Lemonade Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

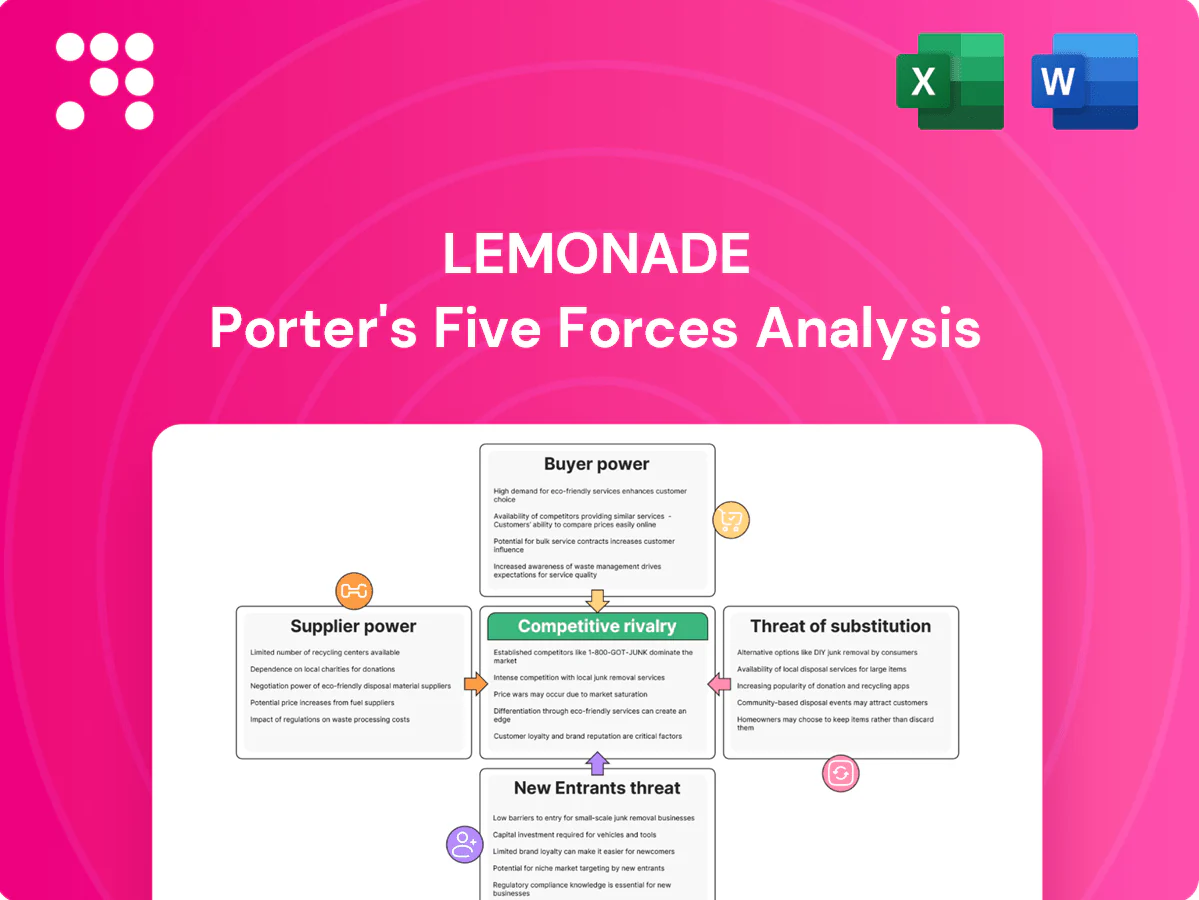

Lemonade's Porter's Five Forces snapshot highlights high buyer power, moderate supplier influence, a tangible threat from new insurtech entrants, and intensifying rivalry as incumbents digitize, while regulation and substitutes constrain margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lemonade’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated reinsurance capacity

Reinsurers supply risk capital and are relatively concentrated, with the top five global players providing about 50% of treaty capacity, giving them leverage on pricing and terms. Recent hard-market cycles produced double-digit reinsurance price increases in 2023–24, tightening capacity and raising ceding rates or attachment points. Lemonade can diversify panels, but high-quality A-rated capacity remains scarce. Dependence intensifies for catastrophe-prone homeowners and fast-growing personal lines.

Cloud and AI infrastructure

Lemonade depends on hyperscalers and ML tooling, creating technical lock-in and switching costs as AWS, Microsoft, and Google control roughly 65% of cloud market (AWS ~32%, Microsoft ~23%, Google ~10%). Vendor pricing on compute, storage and AI services materially affects cost structure; multi-cloud and optimization reduce exposure but performance, latency and compliance constraints limit flexibility. Outages or policy shifts can halt operations and spike costs.

Data and telematics partners

Third-party data (credit, property, driving, pet health) feeds Lemonade’s pricing and underwriting models, and while proprietary datasets can differentiate, many high-value signals still come from a few specialized vendors, concentrating supplier power. Access terms, API limits and usage pricing directly affect unit economics and loss-adjusted acquisition costs. Building in-house alternatives typically requires years and multimillion-dollar investment, making short-term dependence on suppliers likely in 2024.

Claims repair networks

Auto body shops, contractors and vet networks directly drive Lemonade’s auto claims costs and cycle times; concentrated local markets and technician shortages have pushed vendor rates higher and slowed turnaround. Preferred repair networks can cut leakage an estimated 10–20% but demand volume commitments; parts and service inflation (roughly 12% y/y in 2023) has amplified supplier bargaining power.

Payment and app ecosystems

Payment processors and app stores (Apple/Google: standard 30% cut, 15% for small developers in 2024) shape Lemonade’s distribution and cash flow through fees and rules; card fees (~1.5–3%) plus chargeback costs ($20–60 each) and fraud tools affect margins and working capital. Settlement timing (2–30 days) and platform policy shifts can quickly change CAC and servicing economics; redundancy reduces risk but compliance raises switching costs.

- Fees: app store 15–30%

- Card fees: 1.5–3%

- Chargeback cost: $20–60

- Settlement lag: 2–30 days

- Switching: high compliance burden

Reinsurers top-5 ~50%, cloud oligopoly ~65%, parts inflation ~12%

Reinsurers concentrated (top 5 ~50% treaty capacity) and 2023–24 reinsurance prices rose double digits, tightening capacity. Hyperscalers hold ~65% cloud (AWS 32%, Microsoft 23%, Google 10%), creating technical lock-in and cost risk. Third-party data, repair networks and parts inflation (~12% y/y 2023) plus app store fees (15–30%) raise supplier leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Reinsurers | Top‑5 share | ~50% |

| Cloud | Market share (AWS/MS/Google) | 32/23/10% |

| Parts | Inflation y/y | ~12% |

| App stores | Fees | 15–30% |

What is included in the product

Concise Porter's Five Forces review tailored to Lemonade, assessing competitive rivalry, buyer and supplier power, substitution risks, and entry barriers to reveal strategic vulnerabilities and growth levers. Ideal for investor briefings, strategy decks, or academic analysis to inform pricing, product positioning, and defensive moves.

A concise, one-sheet Porter's Five Forces for Lemonade that highlights competitive pressures, regulatory risks, supplier and buyer power, and threat of substitutes—ready to drop into decks or scenario models; customizable inputs and radar chart make shifting market conditions instantly actionable.

Customers Bargaining Power

Highly price-sensitive shoppers

Personal P&C buyers frequently compare quotes and will switch for modest savings; 2024 surveys show about 65% shop multiple carriers before buying. Online aggregators and instant-bind platforms have cut search costs, raising buyer leverage and shortening purchase cycles. Lemonade’s transparent pricing and AI-driven quotes improve retention, but time-limited discounts and bundle incentives still sway decisions; elasticity is higher in renters and auto than in homeowners.

Low switching costs

Digital policy issuance and cancellation make churn easy as customers can switch within minutes, and minimal contractual lock-in plus proration further reduce friction. Retention therefore hinges on claims experience, price stability and service speed; the US personal lines industry shows roughly 85% retention (≈15% annual churn). Loyalty programs and multi-line bundles partially offset switching by improving stickiness.

Limited buyer concentration

Individual Lemonade customers are fragmented, lowering structural bargaining power; however BrightLocal 2024 reports 86% of consumers read online reviews, so ratings amplify collective influence on brand. Negative claims experiences can cascade across platforms and review sites, rapidly affecting perception. In direct-to-consumer models like Lemonade, net promoter effects drive acquisition and churn, making social proof strategically critical.

Transparent product comparability

Transparent online comparability of standardized coverage terms and limits compresses differentiation and strengthens buyer negotiating power; 2024 McKinsey found about 70% of P&C buyers use digital quote channels. Behavioral design and Giveback boost emotional loyalty but must pair with competitive rates; add-ons and endorsements provide targeted uniqueness without broad protection gaps.

- Price pressure: digital comparison increases bargaining

- Emotional stickiness: Giveback offsets rate focus

- Product gaps: endorsements enable niche differentiation

Bundling expectations

Consumers increasingly expect multi-policy discounts and seamless cross-line servicing; incumbents use bundled offerings to lock in accounts and materially reduce churn. By 2024 Lemonade had expanded to five core product lines (renters, homeowners, pet, life, auto), improving competitive parity, but the absolute depth of discounts remains the deciding factor. Failure to match bundle economics elevates buyer leverage and price sensitivity.

- expectations: multi-policy discounts, seamless servicing

- incumbents: bundles lower churn, boost LTV

- Lemonade 2024: five core product lines

Buyers shop widely; 65% compare, 70% use digital quotes—service & bundles win

Buyers hold elevated leverage: 65% shop multiple carriers and ~70% use digital quotes (2024), compressing price and coverage differentiation. Low switching friction; industry retention ≈85% (15% churn) makes claims/service and bundles decisive. Lemonade’s five product lines and AI pricing improve stickiness but price sensitivity remains highest in renters/auto.

| Metric | 2024 |

|---|---|

| Shopped multiple carriers | 65% |

| Digital quote use | 70% |

| Industry retention | 85% (15% churn) |

| Lemonade product lines | 5 |

Same Document Delivered

Lemonade Porter's Five Forces Analysis

This preview shows the exact Lemonade Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable: complete, final, and available instantly after payment.

A Must-Have Tool for Decision-Makers

Lemonade's Porter's Five Forces snapshot highlights high buyer power, moderate supplier influence, a tangible threat from new insurtech entrants, and intensifying rivalry as incumbents digitize, while regulation and substitutes constrain margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lemonade’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated reinsurance capacity

Reinsurers supply risk capital and are relatively concentrated, with the top five global players providing about 50% of treaty capacity, giving them leverage on pricing and terms. Recent hard-market cycles produced double-digit reinsurance price increases in 2023–24, tightening capacity and raising ceding rates or attachment points. Lemonade can diversify panels, but high-quality A-rated capacity remains scarce. Dependence intensifies for catastrophe-prone homeowners and fast-growing personal lines.

Cloud and AI infrastructure

Lemonade depends on hyperscalers and ML tooling, creating technical lock-in and switching costs as AWS, Microsoft, and Google control roughly 65% of cloud market (AWS ~32%, Microsoft ~23%, Google ~10%). Vendor pricing on compute, storage and AI services materially affects cost structure; multi-cloud and optimization reduce exposure but performance, latency and compliance constraints limit flexibility. Outages or policy shifts can halt operations and spike costs.

Data and telematics partners

Third-party data (credit, property, driving, pet health) feeds Lemonade’s pricing and underwriting models, and while proprietary datasets can differentiate, many high-value signals still come from a few specialized vendors, concentrating supplier power. Access terms, API limits and usage pricing directly affect unit economics and loss-adjusted acquisition costs. Building in-house alternatives typically requires years and multimillion-dollar investment, making short-term dependence on suppliers likely in 2024.

Claims repair networks

Auto body shops, contractors and vet networks directly drive Lemonade’s auto claims costs and cycle times; concentrated local markets and technician shortages have pushed vendor rates higher and slowed turnaround. Preferred repair networks can cut leakage an estimated 10–20% but demand volume commitments; parts and service inflation (roughly 12% y/y in 2023) has amplified supplier bargaining power.

Payment and app ecosystems

Payment processors and app stores (Apple/Google: standard 30% cut, 15% for small developers in 2024) shape Lemonade’s distribution and cash flow through fees and rules; card fees (~1.5–3%) plus chargeback costs ($20–60 each) and fraud tools affect margins and working capital. Settlement timing (2–30 days) and platform policy shifts can quickly change CAC and servicing economics; redundancy reduces risk but compliance raises switching costs.

- Fees: app store 15–30%

- Card fees: 1.5–3%

- Chargeback cost: $20–60

- Settlement lag: 2–30 days

- Switching: high compliance burden

Reinsurers top-5 ~50%, cloud oligopoly ~65%, parts inflation ~12%

Reinsurers concentrated (top 5 ~50% treaty capacity) and 2023–24 reinsurance prices rose double digits, tightening capacity. Hyperscalers hold ~65% cloud (AWS 32%, Microsoft 23%, Google 10%), creating technical lock-in and cost risk. Third-party data, repair networks and parts inflation (~12% y/y 2023) plus app store fees (15–30%) raise supplier leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Reinsurers | Top‑5 share | ~50% |

| Cloud | Market share (AWS/MS/Google) | 32/23/10% |

| Parts | Inflation y/y | ~12% |

| App stores | Fees | 15–30% |

What is included in the product

Concise Porter's Five Forces review tailored to Lemonade, assessing competitive rivalry, buyer and supplier power, substitution risks, and entry barriers to reveal strategic vulnerabilities and growth levers. Ideal for investor briefings, strategy decks, or academic analysis to inform pricing, product positioning, and defensive moves.

A concise, one-sheet Porter's Five Forces for Lemonade that highlights competitive pressures, regulatory risks, supplier and buyer power, and threat of substitutes—ready to drop into decks or scenario models; customizable inputs and radar chart make shifting market conditions instantly actionable.

Customers Bargaining Power

Highly price-sensitive shoppers

Personal P&C buyers frequently compare quotes and will switch for modest savings; 2024 surveys show about 65% shop multiple carriers before buying. Online aggregators and instant-bind platforms have cut search costs, raising buyer leverage and shortening purchase cycles. Lemonade’s transparent pricing and AI-driven quotes improve retention, but time-limited discounts and bundle incentives still sway decisions; elasticity is higher in renters and auto than in homeowners.

Low switching costs

Digital policy issuance and cancellation make churn easy as customers can switch within minutes, and minimal contractual lock-in plus proration further reduce friction. Retention therefore hinges on claims experience, price stability and service speed; the US personal lines industry shows roughly 85% retention (≈15% annual churn). Loyalty programs and multi-line bundles partially offset switching by improving stickiness.

Limited buyer concentration

Individual Lemonade customers are fragmented, lowering structural bargaining power; however BrightLocal 2024 reports 86% of consumers read online reviews, so ratings amplify collective influence on brand. Negative claims experiences can cascade across platforms and review sites, rapidly affecting perception. In direct-to-consumer models like Lemonade, net promoter effects drive acquisition and churn, making social proof strategically critical.

Transparent product comparability

Transparent online comparability of standardized coverage terms and limits compresses differentiation and strengthens buyer negotiating power; 2024 McKinsey found about 70% of P&C buyers use digital quote channels. Behavioral design and Giveback boost emotional loyalty but must pair with competitive rates; add-ons and endorsements provide targeted uniqueness without broad protection gaps.

- Price pressure: digital comparison increases bargaining

- Emotional stickiness: Giveback offsets rate focus

- Product gaps: endorsements enable niche differentiation

Bundling expectations

Consumers increasingly expect multi-policy discounts and seamless cross-line servicing; incumbents use bundled offerings to lock in accounts and materially reduce churn. By 2024 Lemonade had expanded to five core product lines (renters, homeowners, pet, life, auto), improving competitive parity, but the absolute depth of discounts remains the deciding factor. Failure to match bundle economics elevates buyer leverage and price sensitivity.

- expectations: multi-policy discounts, seamless servicing

- incumbents: bundles lower churn, boost LTV

- Lemonade 2024: five core product lines

Buyers shop widely; 65% compare, 70% use digital quotes—service & bundles win

Buyers hold elevated leverage: 65% shop multiple carriers and ~70% use digital quotes (2024), compressing price and coverage differentiation. Low switching friction; industry retention ≈85% (15% churn) makes claims/service and bundles decisive. Lemonade’s five product lines and AI pricing improve stickiness but price sensitivity remains highest in renters/auto.

| Metric | 2024 |

|---|---|

| Shopped multiple carriers | 65% |

| Digital quote use | 70% |

| Industry retention | 85% (15% churn) |

| Lemonade product lines | 5 |

Same Document Delivered

Lemonade Porter's Five Forces Analysis

This preview shows the exact Lemonade Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable: complete, final, and available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lemonade's Porter's Five Forces snapshot highlights high buyer power, moderate supplier influence, a tangible threat from new insurtech entrants, and intensifying rivalry as incumbents digitize, while regulation and substitutes constrain margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lemonade’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated reinsurance capacity

Reinsurers supply risk capital and are relatively concentrated, with the top five global players providing about 50% of treaty capacity, giving them leverage on pricing and terms. Recent hard-market cycles produced double-digit reinsurance price increases in 2023–24, tightening capacity and raising ceding rates or attachment points. Lemonade can diversify panels, but high-quality A-rated capacity remains scarce. Dependence intensifies for catastrophe-prone homeowners and fast-growing personal lines.

Cloud and AI infrastructure

Lemonade depends on hyperscalers and ML tooling, creating technical lock-in and switching costs as AWS, Microsoft, and Google control roughly 65% of cloud market (AWS ~32%, Microsoft ~23%, Google ~10%). Vendor pricing on compute, storage and AI services materially affects cost structure; multi-cloud and optimization reduce exposure but performance, latency and compliance constraints limit flexibility. Outages or policy shifts can halt operations and spike costs.

Data and telematics partners

Third-party data (credit, property, driving, pet health) feeds Lemonade’s pricing and underwriting models, and while proprietary datasets can differentiate, many high-value signals still come from a few specialized vendors, concentrating supplier power. Access terms, API limits and usage pricing directly affect unit economics and loss-adjusted acquisition costs. Building in-house alternatives typically requires years and multimillion-dollar investment, making short-term dependence on suppliers likely in 2024.

Claims repair networks

Auto body shops, contractors and vet networks directly drive Lemonade’s auto claims costs and cycle times; concentrated local markets and technician shortages have pushed vendor rates higher and slowed turnaround. Preferred repair networks can cut leakage an estimated 10–20% but demand volume commitments; parts and service inflation (roughly 12% y/y in 2023) has amplified supplier bargaining power.

Payment and app ecosystems

Payment processors and app stores (Apple/Google: standard 30% cut, 15% for small developers in 2024) shape Lemonade’s distribution and cash flow through fees and rules; card fees (~1.5–3%) plus chargeback costs ($20–60 each) and fraud tools affect margins and working capital. Settlement timing (2–30 days) and platform policy shifts can quickly change CAC and servicing economics; redundancy reduces risk but compliance raises switching costs.

- Fees: app store 15–30%

- Card fees: 1.5–3%

- Chargeback cost: $20–60

- Settlement lag: 2–30 days

- Switching: high compliance burden

Reinsurers top-5 ~50%, cloud oligopoly ~65%, parts inflation ~12%

Reinsurers concentrated (top 5 ~50% treaty capacity) and 2023–24 reinsurance prices rose double digits, tightening capacity. Hyperscalers hold ~65% cloud (AWS 32%, Microsoft 23%, Google 10%), creating technical lock-in and cost risk. Third-party data, repair networks and parts inflation (~12% y/y 2023) plus app store fees (15–30%) raise supplier leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Reinsurers | Top‑5 share | ~50% |

| Cloud | Market share (AWS/MS/Google) | 32/23/10% |

| Parts | Inflation y/y | ~12% |

| App stores | Fees | 15–30% |

What is included in the product

Concise Porter's Five Forces review tailored to Lemonade, assessing competitive rivalry, buyer and supplier power, substitution risks, and entry barriers to reveal strategic vulnerabilities and growth levers. Ideal for investor briefings, strategy decks, or academic analysis to inform pricing, product positioning, and defensive moves.

A concise, one-sheet Porter's Five Forces for Lemonade that highlights competitive pressures, regulatory risks, supplier and buyer power, and threat of substitutes—ready to drop into decks or scenario models; customizable inputs and radar chart make shifting market conditions instantly actionable.

Customers Bargaining Power

Highly price-sensitive shoppers

Personal P&C buyers frequently compare quotes and will switch for modest savings; 2024 surveys show about 65% shop multiple carriers before buying. Online aggregators and instant-bind platforms have cut search costs, raising buyer leverage and shortening purchase cycles. Lemonade’s transparent pricing and AI-driven quotes improve retention, but time-limited discounts and bundle incentives still sway decisions; elasticity is higher in renters and auto than in homeowners.

Low switching costs

Digital policy issuance and cancellation make churn easy as customers can switch within minutes, and minimal contractual lock-in plus proration further reduce friction. Retention therefore hinges on claims experience, price stability and service speed; the US personal lines industry shows roughly 85% retention (≈15% annual churn). Loyalty programs and multi-line bundles partially offset switching by improving stickiness.

Limited buyer concentration

Individual Lemonade customers are fragmented, lowering structural bargaining power; however BrightLocal 2024 reports 86% of consumers read online reviews, so ratings amplify collective influence on brand. Negative claims experiences can cascade across platforms and review sites, rapidly affecting perception. In direct-to-consumer models like Lemonade, net promoter effects drive acquisition and churn, making social proof strategically critical.

Transparent product comparability

Transparent online comparability of standardized coverage terms and limits compresses differentiation and strengthens buyer negotiating power; 2024 McKinsey found about 70% of P&C buyers use digital quote channels. Behavioral design and Giveback boost emotional loyalty but must pair with competitive rates; add-ons and endorsements provide targeted uniqueness without broad protection gaps.

- Price pressure: digital comparison increases bargaining

- Emotional stickiness: Giveback offsets rate focus

- Product gaps: endorsements enable niche differentiation

Bundling expectations

Consumers increasingly expect multi-policy discounts and seamless cross-line servicing; incumbents use bundled offerings to lock in accounts and materially reduce churn. By 2024 Lemonade had expanded to five core product lines (renters, homeowners, pet, life, auto), improving competitive parity, but the absolute depth of discounts remains the deciding factor. Failure to match bundle economics elevates buyer leverage and price sensitivity.

- expectations: multi-policy discounts, seamless servicing

- incumbents: bundles lower churn, boost LTV

- Lemonade 2024: five core product lines

Buyers shop widely; 65% compare, 70% use digital quotes—service & bundles win

Buyers hold elevated leverage: 65% shop multiple carriers and ~70% use digital quotes (2024), compressing price and coverage differentiation. Low switching friction; industry retention ≈85% (15% churn) makes claims/service and bundles decisive. Lemonade’s five product lines and AI pricing improve stickiness but price sensitivity remains highest in renters/auto.

| Metric | 2024 |

|---|---|

| Shopped multiple carriers | 65% |

| Digital quote use | 70% |

| Industry retention | 85% (15% churn) |

| Lemonade product lines | 5 |

Same Document Delivered

Lemonade Porter's Five Forces Analysis

This preview shows the exact Lemonade Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable: complete, final, and available instantly after payment.