Levi Strauss & Co. Porter's Five Forces Analysis

From Overview to Strategy Blueprint

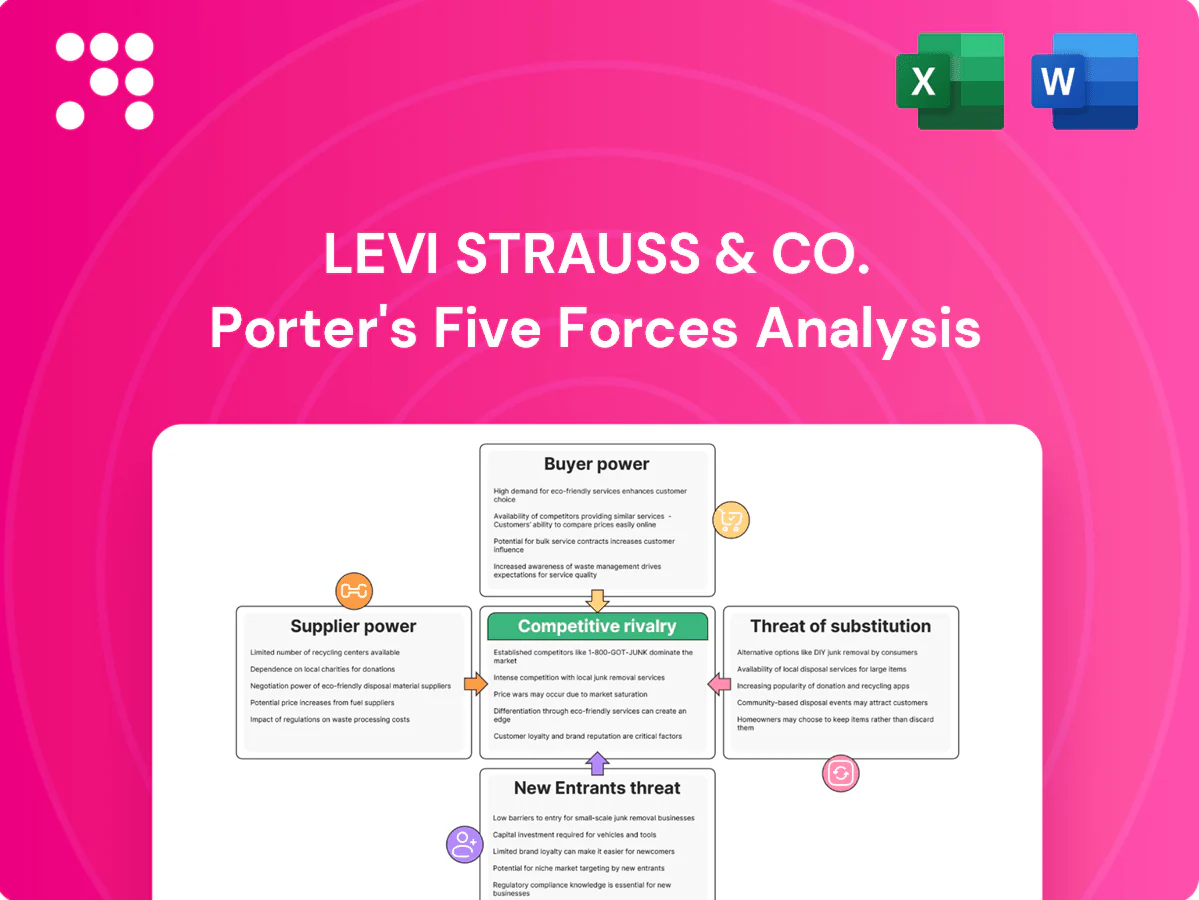

Levi Strauss & Co. faces intense rivalry from fast-fashion and premium denim brands, evolving buyer preferences, and moderate supplier leverage driven by sourcing diversification. Substitutes and digital channel shifts heighten margin pressure while scale and brand equity remain key defenses. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Levi Strauss & Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Diversified cotton and fabric base

Levi’s sources cotton, trims and specialty fabrics from dozens of countries, fragmenting supply and limiting any single supplier’s leverage; global cotton production was about 118 million 480‑lb bales in 2023/24. Levi’s multisourcing and its 2025 target of 100 percent sustainably sourced cotton reduce dependency, but weather, geopolitics and commodity volatility can tighten markets and boost supplier power. Hedging and long‑term contracts dampen shocks but do not eliminate them.

Specialty materials and finishes

Premium denim, performance stretch and proprietary washes narrow the qualified supplier set, raising switching costs and concentrating power with top-tier mills and laundries that hold Bluesign and Oeko-Tex certifications. Certification and quality consistency lengthen onboarding for alternates, while Levi’s scale (net revenue about $6.3 billion in FY2024) aids negotiation but technical lock-in sustains supplier influence.

Compliance and sustainability demands

Rising ESG standards for water, chemicals and labor shrink Levi Strauss & Co.’s eligible supplier pool and raise supplier leverage; Levi’s reports Water

Capacity, lead times, and logistics

- Typical apparel lead times: 8–16 weeks

- FY2024 net revenue: ~$6.6 billion

- Nearshore sourcing: tempers but not eliminates supplier leverage

Levi’s scale and vendor partnerships

Levi’s large, stable volumes and multi‑year vendor ties give pricing and allocation advantages, supported by roughly $6.4 billion in 2024 net revenue, while joint product development and improved demand visibility often yield preferential treatment that partly neutralizes supplier power versus smaller brands; however, advantages vary by material tier and global capacity cycles.

- Scale: long contracts, high order volumes

- Collaboration: joint PD + demand forecasts

- Limitations: raw material tier and capacity-driven

Scale and multisourcing curb supplier power despite cotton volatility and ESG constraints

Levi’s multisourcing, scale (FY2024 net revenue ~$6.6B) and long‑term contracts constrain supplier power, but premium denim specs, certifications and ESG mandates raise switching costs. Commodity volatility (global cotton ~118M 480‑lb bales 2023/24) and tight capacity during peaks amplify supplier leverage. Water

Metric

Value

FY2024 revenue

$6.6B

Cotton 2023/24

~118M 480‑lb bales

Water ~3B liters

Lead times

8–16 weeks

What is included in the product

Tailored Porter's Five Forces analysis of Levi Strauss & Co. uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive forces and market dynamics that shape pricing, profitability, and entry barriers.

Concise, one-sheet Porter's Five Forces for Levi Strauss & Co.—instantly spotlight supplier, buyer, and competitive pressures to guide pricing and sourcing decisions. Swap in your own data or duplicate scenarios (e.g., tariff shock, direct-to-consumer growth) for rapid boardroom-ready insights.

Customers Bargaining Power

Concentrated wholesale accounts

Large retailers and department stores extract discounts, co-op marketing and favorable terms, using volume concentration to secure shelf-space and promotional priority. Levi’s strong brand reduces extreme concessions but cannot eliminate wholesale pressure. Diversifying account mix mitigates dependence; no single customer accounted for 10% or more of net revenues in fiscal 2024.

Consumer price sensitivity vs. brand loyalty

Jeans are a mid-ticket, frequently promoted category, keeping consumers price-aware and sensitive to discounts. Levi’s iconic brand, fit consistency, and heritage temper elasticity and support premium tiers; FY2024 net revenue exceeded $6.07 billion, underscoring pricing power. Loyalty programs and capsule drops further anchor value perception, yet promotions remain important in driving unit velocity.

DTC growth lowers buyer leverage

Company-operated stores, outlets and e-commerce have raised Levi Strauss & Co.’s direct-to-consumer (DTC) mix to about 41% in 2024, lowering dependence on large wholesale buyers. DTC captures richer margin and first-party customer data, giving Levi control over assortments and pricing. As DTC grows, aggregate buyer leverage falls, though Levi must protect price integrity while using outlets for clearance and inventory turn.

E-commerce transparency

Online marketplaces enable instant price comparison, raising customer bargaining power as roughly 70% of apparel shoppers compare prices online (2024); Levi’s approx. 20% e-commerce share (2024) makes clarity on value critical. Reviews and fit feedback accelerate switching between denim brands, so Levi’s must ensure clear value messaging, fast shipping and easy returns (64% expect fast shipping, 2024). Dynamic pricing and exclusive SKUs can blunt transparency effects.

- price-comparison: ~70% shoppers (2024)

- e-commerce-share: ~20% Levi’s (2024)

- fast-shipping-expectation: 64% (2024)

- mitigants: dynamic pricing, exclusive SKUs

Retailer private labels

Denim leader: $6.07B, DTC 41%

Large retailers extract discounts and favorable terms, but Levi’s strong brand and FY2024 net revenue of $6.07B, plus no single customer ≥10%, limit extreme concessions. DTC ~41% of sales (2024) and ~20% e-commerce share reduce wholesale dependence; ~70% shoppers compare prices online and US private-label share ~18% increase buyer leverage.

| Metric | 2024 |

|---|---|

| Net revenue | $6.07B |

| DTC | ~41% |

| E‑commerce share | ~20% |

| No single customer ≥10% | Yes |

| Shoppers price-compare | ~70% |

| Private-label US | ~18% |

Preview the Actual Deliverable

Levi Strauss & Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Levi Strauss & Co. examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with data-driven insights. This preview is the exact, fully formatted document you will receive upon purchase. No placeholders or samples. Instant download and ready for use.

From Overview to Strategy Blueprint

Levi Strauss & Co. faces intense rivalry from fast-fashion and premium denim brands, evolving buyer preferences, and moderate supplier leverage driven by sourcing diversification. Substitutes and digital channel shifts heighten margin pressure while scale and brand equity remain key defenses. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Levi Strauss & Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Diversified cotton and fabric base

Levi’s sources cotton, trims and specialty fabrics from dozens of countries, fragmenting supply and limiting any single supplier’s leverage; global cotton production was about 118 million 480‑lb bales in 2023/24. Levi’s multisourcing and its 2025 target of 100 percent sustainably sourced cotton reduce dependency, but weather, geopolitics and commodity volatility can tighten markets and boost supplier power. Hedging and long‑term contracts dampen shocks but do not eliminate them.

Specialty materials and finishes

Premium denim, performance stretch and proprietary washes narrow the qualified supplier set, raising switching costs and concentrating power with top-tier mills and laundries that hold Bluesign and Oeko-Tex certifications. Certification and quality consistency lengthen onboarding for alternates, while Levi’s scale (net revenue about $6.3 billion in FY2024) aids negotiation but technical lock-in sustains supplier influence.

Compliance and sustainability demands

Rising ESG standards for water, chemicals and labor shrink Levi Strauss & Co.’s eligible supplier pool and raise supplier leverage; Levi’s reports Water

Capacity, lead times, and logistics

- Typical apparel lead times: 8–16 weeks

- FY2024 net revenue: ~$6.6 billion

- Nearshore sourcing: tempers but not eliminates supplier leverage

Levi’s scale and vendor partnerships

Levi’s large, stable volumes and multi‑year vendor ties give pricing and allocation advantages, supported by roughly $6.4 billion in 2024 net revenue, while joint product development and improved demand visibility often yield preferential treatment that partly neutralizes supplier power versus smaller brands; however, advantages vary by material tier and global capacity cycles.

- Scale: long contracts, high order volumes

- Collaboration: joint PD + demand forecasts

- Limitations: raw material tier and capacity-driven

Scale and multisourcing curb supplier power despite cotton volatility and ESG constraints

Levi’s multisourcing, scale (FY2024 net revenue ~$6.6B) and long‑term contracts constrain supplier power, but premium denim specs, certifications and ESG mandates raise switching costs. Commodity volatility (global cotton ~118M 480‑lb bales 2023/24) and tight capacity during peaks amplify supplier leverage. Water

Metric

Value

FY2024 revenue

$6.6B

Cotton 2023/24

~118M 480‑lb bales

Water ~3B liters

Lead times

8–16 weeks

What is included in the product

Tailored Porter's Five Forces analysis of Levi Strauss & Co. uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive forces and market dynamics that shape pricing, profitability, and entry barriers.

Concise, one-sheet Porter's Five Forces for Levi Strauss & Co.—instantly spotlight supplier, buyer, and competitive pressures to guide pricing and sourcing decisions. Swap in your own data or duplicate scenarios (e.g., tariff shock, direct-to-consumer growth) for rapid boardroom-ready insights.

Customers Bargaining Power

Concentrated wholesale accounts

Large retailers and department stores extract discounts, co-op marketing and favorable terms, using volume concentration to secure shelf-space and promotional priority. Levi’s strong brand reduces extreme concessions but cannot eliminate wholesale pressure. Diversifying account mix mitigates dependence; no single customer accounted for 10% or more of net revenues in fiscal 2024.

Consumer price sensitivity vs. brand loyalty

Jeans are a mid-ticket, frequently promoted category, keeping consumers price-aware and sensitive to discounts. Levi’s iconic brand, fit consistency, and heritage temper elasticity and support premium tiers; FY2024 net revenue exceeded $6.07 billion, underscoring pricing power. Loyalty programs and capsule drops further anchor value perception, yet promotions remain important in driving unit velocity.

DTC growth lowers buyer leverage

Company-operated stores, outlets and e-commerce have raised Levi Strauss & Co.’s direct-to-consumer (DTC) mix to about 41% in 2024, lowering dependence on large wholesale buyers. DTC captures richer margin and first-party customer data, giving Levi control over assortments and pricing. As DTC grows, aggregate buyer leverage falls, though Levi must protect price integrity while using outlets for clearance and inventory turn.

E-commerce transparency

Online marketplaces enable instant price comparison, raising customer bargaining power as roughly 70% of apparel shoppers compare prices online (2024); Levi’s approx. 20% e-commerce share (2024) makes clarity on value critical. Reviews and fit feedback accelerate switching between denim brands, so Levi’s must ensure clear value messaging, fast shipping and easy returns (64% expect fast shipping, 2024). Dynamic pricing and exclusive SKUs can blunt transparency effects.

- price-comparison: ~70% shoppers (2024)

- e-commerce-share: ~20% Levi’s (2024)

- fast-shipping-expectation: 64% (2024)

- mitigants: dynamic pricing, exclusive SKUs

Retailer private labels

Denim leader: $6.07B, DTC 41%

Large retailers extract discounts and favorable terms, but Levi’s strong brand and FY2024 net revenue of $6.07B, plus no single customer ≥10%, limit extreme concessions. DTC ~41% of sales (2024) and ~20% e-commerce share reduce wholesale dependence; ~70% shoppers compare prices online and US private-label share ~18% increase buyer leverage.

| Metric | 2024 |

|---|---|

| Net revenue | $6.07B |

| DTC | ~41% |

| E‑commerce share | ~20% |

| No single customer ≥10% | Yes |

| Shoppers price-compare | ~70% |

| Private-label US | ~18% |

Preview the Actual Deliverable

Levi Strauss & Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Levi Strauss & Co. examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with data-driven insights. This preview is the exact, fully formatted document you will receive upon purchase. No placeholders or samples. Instant download and ready for use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Levi Strauss & Co. faces intense rivalry from fast-fashion and premium denim brands, evolving buyer preferences, and moderate supplier leverage driven by sourcing diversification. Substitutes and digital channel shifts heighten margin pressure while scale and brand equity remain key defenses. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Levi Strauss & Co.’s competitive dynamics in detail.

Suppliers Bargaining Power

Diversified cotton and fabric base

Levi’s sources cotton, trims and specialty fabrics from dozens of countries, fragmenting supply and limiting any single supplier’s leverage; global cotton production was about 118 million 480‑lb bales in 2023/24. Levi’s multisourcing and its 2025 target of 100 percent sustainably sourced cotton reduce dependency, but weather, geopolitics and commodity volatility can tighten markets and boost supplier power. Hedging and long‑term contracts dampen shocks but do not eliminate them.

Specialty materials and finishes

Premium denim, performance stretch and proprietary washes narrow the qualified supplier set, raising switching costs and concentrating power with top-tier mills and laundries that hold Bluesign and Oeko-Tex certifications. Certification and quality consistency lengthen onboarding for alternates, while Levi’s scale (net revenue about $6.3 billion in FY2024) aids negotiation but technical lock-in sustains supplier influence.

Compliance and sustainability demands

Rising ESG standards for water, chemicals and labor shrink Levi Strauss & Co.’s eligible supplier pool and raise supplier leverage; Levi’s reports Water

Capacity, lead times, and logistics

- Typical apparel lead times: 8–16 weeks

- FY2024 net revenue: ~$6.6 billion

- Nearshore sourcing: tempers but not eliminates supplier leverage

Levi’s scale and vendor partnerships

Levi’s large, stable volumes and multi‑year vendor ties give pricing and allocation advantages, supported by roughly $6.4 billion in 2024 net revenue, while joint product development and improved demand visibility often yield preferential treatment that partly neutralizes supplier power versus smaller brands; however, advantages vary by material tier and global capacity cycles.

- Scale: long contracts, high order volumes

- Collaboration: joint PD + demand forecasts

- Limitations: raw material tier and capacity-driven

Scale and multisourcing curb supplier power despite cotton volatility and ESG constraints

Levi’s multisourcing, scale (FY2024 net revenue ~$6.6B) and long‑term contracts constrain supplier power, but premium denim specs, certifications and ESG mandates raise switching costs. Commodity volatility (global cotton ~118M 480‑lb bales 2023/24) and tight capacity during peaks amplify supplier leverage. Water

Metric

Value

FY2024 revenue

$6.6B

Cotton 2023/24

~118M 480‑lb bales

Water ~3B liters

Lead times

8–16 weeks

What is included in the product

Tailored Porter's Five Forces analysis of Levi Strauss & Co. uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive forces and market dynamics that shape pricing, profitability, and entry barriers.

Concise, one-sheet Porter's Five Forces for Levi Strauss & Co.—instantly spotlight supplier, buyer, and competitive pressures to guide pricing and sourcing decisions. Swap in your own data or duplicate scenarios (e.g., tariff shock, direct-to-consumer growth) for rapid boardroom-ready insights.

Customers Bargaining Power

Concentrated wholesale accounts

Large retailers and department stores extract discounts, co-op marketing and favorable terms, using volume concentration to secure shelf-space and promotional priority. Levi’s strong brand reduces extreme concessions but cannot eliminate wholesale pressure. Diversifying account mix mitigates dependence; no single customer accounted for 10% or more of net revenues in fiscal 2024.

Consumer price sensitivity vs. brand loyalty

Jeans are a mid-ticket, frequently promoted category, keeping consumers price-aware and sensitive to discounts. Levi’s iconic brand, fit consistency, and heritage temper elasticity and support premium tiers; FY2024 net revenue exceeded $6.07 billion, underscoring pricing power. Loyalty programs and capsule drops further anchor value perception, yet promotions remain important in driving unit velocity.

DTC growth lowers buyer leverage

Company-operated stores, outlets and e-commerce have raised Levi Strauss & Co.’s direct-to-consumer (DTC) mix to about 41% in 2024, lowering dependence on large wholesale buyers. DTC captures richer margin and first-party customer data, giving Levi control over assortments and pricing. As DTC grows, aggregate buyer leverage falls, though Levi must protect price integrity while using outlets for clearance and inventory turn.

E-commerce transparency

Online marketplaces enable instant price comparison, raising customer bargaining power as roughly 70% of apparel shoppers compare prices online (2024); Levi’s approx. 20% e-commerce share (2024) makes clarity on value critical. Reviews and fit feedback accelerate switching between denim brands, so Levi’s must ensure clear value messaging, fast shipping and easy returns (64% expect fast shipping, 2024). Dynamic pricing and exclusive SKUs can blunt transparency effects.

- price-comparison: ~70% shoppers (2024)

- e-commerce-share: ~20% Levi’s (2024)

- fast-shipping-expectation: 64% (2024)

- mitigants: dynamic pricing, exclusive SKUs

Retailer private labels

Denim leader: $6.07B, DTC 41%

Large retailers extract discounts and favorable terms, but Levi’s strong brand and FY2024 net revenue of $6.07B, plus no single customer ≥10%, limit extreme concessions. DTC ~41% of sales (2024) and ~20% e-commerce share reduce wholesale dependence; ~70% shoppers compare prices online and US private-label share ~18% increase buyer leverage.

| Metric | 2024 |

|---|---|

| Net revenue | $6.07B |

| DTC | ~41% |

| E‑commerce share | ~20% |

| No single customer ≥10% | Yes |

| Shoppers price-compare | ~70% |

| Private-label US | ~18% |

Preview the Actual Deliverable

Levi Strauss & Co. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Levi Strauss & Co. examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with data-driven insights. This preview is the exact, fully formatted document you will receive upon purchase. No placeholders or samples. Instant download and ready for use.