LG Chem Boston Consulting Group Matrix

See the Bigger Picture

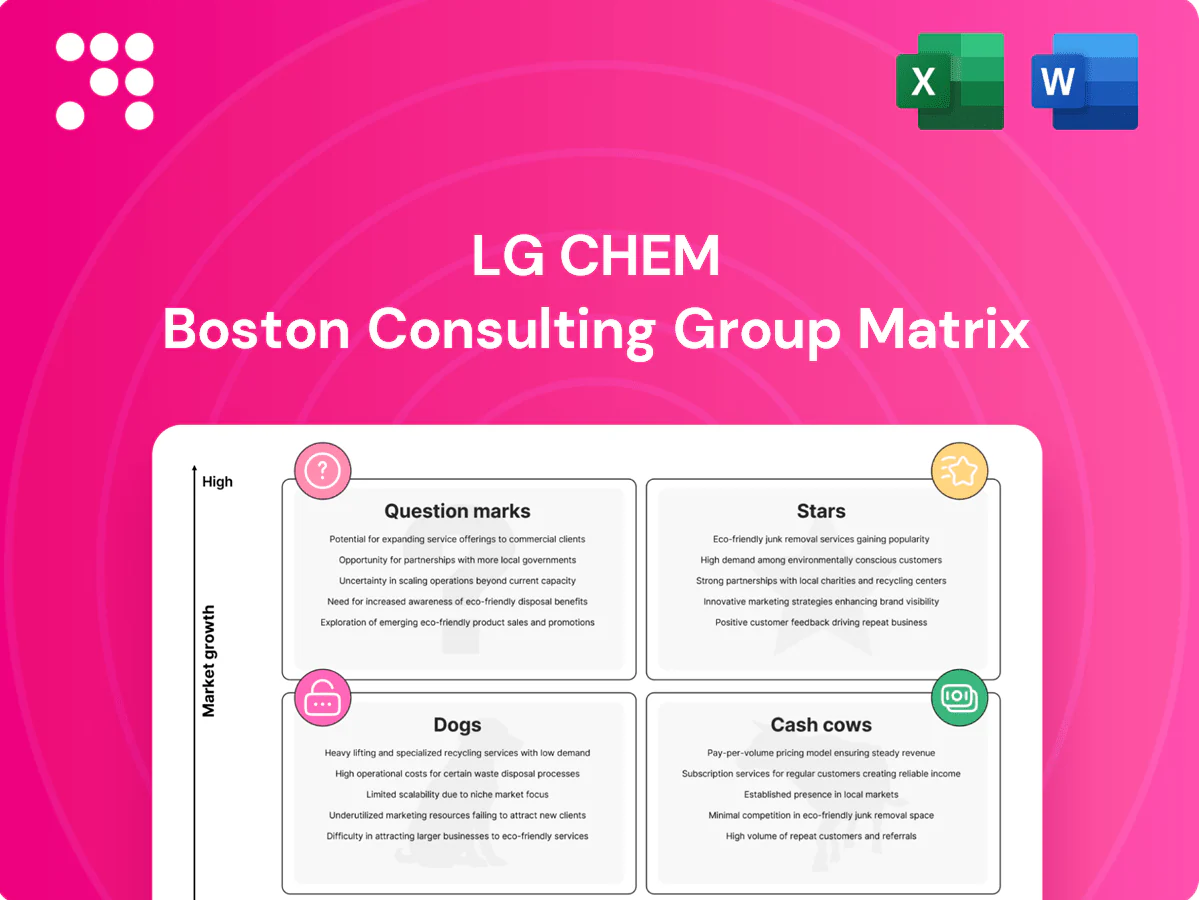

Curious where LG Chem’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the story, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a clear path for resource allocation. Buy the complete report to get a ready-to-use Word analysis plus an Excel summary that speeds decision-making. Grab it now and turn messy market signals into confident strategy.

Stars

EV cathode materials (NCM)

EV cathode materials (NCM) sit in the engine room of EV and ESS growth: NCM accounted for roughly 70% of global cathode demand in 2024 while EVs reached about 20% of new car sales that year, keeping markets racing. LG Chem’s share with blue‑chip OEMs is strong, but capacity build and qualification require continuous reinvestment—cash in equals cash out today. Keep the pedal down and these assets should mature into heavyweight cash generators.

Carbon nanotubes (conductive additives)

CNT demand is spiking as higher‑nickel and LFP cells push conductivity needs; the global CNT market was roughly $3.8bn in 2024 with an estimated ~12% CAGR to 2030, driven heavily by batteries. LG Chem is scaling fast and locking multi‑year supply contracts, securing spec‑in wins in a market that’s sprinting. Margins are healthy but capex‑hungry, so continued investment is needed to avoid commoditization and defend share.

POE for solar encapsulants

Global solar installations topped 400 GW in 2024, driving strong demand for durable encapsulants; POE is increasingly preferred over EVA for long-term module reliability, capturing over 20% of new-module uptake in 2024. LG Chem’s POE materials are qualified with multiple tier-1 module makers and show solid volume visibility into 2025. Growth is high and LG Chem holds meaningful share, though scaling requires working capital and line debottlenecking—act offensively while demand is strong.

Thermal-management engineering plastics

Thermal-management engineering plastics are a Stars segment as EVs and high-power electronics push demand for flame-retardant, thermally conductive resins; the global conductive plastics market showed double-digit growth entering 2024, driven by rising EV OEM requirements and power-electronics thermal loads. LG Chem’s portfolio outperforms on spec and reliability, giving a leadership wedge, but growth requires faster design-in and OEM application support to convert strong market momentum into share.

- Market trend: double-digit growth into 2024

- Strength: LG Chem specs/reliability

- Gap: design-in hustle & application support

- Action: stay close to OEMs; maintain hot pipeline

Battery binders & specialty additives

As energy density climbs, subtle chemistries decide performance. LG Chem’s binders and specialty additives ride the EV wave with sticky spec positions. Binders are typically under 5% of cell mass by weight but materially affect cycle life and safety, so application labs and IP protection keep the moat wide.

- Strategic: small share of cost, outsized impact

- Action: fund application labs for validation

- Defense: prioritize patents and trade secrets

High-growth materials: 70% NCM, $3.8bn CNT

LG Chem Stars (NCM cathodes, CNT, POE, thermal plastics, binders) drove high-growth volumes in 2024: NCM ~70% cathode demand, CNT market $3.8bn, solar >400GW installs, POE >20% new-module uptake. Strong OEM ties and specs; high capex and application support needed to convert growth into durable cash flows.

| Segment | 2024 metric | Market CAGR | Action |

|---|---|---|---|

| NCM | 70% cathode demand | ~15% EV era | Scale capacity |

| CNT | $3.8bn | ~12% to 2030 | Lock contracts |

What is included in the product

In-depth BCG Matrix review of LG Chem’s portfolio, spotting Stars, Cash Cows, Question Marks and Dogs with strategic invest/divest guidance.

One-page LG Chem BCG Matrix mapping business units into quadrants to simplify portfolio decisions and cut executive review time.

Cash Cows

ABS & styrenic resins

ABS and styrenic resins are mature, scale-heavy cash cows for LG Chem—the company ranks among the global leaders in styrenics and benefits from a roughly 9 Mtpa global ABS/styrenics market in 2024. Cyclical demand exists, but a steep cost curve advantage and high customer stickiness generate steady cash flow. Capex remains disciplined with emphasis on yield and product mix optimization. Cash generation is being directed to fund new energy investments.

PVC and general-purpose polyolefins

PVC and general-purpose polyolefins behave as cash cows for LG Chem: steady construction-driven PVC demand (roughly 2% CAGR) and olefins with about 90% plant utilization in 2024 provided resilient cash flow. LG Chem’s integrated petrochemical chain supported a petrochemical segment operating margin near 9% in 2024, cushioning cyclical feedstock swings. Low growth but logistics and utilization improvements convert volumes into strong free cash; keep plants efficient, keep cash flowing.

Naphtha cracking (ethylene chain)

Naphtha cracking (ethylene chain) is the backbone feeding LG Chem’s downstream PVC/PE/MEG streams, with typical naphtha-to-ethylene yields around 30–35% and steam-cracking energy intensity near 13 GJ/ton, so throughput reliability is critical. Scale and integration deliver per-ton cost leverage in normal cycles, making the unit an indispensable cash engine rather than a high-growth asset. Prioritize reliability and energy efficiency to widen the spread and protect margins.

Super Absorbent Polymer (SAP)

Super Absorbent Polymer (SAP) is a cash cow for LG Chem: the global SAP market was about USD 3.1 billion in 2024 and demand from diapers and hygiene—growing ~2% annually—is predictable, letting LG Chem, a top-5 global supplier, sustain volumes and cash returns.

Process know-how and rigorous quality control drive competitiveness more than buzz; low market growth and stable pricing translate to steady free cash flow, while incremental debottlenecking in 2023–24 preserved margins and operating leverage.

- Market size 2024: USD 3.1B

- End-market growth: ~2% CAGR (diapers/hygiene)

- Positioning: top-5 global supplier

- Strategy: debottlenecking + quality/process edge → stable margins

Industrial adhesives & coatings resins

Industrial adhesives and coatings resins are cash cows for LG Chem: large installed base, recurring specs and modest innovation cycles generate steady orders from electronics, packaging and construction while marketing spend remains light and ops excellence sustains margins; focus on harvesting cash, maintaining service levels and avoiding scope creep.

- Large installed base

- Recurring specs

- Low marketing spend

- Ops-driven margins

- Harvest, maintain service, avoid scope creep

Scale petrochemicals turn volumes into free cash for new energy, 9% margin

ABS/styrenics (9 Mtpa market in 2024), PVC/PO (≈2% CAGR demand) and SAP (USD 3.1B market in 2024) are LG Chem cash cows, delivering steady margins (petrochemical segment ~9% operating margin in 2024) and disciplined capex; scale, integration and ops excellence convert volumes into free cash, which funds new energy investments.

| Product | 2024 metric | Position | Notes |

|---|---|---|---|

| ABS/Styrenics | 9 Mtpa market | Global leader | Scale, stickiness |

| PVC/PO | ~2% CAGR | Integrated | High utilization |

| SAP | USD 3.1B | Top-5 | Stable demand |

Preview = Final Product

LG Chem BCG Matrix

The file you're previewing on this page is the exact LG Chem BCG Matrix report you'll receive after purchase — no watermarks, no placeholders. It’s the final, fully formatted document, built for clarity and immediate use in strategy meetings or investor decks. After buying, the same editable file is yours to download, print, or present without surprises. Crafted by analysts, it’s ready to plug straight into your planning workflow.

See the Bigger Picture

Curious where LG Chem’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the story, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a clear path for resource allocation. Buy the complete report to get a ready-to-use Word analysis plus an Excel summary that speeds decision-making. Grab it now and turn messy market signals into confident strategy.

Stars

EV cathode materials (NCM)

EV cathode materials (NCM) sit in the engine room of EV and ESS growth: NCM accounted for roughly 70% of global cathode demand in 2024 while EVs reached about 20% of new car sales that year, keeping markets racing. LG Chem’s share with blue‑chip OEMs is strong, but capacity build and qualification require continuous reinvestment—cash in equals cash out today. Keep the pedal down and these assets should mature into heavyweight cash generators.

Carbon nanotubes (conductive additives)

CNT demand is spiking as higher‑nickel and LFP cells push conductivity needs; the global CNT market was roughly $3.8bn in 2024 with an estimated ~12% CAGR to 2030, driven heavily by batteries. LG Chem is scaling fast and locking multi‑year supply contracts, securing spec‑in wins in a market that’s sprinting. Margins are healthy but capex‑hungry, so continued investment is needed to avoid commoditization and defend share.

POE for solar encapsulants

Global solar installations topped 400 GW in 2024, driving strong demand for durable encapsulants; POE is increasingly preferred over EVA for long-term module reliability, capturing over 20% of new-module uptake in 2024. LG Chem’s POE materials are qualified with multiple tier-1 module makers and show solid volume visibility into 2025. Growth is high and LG Chem holds meaningful share, though scaling requires working capital and line debottlenecking—act offensively while demand is strong.

Thermal-management engineering plastics

Thermal-management engineering plastics are a Stars segment as EVs and high-power electronics push demand for flame-retardant, thermally conductive resins; the global conductive plastics market showed double-digit growth entering 2024, driven by rising EV OEM requirements and power-electronics thermal loads. LG Chem’s portfolio outperforms on spec and reliability, giving a leadership wedge, but growth requires faster design-in and OEM application support to convert strong market momentum into share.

- Market trend: double-digit growth into 2024

- Strength: LG Chem specs/reliability

- Gap: design-in hustle & application support

- Action: stay close to OEMs; maintain hot pipeline

Battery binders & specialty additives

As energy density climbs, subtle chemistries decide performance. LG Chem’s binders and specialty additives ride the EV wave with sticky spec positions. Binders are typically under 5% of cell mass by weight but materially affect cycle life and safety, so application labs and IP protection keep the moat wide.

- Strategic: small share of cost, outsized impact

- Action: fund application labs for validation

- Defense: prioritize patents and trade secrets

High-growth materials: 70% NCM, $3.8bn CNT

LG Chem Stars (NCM cathodes, CNT, POE, thermal plastics, binders) drove high-growth volumes in 2024: NCM ~70% cathode demand, CNT market $3.8bn, solar >400GW installs, POE >20% new-module uptake. Strong OEM ties and specs; high capex and application support needed to convert growth into durable cash flows.

| Segment | 2024 metric | Market CAGR | Action |

|---|---|---|---|

| NCM | 70% cathode demand | ~15% EV era | Scale capacity |

| CNT | $3.8bn | ~12% to 2030 | Lock contracts |

What is included in the product

In-depth BCG Matrix review of LG Chem’s portfolio, spotting Stars, Cash Cows, Question Marks and Dogs with strategic invest/divest guidance.

One-page LG Chem BCG Matrix mapping business units into quadrants to simplify portfolio decisions and cut executive review time.

Cash Cows

ABS & styrenic resins

ABS and styrenic resins are mature, scale-heavy cash cows for LG Chem—the company ranks among the global leaders in styrenics and benefits from a roughly 9 Mtpa global ABS/styrenics market in 2024. Cyclical demand exists, but a steep cost curve advantage and high customer stickiness generate steady cash flow. Capex remains disciplined with emphasis on yield and product mix optimization. Cash generation is being directed to fund new energy investments.

PVC and general-purpose polyolefins

PVC and general-purpose polyolefins behave as cash cows for LG Chem: steady construction-driven PVC demand (roughly 2% CAGR) and olefins with about 90% plant utilization in 2024 provided resilient cash flow. LG Chem’s integrated petrochemical chain supported a petrochemical segment operating margin near 9% in 2024, cushioning cyclical feedstock swings. Low growth but logistics and utilization improvements convert volumes into strong free cash; keep plants efficient, keep cash flowing.

Naphtha cracking (ethylene chain)

Naphtha cracking (ethylene chain) is the backbone feeding LG Chem’s downstream PVC/PE/MEG streams, with typical naphtha-to-ethylene yields around 30–35% and steam-cracking energy intensity near 13 GJ/ton, so throughput reliability is critical. Scale and integration deliver per-ton cost leverage in normal cycles, making the unit an indispensable cash engine rather than a high-growth asset. Prioritize reliability and energy efficiency to widen the spread and protect margins.

Super Absorbent Polymer (SAP)

Super Absorbent Polymer (SAP) is a cash cow for LG Chem: the global SAP market was about USD 3.1 billion in 2024 and demand from diapers and hygiene—growing ~2% annually—is predictable, letting LG Chem, a top-5 global supplier, sustain volumes and cash returns.

Process know-how and rigorous quality control drive competitiveness more than buzz; low market growth and stable pricing translate to steady free cash flow, while incremental debottlenecking in 2023–24 preserved margins and operating leverage.

- Market size 2024: USD 3.1B

- End-market growth: ~2% CAGR (diapers/hygiene)

- Positioning: top-5 global supplier

- Strategy: debottlenecking + quality/process edge → stable margins

Industrial adhesives & coatings resins

Industrial adhesives and coatings resins are cash cows for LG Chem: large installed base, recurring specs and modest innovation cycles generate steady orders from electronics, packaging and construction while marketing spend remains light and ops excellence sustains margins; focus on harvesting cash, maintaining service levels and avoiding scope creep.

- Large installed base

- Recurring specs

- Low marketing spend

- Ops-driven margins

- Harvest, maintain service, avoid scope creep

Scale petrochemicals turn volumes into free cash for new energy, 9% margin

ABS/styrenics (9 Mtpa market in 2024), PVC/PO (≈2% CAGR demand) and SAP (USD 3.1B market in 2024) are LG Chem cash cows, delivering steady margins (petrochemical segment ~9% operating margin in 2024) and disciplined capex; scale, integration and ops excellence convert volumes into free cash, which funds new energy investments.

| Product | 2024 metric | Position | Notes |

|---|---|---|---|

| ABS/Styrenics | 9 Mtpa market | Global leader | Scale, stickiness |

| PVC/PO | ~2% CAGR | Integrated | High utilization |

| SAP | USD 3.1B | Top-5 | Stable demand |

Preview = Final Product

LG Chem BCG Matrix

The file you're previewing on this page is the exact LG Chem BCG Matrix report you'll receive after purchase — no watermarks, no placeholders. It’s the final, fully formatted document, built for clarity and immediate use in strategy meetings or investor decks. After buying, the same editable file is yours to download, print, or present without surprises. Crafted by analysts, it’s ready to plug straight into your planning workflow.

Description

See the Bigger Picture

Curious where LG Chem’s products sit—Stars, Cash Cows, Dogs, or Question Marks? This snapshot teases the story, but the full BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and a clear path for resource allocation. Buy the complete report to get a ready-to-use Word analysis plus an Excel summary that speeds decision-making. Grab it now and turn messy market signals into confident strategy.

Stars

EV cathode materials (NCM)

EV cathode materials (NCM) sit in the engine room of EV and ESS growth: NCM accounted for roughly 70% of global cathode demand in 2024 while EVs reached about 20% of new car sales that year, keeping markets racing. LG Chem’s share with blue‑chip OEMs is strong, but capacity build and qualification require continuous reinvestment—cash in equals cash out today. Keep the pedal down and these assets should mature into heavyweight cash generators.

Carbon nanotubes (conductive additives)

CNT demand is spiking as higher‑nickel and LFP cells push conductivity needs; the global CNT market was roughly $3.8bn in 2024 with an estimated ~12% CAGR to 2030, driven heavily by batteries. LG Chem is scaling fast and locking multi‑year supply contracts, securing spec‑in wins in a market that’s sprinting. Margins are healthy but capex‑hungry, so continued investment is needed to avoid commoditization and defend share.

POE for solar encapsulants

Global solar installations topped 400 GW in 2024, driving strong demand for durable encapsulants; POE is increasingly preferred over EVA for long-term module reliability, capturing over 20% of new-module uptake in 2024. LG Chem’s POE materials are qualified with multiple tier-1 module makers and show solid volume visibility into 2025. Growth is high and LG Chem holds meaningful share, though scaling requires working capital and line debottlenecking—act offensively while demand is strong.

Thermal-management engineering plastics

Thermal-management engineering plastics are a Stars segment as EVs and high-power electronics push demand for flame-retardant, thermally conductive resins; the global conductive plastics market showed double-digit growth entering 2024, driven by rising EV OEM requirements and power-electronics thermal loads. LG Chem’s portfolio outperforms on spec and reliability, giving a leadership wedge, but growth requires faster design-in and OEM application support to convert strong market momentum into share.

- Market trend: double-digit growth into 2024

- Strength: LG Chem specs/reliability

- Gap: design-in hustle & application support

- Action: stay close to OEMs; maintain hot pipeline

Battery binders & specialty additives

As energy density climbs, subtle chemistries decide performance. LG Chem’s binders and specialty additives ride the EV wave with sticky spec positions. Binders are typically under 5% of cell mass by weight but materially affect cycle life and safety, so application labs and IP protection keep the moat wide.

- Strategic: small share of cost, outsized impact

- Action: fund application labs for validation

- Defense: prioritize patents and trade secrets

High-growth materials: 70% NCM, $3.8bn CNT

LG Chem Stars (NCM cathodes, CNT, POE, thermal plastics, binders) drove high-growth volumes in 2024: NCM ~70% cathode demand, CNT market $3.8bn, solar >400GW installs, POE >20% new-module uptake. Strong OEM ties and specs; high capex and application support needed to convert growth into durable cash flows.

| Segment | 2024 metric | Market CAGR | Action |

|---|---|---|---|

| NCM | 70% cathode demand | ~15% EV era | Scale capacity |

| CNT | $3.8bn | ~12% to 2030 | Lock contracts |

What is included in the product

In-depth BCG Matrix review of LG Chem’s portfolio, spotting Stars, Cash Cows, Question Marks and Dogs with strategic invest/divest guidance.

One-page LG Chem BCG Matrix mapping business units into quadrants to simplify portfolio decisions and cut executive review time.

Cash Cows

ABS & styrenic resins

ABS and styrenic resins are mature, scale-heavy cash cows for LG Chem—the company ranks among the global leaders in styrenics and benefits from a roughly 9 Mtpa global ABS/styrenics market in 2024. Cyclical demand exists, but a steep cost curve advantage and high customer stickiness generate steady cash flow. Capex remains disciplined with emphasis on yield and product mix optimization. Cash generation is being directed to fund new energy investments.

PVC and general-purpose polyolefins

PVC and general-purpose polyolefins behave as cash cows for LG Chem: steady construction-driven PVC demand (roughly 2% CAGR) and olefins with about 90% plant utilization in 2024 provided resilient cash flow. LG Chem’s integrated petrochemical chain supported a petrochemical segment operating margin near 9% in 2024, cushioning cyclical feedstock swings. Low growth but logistics and utilization improvements convert volumes into strong free cash; keep plants efficient, keep cash flowing.

Naphtha cracking (ethylene chain)

Naphtha cracking (ethylene chain) is the backbone feeding LG Chem’s downstream PVC/PE/MEG streams, with typical naphtha-to-ethylene yields around 30–35% and steam-cracking energy intensity near 13 GJ/ton, so throughput reliability is critical. Scale and integration deliver per-ton cost leverage in normal cycles, making the unit an indispensable cash engine rather than a high-growth asset. Prioritize reliability and energy efficiency to widen the spread and protect margins.

Super Absorbent Polymer (SAP)

Super Absorbent Polymer (SAP) is a cash cow for LG Chem: the global SAP market was about USD 3.1 billion in 2024 and demand from diapers and hygiene—growing ~2% annually—is predictable, letting LG Chem, a top-5 global supplier, sustain volumes and cash returns.

Process know-how and rigorous quality control drive competitiveness more than buzz; low market growth and stable pricing translate to steady free cash flow, while incremental debottlenecking in 2023–24 preserved margins and operating leverage.

- Market size 2024: USD 3.1B

- End-market growth: ~2% CAGR (diapers/hygiene)

- Positioning: top-5 global supplier

- Strategy: debottlenecking + quality/process edge → stable margins

Industrial adhesives & coatings resins

Industrial adhesives and coatings resins are cash cows for LG Chem: large installed base, recurring specs and modest innovation cycles generate steady orders from electronics, packaging and construction while marketing spend remains light and ops excellence sustains margins; focus on harvesting cash, maintaining service levels and avoiding scope creep.

- Large installed base

- Recurring specs

- Low marketing spend

- Ops-driven margins

- Harvest, maintain service, avoid scope creep

Scale petrochemicals turn volumes into free cash for new energy, 9% margin

ABS/styrenics (9 Mtpa market in 2024), PVC/PO (≈2% CAGR demand) and SAP (USD 3.1B market in 2024) are LG Chem cash cows, delivering steady margins (petrochemical segment ~9% operating margin in 2024) and disciplined capex; scale, integration and ops excellence convert volumes into free cash, which funds new energy investments.

| Product | 2024 metric | Position | Notes |

|---|---|---|---|

| ABS/Styrenics | 9 Mtpa market | Global leader | Scale, stickiness |

| PVC/PO | ~2% CAGR | Integrated | High utilization |

| SAP | USD 3.1B | Top-5 | Stable demand |

Preview = Final Product

LG Chem BCG Matrix

The file you're previewing on this page is the exact LG Chem BCG Matrix report you'll receive after purchase — no watermarks, no placeholders. It’s the final, fully formatted document, built for clarity and immediate use in strategy meetings or investor decks. After buying, the same editable file is yours to download, print, or present without surprises. Crafted by analysts, it’s ready to plug straight into your planning workflow.