LG Display PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech breakthroughs are reshaping LG Display’s strategy and market position. This concise PESTLE snapshot highlights critical risks and growth levers to inform investment and strategic decisions. Buy the full analysis for a complete, actionable breakdown you can use immediately.

Political factors

Trade policy and tariffs

US–China trade tensions and Section 301 tariffs (up to 25% on many goods) directly affect component sourcing and end-market pricing for Korea-based LG Display, while the EU’s CBAM transition (phased 2023–25, full scope from 2026) and China’s variable tariff regimes create divergent landed-cost schedules. Changes in tariff lines and antidumping measures can compress margins or shift pricing in key markets. Proactive supply-chain diversification and tariff engineering are used to mitigate such shocks.

Geopolitical supply-chain risk

Regional flashpoints such as the Taiwan Strait and Korean Peninsula threaten semiconductor and display ecosystems where TSMC held about 53% of foundry share in 2024 and Samsung plus SK Hynix accounted for roughly 70% of DRAM supply in 2024, creating concentrated disruption risk. Logistics chokepoints—Strait of Malacca (~30% of global trade) and volatile air/sea lanes—can delay shipments. Business continuity planning and multi‑region suppliers materially improve resilience. Insurance cost rises and higher inventory buffers are now strategic levers.

Industrial policy and subsidies

US CHIPS Act ($52B) and IRA (~$369B) plus EU proposals (≈€43B) and Korea’s industrial packages (e.g., ₩510T pledges) offer grants/tax credits that can materially boost ROI on OLED/MicroLED capacity. Policy strings and local-content rules (domestic sourcing requirements) may force LG Display to reshape plant locations. Rivals securing subsidies shifts competitive dynamics and can distort pricing and investment timelines.

Export controls and tech restrictions

Tightening export controls since 2019 (notably ASML EUV restrictions) and expanded US measures in 2022–2023 constrain access to advanced lithography, vacuum‑deposition and inspection tools, raising licensing hurdles for LG Display and slowing process upgrades.

Increased compliance and licensing add measurable cost and lead‑time to fabs, while strategic partnerships with government‑approved suppliers and local tooling vendors reduce regulatory friction and procurement delays.

- ASML EUV ban since 2019 affecting advanced tool access

- Controls expanded 2022–2023 increasing licensing hurdles

- Approved‑supplier partnerships lower compliance costs and delays

Government standards in automotive

Public policies accelerating EV and ADAS adoption raise demand for in-car displays, with global EV sales exceeding 14 million in 2023 and China NEV share surpassing 30% in 2024, expanding opportunities for LG Display.

- Regulatory specs drive higher brightness, safety-grade luminance and redundancy requirements

- Local homologation creates variant and timing complexity, increasing R&D and inventory costs

- OEM collaborations align panels to evolving mandates and secure multi-year programs

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

US–China tariffs (Section 301 up to 25%) and regional tensions raise input costs and disruption risk; supply‑chain diversification reduces exposure. Subsidy programs (US CHIPS $52B, IRA ~$369B, EU ≈€43B, Korea ₩510T) shift capex and location decisions. Export controls (ASML EUV limits since 2019; tightened 2022–23) increase tooling lead times and compliance costs.

| Risk | 2024–25 Data |

|---|---|

| Tariffs | Section 301 up to 25% |

| Subsidies | CHIPS $52B; IRA ~$369B; EU ≈€43B; Korea ₩510T |

| Controls | ASML EUV ban since 2019; expansions 2022–23 |

What is included in the product

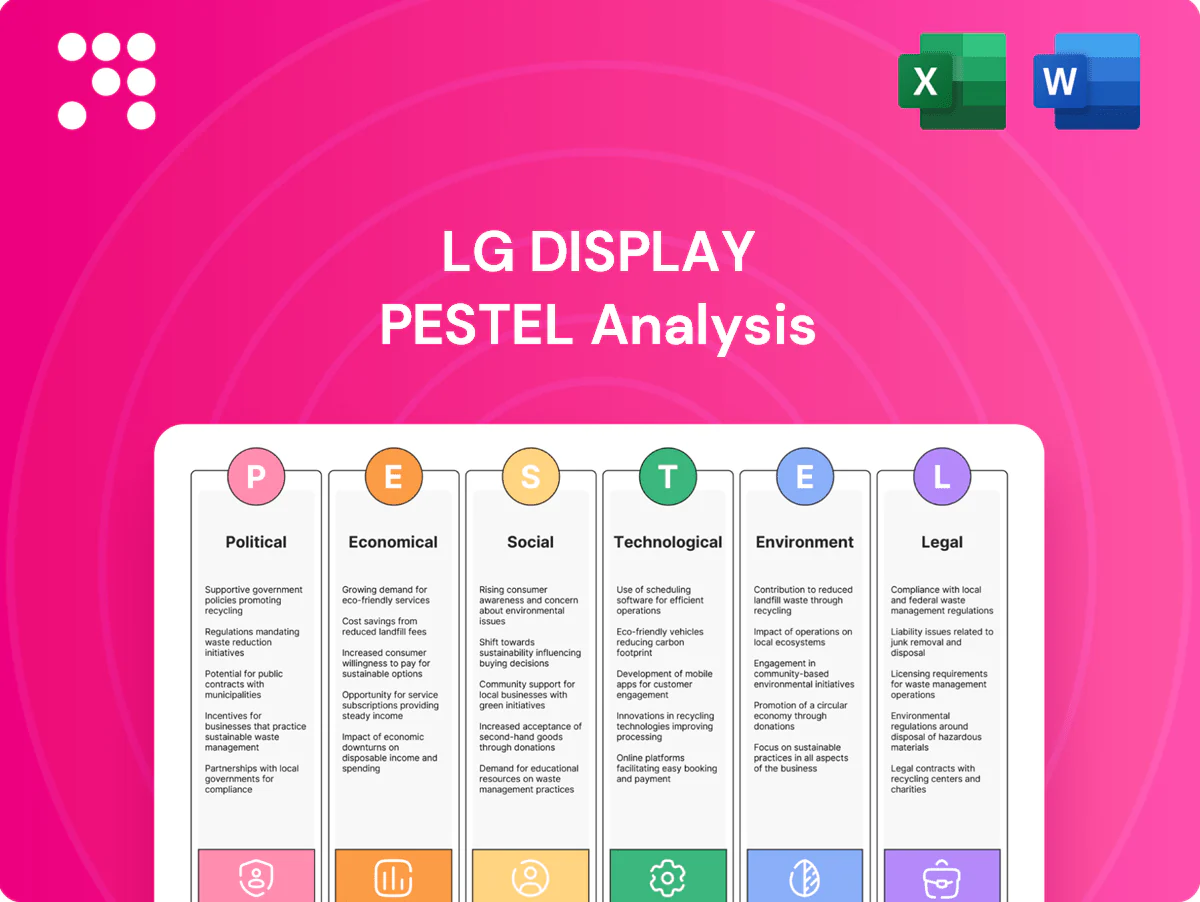

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact LG Display, combining data-driven trends and region-specific regulatory context. Designed for executives and investors, the analysis highlights risks, opportunities and forward-looking scenarios ready for business plans and pitches.

A concise, visually segmented PESTLE summary of LG Display for quick referencing in meetings or presentations, easily shared across teams and annotated to align on external risks, market positioning, and region-specific insights.

Economic factors

Display demand cyclicality

Consumer electronics demand for displays swings with GDP and discretionary income—global GDP grew about 3.1% in 2024 (IMF), driving uneven replacement cycles across TV, IT and mobile segments. These segments rarely peak together, so downturns compress panel utilization and ASPs, as seen in past cyclical drops. LG Display's flexible cost structure and mixed end-market exposure help stabilize revenues during such cycles.

Panel price volatility

Industry supply–demand imbalances produce sharp ASP swings in LCD and OLED, with large capacity additions from BOE and others triggering periodic price wars that pushed LCD TV panel ASPs down by double digits in 2023–24. LG Display mitigates margin erosion via long‑term contracts and product differentiation, while premium niches—OLED TV and automotive, where OLED panels fetch roughly 2–3x LCD prices—limit pure price competition.

Currency fluctuations

LG Display earns largely USD-linked revenues while key costs remain in KRW, JPY and CNY; as of mid-2025 FX rates were roughly USD/KRW 1,320, USD/JPY 155 and USD/CNY 7.3, so swings materially affect reported profits and price competitiveness. Hedging programs and natural currency offsets are essential to stabilize margins. Procurement and production locations in Korea, China and Vietnam shape net exposure and effectiveness of hedges.

Capital intensity and interest rates

Next-gen display fabs need multi-billion-dollar capex (typically $5–10bn) with extended payback periods; higher global rates (US fed funds ~5.25–5.5% mid-2025) push up WACC and required hurdle returns. Phased investments and JV partnerships help de-risk LG Display’s balance sheet, while strict utilization discipline is essential to protect ROIC.

- capex-range: $5–10bn

- rates-impact: fed funds ~5.25–5.5% (mid-2025)

- de-risk: phased capex & partnerships

- priority: utilization to defend ROIC

Input costs and energy

Glass substrates, OLED materials, driver ICs and logistics are major cost drivers for LG Display; capex was about KRW 4.6 trillion in 2024 supporting Gen‑8/10 fabs and OLED investments. Energy price spikes (electricity/gas up ~15–25% during 2022–23 peaks) raised cleanroom and vacuum process expenses, while long‑term supply contracts and efficiency upgrades compressed COGS volatility.

- Glass suppliers: top 3 control >60% global specialty glass capacity

- Energy: electricity/gas spikes ~15–25% (2022–23)

- Capex: KRW 4.6T (2024)

- Supplier consolidation improves bargaining power

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

Demand swings with GDP (~3.1% 2024 IMF) drive panel cycles; LGD's mixed end‑markets and long contracts damp volatility. ASPs remain volatile amid capacity additions; OLED premiums ~2–3x LCD protect niche margins. FX (USD/KRW ~1,320 mid‑2025) and KRW/JPY/CNY exposure materially affect reported profits; capex was KRW 4.6T (2024).

| Metric | Value |

|---|---|

| Global GDP 2024 | 3.1% |

| USD/KRW (mid‑2025) | ~1,320 |

| Fed funds (mid‑2025) | 5.25–5.5% |

| Capex 2024 | KRW 4.6T |

| OLED premium | 2–3x |

What You See Is What You Get

LG Display PESTLE Analysis

The LG Display PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, ready to use in reports or presentations. This real file reflects the final layout, content, and structure with no placeholders. Downloadable immediately upon payment—what you see is what you get.

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech breakthroughs are reshaping LG Display’s strategy and market position. This concise PESTLE snapshot highlights critical risks and growth levers to inform investment and strategic decisions. Buy the full analysis for a complete, actionable breakdown you can use immediately.

Political factors

Trade policy and tariffs

US–China trade tensions and Section 301 tariffs (up to 25% on many goods) directly affect component sourcing and end-market pricing for Korea-based LG Display, while the EU’s CBAM transition (phased 2023–25, full scope from 2026) and China’s variable tariff regimes create divergent landed-cost schedules. Changes in tariff lines and antidumping measures can compress margins or shift pricing in key markets. Proactive supply-chain diversification and tariff engineering are used to mitigate such shocks.

Geopolitical supply-chain risk

Regional flashpoints such as the Taiwan Strait and Korean Peninsula threaten semiconductor and display ecosystems where TSMC held about 53% of foundry share in 2024 and Samsung plus SK Hynix accounted for roughly 70% of DRAM supply in 2024, creating concentrated disruption risk. Logistics chokepoints—Strait of Malacca (~30% of global trade) and volatile air/sea lanes—can delay shipments. Business continuity planning and multi‑region suppliers materially improve resilience. Insurance cost rises and higher inventory buffers are now strategic levers.

Industrial policy and subsidies

US CHIPS Act ($52B) and IRA (~$369B) plus EU proposals (≈€43B) and Korea’s industrial packages (e.g., ₩510T pledges) offer grants/tax credits that can materially boost ROI on OLED/MicroLED capacity. Policy strings and local-content rules (domestic sourcing requirements) may force LG Display to reshape plant locations. Rivals securing subsidies shifts competitive dynamics and can distort pricing and investment timelines.

Export controls and tech restrictions

Tightening export controls since 2019 (notably ASML EUV restrictions) and expanded US measures in 2022–2023 constrain access to advanced lithography, vacuum‑deposition and inspection tools, raising licensing hurdles for LG Display and slowing process upgrades.

Increased compliance and licensing add measurable cost and lead‑time to fabs, while strategic partnerships with government‑approved suppliers and local tooling vendors reduce regulatory friction and procurement delays.

- ASML EUV ban since 2019 affecting advanced tool access

- Controls expanded 2022–2023 increasing licensing hurdles

- Approved‑supplier partnerships lower compliance costs and delays

Government standards in automotive

Public policies accelerating EV and ADAS adoption raise demand for in-car displays, with global EV sales exceeding 14 million in 2023 and China NEV share surpassing 30% in 2024, expanding opportunities for LG Display.

- Regulatory specs drive higher brightness, safety-grade luminance and redundancy requirements

- Local homologation creates variant and timing complexity, increasing R&D and inventory costs

- OEM collaborations align panels to evolving mandates and secure multi-year programs

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

US–China tariffs (Section 301 up to 25%) and regional tensions raise input costs and disruption risk; supply‑chain diversification reduces exposure. Subsidy programs (US CHIPS $52B, IRA ~$369B, EU ≈€43B, Korea ₩510T) shift capex and location decisions. Export controls (ASML EUV limits since 2019; tightened 2022–23) increase tooling lead times and compliance costs.

| Risk | 2024–25 Data |

|---|---|

| Tariffs | Section 301 up to 25% |

| Subsidies | CHIPS $52B; IRA ~$369B; EU ≈€43B; Korea ₩510T |

| Controls | ASML EUV ban since 2019; expansions 2022–23 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact LG Display, combining data-driven trends and region-specific regulatory context. Designed for executives and investors, the analysis highlights risks, opportunities and forward-looking scenarios ready for business plans and pitches.

A concise, visually segmented PESTLE summary of LG Display for quick referencing in meetings or presentations, easily shared across teams and annotated to align on external risks, market positioning, and region-specific insights.

Economic factors

Display demand cyclicality

Consumer electronics demand for displays swings with GDP and discretionary income—global GDP grew about 3.1% in 2024 (IMF), driving uneven replacement cycles across TV, IT and mobile segments. These segments rarely peak together, so downturns compress panel utilization and ASPs, as seen in past cyclical drops. LG Display's flexible cost structure and mixed end-market exposure help stabilize revenues during such cycles.

Panel price volatility

Industry supply–demand imbalances produce sharp ASP swings in LCD and OLED, with large capacity additions from BOE and others triggering periodic price wars that pushed LCD TV panel ASPs down by double digits in 2023–24. LG Display mitigates margin erosion via long‑term contracts and product differentiation, while premium niches—OLED TV and automotive, where OLED panels fetch roughly 2–3x LCD prices—limit pure price competition.

Currency fluctuations

LG Display earns largely USD-linked revenues while key costs remain in KRW, JPY and CNY; as of mid-2025 FX rates were roughly USD/KRW 1,320, USD/JPY 155 and USD/CNY 7.3, so swings materially affect reported profits and price competitiveness. Hedging programs and natural currency offsets are essential to stabilize margins. Procurement and production locations in Korea, China and Vietnam shape net exposure and effectiveness of hedges.

Capital intensity and interest rates

Next-gen display fabs need multi-billion-dollar capex (typically $5–10bn) with extended payback periods; higher global rates (US fed funds ~5.25–5.5% mid-2025) push up WACC and required hurdle returns. Phased investments and JV partnerships help de-risk LG Display’s balance sheet, while strict utilization discipline is essential to protect ROIC.

- capex-range: $5–10bn

- rates-impact: fed funds ~5.25–5.5% (mid-2025)

- de-risk: phased capex & partnerships

- priority: utilization to defend ROIC

Input costs and energy

Glass substrates, OLED materials, driver ICs and logistics are major cost drivers for LG Display; capex was about KRW 4.6 trillion in 2024 supporting Gen‑8/10 fabs and OLED investments. Energy price spikes (electricity/gas up ~15–25% during 2022–23 peaks) raised cleanroom and vacuum process expenses, while long‑term supply contracts and efficiency upgrades compressed COGS volatility.

- Glass suppliers: top 3 control >60% global specialty glass capacity

- Energy: electricity/gas spikes ~15–25% (2022–23)

- Capex: KRW 4.6T (2024)

- Supplier consolidation improves bargaining power

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

Demand swings with GDP (~3.1% 2024 IMF) drive panel cycles; LGD's mixed end‑markets and long contracts damp volatility. ASPs remain volatile amid capacity additions; OLED premiums ~2–3x LCD protect niche margins. FX (USD/KRW ~1,320 mid‑2025) and KRW/JPY/CNY exposure materially affect reported profits; capex was KRW 4.6T (2024).

| Metric | Value |

|---|---|

| Global GDP 2024 | 3.1% |

| USD/KRW (mid‑2025) | ~1,320 |

| Fed funds (mid‑2025) | 5.25–5.5% |

| Capex 2024 | KRW 4.6T |

| OLED premium | 2–3x |

What You See Is What You Get

LG Display PESTLE Analysis

The LG Display PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, ready to use in reports or presentations. This real file reflects the final layout, content, and structure with no placeholders. Downloadable immediately upon payment—what you see is what you get.

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic cycles, and tech breakthroughs are reshaping LG Display’s strategy and market position. This concise PESTLE snapshot highlights critical risks and growth levers to inform investment and strategic decisions. Buy the full analysis for a complete, actionable breakdown you can use immediately.

Political factors

Trade policy and tariffs

US–China trade tensions and Section 301 tariffs (up to 25% on many goods) directly affect component sourcing and end-market pricing for Korea-based LG Display, while the EU’s CBAM transition (phased 2023–25, full scope from 2026) and China’s variable tariff regimes create divergent landed-cost schedules. Changes in tariff lines and antidumping measures can compress margins or shift pricing in key markets. Proactive supply-chain diversification and tariff engineering are used to mitigate such shocks.

Geopolitical supply-chain risk

Regional flashpoints such as the Taiwan Strait and Korean Peninsula threaten semiconductor and display ecosystems where TSMC held about 53% of foundry share in 2024 and Samsung plus SK Hynix accounted for roughly 70% of DRAM supply in 2024, creating concentrated disruption risk. Logistics chokepoints—Strait of Malacca (~30% of global trade) and volatile air/sea lanes—can delay shipments. Business continuity planning and multi‑region suppliers materially improve resilience. Insurance cost rises and higher inventory buffers are now strategic levers.

Industrial policy and subsidies

US CHIPS Act ($52B) and IRA (~$369B) plus EU proposals (≈€43B) and Korea’s industrial packages (e.g., ₩510T pledges) offer grants/tax credits that can materially boost ROI on OLED/MicroLED capacity. Policy strings and local-content rules (domestic sourcing requirements) may force LG Display to reshape plant locations. Rivals securing subsidies shifts competitive dynamics and can distort pricing and investment timelines.

Export controls and tech restrictions

Tightening export controls since 2019 (notably ASML EUV restrictions) and expanded US measures in 2022–2023 constrain access to advanced lithography, vacuum‑deposition and inspection tools, raising licensing hurdles for LG Display and slowing process upgrades.

Increased compliance and licensing add measurable cost and lead‑time to fabs, while strategic partnerships with government‑approved suppliers and local tooling vendors reduce regulatory friction and procurement delays.

- ASML EUV ban since 2019 affecting advanced tool access

- Controls expanded 2022–2023 increasing licensing hurdles

- Approved‑supplier partnerships lower compliance costs and delays

Government standards in automotive

Public policies accelerating EV and ADAS adoption raise demand for in-car displays, with global EV sales exceeding 14 million in 2023 and China NEV share surpassing 30% in 2024, expanding opportunities for LG Display.

- Regulatory specs drive higher brightness, safety-grade luminance and redundancy requirements

- Local homologation creates variant and timing complexity, increasing R&D and inventory costs

- OEM collaborations align panels to evolving mandates and secure multi-year programs

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

US–China tariffs (Section 301 up to 25%) and regional tensions raise input costs and disruption risk; supply‑chain diversification reduces exposure. Subsidy programs (US CHIPS $52B, IRA ~$369B, EU ≈€43B, Korea ₩510T) shift capex and location decisions. Export controls (ASML EUV limits since 2019; tightened 2022–23) increase tooling lead times and compliance costs.

| Risk | 2024–25 Data |

|---|---|

| Tariffs | Section 301 up to 25% |

| Subsidies | CHIPS $52B; IRA ~$369B; EU ≈€43B; Korea ₩510T |

| Controls | ASML EUV ban since 2019; expansions 2022–23 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact LG Display, combining data-driven trends and region-specific regulatory context. Designed for executives and investors, the analysis highlights risks, opportunities and forward-looking scenarios ready for business plans and pitches.

A concise, visually segmented PESTLE summary of LG Display for quick referencing in meetings or presentations, easily shared across teams and annotated to align on external risks, market positioning, and region-specific insights.

Economic factors

Display demand cyclicality

Consumer electronics demand for displays swings with GDP and discretionary income—global GDP grew about 3.1% in 2024 (IMF), driving uneven replacement cycles across TV, IT and mobile segments. These segments rarely peak together, so downturns compress panel utilization and ASPs, as seen in past cyclical drops. LG Display's flexible cost structure and mixed end-market exposure help stabilize revenues during such cycles.

Panel price volatility

Industry supply–demand imbalances produce sharp ASP swings in LCD and OLED, with large capacity additions from BOE and others triggering periodic price wars that pushed LCD TV panel ASPs down by double digits in 2023–24. LG Display mitigates margin erosion via long‑term contracts and product differentiation, while premium niches—OLED TV and automotive, where OLED panels fetch roughly 2–3x LCD prices—limit pure price competition.

Currency fluctuations

LG Display earns largely USD-linked revenues while key costs remain in KRW, JPY and CNY; as of mid-2025 FX rates were roughly USD/KRW 1,320, USD/JPY 155 and USD/CNY 7.3, so swings materially affect reported profits and price competitiveness. Hedging programs and natural currency offsets are essential to stabilize margins. Procurement and production locations in Korea, China and Vietnam shape net exposure and effectiveness of hedges.

Capital intensity and interest rates

Next-gen display fabs need multi-billion-dollar capex (typically $5–10bn) with extended payback periods; higher global rates (US fed funds ~5.25–5.5% mid-2025) push up WACC and required hurdle returns. Phased investments and JV partnerships help de-risk LG Display’s balance sheet, while strict utilization discipline is essential to protect ROIC.

- capex-range: $5–10bn

- rates-impact: fed funds ~5.25–5.5% (mid-2025)

- de-risk: phased capex & partnerships

- priority: utilization to defend ROIC

Input costs and energy

Glass substrates, OLED materials, driver ICs and logistics are major cost drivers for LG Display; capex was about KRW 4.6 trillion in 2024 supporting Gen‑8/10 fabs and OLED investments. Energy price spikes (electricity/gas up ~15–25% during 2022–23 peaks) raised cleanroom and vacuum process expenses, while long‑term supply contracts and efficiency upgrades compressed COGS volatility.

- Glass suppliers: top 3 control >60% global specialty glass capacity

- Energy: electricity/gas spikes ~15–25% (2022–23)

- Capex: KRW 4.6T (2024)

- Supplier consolidation improves bargaining power

Tariffs, export controls and subsidies reshape chip supply chains and capex decisions

Demand swings with GDP (~3.1% 2024 IMF) drive panel cycles; LGD's mixed end‑markets and long contracts damp volatility. ASPs remain volatile amid capacity additions; OLED premiums ~2–3x LCD protect niche margins. FX (USD/KRW ~1,320 mid‑2025) and KRW/JPY/CNY exposure materially affect reported profits; capex was KRW 4.6T (2024).

| Metric | Value |

|---|---|

| Global GDP 2024 | 3.1% |

| USD/KRW (mid‑2025) | ~1,320 |

| Fed funds (mid‑2025) | 5.25–5.5% |

| Capex 2024 | KRW 4.6T |

| OLED premium | 2–3x |

What You See Is What You Get

LG Display PESTLE Analysis

The LG Display PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase, ready to use in reports or presentations. This real file reflects the final layout, content, and structure with no placeholders. Downloadable immediately upon payment—what you see is what you get.