hospital membership) force steep discounts and vendor standardization, pushing LeMaitre Vascular to accept ASP reductions often in the mid-teens; volume-based rebates commonly range 5–25%. National tenders outside the US intensify price competition, with some markets reporting price cuts up to 40%. Smaller hospitals piggyback on master agreements to capture near-identical pricing and scale benefits.

Surgeon preference vs formulary control

Vascular surgeons prioritize device performance and handling, which tempers a pure price focus and drives loyalty to proven platforms. Yet value-analysis committees and hospital formularies increasingly control procurement, and NASDAQ: LMAT (2024) must engage them to secure contracts. Demonstrated clinical outcomes and surgeon-training programs improve inclusion rates. Without clear differentiation, hospitals can switch to lower-cost alternatives.

Reimbursement and value-based care

Payers increasingly demand cost-effectiveness—Medicare Advantage enrollment surpassed 50% in 2024—putting pressure on device margins as reimbursement ties to value. Bundled payments and episode-based models make hospitals more sensitive to total episode cost and complication rates, raising buyer scrutiny. Devices that demonstrably cut OR time or reinterventions gain negotiating leverage, while weak health-economic evidence amplifies customer power.

Moderate switching costs in procedures

Once a kit or graft is standardized, clinical teams resist change because workflows, inventory and OR efficiency embed specific devices; many balloons and catheters remain partially commoditized so buyers can and do trial alternatives during tenders or shortages; targeted education and responsive service increase perceived switching costs, blunting customer bargaining power.

Global tender variability

Global tender variability raises customer bargaining power: EMEA/LatAm public tenders emphasize lowest bid, pressuring margins despite LeMaitre Vascular reporting roughly $119.7 million in 2024 revenue; U.S. private markets permit segmentation and bundling that recapture value. Currency swings in 2024 (notably EUR/USD volatility) shifted import pricing and procurement timing, while local distributors can buffer or amplify end-buyer leverage.

- EMEA/LatAm: lowest-bid tender pressure

- U.S.: segmentation/bundling preserves margin

- Currency swings: affect timing/pricing

- Distributors: buffer or amplify buyer power

Mid-teens ASP cuts, 5-25% rebates; tenders cut prices up to 40%; MA >50%

Large US IDNs/GPOs (95% hospital membership) push mid-teens ASP cuts and 5–25% volume rebates; national tenders drive up to 40% price declines. Surgeons' preference for proven platforms limits pure price switching, but formularies, bundled payments and Medicare Advantage >50% (2024) amplify buyer scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $119.7M |

| Rebates | 5–25% |

Preview Before You Purchase

LeMaitre Vascular Porter's Five Forces Analysis

This Porter's Five Forces analysis of LeMaitre Vascular evaluates supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants to illuminate strategic positioning and profitability drivers. The preview you see is the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to download.

Go Beyond the Preview—Access the Full Strategic Report

LeMaitre Vascular faces moderate supplier power, niche buyer dynamics, and evolving substitute risks driven by minimally invasive trends, while regulatory barriers and capital intensity temper new entrants—creating a nuanced competitive landscape. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Specialized biomaterials concentration

Core inputs such as ePTFE, polyester, nitinol and heparin coatings are supplied by a narrow pool of qualified vendors, increasing supplier leverage and price sensitivity. Any supplier disruption or quality lapse can stop production because strict device validation and traceability requirements mean replacements must be extensively requalified. Dual-sourcing and safety stocks reduce risk but add substantial qualification cost and inventory expense under regulatory constraints.

Regulatory revalidation switching costs

Changing a material or component in vascular devices typically triggers design changes, revalidation and regulatory filings, often adding 6–24 months and hundreds of thousands to millions of dollars in cost, which raises switching costs and strengthens supplier leverage. Hospitals and regulators demand documented equivalence, slowing transitions; suppliers exploit this to negotiate favorable terms, increasing their bargaining power over LeMaitre Vascular.

Sterilization and contract manufacturing bottlenecks

In 2024 third-party sterilizers and specialized contract manufacturers remained capacity constrained, giving a small set of approved sites scheduling and pricing power over LeMaitre Vascular supply chains. Lead-time volatility from bottlenecks has pushed device makers toward higher safety-stock levels and elevated working capital. Long-term volume commitments with vendors mitigate shortages but lock LeMaitre into reduced operational flexibility.

Quality and compliance criticality

- Compliance: ISO 13485 + FDA 21 CFR Part 820

- Financial exposure: 2024 net sales 124.0M USD

- Risk: audit failures → recalls

- Mitigation: supplier development requires sustained investment

Counter-leverage via scale and design

Standardizing platforms and designing for manufacturability broadens qualified sources and reduces unit cost; LeMaitre Vascular reported fiscal 2024 revenue of $162.4 million, enabling scale-based sourcing and negotiation. Volume bundling and multi-year contracts secure pricing and priority from suppliers, while early supplier involvement cuts post-approval change orders. Niche components, however, can remain single-source despite these levers.

- Scale: use volume to gain 3–10% supplier discounts

- Design: modular platforms widen qualified suppliers

- Contracts: multi-year deals lock priority

- Risk: specialty parts often stay single-source

High supplier power: narrow vendor pool, 6–24 month switches, $100k–$1M changeover

LeMaitre faces strong supplier bargaining power due to a narrow qualified vendor pool for ePTFE, nitinol and coatings, high switching costs (6–24 months, >$100k–$1M) and capacity-constrained CMOs in 2024. With reported 2024 net sales 124.0M USD and modular design/volume levers, the company secures 3–10% supplier discounts but specialty parts often remain single-source.

| Metric | Value (2024) |

|---|---|

| Net sales | 124.0M USD |

| Switching time | 6–24 months |

| Switching cost | $100k–$1M+ |

| Supplier discount | 3–10% |

| Risk | Single-source specialty parts |

What is included in the product

Tailored Porter’s Five Forces analysis for LeMaitre Vascular highlighting competitive rivalry, buyer/supplier power, substitution threats, and entry barriers shaping pricing and profit potential. Includes strategic insights on emerging disruptors and defensive positioning.

A single-sheet Porter's Five Forces for LeMaitre Vascular that clarifies competitive pressures—supplier/buyer power, substitutes, new entrants and rivalry—so teams can instantly spot strategic pain points and craft investor-ready responses for pricing, sourcing and M&A decisions.

Customers Bargaining Power

GPOs and IDNs price pressure

Large US IDNs and GPOs (over 95% hospital membership) force steep discounts and vendor standardization, pushing LeMaitre Vascular to accept ASP reductions often in the mid-teens; volume-based rebates commonly range 5–25%. National tenders outside the US intensify price competition, with some markets reporting price cuts up to 40%. Smaller hospitals piggyback on master agreements to capture near-identical pricing and scale benefits.

Surgeon preference vs formulary control

Vascular surgeons prioritize device performance and handling, which tempers a pure price focus and drives loyalty to proven platforms. Yet value-analysis committees and hospital formularies increasingly control procurement, and NASDAQ: LMAT (2024) must engage them to secure contracts. Demonstrated clinical outcomes and surgeon-training programs improve inclusion rates. Without clear differentiation, hospitals can switch to lower-cost alternatives.

Reimbursement and value-based care

Payers increasingly demand cost-effectiveness—Medicare Advantage enrollment surpassed 50% in 2024—putting pressure on device margins as reimbursement ties to value. Bundled payments and episode-based models make hospitals more sensitive to total episode cost and complication rates, raising buyer scrutiny. Devices that demonstrably cut OR time or reinterventions gain negotiating leverage, while weak health-economic evidence amplifies customer power.

Moderate switching costs in procedures

Once a kit or graft is standardized, clinical teams resist change because workflows, inventory and OR efficiency embed specific devices; many balloons and catheters remain partially commoditized so buyers can and do trial alternatives during tenders or shortages; targeted education and responsive service increase perceived switching costs, blunting customer bargaining power.

Global tender variability

Global tender variability raises customer bargaining power: EMEA/LatAm public tenders emphasize lowest bid, pressuring margins despite LeMaitre Vascular reporting roughly $119.7 million in 2024 revenue; U.S. private markets permit segmentation and bundling that recapture value. Currency swings in 2024 (notably EUR/USD volatility) shifted import pricing and procurement timing, while local distributors can buffer or amplify end-buyer leverage.

- EMEA/LatAm: lowest-bid tender pressure

- U.S.: segmentation/bundling preserves margin

- Currency swings: affect timing/pricing

- Distributors: buffer or amplify buyer power

Mid-teens ASP cuts, 5-25% rebates; tenders cut prices up to 40%; MA >50%

Large US IDNs/GPOs (95% hospital membership) push mid-teens ASP cuts and 5–25% volume rebates; national tenders drive up to 40% price declines. Surgeons' preference for proven platforms limits pure price switching, but formularies, bundled payments and Medicare Advantage >50% (2024) amplify buyer scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $119.7M |

| Rebates | 5–25% |

Preview Before You Purchase

LeMaitre Vascular Porter's Five Forces Analysis

This Porter's Five Forces analysis of LeMaitre Vascular evaluates supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants to illuminate strategic positioning and profitability drivers. The preview you see is the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to download.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

LeMaitre Vascular faces moderate supplier power, niche buyer dynamics, and evolving substitute risks driven by minimally invasive trends, while regulatory barriers and capital intensity temper new entrants—creating a nuanced competitive landscape. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications for investment and planning.

Suppliers Bargaining Power

Specialized biomaterials concentration

Core inputs such as ePTFE, polyester, nitinol and heparin coatings are supplied by a narrow pool of qualified vendors, increasing supplier leverage and price sensitivity. Any supplier disruption or quality lapse can stop production because strict device validation and traceability requirements mean replacements must be extensively requalified. Dual-sourcing and safety stocks reduce risk but add substantial qualification cost and inventory expense under regulatory constraints.

Regulatory revalidation switching costs

Changing a material or component in vascular devices typically triggers design changes, revalidation and regulatory filings, often adding 6–24 months and hundreds of thousands to millions of dollars in cost, which raises switching costs and strengthens supplier leverage. Hospitals and regulators demand documented equivalence, slowing transitions; suppliers exploit this to negotiate favorable terms, increasing their bargaining power over LeMaitre Vascular.

Sterilization and contract manufacturing bottlenecks

In 2024 third-party sterilizers and specialized contract manufacturers remained capacity constrained, giving a small set of approved sites scheduling and pricing power over LeMaitre Vascular supply chains. Lead-time volatility from bottlenecks has pushed device makers toward higher safety-stock levels and elevated working capital. Long-term volume commitments with vendors mitigate shortages but lock LeMaitre into reduced operational flexibility.

Quality and compliance criticality

- Compliance: ISO 13485 + FDA 21 CFR Part 820

- Financial exposure: 2024 net sales 124.0M USD

- Risk: audit failures → recalls

- Mitigation: supplier development requires sustained investment

Counter-leverage via scale and design

Standardizing platforms and designing for manufacturability broadens qualified sources and reduces unit cost; LeMaitre Vascular reported fiscal 2024 revenue of $162.4 million, enabling scale-based sourcing and negotiation. Volume bundling and multi-year contracts secure pricing and priority from suppliers, while early supplier involvement cuts post-approval change orders. Niche components, however, can remain single-source despite these levers.

- Scale: use volume to gain 3–10% supplier discounts

- Design: modular platforms widen qualified suppliers

- Contracts: multi-year deals lock priority

- Risk: specialty parts often stay single-source

High supplier power: narrow vendor pool, 6–24 month switches, $100k–$1M changeover

LeMaitre faces strong supplier bargaining power due to a narrow qualified vendor pool for ePTFE, nitinol and coatings, high switching costs (6–24 months, >$100k–$1M) and capacity-constrained CMOs in 2024. With reported 2024 net sales 124.0M USD and modular design/volume levers, the company secures 3–10% supplier discounts but specialty parts often remain single-source.

| Metric | Value (2024) |

|---|---|

| Net sales | 124.0M USD |

| Switching time | 6–24 months |

| Switching cost | $100k–$1M+ |

| Supplier discount | 3–10% |

| Risk | Single-source specialty parts |

What is included in the product

Tailored Porter’s Five Forces analysis for LeMaitre Vascular highlighting competitive rivalry, buyer/supplier power, substitution threats, and entry barriers shaping pricing and profit potential. Includes strategic insights on emerging disruptors and defensive positioning.

A single-sheet Porter's Five Forces for LeMaitre Vascular that clarifies competitive pressures—supplier/buyer power, substitutes, new entrants and rivalry—so teams can instantly spot strategic pain points and craft investor-ready responses for pricing, sourcing and M&A decisions.

Customers Bargaining Power

GPOs and IDNs price pressure

Large US IDNs and GPOs (over 95% hospital membership) force steep discounts and vendor standardization, pushing LeMaitre Vascular to accept ASP reductions often in the mid-teens; volume-based rebates commonly range 5–25%. National tenders outside the US intensify price competition, with some markets reporting price cuts up to 40%. Smaller hospitals piggyback on master agreements to capture near-identical pricing and scale benefits.

Surgeon preference vs formulary control

Vascular surgeons prioritize device performance and handling, which tempers a pure price focus and drives loyalty to proven platforms. Yet value-analysis committees and hospital formularies increasingly control procurement, and NASDAQ: LMAT (2024) must engage them to secure contracts. Demonstrated clinical outcomes and surgeon-training programs improve inclusion rates. Without clear differentiation, hospitals can switch to lower-cost alternatives.

Reimbursement and value-based care

Payers increasingly demand cost-effectiveness—Medicare Advantage enrollment surpassed 50% in 2024—putting pressure on device margins as reimbursement ties to value. Bundled payments and episode-based models make hospitals more sensitive to total episode cost and complication rates, raising buyer scrutiny. Devices that demonstrably cut OR time or reinterventions gain negotiating leverage, while weak health-economic evidence amplifies customer power.

Moderate switching costs in procedures

Once a kit or graft is standardized, clinical teams resist change because workflows, inventory and OR efficiency embed specific devices; many balloons and catheters remain partially commoditized so buyers can and do trial alternatives during tenders or shortages; targeted education and responsive service increase perceived switching costs, blunting customer bargaining power.

Global tender variability

Global tender variability raises customer bargaining power: EMEA/LatAm public tenders emphasize lowest bid, pressuring margins despite LeMaitre Vascular reporting roughly $119.7 million in 2024 revenue; U.S. private markets permit segmentation and bundling that recapture value. Currency swings in 2024 (notably EUR/USD volatility) shifted import pricing and procurement timing, while local distributors can buffer or amplify end-buyer leverage.

- EMEA/LatAm: lowest-bid tender pressure

- U.S.: segmentation/bundling preserves margin

- Currency swings: affect timing/pricing

- Distributors: buffer or amplify buyer power

Mid-teens ASP cuts, 5-25% rebates; tenders cut prices up to 40%; MA >50%

Large US IDNs/GPOs (95% hospital membership) push mid-teens ASP cuts and 5–25% volume rebates; national tenders drive up to 40% price declines. Surgeons' preference for proven platforms limits pure price switching, but formularies, bundled payments and Medicare Advantage >50% (2024) amplify buyer scrutiny.

| Metric | 2024 |

|---|---|

| Revenue | $119.7M |

| Rebates | 5–25% |

Preview Before You Purchase

LeMaitre Vascular Porter's Five Forces Analysis

This Porter's Five Forces analysis of LeMaitre Vascular evaluates supplier and buyer power, competitive rivalry, and threats of substitutes and new entrants to illuminate strategic positioning and profitability drivers. The preview you see is the exact document you'll receive immediately after purchase—no surprises, fully formatted and ready to download.