Lincoln National Boston Consulting Group Matrix

Download Your Competitive Advantage

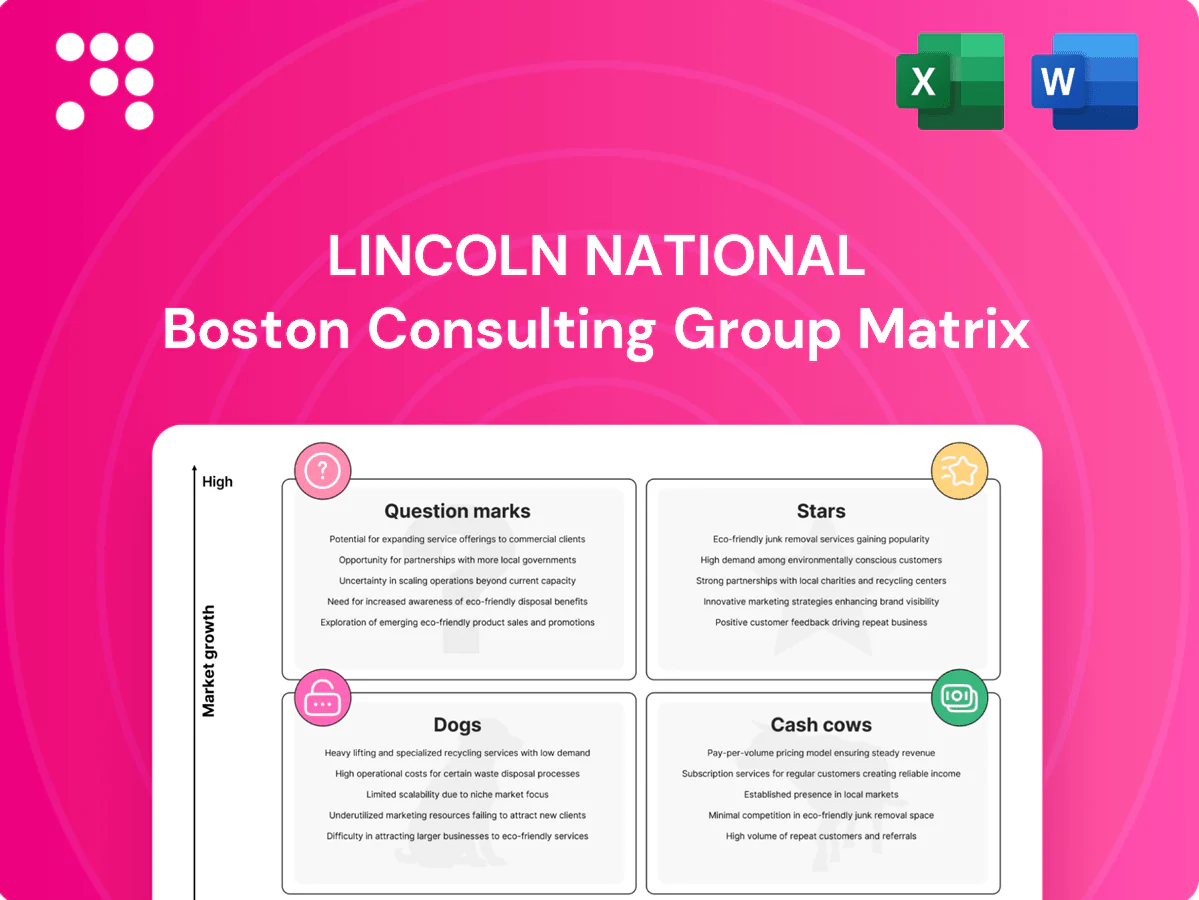

The Lincoln National BCG Matrix snapshot shows which lines are fueling growth and which are tying up cash — a quick read that already spots Stars, Cash Cows, Dogs, and Question Marks in their portfolio. This preview teases the key moves; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis and an Excel summary you can present or act on immediately.

Stars

Indexed annuities momentum

Fixed indexed annuities are benefiting from higher interest rates (federal funds ~5.25–5.50% in 2024) and strong consumer demand for downside protection; Lincoln already holds meaningful share and can lean into product innovation and expanded distribution. These products consume capital for hedging and marketing, but continued premium growth supports the investment. Defend share now to graduate FIAs into durable earnings generators.

Indexed UL & protection-led life

IUL continues to outgrow traditional life as clients seek flexibility and cash-value upside, with LIMRA reporting roughly 10% year-over-year growth in IUL sales into 2024; Lincoln’s national franchise and wholesaler reach keep it near the front of the pack. It still needs targeted spend on pricing agility, underwriting tech, and expanded advisor education to capture share. Keep fueling it; the curve remains up-and-to-the-right.

Voluntary benefits in Group

Employers are expanding voluntary menus and employee opt-in rates rose to about 50% in mid-market in 2024, driving category expansion. Lincoln’s group platform can cross-sell life, accident and disability in one swing, leveraging bundled underwriting and payroll deduction. Success hinges on promotion, modern enrollment tech and broker engagement. Worth the push—category growth is doing the heavy lifting for unit economics.

Retirement plan services mid‑market

401(k) recordkeeping and managed accounts show steady inflows in 2024; auto-features boost participation by about 10 percentage points. Lincoln remains competitive in service and advisor-led distribution, serving roughly $300bn AUA (2024). Margins scale with assets, though onboarding and tech require heavy investment; continue capturing plans amid ongoing consolidation.

- auto-features:+10pp participation (2024)

- Lincoln AUA:≈$300bn (2024)

- margin scale with AUA

- onboarding/tech capex high

Worksite distribution scale

Worksite distribution is a star for Lincoln when enrollment is clean and digital, leveraging its national footprint to secure more RFPs and employer panels. High-touch broker relationships and ongoing education remain critical to convert scale into retention and cross-sell. Investing now to lock multi-year employer contracts preserves lifetime value and accelerates margin expansion.

Lock growth: FIA, IUL, and worksite 401(k) tech to win premiums and scale margins

Stars: FIAs (benefit from fed funds ~5.25–5.50% in 2024) and IUL (~10% YoY sales growth into 2024) plus worksite/401(k) (Lincoln AUA ≈$300bn; mid-market voluntary opt-in ~50%) drive premium and AUA growth; invest in product, distribution, and enrollment tech to lock share and scale margins.

| Product | 2024 Metric | Priority |

|---|---|---|

| FIA | Fed funds 5.25–5.50% | Hedge & innovate |

| IUL | ~10% YoY | Pricing & UW tech |

| 401(k)/Worksite | AUA ≈$300bn; opt-in ~50% | Enrollment tech |

What is included in the product

Concise strategic assessment of Lincoln National's products across BCG quadrants, showing where to invest, hold or divest.

One-page Lincoln BCG matrix placing each business unit in a quadrant to spot winners, underperformers and resource needs.

Cash Cows

In‑force life blocks

In‑force life blocks are Lincoln’s cash cows, producing stable margins and predictable fee income from seasoned books with well‑modeled lapse, mortality and expense assumptions. Minimal new sales spend is required—management focuses on experience management and capital allocation. Cash flow is systematically harvested to fund growth initiatives and to de‑risk the balance sheet.

Traditional fixed annuities

Traditional fixed annuities sit in Lincoln Nationals mature cash-cow bucket, serving loyal, conservative buyers with steady spreads typically around 200–300 basis points and lower sales churn versus variable products. Pricing discipline and tight asset-liability matching drive reliable earnings, with promotion light and retention-focused distribution. Continued optimization of operations and hedging is key to preserving those spreads amid 2024 rate volatility.

Group basic life & disability

Group basic life & disability is a cash cow for Lincoln, with sticky employer-paid coverage that yields low acquisition cost once installed and renewal margins in 2024 running in the mid-teens. Renewal economics and scale in claims management produce steady cash flow, supporting capital generation. Growth is modest but retention remains high, around 92% in 2024, so emphasis is on underwriting discipline and admin efficiency.

Separate account fees on annuities

Separate account fees on annuities generate steady asset-based revenue — typically in the industry range of 30 to 80 basis points — that hums along as balances compound; operating leverage is high once Lincoln’s platform is in place, so incremental AUM lifts margins. Market swings affect flows, but long-tenured accounts and sticky surrender behavior in 2024 help cushion volatility; maintain service quality and let AUM compounding do the work.

- steady-fee: asset-based fees 30–80 bps

- high-operating-leverage: fixed platform costs dilute

- sticky-aum: long-tenured accounts cushion 2024 market swings

- operational-focus: maintain service quality to compound AUM

Advisor & broker relationships

Lincoln’s advisor and broker relationships are cash cows: established channels lower marginal selling costs across life, annuity and investment products, with Deloitte 2024 finding advisers increase cross-sell revenue by ~35%, lifting customer lifetime value without heavy promotional spend.

The model is a durable moat so long as service levels remain high; Lincoln’s distribution focus preserves retention and unit economics, so maintain the relationship engine—steady investment, not overfunding.

- Lower marginal cost: repeat channel leverage

- Cross-sell lift: ~35% (Deloitte 2024)

- Durability: dependent on service quality

- Capex guidance: optimize, don’t overspend

In-force life, fixed annuities & group benefits: steady margins, strong cashflow in 2024

In‑force life blocks, traditional fixed annuities and group life/disability are Lincoln’s cash cows in 2024, delivering stable margins (renewal margins ~15%), annuity spreads ~200–300 bps and retention ~92%. Separate account fees (30–80 bps) and advisor channels (cross-sell +35%) provide steady, low‑cost cashflow used for capital generation and selective growth funding.

| Product | 2024 Metric | Note |

|---|---|---|

| In‑force life | Renewal margin ~15% | Predictable lapses |

| Fixed annuities | Spreads 200–300 bps | Low promo, ALM focus |

| Group life/disability | Retention 92% | Low acquisition cost |

| Separate accounts | Fees 30–80 bps | High operating leverage |

Full Transparency, Always

Lincoln National BCG Matrix

The file you’re previewing is the exact Lincoln National BCG Matrix you’ll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report built for strategic clarity. Once bought, the full document is instantly downloadable and editable for presentations or planning. It’s professionally designed and market-informed, so there are no surprises—just plug-and-play analysis.

Download Your Competitive Advantage

The Lincoln National BCG Matrix snapshot shows which lines are fueling growth and which are tying up cash — a quick read that already spots Stars, Cash Cows, Dogs, and Question Marks in their portfolio. This preview teases the key moves; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis and an Excel summary you can present or act on immediately.

Stars

Indexed annuities momentum

Fixed indexed annuities are benefiting from higher interest rates (federal funds ~5.25–5.50% in 2024) and strong consumer demand for downside protection; Lincoln already holds meaningful share and can lean into product innovation and expanded distribution. These products consume capital for hedging and marketing, but continued premium growth supports the investment. Defend share now to graduate FIAs into durable earnings generators.

Indexed UL & protection-led life

IUL continues to outgrow traditional life as clients seek flexibility and cash-value upside, with LIMRA reporting roughly 10% year-over-year growth in IUL sales into 2024; Lincoln’s national franchise and wholesaler reach keep it near the front of the pack. It still needs targeted spend on pricing agility, underwriting tech, and expanded advisor education to capture share. Keep fueling it; the curve remains up-and-to-the-right.

Voluntary benefits in Group

Employers are expanding voluntary menus and employee opt-in rates rose to about 50% in mid-market in 2024, driving category expansion. Lincoln’s group platform can cross-sell life, accident and disability in one swing, leveraging bundled underwriting and payroll deduction. Success hinges on promotion, modern enrollment tech and broker engagement. Worth the push—category growth is doing the heavy lifting for unit economics.

Retirement plan services mid‑market

401(k) recordkeeping and managed accounts show steady inflows in 2024; auto-features boost participation by about 10 percentage points. Lincoln remains competitive in service and advisor-led distribution, serving roughly $300bn AUA (2024). Margins scale with assets, though onboarding and tech require heavy investment; continue capturing plans amid ongoing consolidation.

- auto-features:+10pp participation (2024)

- Lincoln AUA:≈$300bn (2024)

- margin scale with AUA

- onboarding/tech capex high

Worksite distribution scale

Worksite distribution is a star for Lincoln when enrollment is clean and digital, leveraging its national footprint to secure more RFPs and employer panels. High-touch broker relationships and ongoing education remain critical to convert scale into retention and cross-sell. Investing now to lock multi-year employer contracts preserves lifetime value and accelerates margin expansion.

Lock growth: FIA, IUL, and worksite 401(k) tech to win premiums and scale margins

Stars: FIAs (benefit from fed funds ~5.25–5.50% in 2024) and IUL (~10% YoY sales growth into 2024) plus worksite/401(k) (Lincoln AUA ≈$300bn; mid-market voluntary opt-in ~50%) drive premium and AUA growth; invest in product, distribution, and enrollment tech to lock share and scale margins.

| Product | 2024 Metric | Priority |

|---|---|---|

| FIA | Fed funds 5.25–5.50% | Hedge & innovate |

| IUL | ~10% YoY | Pricing & UW tech |

| 401(k)/Worksite | AUA ≈$300bn; opt-in ~50% | Enrollment tech |

What is included in the product

Concise strategic assessment of Lincoln National's products across BCG quadrants, showing where to invest, hold or divest.

One-page Lincoln BCG matrix placing each business unit in a quadrant to spot winners, underperformers and resource needs.

Cash Cows

In‑force life blocks

In‑force life blocks are Lincoln’s cash cows, producing stable margins and predictable fee income from seasoned books with well‑modeled lapse, mortality and expense assumptions. Minimal new sales spend is required—management focuses on experience management and capital allocation. Cash flow is systematically harvested to fund growth initiatives and to de‑risk the balance sheet.

Traditional fixed annuities

Traditional fixed annuities sit in Lincoln Nationals mature cash-cow bucket, serving loyal, conservative buyers with steady spreads typically around 200–300 basis points and lower sales churn versus variable products. Pricing discipline and tight asset-liability matching drive reliable earnings, with promotion light and retention-focused distribution. Continued optimization of operations and hedging is key to preserving those spreads amid 2024 rate volatility.

Group basic life & disability

Group basic life & disability is a cash cow for Lincoln, with sticky employer-paid coverage that yields low acquisition cost once installed and renewal margins in 2024 running in the mid-teens. Renewal economics and scale in claims management produce steady cash flow, supporting capital generation. Growth is modest but retention remains high, around 92% in 2024, so emphasis is on underwriting discipline and admin efficiency.

Separate account fees on annuities

Separate account fees on annuities generate steady asset-based revenue — typically in the industry range of 30 to 80 basis points — that hums along as balances compound; operating leverage is high once Lincoln’s platform is in place, so incremental AUM lifts margins. Market swings affect flows, but long-tenured accounts and sticky surrender behavior in 2024 help cushion volatility; maintain service quality and let AUM compounding do the work.

- steady-fee: asset-based fees 30–80 bps

- high-operating-leverage: fixed platform costs dilute

- sticky-aum: long-tenured accounts cushion 2024 market swings

- operational-focus: maintain service quality to compound AUM

Advisor & broker relationships

Lincoln’s advisor and broker relationships are cash cows: established channels lower marginal selling costs across life, annuity and investment products, with Deloitte 2024 finding advisers increase cross-sell revenue by ~35%, lifting customer lifetime value without heavy promotional spend.

The model is a durable moat so long as service levels remain high; Lincoln’s distribution focus preserves retention and unit economics, so maintain the relationship engine—steady investment, not overfunding.

- Lower marginal cost: repeat channel leverage

- Cross-sell lift: ~35% (Deloitte 2024)

- Durability: dependent on service quality

- Capex guidance: optimize, don’t overspend

In-force life, fixed annuities & group benefits: steady margins, strong cashflow in 2024

In‑force life blocks, traditional fixed annuities and group life/disability are Lincoln’s cash cows in 2024, delivering stable margins (renewal margins ~15%), annuity spreads ~200–300 bps and retention ~92%. Separate account fees (30–80 bps) and advisor channels (cross-sell +35%) provide steady, low‑cost cashflow used for capital generation and selective growth funding.

| Product | 2024 Metric | Note |

|---|---|---|

| In‑force life | Renewal margin ~15% | Predictable lapses |

| Fixed annuities | Spreads 200–300 bps | Low promo, ALM focus |

| Group life/disability | Retention 92% | Low acquisition cost |

| Separate accounts | Fees 30–80 bps | High operating leverage |

Full Transparency, Always

Lincoln National BCG Matrix

The file you’re previewing is the exact Lincoln National BCG Matrix you’ll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report built for strategic clarity. Once bought, the full document is instantly downloadable and editable for presentations or planning. It’s professionally designed and market-informed, so there are no surprises—just plug-and-play analysis.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

The Lincoln National BCG Matrix snapshot shows which lines are fueling growth and which are tying up cash — a quick read that already spots Stars, Cash Cows, Dogs, and Question Marks in their portfolio. This preview teases the key moves; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for capital allocation. Buy the complete report for a ready-to-use Word analysis and an Excel summary you can present or act on immediately.

Stars

Indexed annuities momentum

Fixed indexed annuities are benefiting from higher interest rates (federal funds ~5.25–5.50% in 2024) and strong consumer demand for downside protection; Lincoln already holds meaningful share and can lean into product innovation and expanded distribution. These products consume capital for hedging and marketing, but continued premium growth supports the investment. Defend share now to graduate FIAs into durable earnings generators.

Indexed UL & protection-led life

IUL continues to outgrow traditional life as clients seek flexibility and cash-value upside, with LIMRA reporting roughly 10% year-over-year growth in IUL sales into 2024; Lincoln’s national franchise and wholesaler reach keep it near the front of the pack. It still needs targeted spend on pricing agility, underwriting tech, and expanded advisor education to capture share. Keep fueling it; the curve remains up-and-to-the-right.

Voluntary benefits in Group

Employers are expanding voluntary menus and employee opt-in rates rose to about 50% in mid-market in 2024, driving category expansion. Lincoln’s group platform can cross-sell life, accident and disability in one swing, leveraging bundled underwriting and payroll deduction. Success hinges on promotion, modern enrollment tech and broker engagement. Worth the push—category growth is doing the heavy lifting for unit economics.

Retirement plan services mid‑market

401(k) recordkeeping and managed accounts show steady inflows in 2024; auto-features boost participation by about 10 percentage points. Lincoln remains competitive in service and advisor-led distribution, serving roughly $300bn AUA (2024). Margins scale with assets, though onboarding and tech require heavy investment; continue capturing plans amid ongoing consolidation.

- auto-features:+10pp participation (2024)

- Lincoln AUA:≈$300bn (2024)

- margin scale with AUA

- onboarding/tech capex high

Worksite distribution scale

Worksite distribution is a star for Lincoln when enrollment is clean and digital, leveraging its national footprint to secure more RFPs and employer panels. High-touch broker relationships and ongoing education remain critical to convert scale into retention and cross-sell. Investing now to lock multi-year employer contracts preserves lifetime value and accelerates margin expansion.

Lock growth: FIA, IUL, and worksite 401(k) tech to win premiums and scale margins

Stars: FIAs (benefit from fed funds ~5.25–5.50% in 2024) and IUL (~10% YoY sales growth into 2024) plus worksite/401(k) (Lincoln AUA ≈$300bn; mid-market voluntary opt-in ~50%) drive premium and AUA growth; invest in product, distribution, and enrollment tech to lock share and scale margins.

| Product | 2024 Metric | Priority |

|---|---|---|

| FIA | Fed funds 5.25–5.50% | Hedge & innovate |

| IUL | ~10% YoY | Pricing & UW tech |

| 401(k)/Worksite | AUA ≈$300bn; opt-in ~50% | Enrollment tech |

What is included in the product

Concise strategic assessment of Lincoln National's products across BCG quadrants, showing where to invest, hold or divest.

One-page Lincoln BCG matrix placing each business unit in a quadrant to spot winners, underperformers and resource needs.

Cash Cows

In‑force life blocks

In‑force life blocks are Lincoln’s cash cows, producing stable margins and predictable fee income from seasoned books with well‑modeled lapse, mortality and expense assumptions. Minimal new sales spend is required—management focuses on experience management and capital allocation. Cash flow is systematically harvested to fund growth initiatives and to de‑risk the balance sheet.

Traditional fixed annuities

Traditional fixed annuities sit in Lincoln Nationals mature cash-cow bucket, serving loyal, conservative buyers with steady spreads typically around 200–300 basis points and lower sales churn versus variable products. Pricing discipline and tight asset-liability matching drive reliable earnings, with promotion light and retention-focused distribution. Continued optimization of operations and hedging is key to preserving those spreads amid 2024 rate volatility.

Group basic life & disability

Group basic life & disability is a cash cow for Lincoln, with sticky employer-paid coverage that yields low acquisition cost once installed and renewal margins in 2024 running in the mid-teens. Renewal economics and scale in claims management produce steady cash flow, supporting capital generation. Growth is modest but retention remains high, around 92% in 2024, so emphasis is on underwriting discipline and admin efficiency.

Separate account fees on annuities

Separate account fees on annuities generate steady asset-based revenue — typically in the industry range of 30 to 80 basis points — that hums along as balances compound; operating leverage is high once Lincoln’s platform is in place, so incremental AUM lifts margins. Market swings affect flows, but long-tenured accounts and sticky surrender behavior in 2024 help cushion volatility; maintain service quality and let AUM compounding do the work.

- steady-fee: asset-based fees 30–80 bps

- high-operating-leverage: fixed platform costs dilute

- sticky-aum: long-tenured accounts cushion 2024 market swings

- operational-focus: maintain service quality to compound AUM

Advisor & broker relationships

Lincoln’s advisor and broker relationships are cash cows: established channels lower marginal selling costs across life, annuity and investment products, with Deloitte 2024 finding advisers increase cross-sell revenue by ~35%, lifting customer lifetime value without heavy promotional spend.

The model is a durable moat so long as service levels remain high; Lincoln’s distribution focus preserves retention and unit economics, so maintain the relationship engine—steady investment, not overfunding.

- Lower marginal cost: repeat channel leverage

- Cross-sell lift: ~35% (Deloitte 2024)

- Durability: dependent on service quality

- Capex guidance: optimize, don’t overspend

In-force life, fixed annuities & group benefits: steady margins, strong cashflow in 2024

In‑force life blocks, traditional fixed annuities and group life/disability are Lincoln’s cash cows in 2024, delivering stable margins (renewal margins ~15%), annuity spreads ~200–300 bps and retention ~92%. Separate account fees (30–80 bps) and advisor channels (cross-sell +35%) provide steady, low‑cost cashflow used for capital generation and selective growth funding.

| Product | 2024 Metric | Note |

|---|---|---|

| In‑force life | Renewal margin ~15% | Predictable lapses |

| Fixed annuities | Spreads 200–300 bps | Low promo, ALM focus |

| Group life/disability | Retention 92% | Low acquisition cost |

| Separate accounts | Fees 30–80 bps | High operating leverage |

Full Transparency, Always

Lincoln National BCG Matrix

The file you’re previewing is the exact Lincoln National BCG Matrix you’ll receive after purchase. No watermarks, no demo text—just a fully formatted, ready-to-use report built for strategic clarity. Once bought, the full document is instantly downloadable and editable for presentations or planning. It’s professionally designed and market-informed, so there are no surprises—just plug-and-play analysis.