Leong Hup International Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Leong Hup International faces intense supplier consolidation, evolving buyer expectations, and rising substitute protein threats that shape its strategic outlook. This snapshot teases force-by-force impacts but omits granular ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to gain a consultant-grade breakdown and equip your investment or strategy decisions with data-driven insight.

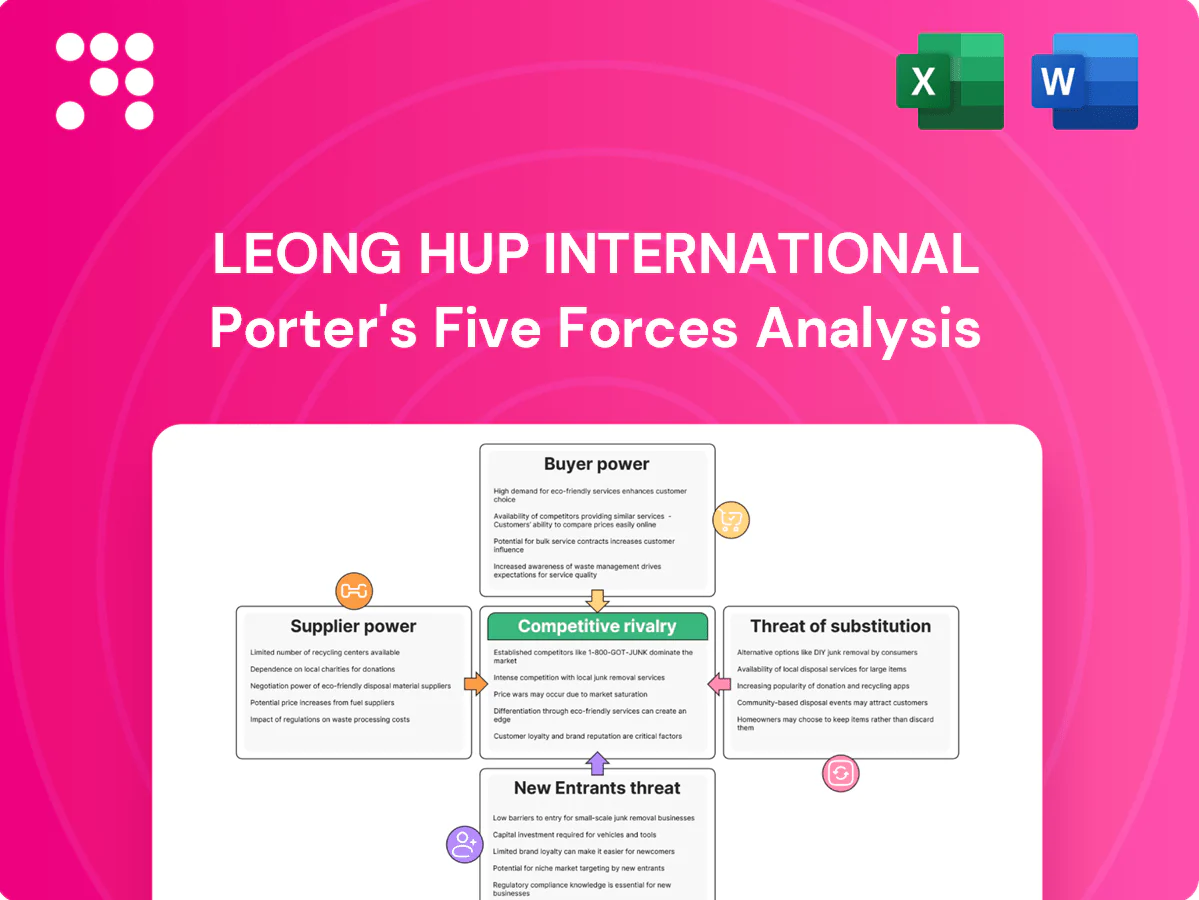

Suppliers Bargaining Power

Dependence on imported grains

Maize and soybean meal are largely imported for Leong Hup (over 60% of regional feed needs), exposing feed costs to 2024 global commodity cycles and FX swings; 2024 average CME corn ~ $5.20/bu (~$205/ton) and soybean meal ~ $420/ton amplified cost pass-through. A handful of global traders concentrate supply, boosting supplier leverage in tight markets. Hedging and diverse sourcing reduce but do not eliminate volatility; vertical integration into feed milling improves conversion efficiency but offers no control over raw grain prices.

Concentrated animal health and genetics

Vaccine, veterinary pharma and breeder genetics are concentrated: in 2024 the top three veterinary pharma players (Zoetis, Elanco, Merck Animal Health) control roughly 50–60% of the global market, while leading broiler breeders dominate supply chains. Switching is limited by biosecurity, performance data and regulatory approvals, enabling price increases and strict contract terms; long-term supply agreements reduce disruption risk but heighten dependence.

Energy, packaging, and cold-chain inputs

Electricity, LPG, diesel and packaging are core inputs with few substitutes, giving suppliers situational leverage as energy price spikes (Brent crude averaged about 86 USD/bbl in 2024) only pass through imperfectly in competitive markets; cold-chain equipment and refrigerants bind firms to specialized vendors, while efficiency and on-site generation programs (requiring capex) can lower exposure but lengthen payback periods.

Logistics and port congestion exposure

Import reliance makes Leong Hup vulnerable to shipping rates, container availability and port bottlenecks; during disruptions carriers and freight forwarders gain clear bargaining leverage, extending lead times and driving up freight premia. Longer lead times force higher safety stocks and working capital, while multi-port routing and forward booking mitigate but do not eliminate supplier power.

- Exposure: high import dependency

- Power shift: carriers gain leverage in disruption

- Impact: stretched lead times → higher inventory costs

- Mitigation: multi-port + forward booking reduce, not remove, risk

Partial offset via vertical integration

Vertical integration—in-house feed milling, breeding and processing—lowers reliance on intermediate suppliers and strengthens bulk-purchase leverage and access to technical services, partially offsetting supplier bargaining power. Scale enables centralized procurement and price management, but exposure to global commodity grains and regulated inputs sustains structural supplier influence. Overall supplier power is moderate with periodic cyclical spikes tied to feed-grain markets.

- In-house feed mills reduce intermediates

- Breeding and processing cut supplier dependence

- Scale improves negotiating clout on bulk buys

- Commodity grains and regulated inputs maintain supplier leverage

- Net: moderate supplier power, cyclical spikes

Input risks: corn & SBM reliance, vet pharma 50-60% market power

High import dependence on corn ($5.20/bu ≈ $205/t in 2024) and SBM ($420/t) raises supplier leverage; top-3 vet pharma ~50–60% market share increases switching costs. Energy (Brent $86/bbl 2024) and freight bottlenecks periodically spike costs and lead times; vertical integration and hedging reduce but do not remove exposure.

| Input | 2024 | Impact | Mitigation |

|---|---|---|---|

| Corn | $5.20/bu (~$205/t) | High cost volatility | Hedging, multi-sourcing |

| SBM | $420/t | Pass-through | In-house feed mills |

| Vet pharma | Top3 50–60% | Supplier power | Long-term contracts |

What is included in the product

Tailored Porter's Five Forces analysis for Leong Hup International uncovering key competitive drivers, supplier and buyer power, entry barriers, and substitutes that threaten market share, with strategic commentary for investor reports and internal strategy use.

A concise one-sheet Porter’s Five Forces for Leong Hup International—clarifies supplier, buyer and competitive pressures for fast strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Concentrated modern retail and QSR buyers

Large supermarkets, processors and QSRs buy poultry at scale and push for lower prices and tighter specs, with top buyers in Southeast Asia driving annual tenders and private label programs that now account for about 20% of grocery volumes in 2024; easy switching among compliant suppliers amplifies buyer leverage. Service levels, on-time delivery and consistent quality remain the main levers Leong Hup can use to protect margins.

Price-sensitive mass market

Chicken and eggs are staple proteins so end demand for Leong Hup is highly price elastic; consumers increasingly trade down when retail prices rise and chase promotions when they fall, a dynamic evident through 2024 retail volatility.

Export buyers and compliance requirements

Regional export buyers increasingly insist on JAKIM halal certification, HACCP and end-to-end traceability, raising qualification thresholds and adding compliance lead times of weeks to months. Once Leong Hup secures certification switching is possible but not instantaneous, tempering buyer power. Currency swings and cross-border logistics create additional negotiating variables. Long-term supply programs trade committed volumes for sharper pricing and predictable off-take.

Low switching costs among compliant suppliers

Channel mix influences leverage

Retail and foodservice majors wield strong bargaining power over Leong Hup, while fragmented traditional wet markets have much lower leverage. Expanding direct-to-consumer and e-commerce channels can lift realized prices but requires investment in fulfillment and logistics. Managing the channel mix and leveraging a broad portfolio enables cross-selling and bundled pricing to smooth average margins.

- Retail/foodservice: high power

- Wet markets: fragmented, low power

- D2C/e-commerce: higher pricing, higher fulfillment cost

- Portfolio breadth: enables cross-sell bundles

Retailer pressure, private label 20%; global supply 137m

Large retailers, processors and QSRs exert high price pressure via tenders and private labels (≈20% grocery volumes in 2024), amplified by low switching costs among compliant suppliers. Global oversupply (poultry output ~137 million tonnes in 2024) strengthens buyer leverage; certification requirements (JAKIM, HACCP, traceability) raise entry time but not long-term switching. D2C/e-commerce can lift realized prices but increases fulfillment costs.

| Buyer type | Power | Key stat (2024) |

|---|---|---|

| Retail/QSR | High | Private label ~20% |

| Market supply | Competitive | Global output ~137m t |

| Certification | Barrier | JAKIM/HACCP, weeks–months |

Same Document Delivered

Leong Hup International Porter's Five Forces Analysis

This preview shows the exact Leong Hup International Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, ready for download and use the moment you buy, and contains the complete, professionally written analysis.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Leong Hup International faces intense supplier consolidation, evolving buyer expectations, and rising substitute protein threats that shape its strategic outlook. This snapshot teases force-by-force impacts but omits granular ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to gain a consultant-grade breakdown and equip your investment or strategy decisions with data-driven insight.

Suppliers Bargaining Power

Dependence on imported grains

Maize and soybean meal are largely imported for Leong Hup (over 60% of regional feed needs), exposing feed costs to 2024 global commodity cycles and FX swings; 2024 average CME corn ~ $5.20/bu (~$205/ton) and soybean meal ~ $420/ton amplified cost pass-through. A handful of global traders concentrate supply, boosting supplier leverage in tight markets. Hedging and diverse sourcing reduce but do not eliminate volatility; vertical integration into feed milling improves conversion efficiency but offers no control over raw grain prices.

Concentrated animal health and genetics

Vaccine, veterinary pharma and breeder genetics are concentrated: in 2024 the top three veterinary pharma players (Zoetis, Elanco, Merck Animal Health) control roughly 50–60% of the global market, while leading broiler breeders dominate supply chains. Switching is limited by biosecurity, performance data and regulatory approvals, enabling price increases and strict contract terms; long-term supply agreements reduce disruption risk but heighten dependence.

Energy, packaging, and cold-chain inputs

Electricity, LPG, diesel and packaging are core inputs with few substitutes, giving suppliers situational leverage as energy price spikes (Brent crude averaged about 86 USD/bbl in 2024) only pass through imperfectly in competitive markets; cold-chain equipment and refrigerants bind firms to specialized vendors, while efficiency and on-site generation programs (requiring capex) can lower exposure but lengthen payback periods.

Logistics and port congestion exposure

Import reliance makes Leong Hup vulnerable to shipping rates, container availability and port bottlenecks; during disruptions carriers and freight forwarders gain clear bargaining leverage, extending lead times and driving up freight premia. Longer lead times force higher safety stocks and working capital, while multi-port routing and forward booking mitigate but do not eliminate supplier power.

- Exposure: high import dependency

- Power shift: carriers gain leverage in disruption

- Impact: stretched lead times → higher inventory costs

- Mitigation: multi-port + forward booking reduce, not remove, risk

Partial offset via vertical integration

Vertical integration—in-house feed milling, breeding and processing—lowers reliance on intermediate suppliers and strengthens bulk-purchase leverage and access to technical services, partially offsetting supplier bargaining power. Scale enables centralized procurement and price management, but exposure to global commodity grains and regulated inputs sustains structural supplier influence. Overall supplier power is moderate with periodic cyclical spikes tied to feed-grain markets.

- In-house feed mills reduce intermediates

- Breeding and processing cut supplier dependence

- Scale improves negotiating clout on bulk buys

- Commodity grains and regulated inputs maintain supplier leverage

- Net: moderate supplier power, cyclical spikes

Input risks: corn & SBM reliance, vet pharma 50-60% market power

High import dependence on corn ($5.20/bu ≈ $205/t in 2024) and SBM ($420/t) raises supplier leverage; top-3 vet pharma ~50–60% market share increases switching costs. Energy (Brent $86/bbl 2024) and freight bottlenecks periodically spike costs and lead times; vertical integration and hedging reduce but do not remove exposure.

| Input | 2024 | Impact | Mitigation |

|---|---|---|---|

| Corn | $5.20/bu (~$205/t) | High cost volatility | Hedging, multi-sourcing |

| SBM | $420/t | Pass-through | In-house feed mills |

| Vet pharma | Top3 50–60% | Supplier power | Long-term contracts |

What is included in the product

Tailored Porter's Five Forces analysis for Leong Hup International uncovering key competitive drivers, supplier and buyer power, entry barriers, and substitutes that threaten market share, with strategic commentary for investor reports and internal strategy use.

A concise one-sheet Porter’s Five Forces for Leong Hup International—clarifies supplier, buyer and competitive pressures for fast strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Concentrated modern retail and QSR buyers

Large supermarkets, processors and QSRs buy poultry at scale and push for lower prices and tighter specs, with top buyers in Southeast Asia driving annual tenders and private label programs that now account for about 20% of grocery volumes in 2024; easy switching among compliant suppliers amplifies buyer leverage. Service levels, on-time delivery and consistent quality remain the main levers Leong Hup can use to protect margins.

Price-sensitive mass market

Chicken and eggs are staple proteins so end demand for Leong Hup is highly price elastic; consumers increasingly trade down when retail prices rise and chase promotions when they fall, a dynamic evident through 2024 retail volatility.

Export buyers and compliance requirements

Regional export buyers increasingly insist on JAKIM halal certification, HACCP and end-to-end traceability, raising qualification thresholds and adding compliance lead times of weeks to months. Once Leong Hup secures certification switching is possible but not instantaneous, tempering buyer power. Currency swings and cross-border logistics create additional negotiating variables. Long-term supply programs trade committed volumes for sharper pricing and predictable off-take.

Low switching costs among compliant suppliers

Channel mix influences leverage

Retail and foodservice majors wield strong bargaining power over Leong Hup, while fragmented traditional wet markets have much lower leverage. Expanding direct-to-consumer and e-commerce channels can lift realized prices but requires investment in fulfillment and logistics. Managing the channel mix and leveraging a broad portfolio enables cross-selling and bundled pricing to smooth average margins.

- Retail/foodservice: high power

- Wet markets: fragmented, low power

- D2C/e-commerce: higher pricing, higher fulfillment cost

- Portfolio breadth: enables cross-sell bundles

Retailer pressure, private label 20%; global supply 137m

Large retailers, processors and QSRs exert high price pressure via tenders and private labels (≈20% grocery volumes in 2024), amplified by low switching costs among compliant suppliers. Global oversupply (poultry output ~137 million tonnes in 2024) strengthens buyer leverage; certification requirements (JAKIM, HACCP, traceability) raise entry time but not long-term switching. D2C/e-commerce can lift realized prices but increases fulfillment costs.

| Buyer type | Power | Key stat (2024) |

|---|---|---|

| Retail/QSR | High | Private label ~20% |

| Market supply | Competitive | Global output ~137m t |

| Certification | Barrier | JAKIM/HACCP, weeks–months |

Same Document Delivered

Leong Hup International Porter's Five Forces Analysis

This preview shows the exact Leong Hup International Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, ready for download and use the moment you buy, and contains the complete, professionally written analysis.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Leong Hup International faces intense supplier consolidation, evolving buyer expectations, and rising substitute protein threats that shape its strategic outlook. This snapshot teases force-by-force impacts but omits granular ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to gain a consultant-grade breakdown and equip your investment or strategy decisions with data-driven insight.

Suppliers Bargaining Power

Dependence on imported grains

Maize and soybean meal are largely imported for Leong Hup (over 60% of regional feed needs), exposing feed costs to 2024 global commodity cycles and FX swings; 2024 average CME corn ~ $5.20/bu (~$205/ton) and soybean meal ~ $420/ton amplified cost pass-through. A handful of global traders concentrate supply, boosting supplier leverage in tight markets. Hedging and diverse sourcing reduce but do not eliminate volatility; vertical integration into feed milling improves conversion efficiency but offers no control over raw grain prices.

Concentrated animal health and genetics

Vaccine, veterinary pharma and breeder genetics are concentrated: in 2024 the top three veterinary pharma players (Zoetis, Elanco, Merck Animal Health) control roughly 50–60% of the global market, while leading broiler breeders dominate supply chains. Switching is limited by biosecurity, performance data and regulatory approvals, enabling price increases and strict contract terms; long-term supply agreements reduce disruption risk but heighten dependence.

Energy, packaging, and cold-chain inputs

Electricity, LPG, diesel and packaging are core inputs with few substitutes, giving suppliers situational leverage as energy price spikes (Brent crude averaged about 86 USD/bbl in 2024) only pass through imperfectly in competitive markets; cold-chain equipment and refrigerants bind firms to specialized vendors, while efficiency and on-site generation programs (requiring capex) can lower exposure but lengthen payback periods.

Logistics and port congestion exposure

Import reliance makes Leong Hup vulnerable to shipping rates, container availability and port bottlenecks; during disruptions carriers and freight forwarders gain clear bargaining leverage, extending lead times and driving up freight premia. Longer lead times force higher safety stocks and working capital, while multi-port routing and forward booking mitigate but do not eliminate supplier power.

- Exposure: high import dependency

- Power shift: carriers gain leverage in disruption

- Impact: stretched lead times → higher inventory costs

- Mitigation: multi-port + forward booking reduce, not remove, risk

Partial offset via vertical integration

Vertical integration—in-house feed milling, breeding and processing—lowers reliance on intermediate suppliers and strengthens bulk-purchase leverage and access to technical services, partially offsetting supplier bargaining power. Scale enables centralized procurement and price management, but exposure to global commodity grains and regulated inputs sustains structural supplier influence. Overall supplier power is moderate with periodic cyclical spikes tied to feed-grain markets.

- In-house feed mills reduce intermediates

- Breeding and processing cut supplier dependence

- Scale improves negotiating clout on bulk buys

- Commodity grains and regulated inputs maintain supplier leverage

- Net: moderate supplier power, cyclical spikes

Input risks: corn & SBM reliance, vet pharma 50-60% market power

High import dependence on corn ($5.20/bu ≈ $205/t in 2024) and SBM ($420/t) raises supplier leverage; top-3 vet pharma ~50–60% market share increases switching costs. Energy (Brent $86/bbl 2024) and freight bottlenecks periodically spike costs and lead times; vertical integration and hedging reduce but do not remove exposure.

| Input | 2024 | Impact | Mitigation |

|---|---|---|---|

| Corn | $5.20/bu (~$205/t) | High cost volatility | Hedging, multi-sourcing |

| SBM | $420/t | Pass-through | In-house feed mills |

| Vet pharma | Top3 50–60% | Supplier power | Long-term contracts |

What is included in the product

Tailored Porter's Five Forces analysis for Leong Hup International uncovering key competitive drivers, supplier and buyer power, entry barriers, and substitutes that threaten market share, with strategic commentary for investor reports and internal strategy use.

A concise one-sheet Porter’s Five Forces for Leong Hup International—clarifies supplier, buyer and competitive pressures for fast strategic decisions and boardroom-ready slides.

Customers Bargaining Power

Concentrated modern retail and QSR buyers

Large supermarkets, processors and QSRs buy poultry at scale and push for lower prices and tighter specs, with top buyers in Southeast Asia driving annual tenders and private label programs that now account for about 20% of grocery volumes in 2024; easy switching among compliant suppliers amplifies buyer leverage. Service levels, on-time delivery and consistent quality remain the main levers Leong Hup can use to protect margins.

Price-sensitive mass market

Chicken and eggs are staple proteins so end demand for Leong Hup is highly price elastic; consumers increasingly trade down when retail prices rise and chase promotions when they fall, a dynamic evident through 2024 retail volatility.

Export buyers and compliance requirements

Regional export buyers increasingly insist on JAKIM halal certification, HACCP and end-to-end traceability, raising qualification thresholds and adding compliance lead times of weeks to months. Once Leong Hup secures certification switching is possible but not instantaneous, tempering buyer power. Currency swings and cross-border logistics create additional negotiating variables. Long-term supply programs trade committed volumes for sharper pricing and predictable off-take.

Low switching costs among compliant suppliers

Channel mix influences leverage

Retail and foodservice majors wield strong bargaining power over Leong Hup, while fragmented traditional wet markets have much lower leverage. Expanding direct-to-consumer and e-commerce channels can lift realized prices but requires investment in fulfillment and logistics. Managing the channel mix and leveraging a broad portfolio enables cross-selling and bundled pricing to smooth average margins.

- Retail/foodservice: high power

- Wet markets: fragmented, low power

- D2C/e-commerce: higher pricing, higher fulfillment cost

- Portfolio breadth: enables cross-sell bundles

Retailer pressure, private label 20%; global supply 137m

Large retailers, processors and QSRs exert high price pressure via tenders and private labels (≈20% grocery volumes in 2024), amplified by low switching costs among compliant suppliers. Global oversupply (poultry output ~137 million tonnes in 2024) strengthens buyer leverage; certification requirements (JAKIM, HACCP, traceability) raise entry time but not long-term switching. D2C/e-commerce can lift realized prices but increases fulfillment costs.

| Buyer type | Power | Key stat (2024) |

|---|---|---|

| Retail/QSR | High | Private label ~20% |

| Market supply | Competitive | Global output ~137m t |

| Certification | Barrier | JAKIM/HACCP, weeks–months |

Same Document Delivered

Leong Hup International Porter's Five Forces Analysis

This preview shows the exact Leong Hup International Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document is fully formatted, ready for download and use the moment you buy, and contains the complete, professionally written analysis.