Leyard Optoelectronic PESTLE Analysis

Your Shortcut to Market Insight Starts Here

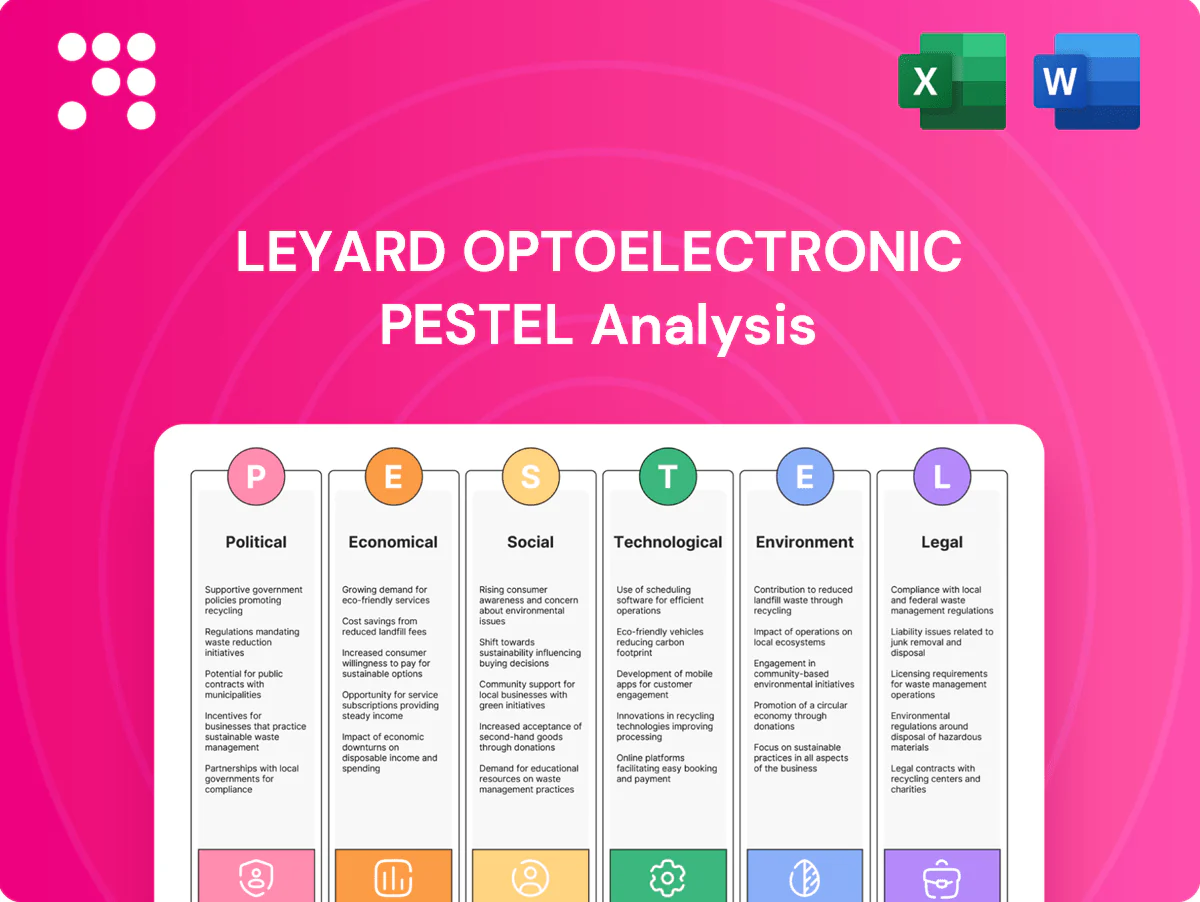

Gain a strategic advantage with our PESTLE Analysis of Leyard Optoelectronic. Discover how political, economic, social, technological, legal and environmental forces shape its future and competitive position. Ideal for investors and strategists—buy the full, downloadable report now.

Political factors

Trade policy and tariffs

Leyard faces shifting US/EU tariffs on LEDs and electronics that can materially alter pricing and margins. US Section 301 tariffs impose up to 25% on many Chinese imports, affecting competitiveness. Periodic tariff exemptions for specific HS/HTS codes have opened windows for competitive bids. Localizing assembly in key markets mitigates duty exposure and makes continuous monitoring of customs classifications and rules of origin critical.

Government infrastructure spending

Public investments in smart cities, transportation hubs and cultural venues directly drive demand for large-format LED displays. Stimulus programs and urban renewal policies in China, the Middle East and emerging markets can accelerate project pipelines; China’s urbanization reached 64.7% in 2023. Budget cycles and tender processes affect revenue timing, so strong public-sector relationships and compliance readiness improve win rates.

Geopolitical tensions and supply chain security

US–China technology frictions, reinforced by US export controls on advanced semiconductors and the CHIPS and Science Act (about 52 billion USD in incentives), constrain component access, export licensing and partner selection for Leyard.

Customers increasingly demand supply chain transparency and country-of-origin assurances, raising procurement due-diligence costs.

Dual-sourcing and regional inventories are recommended to lower disruption risk and maintain service levels.

Crisis scenarios should be stress-tested for logistics routes and key component continuity with measurable recovery-time objectives.

Subsidies and industrial policies

National and provincial incentives for semiconductor and LED ecosystems can materially lower Leyard’s capex and R&D burden by offsetting equipment and pilot-line costs, while competing regions’ subsidies for local champions heighten competitive intensity and risk of subsidy-driven pricing. Policy eligibility commonly ties disbursements to localization and demonstrable innovation milestones, so strategic site selection should target jurisdictions with matching incentive criteria and supply-chain depth.

Public procurement standards

Government tenders increasingly mandate energy-efficiency labels, TÜV/UL safety certifications and NIST/ISO 27001-class cybersecurity controls; public procurement represents roughly 12% of global GDP (about $11 trillion in 2024), so compliance is material for Leyard's large-display bids. Preferential procurement for domestic vendors in markets like China and parts of the EU can reduce foreign win rates, while transparent anti-corruption protocols are decisive in state projects and compliance capabilities often swing close contests.

- Energy-efficiency, safety, cybersecurity required

- Public procurement ≈ 12% GDP (~$11T in 2024)

- Domestic preference lowers foreign win probability

- Anti-corruption transparency and compliance = differentiator

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

Leyard faces up to 25% US Section 301 tariffs and export controls from CHIPS (≈52B USD) that constrain components and partner choices. Public procurement (~12% global GDP, ~11T USD in 2024) and China urbanization (64.7% in 2023) drive LED demand and favor local suppliers; incentives lower capex but boost subsidy-led competition. Compliance, localization and dual-sourcing are critical.

| Factor | Key data |

|---|---|

| Tariffs | Up to 25% |

| CHIPS funding | ≈52B USD |

| Public procurement | ~12% GDP (~11T USD) |

| Urbanization (China) | 64.7% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Leyard Optoelectronic, with data‑backed trends, region‑ and industry‑specific subpoints and forward‑looking insights to inform scenario planning; designed for executives and investors and formatted for direct use in plans, decks and reports.

A concise, visually segmented PESTLE summary for Leyard Optoelectronic that streamlines meeting prep and strategy sessions, easily dropped into slides or shared across teams for quick alignment. It uses clear language and editable notes to contextualize risks and opportunities for specific regions or business lines.

Economic factors

Capex cycles and event-driven demand

LED projects remain highly cyclical, tracking macro capex and advertising budgets—global ad spend was roughly $850 billion in 2024 (GroupM), so cuts quickly depress demand for signage and digital OOH.

Major events such as Paris 2024 and the FIFA World Cup 2026 drive concentrated upgrade waves across rental and fixed-install segments, lifting short-term unit sales and rental demand.

Economic slowdowns typically defer discretionary screen refreshes and venue investments, while Leyard’s diversified end-market mix across rental, control rooms, retail and stadiums helps smooth revenue volatility.

FX fluctuations and pricing power

Leyard's FY2024 disclosure shows overseas sales around 30% of revenue, creating USD/EUR exposure while costs remain largely in RMB, producing translation and transaction risk that can compress margins during adverse moves (USD/CNY volatility peaked near 7.3 in 2023–24). Hedging programs and offshore sourcing have reduced realized FX swings, and tiered pricing plus value-added services have helped sustain ASPs despite currency pressure.

Input costs and component availability

Driver ICs, LEDs, power supplies and key metals now account for roughly 40–60% of a large-format LED display bill of materials, directly driving Leyard’s COGS and margin volatility. Industry tightness and foundry constraints kept average semiconductor lead times near 10–12 weeks in 2024, extending project timelines. Long-term supply agreements and 60–120 day inventory buffers have materially reduced stockout risk. Modular product architectures enable rapid component substitution when shortages occur.

Advertising and OOH media cycles

DOOH networks invest counter-cyclically with strong ad markets accelerating network rollouts and pixel-pitch upgrades, while downturns pivot spend to maintenance over new builds. Industry estimates show global DOOH ad spend exceeded 18 billion USD in 2024, driving larger-format and higher-resolution demand. Offering financing or revenue-share models has unlocked deployments, shortening payback from 5–8 years toward 3–5 years in many markets.

- Counter-cyclical investment

- 2024 DOOH spend >18B USD

- Upgrades tied to ad market strength

- Financing/revenue-share shortens payback

Global growth divergence

Global growth divergence drives demand splits for Leyard: developed markets favor premium microLED/COB, while emerging markets prioritize cost-optimized LED walls; IMF 2024 estimated advanced economy growth ~1.4% vs emerging markets ~4.3%, underscoring different purchasing power and product mix.

- Premium demand — developed markets

- Cost focus — emerging markets

- Currency pressure on imports

- Regional hubs tailor offerings

- Geographic diversification hedges slowdowns

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

LED demand is cyclical with global ad spend ~850B USD in 2024 (GroupM) and DOOH >18B USD, driving upgrade waves around mega events; economic slowdowns defer refreshes but Leyard's diverse end-markets smooth revenue. FX exposure (overseas ~30% revenue) and USD/CNY volatility (peaked ~7.3 in 2023–24) can compress margins; supply tightness (IC lead times 10–12 wks in 2024) affects COGS.

| Metric | 2024/2024–25 |

|---|---|

| Global ad spend | ~850B USD (2024) |

| DOOH spend | >18B USD (2024) |

| Overseas revenue | ~30% |

| USD/CNY | ~7.3 peak (2023–24) |

| IC lead times | 10–12 weeks (2024) |

Preview Before You Purchase

Leyard Optoelectronic PESTLE Analysis

The preview shown here is the exact Leyard Optoelectronic PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with actionable insights and strategic implications. No placeholders, just the final professional file.

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Leyard Optoelectronic. Discover how political, economic, social, technological, legal and environmental forces shape its future and competitive position. Ideal for investors and strategists—buy the full, downloadable report now.

Political factors

Trade policy and tariffs

Leyard faces shifting US/EU tariffs on LEDs and electronics that can materially alter pricing and margins. US Section 301 tariffs impose up to 25% on many Chinese imports, affecting competitiveness. Periodic tariff exemptions for specific HS/HTS codes have opened windows for competitive bids. Localizing assembly in key markets mitigates duty exposure and makes continuous monitoring of customs classifications and rules of origin critical.

Government infrastructure spending

Public investments in smart cities, transportation hubs and cultural venues directly drive demand for large-format LED displays. Stimulus programs and urban renewal policies in China, the Middle East and emerging markets can accelerate project pipelines; China’s urbanization reached 64.7% in 2023. Budget cycles and tender processes affect revenue timing, so strong public-sector relationships and compliance readiness improve win rates.

Geopolitical tensions and supply chain security

US–China technology frictions, reinforced by US export controls on advanced semiconductors and the CHIPS and Science Act (about 52 billion USD in incentives), constrain component access, export licensing and partner selection for Leyard.

Customers increasingly demand supply chain transparency and country-of-origin assurances, raising procurement due-diligence costs.

Dual-sourcing and regional inventories are recommended to lower disruption risk and maintain service levels.

Crisis scenarios should be stress-tested for logistics routes and key component continuity with measurable recovery-time objectives.

Subsidies and industrial policies

National and provincial incentives for semiconductor and LED ecosystems can materially lower Leyard’s capex and R&D burden by offsetting equipment and pilot-line costs, while competing regions’ subsidies for local champions heighten competitive intensity and risk of subsidy-driven pricing. Policy eligibility commonly ties disbursements to localization and demonstrable innovation milestones, so strategic site selection should target jurisdictions with matching incentive criteria and supply-chain depth.

Public procurement standards

Government tenders increasingly mandate energy-efficiency labels, TÜV/UL safety certifications and NIST/ISO 27001-class cybersecurity controls; public procurement represents roughly 12% of global GDP (about $11 trillion in 2024), so compliance is material for Leyard's large-display bids. Preferential procurement for domestic vendors in markets like China and parts of the EU can reduce foreign win rates, while transparent anti-corruption protocols are decisive in state projects and compliance capabilities often swing close contests.

- Energy-efficiency, safety, cybersecurity required

- Public procurement ≈ 12% GDP (~$11T in 2024)

- Domestic preference lowers foreign win probability

- Anti-corruption transparency and compliance = differentiator

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

Leyard faces up to 25% US Section 301 tariffs and export controls from CHIPS (≈52B USD) that constrain components and partner choices. Public procurement (~12% global GDP, ~11T USD in 2024) and China urbanization (64.7% in 2023) drive LED demand and favor local suppliers; incentives lower capex but boost subsidy-led competition. Compliance, localization and dual-sourcing are critical.

| Factor | Key data |

|---|---|

| Tariffs | Up to 25% |

| CHIPS funding | ≈52B USD |

| Public procurement | ~12% GDP (~11T USD) |

| Urbanization (China) | 64.7% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Leyard Optoelectronic, with data‑backed trends, region‑ and industry‑specific subpoints and forward‑looking insights to inform scenario planning; designed for executives and investors and formatted for direct use in plans, decks and reports.

A concise, visually segmented PESTLE summary for Leyard Optoelectronic that streamlines meeting prep and strategy sessions, easily dropped into slides or shared across teams for quick alignment. It uses clear language and editable notes to contextualize risks and opportunities for specific regions or business lines.

Economic factors

Capex cycles and event-driven demand

LED projects remain highly cyclical, tracking macro capex and advertising budgets—global ad spend was roughly $850 billion in 2024 (GroupM), so cuts quickly depress demand for signage and digital OOH.

Major events such as Paris 2024 and the FIFA World Cup 2026 drive concentrated upgrade waves across rental and fixed-install segments, lifting short-term unit sales and rental demand.

Economic slowdowns typically defer discretionary screen refreshes and venue investments, while Leyard’s diversified end-market mix across rental, control rooms, retail and stadiums helps smooth revenue volatility.

FX fluctuations and pricing power

Leyard's FY2024 disclosure shows overseas sales around 30% of revenue, creating USD/EUR exposure while costs remain largely in RMB, producing translation and transaction risk that can compress margins during adverse moves (USD/CNY volatility peaked near 7.3 in 2023–24). Hedging programs and offshore sourcing have reduced realized FX swings, and tiered pricing plus value-added services have helped sustain ASPs despite currency pressure.

Input costs and component availability

Driver ICs, LEDs, power supplies and key metals now account for roughly 40–60% of a large-format LED display bill of materials, directly driving Leyard’s COGS and margin volatility. Industry tightness and foundry constraints kept average semiconductor lead times near 10–12 weeks in 2024, extending project timelines. Long-term supply agreements and 60–120 day inventory buffers have materially reduced stockout risk. Modular product architectures enable rapid component substitution when shortages occur.

Advertising and OOH media cycles

DOOH networks invest counter-cyclically with strong ad markets accelerating network rollouts and pixel-pitch upgrades, while downturns pivot spend to maintenance over new builds. Industry estimates show global DOOH ad spend exceeded 18 billion USD in 2024, driving larger-format and higher-resolution demand. Offering financing or revenue-share models has unlocked deployments, shortening payback from 5–8 years toward 3–5 years in many markets.

- Counter-cyclical investment

- 2024 DOOH spend >18B USD

- Upgrades tied to ad market strength

- Financing/revenue-share shortens payback

Global growth divergence

Global growth divergence drives demand splits for Leyard: developed markets favor premium microLED/COB, while emerging markets prioritize cost-optimized LED walls; IMF 2024 estimated advanced economy growth ~1.4% vs emerging markets ~4.3%, underscoring different purchasing power and product mix.

- Premium demand — developed markets

- Cost focus — emerging markets

- Currency pressure on imports

- Regional hubs tailor offerings

- Geographic diversification hedges slowdowns

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

LED demand is cyclical with global ad spend ~850B USD in 2024 (GroupM) and DOOH >18B USD, driving upgrade waves around mega events; economic slowdowns defer refreshes but Leyard's diverse end-markets smooth revenue. FX exposure (overseas ~30% revenue) and USD/CNY volatility (peaked ~7.3 in 2023–24) can compress margins; supply tightness (IC lead times 10–12 wks in 2024) affects COGS.

| Metric | 2024/2024–25 |

|---|---|

| Global ad spend | ~850B USD (2024) |

| DOOH spend | >18B USD (2024) |

| Overseas revenue | ~30% |

| USD/CNY | ~7.3 peak (2023–24) |

| IC lead times | 10–12 weeks (2024) |

Preview Before You Purchase

Leyard Optoelectronic PESTLE Analysis

The preview shown here is the exact Leyard Optoelectronic PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with actionable insights and strategic implications. No placeholders, just the final professional file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Leyard Optoelectronic. Discover how political, economic, social, technological, legal and environmental forces shape its future and competitive position. Ideal for investors and strategists—buy the full, downloadable report now.

Political factors

Trade policy and tariffs

Leyard faces shifting US/EU tariffs on LEDs and electronics that can materially alter pricing and margins. US Section 301 tariffs impose up to 25% on many Chinese imports, affecting competitiveness. Periodic tariff exemptions for specific HS/HTS codes have opened windows for competitive bids. Localizing assembly in key markets mitigates duty exposure and makes continuous monitoring of customs classifications and rules of origin critical.

Government infrastructure spending

Public investments in smart cities, transportation hubs and cultural venues directly drive demand for large-format LED displays. Stimulus programs and urban renewal policies in China, the Middle East and emerging markets can accelerate project pipelines; China’s urbanization reached 64.7% in 2023. Budget cycles and tender processes affect revenue timing, so strong public-sector relationships and compliance readiness improve win rates.

Geopolitical tensions and supply chain security

US–China technology frictions, reinforced by US export controls on advanced semiconductors and the CHIPS and Science Act (about 52 billion USD in incentives), constrain component access, export licensing and partner selection for Leyard.

Customers increasingly demand supply chain transparency and country-of-origin assurances, raising procurement due-diligence costs.

Dual-sourcing and regional inventories are recommended to lower disruption risk and maintain service levels.

Crisis scenarios should be stress-tested for logistics routes and key component continuity with measurable recovery-time objectives.

Subsidies and industrial policies

National and provincial incentives for semiconductor and LED ecosystems can materially lower Leyard’s capex and R&D burden by offsetting equipment and pilot-line costs, while competing regions’ subsidies for local champions heighten competitive intensity and risk of subsidy-driven pricing. Policy eligibility commonly ties disbursements to localization and demonstrable innovation milestones, so strategic site selection should target jurisdictions with matching incentive criteria and supply-chain depth.

Public procurement standards

Government tenders increasingly mandate energy-efficiency labels, TÜV/UL safety certifications and NIST/ISO 27001-class cybersecurity controls; public procurement represents roughly 12% of global GDP (about $11 trillion in 2024), so compliance is material for Leyard's large-display bids. Preferential procurement for domestic vendors in markets like China and parts of the EU can reduce foreign win rates, while transparent anti-corruption protocols are decisive in state projects and compliance capabilities often swing close contests.

- Energy-efficiency, safety, cybersecurity required

- Public procurement ≈ 12% GDP (~$11T in 2024)

- Domestic preference lowers foreign win probability

- Anti-corruption transparency and compliance = differentiator

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

Leyard faces up to 25% US Section 301 tariffs and export controls from CHIPS (≈52B USD) that constrain components and partner choices. Public procurement (~12% global GDP, ~11T USD in 2024) and China urbanization (64.7% in 2023) drive LED demand and favor local suppliers; incentives lower capex but boost subsidy-led competition. Compliance, localization and dual-sourcing are critical.

| Factor | Key data |

|---|---|

| Tariffs | Up to 25% |

| CHIPS funding | ≈52B USD |

| Public procurement | ~12% GDP (~11T USD) |

| Urbanization (China) | 64.7% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Leyard Optoelectronic, with data‑backed trends, region‑ and industry‑specific subpoints and forward‑looking insights to inform scenario planning; designed for executives and investors and formatted for direct use in plans, decks and reports.

A concise, visually segmented PESTLE summary for Leyard Optoelectronic that streamlines meeting prep and strategy sessions, easily dropped into slides or shared across teams for quick alignment. It uses clear language and editable notes to contextualize risks and opportunities for specific regions or business lines.

Economic factors

Capex cycles and event-driven demand

LED projects remain highly cyclical, tracking macro capex and advertising budgets—global ad spend was roughly $850 billion in 2024 (GroupM), so cuts quickly depress demand for signage and digital OOH.

Major events such as Paris 2024 and the FIFA World Cup 2026 drive concentrated upgrade waves across rental and fixed-install segments, lifting short-term unit sales and rental demand.

Economic slowdowns typically defer discretionary screen refreshes and venue investments, while Leyard’s diversified end-market mix across rental, control rooms, retail and stadiums helps smooth revenue volatility.

FX fluctuations and pricing power

Leyard's FY2024 disclosure shows overseas sales around 30% of revenue, creating USD/EUR exposure while costs remain largely in RMB, producing translation and transaction risk that can compress margins during adverse moves (USD/CNY volatility peaked near 7.3 in 2023–24). Hedging programs and offshore sourcing have reduced realized FX swings, and tiered pricing plus value-added services have helped sustain ASPs despite currency pressure.

Input costs and component availability

Driver ICs, LEDs, power supplies and key metals now account for roughly 40–60% of a large-format LED display bill of materials, directly driving Leyard’s COGS and margin volatility. Industry tightness and foundry constraints kept average semiconductor lead times near 10–12 weeks in 2024, extending project timelines. Long-term supply agreements and 60–120 day inventory buffers have materially reduced stockout risk. Modular product architectures enable rapid component substitution when shortages occur.

Advertising and OOH media cycles

DOOH networks invest counter-cyclically with strong ad markets accelerating network rollouts and pixel-pitch upgrades, while downturns pivot spend to maintenance over new builds. Industry estimates show global DOOH ad spend exceeded 18 billion USD in 2024, driving larger-format and higher-resolution demand. Offering financing or revenue-share models has unlocked deployments, shortening payback from 5–8 years toward 3–5 years in many markets.

- Counter-cyclical investment

- 2024 DOOH spend >18B USD

- Upgrades tied to ad market strength

- Financing/revenue-share shortens payback

Global growth divergence

Global growth divergence drives demand splits for Leyard: developed markets favor premium microLED/COB, while emerging markets prioritize cost-optimized LED walls; IMF 2024 estimated advanced economy growth ~1.4% vs emerging markets ~4.3%, underscoring different purchasing power and product mix.

- Premium demand — developed markets

- Cost focus — emerging markets

- Currency pressure on imports

- Regional hubs tailor offerings

- Geographic diversification hedges slowdowns

Tariffs up to 25% and CHIPS ≈52B USD reshape LED supply chains, boosting localization

LED demand is cyclical with global ad spend ~850B USD in 2024 (GroupM) and DOOH >18B USD, driving upgrade waves around mega events; economic slowdowns defer refreshes but Leyard's diverse end-markets smooth revenue. FX exposure (overseas ~30% revenue) and USD/CNY volatility (peaked ~7.3 in 2023–24) can compress margins; supply tightness (IC lead times 10–12 wks in 2024) affects COGS.

| Metric | 2024/2024–25 |

|---|---|

| Global ad spend | ~850B USD (2024) |

| DOOH spend | >18B USD (2024) |

| Overseas revenue | ~30% |

| USD/CNY | ~7.3 peak (2023–24) |

| IC lead times | 10–12 weeks (2024) |

Preview Before You Purchase

Leyard Optoelectronic PESTLE Analysis

The preview shown here is the exact Leyard Optoelectronic PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with actionable insights and strategic implications. No placeholders, just the final professional file.