LG Household & Health Care Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

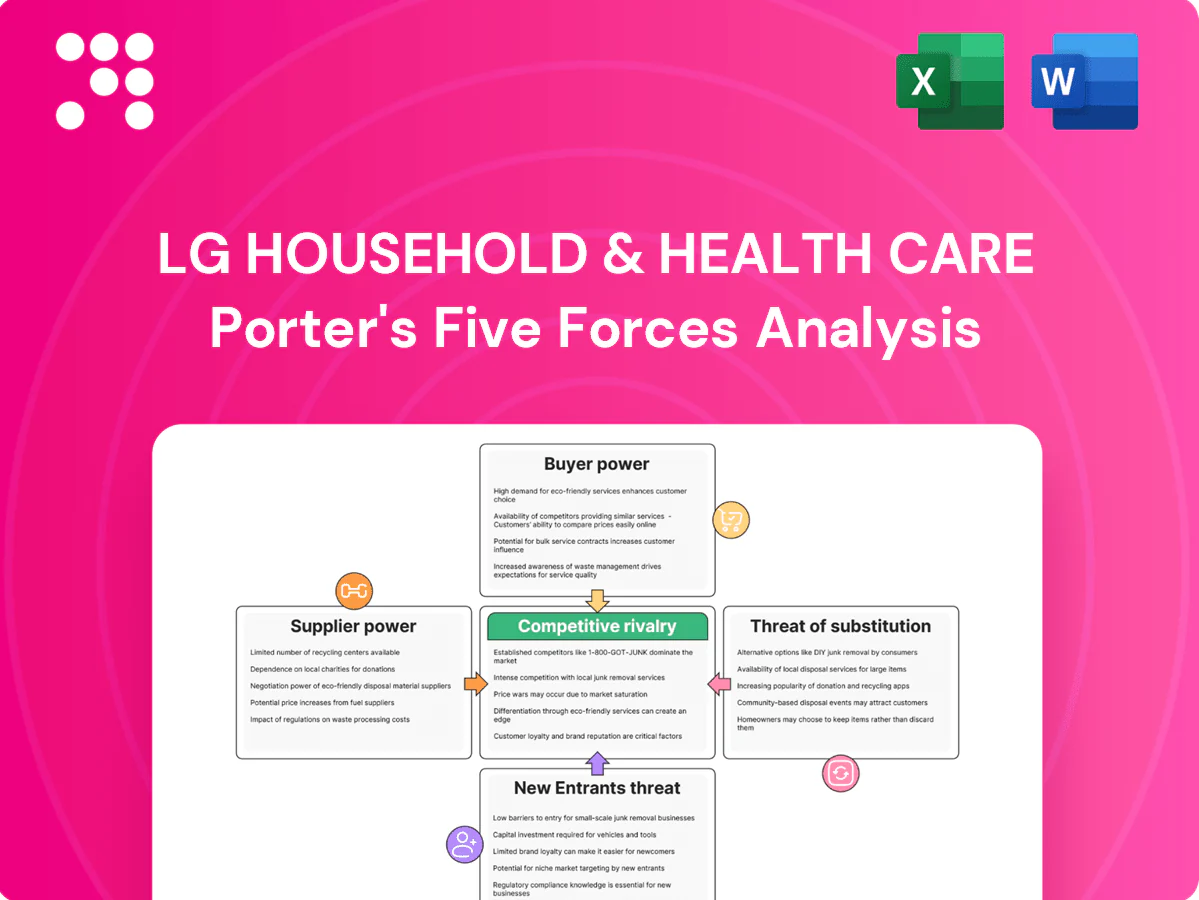

LG Household & Health Care faces intense rivalry in beauty and household segments, moderate supplier power, rising buyer expectations, manageable threat of new entrants, and growing substitution risks from global indie brands; this snapshot highlights key tensions. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals, and strategic implications. Unlock the complete report to inform confident investment and strategy decisions.

Suppliers Bargaining Power

Diverse raw-material base

LG H&H sources petrochemicals, surfactants, botanicals, fragrances and beverage inputs from numerous global vendors, creating a diverse raw-material base. This broad supplier pool reduces individual supplier leverage and helps maintain competitive input pricing. However, commodity volatility in oil, paper and sugar can transmit cost shocks to margins, which LG H&H mitigates through long-term contracts and hedging strategies.

Specialty actives concentration

High-performance actives, biotech ferments and patented delivery systems for LG Household & Health Care are concentrated among a few specialty suppliers and ODM partners, raising switching costs and lengthening lead times. This concentration creates higher input pricing and allocation risk for hero products, affecting gross margins and launch timing. Co-development and exclusivity deals mitigate supply risk but increase long-term dependence on those partners. Suppliers’ pricing power therefore intensifies procurement leverage and operational vulnerability.

Packaging and logistics leverage

Premium packaging (airless pumps, glass, sustainable resins) and 2024 freight constraints can boost supplier leverage by raising unit costs and lead times; the global beauty packaging market was about $39 billion in 2024, concentrating volume with specialist suppliers. Tight capacity during demand surges elevates lead times and spot freight rates, increasing procurement drag. Multi-sourcing and regionalized logistics reduce this leverage, while design-to-value shifts specs to lower-cost materials without harming brand perception.

Compliance and ESG requirements

Rising standards for clean ingredients, recyclability and traceability are narrowing LG Household & Health Cares qualified supplier pool, increasing supplier differentiation and bargaining power; non-compliant suppliers create regulatory and reputational risk. Joint audits and supplier development programs preserve procurement options and mitigate supply disruptions.

- Supplier pool: restricted

- ESG compliance: increases bargaining power

- Non-compliance: regulatory & reputational risk

- Mitigation: joint audits, development programs

ODM/OEM dependencies

Select skincare and color cosmetics lines depend on ODMs for formulation agility and speed to market, with LG H&H using external partners for roughly 35% of new SKU launches in 2024, giving trend-leading ODMs measurable leverage.

Knowledge lock-in from proprietary libraries raises replacement friction and switching costs, while LG H&H’s incremental in‑house R&D spend and dual‑qualifying manufacturers in 2024 reduced single‑supplier exposure.

- ODM reliance: ~35% of new SKUs (2024)

- Trend-library leverage: increases negotiation power

- Knowledge lock-in: higher switching costs

- Mitigants: higher R&D spend, dual qualification

Beauty sector sees rising supplier power: ODMs, specialty actives and packaging tighten supply

LG H&H faces moderate-to-high supplier power: diverse commodity vendors limit leverage, but specialty actives, premium packaging and ODMs concentrate power (35% of new SKUs in 2024). ESG and traceability narrow qualified suppliers; long‑term contracts, hedges and dual‑qualification partially mitigate margin risk.

| Metric | 2024 |

|---|---|

| ODM share new SKUs | 35% |

| Beauty packaging market | $39B |

| Supplier pool | Restricted (ESG) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to LG Household & Health Care, identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power, pricing pressures, and barriers that protect incumbency for strategic planning and investor analysis.

A concise Porter's Five Forces snapshot tailored to LG Household & Health Care—pinpoints supplier and retailer leverage, private-label and online entrant threats, regulatory pressure, and shifting consumer power to quickly surface strategic pain points and prioritize actions.

Customers Bargaining Power

Retailer consolidation

Retailer consolidation gives large chains, duty-free operators and convenience channels outsized leverage to push for lower prices, stricter payment terms and premium shelf allocation, driving higher trade spend and private-label initiatives that compress margins in LG Household & Health Care’s mature beauty and household segments. Their scale forces manufacturers into joint business planning and promotional funding agreements. Securing exclusive SKUs and category-specific partnerships helps LG H&H rebalance negotiating power and protect margins.

Platform-driven transparency

E-commerce and social platforms enable instant price comparisons and user reviews, amplified by South Korea’s 96% internet penetration in 2024 (ITU), increasing visibility into LG H&H pricing. Low switching costs raise price sensitivity and reliance on promotions. Algorithmic exposure on marketplaces and feeds can rapidly shift demand, while DTC data and loyalty programs help stabilize repeat purchases by enabling targeted retention.

Trend-driven beauty consumers

Trend-driven K-beauty consumers relentlessly trial new SKUs and abandon quickly; in 2024 surveys over 60% of Korean beauty buyers reported trying new products monthly, amplifying bargaining power. Influencer-driven spikes can reallocate category share overnight, forcing LG Household & Health Care to sustain a high innovation cadence and frequent NPD to retain attention and margin.

Institutional buyers in refreshment

Institutional buyers in refreshment—foodservice and vending operators—bundle negotiations across multiple beverage SKUs, increasing leverage on pricing, slotting fees and rebates; high volume concentration means a few large operators can demand deeper discounts. Multi-year contracts smooth demand but lock LG H&H into terms, while LG H&H’s broad portfolio strengthens its negotiating position by offering scale and promotional flexibility.

- Bundle negotiations raise buyer leverage

- Volume concentration amplifies discount pressure

- Contracts smooth demand but limit pricing flexibility

- Portfolio breadth improves LG H&H’s countervailing power

Private label and indie options

Proliferation of private label and indie brands gives buyers credible alternatives, allowing retailers to swap shelf facings quickly if velocity lags and compressing LG Household & Health Care pricing power; differentiated claims and strong brand equity are therefore essential to resist down‑trading. Incumbents must invest in innovation, storytelling and premium positioning to retain margin and shelf space.

- Private label competition: credible alternative

- Retailer agility: quick shelf replacement

- Pressure on pricing power

- Defense: differentiated claims + brand equity

Retailer consolidation squeezes margins; exclusive SKUs and faster NPD amid 96% online, ~60% try new

Retailer consolidation forces deeper trade spend and stricter terms, pressuring margins while LG H&H uses exclusive SKUs to regain leverage. 96% internet penetration in 2024 and ~60% of Korean beauty buyers trying new products monthly raise price sensitivity and churn. Private-label and indie growth increase retailer switching power, requiring stronger branding and faster NPD.

| Driver | Metric (2024) |

|---|---|

| Internet penetration | 96% (ITU) |

| Monthly product trial | ~60% (2024 survey) |

Same Document Delivered

LG Household & Health Care Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of LG Household & Health Care you'll receive—fully written, formatted, and ready to download upon purchase. No placeholders or samples: the content shown here is the final deliverable. Buy once and get instant access to this identical file for your analysis needs.

Go Beyond the Preview—Access the Full Strategic Report

LG Household & Health Care faces intense rivalry in beauty and household segments, moderate supplier power, rising buyer expectations, manageable threat of new entrants, and growing substitution risks from global indie brands; this snapshot highlights key tensions. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals, and strategic implications. Unlock the complete report to inform confident investment and strategy decisions.

Suppliers Bargaining Power

Diverse raw-material base

LG H&H sources petrochemicals, surfactants, botanicals, fragrances and beverage inputs from numerous global vendors, creating a diverse raw-material base. This broad supplier pool reduces individual supplier leverage and helps maintain competitive input pricing. However, commodity volatility in oil, paper and sugar can transmit cost shocks to margins, which LG H&H mitigates through long-term contracts and hedging strategies.

Specialty actives concentration

High-performance actives, biotech ferments and patented delivery systems for LG Household & Health Care are concentrated among a few specialty suppliers and ODM partners, raising switching costs and lengthening lead times. This concentration creates higher input pricing and allocation risk for hero products, affecting gross margins and launch timing. Co-development and exclusivity deals mitigate supply risk but increase long-term dependence on those partners. Suppliers’ pricing power therefore intensifies procurement leverage and operational vulnerability.

Packaging and logistics leverage

Premium packaging (airless pumps, glass, sustainable resins) and 2024 freight constraints can boost supplier leverage by raising unit costs and lead times; the global beauty packaging market was about $39 billion in 2024, concentrating volume with specialist suppliers. Tight capacity during demand surges elevates lead times and spot freight rates, increasing procurement drag. Multi-sourcing and regionalized logistics reduce this leverage, while design-to-value shifts specs to lower-cost materials without harming brand perception.

Compliance and ESG requirements

Rising standards for clean ingredients, recyclability and traceability are narrowing LG Household & Health Cares qualified supplier pool, increasing supplier differentiation and bargaining power; non-compliant suppliers create regulatory and reputational risk. Joint audits and supplier development programs preserve procurement options and mitigate supply disruptions.

- Supplier pool: restricted

- ESG compliance: increases bargaining power

- Non-compliance: regulatory & reputational risk

- Mitigation: joint audits, development programs

ODM/OEM dependencies

Select skincare and color cosmetics lines depend on ODMs for formulation agility and speed to market, with LG H&H using external partners for roughly 35% of new SKU launches in 2024, giving trend-leading ODMs measurable leverage.

Knowledge lock-in from proprietary libraries raises replacement friction and switching costs, while LG H&H’s incremental in‑house R&D spend and dual‑qualifying manufacturers in 2024 reduced single‑supplier exposure.

- ODM reliance: ~35% of new SKUs (2024)

- Trend-library leverage: increases negotiation power

- Knowledge lock-in: higher switching costs

- Mitigants: higher R&D spend, dual qualification

Beauty sector sees rising supplier power: ODMs, specialty actives and packaging tighten supply

LG H&H faces moderate-to-high supplier power: diverse commodity vendors limit leverage, but specialty actives, premium packaging and ODMs concentrate power (35% of new SKUs in 2024). ESG and traceability narrow qualified suppliers; long‑term contracts, hedges and dual‑qualification partially mitigate margin risk.

| Metric | 2024 |

|---|---|

| ODM share new SKUs | 35% |

| Beauty packaging market | $39B |

| Supplier pool | Restricted (ESG) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to LG Household & Health Care, identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power, pricing pressures, and barriers that protect incumbency for strategic planning and investor analysis.

A concise Porter's Five Forces snapshot tailored to LG Household & Health Care—pinpoints supplier and retailer leverage, private-label and online entrant threats, regulatory pressure, and shifting consumer power to quickly surface strategic pain points and prioritize actions.

Customers Bargaining Power

Retailer consolidation

Retailer consolidation gives large chains, duty-free operators and convenience channels outsized leverage to push for lower prices, stricter payment terms and premium shelf allocation, driving higher trade spend and private-label initiatives that compress margins in LG Household & Health Care’s mature beauty and household segments. Their scale forces manufacturers into joint business planning and promotional funding agreements. Securing exclusive SKUs and category-specific partnerships helps LG H&H rebalance negotiating power and protect margins.

Platform-driven transparency

E-commerce and social platforms enable instant price comparisons and user reviews, amplified by South Korea’s 96% internet penetration in 2024 (ITU), increasing visibility into LG H&H pricing. Low switching costs raise price sensitivity and reliance on promotions. Algorithmic exposure on marketplaces and feeds can rapidly shift demand, while DTC data and loyalty programs help stabilize repeat purchases by enabling targeted retention.

Trend-driven beauty consumers

Trend-driven K-beauty consumers relentlessly trial new SKUs and abandon quickly; in 2024 surveys over 60% of Korean beauty buyers reported trying new products monthly, amplifying bargaining power. Influencer-driven spikes can reallocate category share overnight, forcing LG Household & Health Care to sustain a high innovation cadence and frequent NPD to retain attention and margin.

Institutional buyers in refreshment

Institutional buyers in refreshment—foodservice and vending operators—bundle negotiations across multiple beverage SKUs, increasing leverage on pricing, slotting fees and rebates; high volume concentration means a few large operators can demand deeper discounts. Multi-year contracts smooth demand but lock LG H&H into terms, while LG H&H’s broad portfolio strengthens its negotiating position by offering scale and promotional flexibility.

- Bundle negotiations raise buyer leverage

- Volume concentration amplifies discount pressure

- Contracts smooth demand but limit pricing flexibility

- Portfolio breadth improves LG H&H’s countervailing power

Private label and indie options

Proliferation of private label and indie brands gives buyers credible alternatives, allowing retailers to swap shelf facings quickly if velocity lags and compressing LG Household & Health Care pricing power; differentiated claims and strong brand equity are therefore essential to resist down‑trading. Incumbents must invest in innovation, storytelling and premium positioning to retain margin and shelf space.

- Private label competition: credible alternative

- Retailer agility: quick shelf replacement

- Pressure on pricing power

- Defense: differentiated claims + brand equity

Retailer consolidation squeezes margins; exclusive SKUs and faster NPD amid 96% online, ~60% try new

Retailer consolidation forces deeper trade spend and stricter terms, pressuring margins while LG H&H uses exclusive SKUs to regain leverage. 96% internet penetration in 2024 and ~60% of Korean beauty buyers trying new products monthly raise price sensitivity and churn. Private-label and indie growth increase retailer switching power, requiring stronger branding and faster NPD.

| Driver | Metric (2024) |

|---|---|

| Internet penetration | 96% (ITU) |

| Monthly product trial | ~60% (2024 survey) |

Same Document Delivered

LG Household & Health Care Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of LG Household & Health Care you'll receive—fully written, formatted, and ready to download upon purchase. No placeholders or samples: the content shown here is the final deliverable. Buy once and get instant access to this identical file for your analysis needs.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

LG Household & Health Care faces intense rivalry in beauty and household segments, moderate supplier power, rising buyer expectations, manageable threat of new entrants, and growing substitution risks from global indie brands; this snapshot highlights key tensions. The full Porter's Five Forces Analysis unpacks force-by-force ratings, visuals, and strategic implications. Unlock the complete report to inform confident investment and strategy decisions.

Suppliers Bargaining Power

Diverse raw-material base

LG H&H sources petrochemicals, surfactants, botanicals, fragrances and beverage inputs from numerous global vendors, creating a diverse raw-material base. This broad supplier pool reduces individual supplier leverage and helps maintain competitive input pricing. However, commodity volatility in oil, paper and sugar can transmit cost shocks to margins, which LG H&H mitigates through long-term contracts and hedging strategies.

Specialty actives concentration

High-performance actives, biotech ferments and patented delivery systems for LG Household & Health Care are concentrated among a few specialty suppliers and ODM partners, raising switching costs and lengthening lead times. This concentration creates higher input pricing and allocation risk for hero products, affecting gross margins and launch timing. Co-development and exclusivity deals mitigate supply risk but increase long-term dependence on those partners. Suppliers’ pricing power therefore intensifies procurement leverage and operational vulnerability.

Packaging and logistics leverage

Premium packaging (airless pumps, glass, sustainable resins) and 2024 freight constraints can boost supplier leverage by raising unit costs and lead times; the global beauty packaging market was about $39 billion in 2024, concentrating volume with specialist suppliers. Tight capacity during demand surges elevates lead times and spot freight rates, increasing procurement drag. Multi-sourcing and regionalized logistics reduce this leverage, while design-to-value shifts specs to lower-cost materials without harming brand perception.

Compliance and ESG requirements

Rising standards for clean ingredients, recyclability and traceability are narrowing LG Household & Health Cares qualified supplier pool, increasing supplier differentiation and bargaining power; non-compliant suppliers create regulatory and reputational risk. Joint audits and supplier development programs preserve procurement options and mitigate supply disruptions.

- Supplier pool: restricted

- ESG compliance: increases bargaining power

- Non-compliance: regulatory & reputational risk

- Mitigation: joint audits, development programs

ODM/OEM dependencies

Select skincare and color cosmetics lines depend on ODMs for formulation agility and speed to market, with LG H&H using external partners for roughly 35% of new SKU launches in 2024, giving trend-leading ODMs measurable leverage.

Knowledge lock-in from proprietary libraries raises replacement friction and switching costs, while LG H&H’s incremental in‑house R&D spend and dual‑qualifying manufacturers in 2024 reduced single‑supplier exposure.

- ODM reliance: ~35% of new SKUs (2024)

- Trend-library leverage: increases negotiation power

- Knowledge lock-in: higher switching costs

- Mitigants: higher R&D spend, dual qualification

Beauty sector sees rising supplier power: ODMs, specialty actives and packaging tighten supply

LG H&H faces moderate-to-high supplier power: diverse commodity vendors limit leverage, but specialty actives, premium packaging and ODMs concentrate power (35% of new SKUs in 2024). ESG and traceability narrow qualified suppliers; long‑term contracts, hedges and dual‑qualification partially mitigate margin risk.

| Metric | 2024 |

|---|---|

| ODM share new SKUs | 35% |

| Beauty packaging market | $39B |

| Supplier pool | Restricted (ESG) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to LG Household & Health Care, identifying disruptive substitutes and emerging threats to market share. Evaluates supplier and buyer power, pricing pressures, and barriers that protect incumbency for strategic planning and investor analysis.

A concise Porter's Five Forces snapshot tailored to LG Household & Health Care—pinpoints supplier and retailer leverage, private-label and online entrant threats, regulatory pressure, and shifting consumer power to quickly surface strategic pain points and prioritize actions.

Customers Bargaining Power

Retailer consolidation

Retailer consolidation gives large chains, duty-free operators and convenience channels outsized leverage to push for lower prices, stricter payment terms and premium shelf allocation, driving higher trade spend and private-label initiatives that compress margins in LG Household & Health Care’s mature beauty and household segments. Their scale forces manufacturers into joint business planning and promotional funding agreements. Securing exclusive SKUs and category-specific partnerships helps LG H&H rebalance negotiating power and protect margins.

Platform-driven transparency

E-commerce and social platforms enable instant price comparisons and user reviews, amplified by South Korea’s 96% internet penetration in 2024 (ITU), increasing visibility into LG H&H pricing. Low switching costs raise price sensitivity and reliance on promotions. Algorithmic exposure on marketplaces and feeds can rapidly shift demand, while DTC data and loyalty programs help stabilize repeat purchases by enabling targeted retention.

Trend-driven beauty consumers

Trend-driven K-beauty consumers relentlessly trial new SKUs and abandon quickly; in 2024 surveys over 60% of Korean beauty buyers reported trying new products monthly, amplifying bargaining power. Influencer-driven spikes can reallocate category share overnight, forcing LG Household & Health Care to sustain a high innovation cadence and frequent NPD to retain attention and margin.

Institutional buyers in refreshment

Institutional buyers in refreshment—foodservice and vending operators—bundle negotiations across multiple beverage SKUs, increasing leverage on pricing, slotting fees and rebates; high volume concentration means a few large operators can demand deeper discounts. Multi-year contracts smooth demand but lock LG H&H into terms, while LG H&H’s broad portfolio strengthens its negotiating position by offering scale and promotional flexibility.

- Bundle negotiations raise buyer leverage

- Volume concentration amplifies discount pressure

- Contracts smooth demand but limit pricing flexibility

- Portfolio breadth improves LG H&H’s countervailing power

Private label and indie options

Proliferation of private label and indie brands gives buyers credible alternatives, allowing retailers to swap shelf facings quickly if velocity lags and compressing LG Household & Health Care pricing power; differentiated claims and strong brand equity are therefore essential to resist down‑trading. Incumbents must invest in innovation, storytelling and premium positioning to retain margin and shelf space.

- Private label competition: credible alternative

- Retailer agility: quick shelf replacement

- Pressure on pricing power

- Defense: differentiated claims + brand equity

Retailer consolidation squeezes margins; exclusive SKUs and faster NPD amid 96% online, ~60% try new

Retailer consolidation forces deeper trade spend and stricter terms, pressuring margins while LG H&H uses exclusive SKUs to regain leverage. 96% internet penetration in 2024 and ~60% of Korean beauty buyers trying new products monthly raise price sensitivity and churn. Private-label and indie growth increase retailer switching power, requiring stronger branding and faster NPD.

| Driver | Metric (2024) |

|---|---|

| Internet penetration | 96% (ITU) |

| Monthly product trial | ~60% (2024 survey) |

Same Document Delivered

LG Household & Health Care Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis of LG Household & Health Care you'll receive—fully written, formatted, and ready to download upon purchase. No placeholders or samples: the content shown here is the final deliverable. Buy once and get instant access to this identical file for your analysis needs.