Lenovo Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and rapid tech innovation are reshaping Lenovo Group’s strategic landscape in our concise PESTLE overview. This snapshot highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to access detailed, actionable insights and ready-to-use analysis.

Political factors

Geopolitical tensions and trade controls

US–China tensions and export controls, tightened since 2022 to curb shipments of advanced AI chips and tooling, constrain Lenovo’s access to key components and some markets. Sanctions, entity lists and licensing regimes can abruptly disrupt product roadmaps and supply lines. As the world’s largest PC vendor with about 24% share in 2024 (IDC), Lenovo must diversify sourcing and redesign around restricted components. Proactive compliance, licensing strategies and diplomatic engagement mitigate sudden shocks.

Tariffs, localization, and industrial policy

Shifting tariffs, including US Section 301 duties on about $370bn of Chinese goods and variable local content rules, alter unit costs and drive plant placement decisions. Incentives such as the US CHIPS Act ($52bn) and India’s IT hardware PLI (₹17,000 crore) push Lenovo capex toward onshore manufacturing in the US, EU, India and ASEAN (Vietnam FDI ~ $28bn in 2023). By localizing assembly and forming joint ventures Lenovo can capture policy tailwinds; misalignment raises landed costs and extends delivery by weeks.

Government procurement and national security

Public-sector IT spending represents a major addressable market for Lenovo but procurement is highly sensitive to security vetting, making country-of-origin and supply-chain assurances decisive for contract eligibility.

Restrictions on vendors from certain countries can bar participation in critical bids, while formal certification and trusted-partner programs (eg. government-approved vendor lists) unlock substantial institutional demand.

Providing clear, auditable security documentation and third-party attestations builds credibility with regulators and procurement officers, improving Lenovo’s win rates in national-security-sensitive tenders.

Emerging market political stability

Lenovo operates in 180+ markets and maintains manufacturing and service hubs across China, Vietnam, India and Mexico, exposing it to varying governance and stability; political unrest can disrupt facilities, logistics and sales, as seen in regional shutdowns that affected supply chains in 2023–24. Insurance, dual sourcing and regional hubs reduce exposure, while scenario planning guides resilient inventory and service-team allocation aligned with FY2024 operational priorities.

- Markets: 180+

- Hubs: China, Vietnam, India, Mexico

- Mitigants: insurance, dual sourcing, regional hubs

- Resilience: scenario-based inventory & service allocation

Standards and digital sovereignty agendas

Governments push domestic standards, cloud sovereignty and data residency—GDPR covers 27 EU states and China enforces strict data residency under its Cybersecurity Law—while over 100 countries now consider localization rules. Lenovo’s modular servers and software stacks can interoperate with mandated frameworks, and early engagement with ISO/NIST/ETSI lowers compliance friction and go-to-market delays.

- Tag: standards

- Tag: data residency

- Tag: cloud sovereignty

- Tag: modularity

- Tag: standards bodies

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Geopolitical tensions and export controls since 2022 restrict Lenovo’s access to advanced chips, impacting product roadmaps; Lenovo holds ~24% PC share (IDC 2024). Tariffs, US Section 301 on ~$370bn and incentives like CHIPS $52bn and India PLI ₹17,000 crore shift capex to US/EU/India/ASEAN (Vietnam FDI ~$28bn 2023). Public procurement needs strict supply‑chain provenance across 180+ markets and hubs in China, Vietnam, India, Mexico.

| Metric | Value |

|---|---|

| PC market share (2024) | 24% (IDC) |

| US Section 301 scope | $370bn |

| CHIPS Act | $52bn |

| India PLI | ₹17,000 crore |

| Vietnam FDI 2023 | $28bn |

| Markets / Hubs | 180+ / China, Vietnam, India, Mexico |

What is included in the product

Explores how macro-environmental factors uniquely affect Lenovo Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trend analysis. Designed to help executives, investors and strategists identify actionable threats and opportunities for scenario planning.

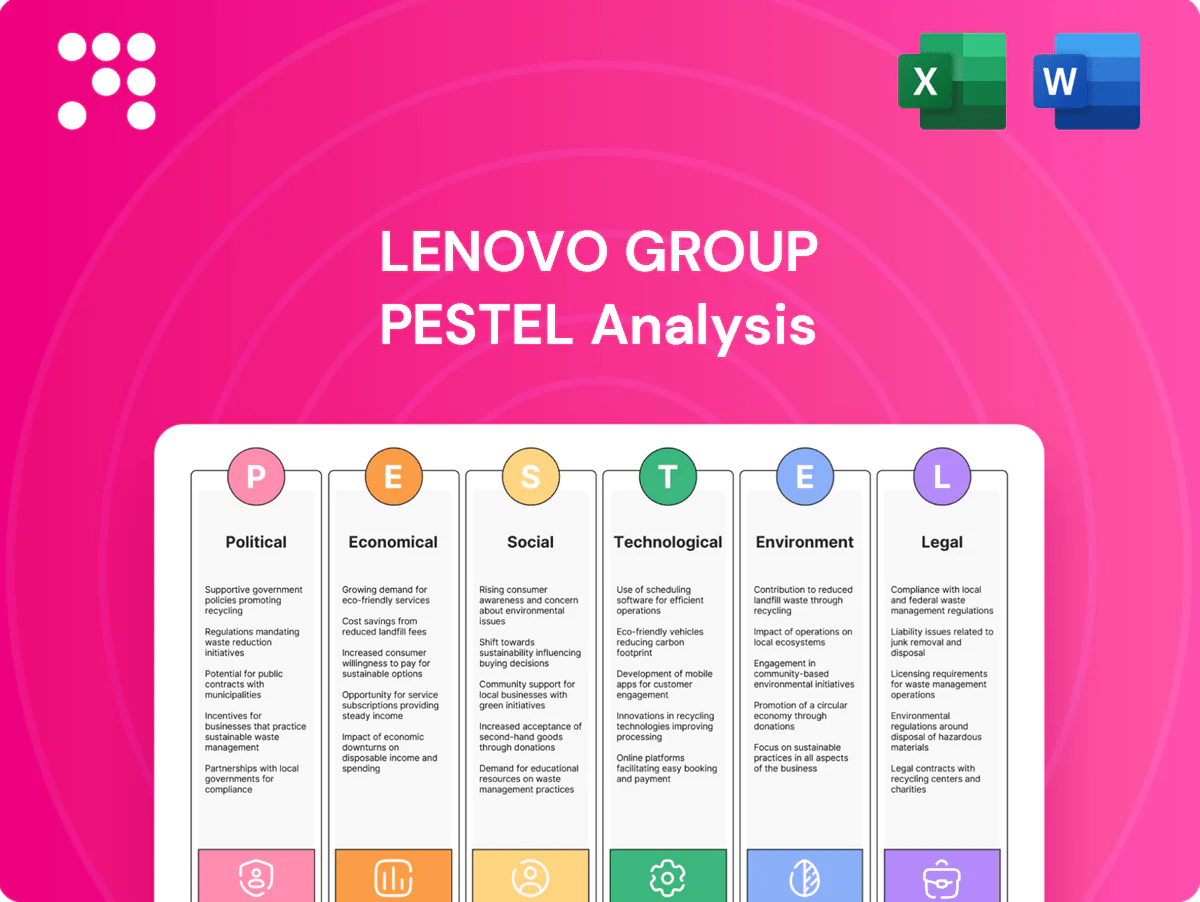

Visually segmented by PESTEL categories, the Lenovo Group PESTLE Analysis enables quick interpretation at a glance and seamless insertion into presentations or planning sessions. It simplifies external risk assessment and market positioning to align teams swiftly during strategic discussions.

Economic factors

PC demand cyclicality and refresh cycles

PC and tablet demand remains cyclical, swinging with macro conditions and post‑pandemic refresh waves; Lenovo held approximately 24% of the global PC market in 2024 (IDC), exposing revenues to these cycles. Enterprise refreshes, Windows transitions and rising AI‑PC adoption are lifting ASPs and supporting upgrade demand. Inventory discipline in downturns preserved margins, while flexible pricing and bundled services stabilize utilization and sell‑through.

Enterprise IT and cloud capex

Data center and edge investments underpin Lenovo’s server and storage growth, with Data Center Group revenue about US$10.2bn in FY2024 as enterprises build out capacity for AI and edge use cases. AI workload build-outs pushed demand for high-density designs, with IDC reporting AI-optimized server shipments rose ~45% YoY in 2024. Budget freezes or shifts to hyperscale cloud services pressure on-prem mix as Gartner noted enterprise cloud spending climbed ~18% in 2024, while service attach and financing programs smooth revenue volatility by expanding recurring-income streams.

Currency fluctuations and cost inflation

Lenovo’s multi-currency revenues and USD-denominated components create tangible FX risk as the dollar strengthened through 2022–24, pressuring reported margins. Freight and energy cost swings plus memory price cycles (PC shipments fell ~12% in 2023 per IDC) materially affect COGS, while hedging programs and dynamic BOM management have protected gross margin. Regional pricing adjustments preserve competitiveness across markets.

Emerging market growth and affordability

Supply chain resilience and lead times

Supply chain disruptions from pandemics, conflicts, and port congestion can sharply extend lead times for Lenovo, impacting its FY2024 global revenue of US$66.7bn; multi-geo manufacturing and component dual sourcing across ~30 countries reduce single-point risk. Nearshoring shortens cycle times for priority markets, while visibility tools improve inventory turns and fulfillment accuracy.

- Disruption drivers: pandemics, conflicts, port congestion

- Mitigation: multi-geo manufacturing, dual sourcing

- Nearshoring: shorter cycles for key markets

- Tech: visibility tools boost inventory turns

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Lenovo faces cyclical PC demand (24% global share, IDC 2024) and rising ASPs from AI‑PC upgrades; FY2024 revenue was US$66.7bn. Data Center Group drove growth (US$10.2bn FY2024) as AI‑optimized server shipments rose ~45% YoY (2024); enterprise cloud spend +18% (Gartner 2024) shifts on‑prem mix. FX, memory and freight volatility pressure margins, mitigated by hedging and multi‑geo sourcing.

| Metric | Value (2024) |

|---|---|

| Revenue (FY2024) | US$66.7bn |

| PC market share | ~24% (IDC) |

| DCG revenue | US$10.2bn |

| AI server growth | ~+45% YoY |

| Enterprise cloud spend | +18% YoY |

Preview Before You Purchase

Lenovo Group PESTLE Analysis

This Lenovo Group PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides concise political, economic, social, technological, legal, and environmental insights tailored to Lenovo’s strategy and risks. No placeholders or teasers—what you see is the final, downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and rapid tech innovation are reshaping Lenovo Group’s strategic landscape in our concise PESTLE overview. This snapshot highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to access detailed, actionable insights and ready-to-use analysis.

Political factors

Geopolitical tensions and trade controls

US–China tensions and export controls, tightened since 2022 to curb shipments of advanced AI chips and tooling, constrain Lenovo’s access to key components and some markets. Sanctions, entity lists and licensing regimes can abruptly disrupt product roadmaps and supply lines. As the world’s largest PC vendor with about 24% share in 2024 (IDC), Lenovo must diversify sourcing and redesign around restricted components. Proactive compliance, licensing strategies and diplomatic engagement mitigate sudden shocks.

Tariffs, localization, and industrial policy

Shifting tariffs, including US Section 301 duties on about $370bn of Chinese goods and variable local content rules, alter unit costs and drive plant placement decisions. Incentives such as the US CHIPS Act ($52bn) and India’s IT hardware PLI (₹17,000 crore) push Lenovo capex toward onshore manufacturing in the US, EU, India and ASEAN (Vietnam FDI ~ $28bn in 2023). By localizing assembly and forming joint ventures Lenovo can capture policy tailwinds; misalignment raises landed costs and extends delivery by weeks.

Government procurement and national security

Public-sector IT spending represents a major addressable market for Lenovo but procurement is highly sensitive to security vetting, making country-of-origin and supply-chain assurances decisive for contract eligibility.

Restrictions on vendors from certain countries can bar participation in critical bids, while formal certification and trusted-partner programs (eg. government-approved vendor lists) unlock substantial institutional demand.

Providing clear, auditable security documentation and third-party attestations builds credibility with regulators and procurement officers, improving Lenovo’s win rates in national-security-sensitive tenders.

Emerging market political stability

Lenovo operates in 180+ markets and maintains manufacturing and service hubs across China, Vietnam, India and Mexico, exposing it to varying governance and stability; political unrest can disrupt facilities, logistics and sales, as seen in regional shutdowns that affected supply chains in 2023–24. Insurance, dual sourcing and regional hubs reduce exposure, while scenario planning guides resilient inventory and service-team allocation aligned with FY2024 operational priorities.

- Markets: 180+

- Hubs: China, Vietnam, India, Mexico

- Mitigants: insurance, dual sourcing, regional hubs

- Resilience: scenario-based inventory & service allocation

Standards and digital sovereignty agendas

Governments push domestic standards, cloud sovereignty and data residency—GDPR covers 27 EU states and China enforces strict data residency under its Cybersecurity Law—while over 100 countries now consider localization rules. Lenovo’s modular servers and software stacks can interoperate with mandated frameworks, and early engagement with ISO/NIST/ETSI lowers compliance friction and go-to-market delays.

- Tag: standards

- Tag: data residency

- Tag: cloud sovereignty

- Tag: modularity

- Tag: standards bodies

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Geopolitical tensions and export controls since 2022 restrict Lenovo’s access to advanced chips, impacting product roadmaps; Lenovo holds ~24% PC share (IDC 2024). Tariffs, US Section 301 on ~$370bn and incentives like CHIPS $52bn and India PLI ₹17,000 crore shift capex to US/EU/India/ASEAN (Vietnam FDI ~$28bn 2023). Public procurement needs strict supply‑chain provenance across 180+ markets and hubs in China, Vietnam, India, Mexico.

| Metric | Value |

|---|---|

| PC market share (2024) | 24% (IDC) |

| US Section 301 scope | $370bn |

| CHIPS Act | $52bn |

| India PLI | ₹17,000 crore |

| Vietnam FDI 2023 | $28bn |

| Markets / Hubs | 180+ / China, Vietnam, India, Mexico |

What is included in the product

Explores how macro-environmental factors uniquely affect Lenovo Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trend analysis. Designed to help executives, investors and strategists identify actionable threats and opportunities for scenario planning.

Visually segmented by PESTEL categories, the Lenovo Group PESTLE Analysis enables quick interpretation at a glance and seamless insertion into presentations or planning sessions. It simplifies external risk assessment and market positioning to align teams swiftly during strategic discussions.

Economic factors

PC demand cyclicality and refresh cycles

PC and tablet demand remains cyclical, swinging with macro conditions and post‑pandemic refresh waves; Lenovo held approximately 24% of the global PC market in 2024 (IDC), exposing revenues to these cycles. Enterprise refreshes, Windows transitions and rising AI‑PC adoption are lifting ASPs and supporting upgrade demand. Inventory discipline in downturns preserved margins, while flexible pricing and bundled services stabilize utilization and sell‑through.

Enterprise IT and cloud capex

Data center and edge investments underpin Lenovo’s server and storage growth, with Data Center Group revenue about US$10.2bn in FY2024 as enterprises build out capacity for AI and edge use cases. AI workload build-outs pushed demand for high-density designs, with IDC reporting AI-optimized server shipments rose ~45% YoY in 2024. Budget freezes or shifts to hyperscale cloud services pressure on-prem mix as Gartner noted enterprise cloud spending climbed ~18% in 2024, while service attach and financing programs smooth revenue volatility by expanding recurring-income streams.

Currency fluctuations and cost inflation

Lenovo’s multi-currency revenues and USD-denominated components create tangible FX risk as the dollar strengthened through 2022–24, pressuring reported margins. Freight and energy cost swings plus memory price cycles (PC shipments fell ~12% in 2023 per IDC) materially affect COGS, while hedging programs and dynamic BOM management have protected gross margin. Regional pricing adjustments preserve competitiveness across markets.

Emerging market growth and affordability

Supply chain resilience and lead times

Supply chain disruptions from pandemics, conflicts, and port congestion can sharply extend lead times for Lenovo, impacting its FY2024 global revenue of US$66.7bn; multi-geo manufacturing and component dual sourcing across ~30 countries reduce single-point risk. Nearshoring shortens cycle times for priority markets, while visibility tools improve inventory turns and fulfillment accuracy.

- Disruption drivers: pandemics, conflicts, port congestion

- Mitigation: multi-geo manufacturing, dual sourcing

- Nearshoring: shorter cycles for key markets

- Tech: visibility tools boost inventory turns

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Lenovo faces cyclical PC demand (24% global share, IDC 2024) and rising ASPs from AI‑PC upgrades; FY2024 revenue was US$66.7bn. Data Center Group drove growth (US$10.2bn FY2024) as AI‑optimized server shipments rose ~45% YoY (2024); enterprise cloud spend +18% (Gartner 2024) shifts on‑prem mix. FX, memory and freight volatility pressure margins, mitigated by hedging and multi‑geo sourcing.

| Metric | Value (2024) |

|---|---|

| Revenue (FY2024) | US$66.7bn |

| PC market share | ~24% (IDC) |

| DCG revenue | US$10.2bn |

| AI server growth | ~+45% YoY |

| Enterprise cloud spend | +18% YoY |

Preview Before You Purchase

Lenovo Group PESTLE Analysis

This Lenovo Group PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides concise political, economic, social, technological, legal, and environmental insights tailored to Lenovo’s strategy and risks. No placeholders or teasers—what you see is the final, downloadable file.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic trends, and rapid tech innovation are reshaping Lenovo Group’s strategic landscape in our concise PESTLE overview. This snapshot highlights risks and opportunities for investors and strategists. Purchase the full PESTLE to access detailed, actionable insights and ready-to-use analysis.

Political factors

Geopolitical tensions and trade controls

US–China tensions and export controls, tightened since 2022 to curb shipments of advanced AI chips and tooling, constrain Lenovo’s access to key components and some markets. Sanctions, entity lists and licensing regimes can abruptly disrupt product roadmaps and supply lines. As the world’s largest PC vendor with about 24% share in 2024 (IDC), Lenovo must diversify sourcing and redesign around restricted components. Proactive compliance, licensing strategies and diplomatic engagement mitigate sudden shocks.

Tariffs, localization, and industrial policy

Shifting tariffs, including US Section 301 duties on about $370bn of Chinese goods and variable local content rules, alter unit costs and drive plant placement decisions. Incentives such as the US CHIPS Act ($52bn) and India’s IT hardware PLI (₹17,000 crore) push Lenovo capex toward onshore manufacturing in the US, EU, India and ASEAN (Vietnam FDI ~ $28bn in 2023). By localizing assembly and forming joint ventures Lenovo can capture policy tailwinds; misalignment raises landed costs and extends delivery by weeks.

Government procurement and national security

Public-sector IT spending represents a major addressable market for Lenovo but procurement is highly sensitive to security vetting, making country-of-origin and supply-chain assurances decisive for contract eligibility.

Restrictions on vendors from certain countries can bar participation in critical bids, while formal certification and trusted-partner programs (eg. government-approved vendor lists) unlock substantial institutional demand.

Providing clear, auditable security documentation and third-party attestations builds credibility with regulators and procurement officers, improving Lenovo’s win rates in national-security-sensitive tenders.

Emerging market political stability

Lenovo operates in 180+ markets and maintains manufacturing and service hubs across China, Vietnam, India and Mexico, exposing it to varying governance and stability; political unrest can disrupt facilities, logistics and sales, as seen in regional shutdowns that affected supply chains in 2023–24. Insurance, dual sourcing and regional hubs reduce exposure, while scenario planning guides resilient inventory and service-team allocation aligned with FY2024 operational priorities.

- Markets: 180+

- Hubs: China, Vietnam, India, Mexico

- Mitigants: insurance, dual sourcing, regional hubs

- Resilience: scenario-based inventory & service allocation

Standards and digital sovereignty agendas

Governments push domestic standards, cloud sovereignty and data residency—GDPR covers 27 EU states and China enforces strict data residency under its Cybersecurity Law—while over 100 countries now consider localization rules. Lenovo’s modular servers and software stacks can interoperate with mandated frameworks, and early engagement with ISO/NIST/ETSI lowers compliance friction and go-to-market delays.

- Tag: standards

- Tag: data residency

- Tag: cloud sovereignty

- Tag: modularity

- Tag: standards bodies

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Geopolitical tensions and export controls since 2022 restrict Lenovo’s access to advanced chips, impacting product roadmaps; Lenovo holds ~24% PC share (IDC 2024). Tariffs, US Section 301 on ~$370bn and incentives like CHIPS $52bn and India PLI ₹17,000 crore shift capex to US/EU/India/ASEAN (Vietnam FDI ~$28bn 2023). Public procurement needs strict supply‑chain provenance across 180+ markets and hubs in China, Vietnam, India, Mexico.

| Metric | Value |

|---|---|

| PC market share (2024) | 24% (IDC) |

| US Section 301 scope | $370bn |

| CHIPS Act | $52bn |

| India PLI | ₹17,000 crore |

| Vietnam FDI 2023 | $28bn |

| Markets / Hubs | 180+ / China, Vietnam, India, Mexico |

What is included in the product

Explores how macro-environmental factors uniquely affect Lenovo Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and trend analysis. Designed to help executives, investors and strategists identify actionable threats and opportunities for scenario planning.

Visually segmented by PESTEL categories, the Lenovo Group PESTLE Analysis enables quick interpretation at a glance and seamless insertion into presentations or planning sessions. It simplifies external risk assessment and market positioning to align teams swiftly during strategic discussions.

Economic factors

PC demand cyclicality and refresh cycles

PC and tablet demand remains cyclical, swinging with macro conditions and post‑pandemic refresh waves; Lenovo held approximately 24% of the global PC market in 2024 (IDC), exposing revenues to these cycles. Enterprise refreshes, Windows transitions and rising AI‑PC adoption are lifting ASPs and supporting upgrade demand. Inventory discipline in downturns preserved margins, while flexible pricing and bundled services stabilize utilization and sell‑through.

Enterprise IT and cloud capex

Data center and edge investments underpin Lenovo’s server and storage growth, with Data Center Group revenue about US$10.2bn in FY2024 as enterprises build out capacity for AI and edge use cases. AI workload build-outs pushed demand for high-density designs, with IDC reporting AI-optimized server shipments rose ~45% YoY in 2024. Budget freezes or shifts to hyperscale cloud services pressure on-prem mix as Gartner noted enterprise cloud spending climbed ~18% in 2024, while service attach and financing programs smooth revenue volatility by expanding recurring-income streams.

Currency fluctuations and cost inflation

Lenovo’s multi-currency revenues and USD-denominated components create tangible FX risk as the dollar strengthened through 2022–24, pressuring reported margins. Freight and energy cost swings plus memory price cycles (PC shipments fell ~12% in 2023 per IDC) materially affect COGS, while hedging programs and dynamic BOM management have protected gross margin. Regional pricing adjustments preserve competitiveness across markets.

Emerging market growth and affordability

Supply chain resilience and lead times

Supply chain disruptions from pandemics, conflicts, and port congestion can sharply extend lead times for Lenovo, impacting its FY2024 global revenue of US$66.7bn; multi-geo manufacturing and component dual sourcing across ~30 countries reduce single-point risk. Nearshoring shortens cycle times for priority markets, while visibility tools improve inventory turns and fulfillment accuracy.

- Disruption drivers: pandemics, conflicts, port congestion

- Mitigation: multi-geo manufacturing, dual sourcing

- Nearshoring: shorter cycles for key markets

- Tech: visibility tools boost inventory turns

Export curbs since 2022 limit chips; PC share ~24%; capex to US/EU/India

Lenovo faces cyclical PC demand (24% global share, IDC 2024) and rising ASPs from AI‑PC upgrades; FY2024 revenue was US$66.7bn. Data Center Group drove growth (US$10.2bn FY2024) as AI‑optimized server shipments rose ~45% YoY (2024); enterprise cloud spend +18% (Gartner 2024) shifts on‑prem mix. FX, memory and freight volatility pressure margins, mitigated by hedging and multi‑geo sourcing.

| Metric | Value (2024) |

|---|---|

| Revenue (FY2024) | US$66.7bn |

| PC market share | ~24% (IDC) |

| DCG revenue | US$10.2bn |

| AI server growth | ~+45% YoY |

| Enterprise cloud spend | +18% YoY |

Preview Before You Purchase

Lenovo Group PESTLE Analysis

This Lenovo Group PESTLE Analysis preview is the exact document you’ll receive after purchase—fully formatted and ready to use. It provides concise political, economic, social, technological, legal, and environmental insights tailored to Lenovo’s strategy and risks. No placeholders or teasers—what you see is the final, downloadable file.