LIC Housing Finance Business Model Canvas

Mortgage Lender Business Model Canvas: Value, Risk Management, and Revenue Streams

Unlock the full strategic blueprint behind LIC Housing Finance with our concise Business Model Canvas summary—see how it creates customer value, manages risk, and monetizes mortgage lending. Dive deeper by purchasing the complete, editable canvas (Word & Excel) for detailed insights, benchmarking, and investor-ready analysis.

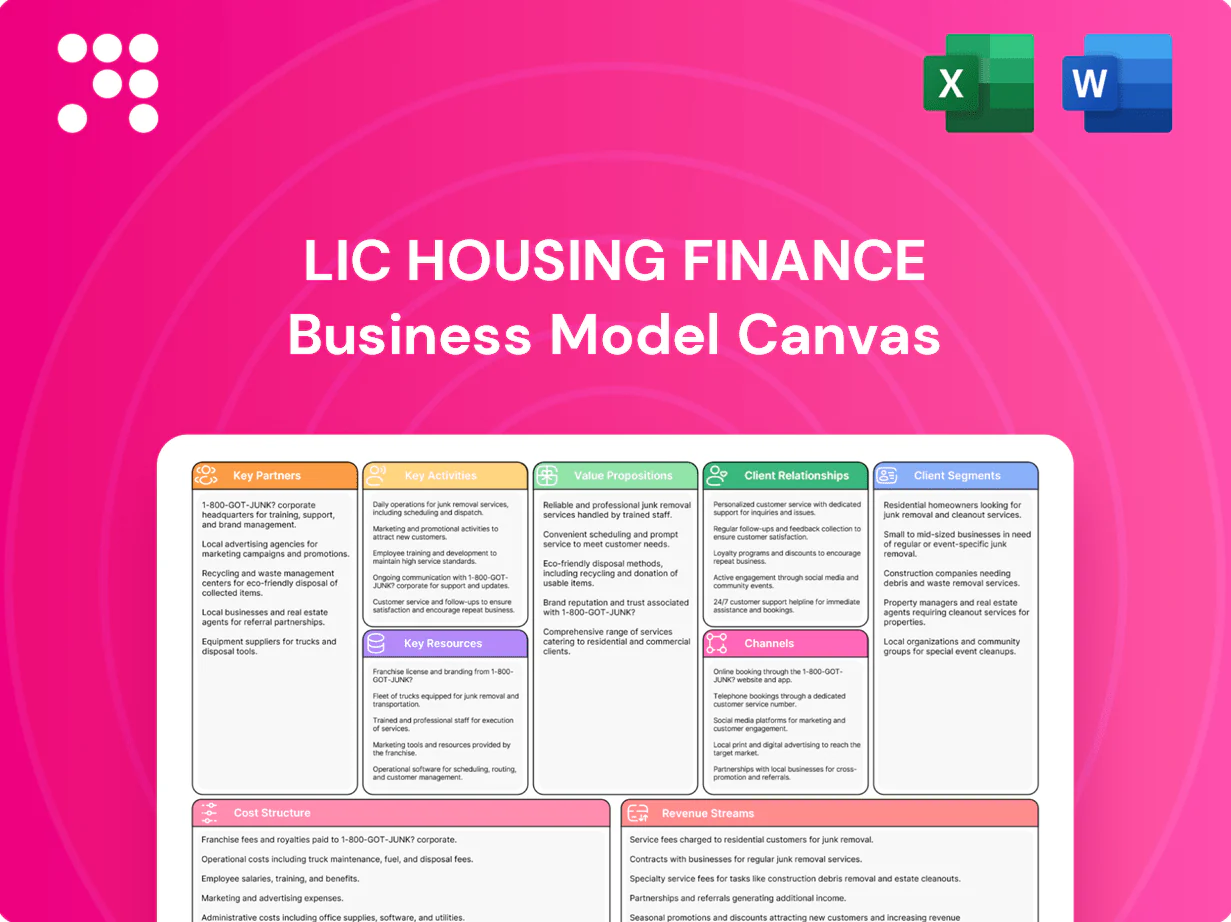

Partnerships

LIC ecosystem alliances

Leverages LIC group brand and distribution: LIC's ~60% life-market share and ~290 million policyholders in 2024 give LIC Housing Finance access to a vast, trust-based customer base for co-marketing and cross-selling. Shared insights enable pre-qualified home-loan offers and bundled home-protection products, boosting conversion and lowering acquisition costs. Co-branded efforts drive higher-ticket originations and improved retention.

Banks and capital providers

Maintain diversified funding lines from PSU and private banks and money markets, deploying term loans, refinance and working capital facilities to ensure liquidity; competitive bidding for wholesale funds helps optimize cost of funds, supporting margin preservation. This funding mix underpins growth financing while enhancing ALM stability through tenor-matched disbursements and contingency backstops.

NHB and regulators

Engage with National Housing Bank and RBI for refinance lines and compliance, leveraging NHB refinance schemes (updated 2024) to lower wholesale funding costs. Align to prudential norms and central affordable housing initiatives so loans meet RBI/NHB priority sector criteria and subsidy programmes. Access priority sector support to expand affordable housing outreach and enhance governance credibility through strengthened regulatory reporting.

Builders and channel partners

Partner with reputed developers for project approvals to secure credit-worthy inventory and align with regulatory compliance; collaborate with DSAs, connectors, and brokers to expand sourcing reach and increase lead conversion; implement stringent due diligence and maintain an active inventory pipeline to mitigate default risk; enable faster sanctioning for approved projects through pre-approved limits and streamlined credit workflows.

- Developer tie-ups for approved projects

- DSAs, connectors, brokers for sourcing

- Robust due diligence and inventory pipeline

- Faster sanctions via pre-approved frameworks

Fintechs and bureaus

Partner with major credit bureaus—CIBIL (TransUnion), Experian, Equifax and CRIF High Mark—plus UIDAI-enabled eKYC and data providers; fintechs supply eKYC, NPCI eNACH and digital underwriting engines to cut turn-around times, lower fraud and scale paper-light processes.

- credit-bureaus

- eKYC-UIDAI

- eNACH-NPCI

- digital-underwriting

Drive low-cost loans via market-leading life insurer co-marketing, ≈60% share

Leverages LIC group brand (≈60% life-market share; ≈290 million policyholders in 2024) to drive co-marketing, pre-qualified cross-sell and lower acquisition costs. Maintains diversified funding from PSU/private banks, money markets and NHB refinance lines to preserve margins and ALM. Partners with developers, DSAs, credit bureaus, UIDAI, NPCI and fintechs to scale sourcing, speed underwriting and reduce fraud.

| Metric | 2024 |

|---|---|

| LIC market share | ≈60% |

| LIC policyholders | ≈290M |

| NHB/refinance | Active 2024 schemes |

What is included in the product

A concise Business Model Canvas for LIC Housing Finance detailing customer segments, channels, value propositions, revenue streams, cost structure, key resources, activities, partnerships and customer relationships to reflect its mortgage lending operations. It highlights competitive advantages, linked SWOT insights, and is tailored for presentations, investor discussions and strategic decision-making.

High-level snapshot that relieves lending pain points by mapping LIC Housing Finance’s customer segments, underwriting controls, risk mitigation and distribution channels into editable cells for fast problem diagnosis and team collaboration.

Activities

Loan origination

LIC Housing Finance sources applications via its branch network, digital platform and distribution partners, operating through 200+ branches across India to widen reach. KYC and preliminary screening follow RBI/NHB-compliant Aadhaar and PAN verifications and automated credit checks to speed processing. Documentation is collected efficiently through digital uploads and field verification, enabling quick in-principle sanctions typically within 48–72 hours.

Credit underwriting

Assess borrower income, credit history, collateral value and property title using automated scorecards plus expert judgment; LIC Housing Finance manages a loan book ~Rs 1.1 lakh crore (FY24) with gross NPA ~1.7% (FY24). Price loans for risk, set covenants (LTV, insurance), and approve within defined TAT SLAs (typically 48–72 hours for salaried cases).

Collections and servicing

Manage repayment schedules and customer queries across a loan book of about Rs 81,000 crore (FY2024), using reminders, auto-debits and targeted cure programs to keep collection efficiency high; handle restructures strictly per policy and credit norms; aim to maintain GNPA near reported FY2024 levels of ~0.68% through proactive servicing and early NPA interventions.

ALM and treasury

ALM and treasury align retail and home loan maturities with funding tenors to reduce rollover risk, hedge interest-rate exposure through swaps and options, and keep liquidity buffers covering 3–6 months of expected contractual outflows while seeking to optimize borrowing costs via diversified short- and long-term markets and negotiable bank lines.

- Match maturities

- Prudent hedging

- 3–6 months liquidity

- Optimize borrowing

Risk, compliance, and audit

Ensure regulatory adherence across operations by aligning policies with RBI and NHB guidelines, maintaining timely statutory filings and KYC/AML compliance to protect lending licenses and reputation.

Monitor portfolio analytics and early warnings through vintage analysis, stress-testing and automated watchlists to pre-empt delinquencies and optimize provisioning.

Conduct internal audits and vendor oversight with risk-based audit plans and third-party controls, while continuously strengthening governance, policy updates, and remediation tracking.

- Regulatory alignment: RBI/NHB compliance

- Analytics: vintage, stress tests, watchlists

- Audit: risk-based internal audits, vendor controls

- Controls: continuous policy and remediation

200+ branches; Rs 1.1L cr loan book, GNPA 0.68%

Originate via 200+ branches, digital channels and partners; KYC, automated credit checks and e-docs enable 48–72h in‑principle sanctions. Underwrite using scorecards and manual review; manage loan book ~Rs 1.1 lakh crore (FY24) with GNPA ~0.68% (FY24). Collections use auto-debits and cure programs across ~Rs 81,000 crore retail book; ALM keeps 3–6 months liquidity.

| Metric | Value (FY24) |

|---|---|

| Branches | 200+ |

| Loan book | Rs 1.1 lakh crore |

| Retail book | Rs 81,000 crore |

| GNPA | 0.68% |

| TAT | 48–72 hrs |

| Liquidity buffer | 3–6 months |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual LIC Housing Finance Business Model Canvas, not a mockup. When you purchase, you will receive this same complete file with all sections included. It arrives ready to edit and present in Word and Excel formats. No placeholders, no surprises.

Mortgage Lender Business Model Canvas: Value, Risk Management, and Revenue Streams

Unlock the full strategic blueprint behind LIC Housing Finance with our concise Business Model Canvas summary—see how it creates customer value, manages risk, and monetizes mortgage lending. Dive deeper by purchasing the complete, editable canvas (Word & Excel) for detailed insights, benchmarking, and investor-ready analysis.

Partnerships

LIC ecosystem alliances

Leverages LIC group brand and distribution: LIC's ~60% life-market share and ~290 million policyholders in 2024 give LIC Housing Finance access to a vast, trust-based customer base for co-marketing and cross-selling. Shared insights enable pre-qualified home-loan offers and bundled home-protection products, boosting conversion and lowering acquisition costs. Co-branded efforts drive higher-ticket originations and improved retention.

Banks and capital providers

Maintain diversified funding lines from PSU and private banks and money markets, deploying term loans, refinance and working capital facilities to ensure liquidity; competitive bidding for wholesale funds helps optimize cost of funds, supporting margin preservation. This funding mix underpins growth financing while enhancing ALM stability through tenor-matched disbursements and contingency backstops.

NHB and regulators

Engage with National Housing Bank and RBI for refinance lines and compliance, leveraging NHB refinance schemes (updated 2024) to lower wholesale funding costs. Align to prudential norms and central affordable housing initiatives so loans meet RBI/NHB priority sector criteria and subsidy programmes. Access priority sector support to expand affordable housing outreach and enhance governance credibility through strengthened regulatory reporting.

Builders and channel partners

Partner with reputed developers for project approvals to secure credit-worthy inventory and align with regulatory compliance; collaborate with DSAs, connectors, and brokers to expand sourcing reach and increase lead conversion; implement stringent due diligence and maintain an active inventory pipeline to mitigate default risk; enable faster sanctioning for approved projects through pre-approved limits and streamlined credit workflows.

- Developer tie-ups for approved projects

- DSAs, connectors, brokers for sourcing

- Robust due diligence and inventory pipeline

- Faster sanctions via pre-approved frameworks

Fintechs and bureaus

Partner with major credit bureaus—CIBIL (TransUnion), Experian, Equifax and CRIF High Mark—plus UIDAI-enabled eKYC and data providers; fintechs supply eKYC, NPCI eNACH and digital underwriting engines to cut turn-around times, lower fraud and scale paper-light processes.

- credit-bureaus

- eKYC-UIDAI

- eNACH-NPCI

- digital-underwriting

Drive low-cost loans via market-leading life insurer co-marketing, ≈60% share

Leverages LIC group brand (≈60% life-market share; ≈290 million policyholders in 2024) to drive co-marketing, pre-qualified cross-sell and lower acquisition costs. Maintains diversified funding from PSU/private banks, money markets and NHB refinance lines to preserve margins and ALM. Partners with developers, DSAs, credit bureaus, UIDAI, NPCI and fintechs to scale sourcing, speed underwriting and reduce fraud.

| Metric | 2024 |

|---|---|

| LIC market share | ≈60% |

| LIC policyholders | ≈290M |

| NHB/refinance | Active 2024 schemes |

What is included in the product

A concise Business Model Canvas for LIC Housing Finance detailing customer segments, channels, value propositions, revenue streams, cost structure, key resources, activities, partnerships and customer relationships to reflect its mortgage lending operations. It highlights competitive advantages, linked SWOT insights, and is tailored for presentations, investor discussions and strategic decision-making.

High-level snapshot that relieves lending pain points by mapping LIC Housing Finance’s customer segments, underwriting controls, risk mitigation and distribution channels into editable cells for fast problem diagnosis and team collaboration.

Activities

Loan origination

LIC Housing Finance sources applications via its branch network, digital platform and distribution partners, operating through 200+ branches across India to widen reach. KYC and preliminary screening follow RBI/NHB-compliant Aadhaar and PAN verifications and automated credit checks to speed processing. Documentation is collected efficiently through digital uploads and field verification, enabling quick in-principle sanctions typically within 48–72 hours.

Credit underwriting

Assess borrower income, credit history, collateral value and property title using automated scorecards plus expert judgment; LIC Housing Finance manages a loan book ~Rs 1.1 lakh crore (FY24) with gross NPA ~1.7% (FY24). Price loans for risk, set covenants (LTV, insurance), and approve within defined TAT SLAs (typically 48–72 hours for salaried cases).

Collections and servicing

Manage repayment schedules and customer queries across a loan book of about Rs 81,000 crore (FY2024), using reminders, auto-debits and targeted cure programs to keep collection efficiency high; handle restructures strictly per policy and credit norms; aim to maintain GNPA near reported FY2024 levels of ~0.68% through proactive servicing and early NPA interventions.

ALM and treasury

ALM and treasury align retail and home loan maturities with funding tenors to reduce rollover risk, hedge interest-rate exposure through swaps and options, and keep liquidity buffers covering 3–6 months of expected contractual outflows while seeking to optimize borrowing costs via diversified short- and long-term markets and negotiable bank lines.

- Match maturities

- Prudent hedging

- 3–6 months liquidity

- Optimize borrowing

Risk, compliance, and audit

Ensure regulatory adherence across operations by aligning policies with RBI and NHB guidelines, maintaining timely statutory filings and KYC/AML compliance to protect lending licenses and reputation.

Monitor portfolio analytics and early warnings through vintage analysis, stress-testing and automated watchlists to pre-empt delinquencies and optimize provisioning.

Conduct internal audits and vendor oversight with risk-based audit plans and third-party controls, while continuously strengthening governance, policy updates, and remediation tracking.

- Regulatory alignment: RBI/NHB compliance

- Analytics: vintage, stress tests, watchlists

- Audit: risk-based internal audits, vendor controls

- Controls: continuous policy and remediation

200+ branches; Rs 1.1L cr loan book, GNPA 0.68%

Originate via 200+ branches, digital channels and partners; KYC, automated credit checks and e-docs enable 48–72h in‑principle sanctions. Underwrite using scorecards and manual review; manage loan book ~Rs 1.1 lakh crore (FY24) with GNPA ~0.68% (FY24). Collections use auto-debits and cure programs across ~Rs 81,000 crore retail book; ALM keeps 3–6 months liquidity.

| Metric | Value (FY24) |

|---|---|

| Branches | 200+ |

| Loan book | Rs 1.1 lakh crore |

| Retail book | Rs 81,000 crore |

| GNPA | 0.68% |

| TAT | 48–72 hrs |

| Liquidity buffer | 3–6 months |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual LIC Housing Finance Business Model Canvas, not a mockup. When you purchase, you will receive this same complete file with all sections included. It arrives ready to edit and present in Word and Excel formats. No placeholders, no surprises.

Description

Mortgage Lender Business Model Canvas: Value, Risk Management, and Revenue Streams

Unlock the full strategic blueprint behind LIC Housing Finance with our concise Business Model Canvas summary—see how it creates customer value, manages risk, and monetizes mortgage lending. Dive deeper by purchasing the complete, editable canvas (Word & Excel) for detailed insights, benchmarking, and investor-ready analysis.

Partnerships

LIC ecosystem alliances

Leverages LIC group brand and distribution: LIC's ~60% life-market share and ~290 million policyholders in 2024 give LIC Housing Finance access to a vast, trust-based customer base for co-marketing and cross-selling. Shared insights enable pre-qualified home-loan offers and bundled home-protection products, boosting conversion and lowering acquisition costs. Co-branded efforts drive higher-ticket originations and improved retention.

Banks and capital providers

Maintain diversified funding lines from PSU and private banks and money markets, deploying term loans, refinance and working capital facilities to ensure liquidity; competitive bidding for wholesale funds helps optimize cost of funds, supporting margin preservation. This funding mix underpins growth financing while enhancing ALM stability through tenor-matched disbursements and contingency backstops.

NHB and regulators

Engage with National Housing Bank and RBI for refinance lines and compliance, leveraging NHB refinance schemes (updated 2024) to lower wholesale funding costs. Align to prudential norms and central affordable housing initiatives so loans meet RBI/NHB priority sector criteria and subsidy programmes. Access priority sector support to expand affordable housing outreach and enhance governance credibility through strengthened regulatory reporting.

Builders and channel partners

Partner with reputed developers for project approvals to secure credit-worthy inventory and align with regulatory compliance; collaborate with DSAs, connectors, and brokers to expand sourcing reach and increase lead conversion; implement stringent due diligence and maintain an active inventory pipeline to mitigate default risk; enable faster sanctioning for approved projects through pre-approved limits and streamlined credit workflows.

- Developer tie-ups for approved projects

- DSAs, connectors, brokers for sourcing

- Robust due diligence and inventory pipeline

- Faster sanctions via pre-approved frameworks

Fintechs and bureaus

Partner with major credit bureaus—CIBIL (TransUnion), Experian, Equifax and CRIF High Mark—plus UIDAI-enabled eKYC and data providers; fintechs supply eKYC, NPCI eNACH and digital underwriting engines to cut turn-around times, lower fraud and scale paper-light processes.

- credit-bureaus

- eKYC-UIDAI

- eNACH-NPCI

- digital-underwriting

Drive low-cost loans via market-leading life insurer co-marketing, ≈60% share

Leverages LIC group brand (≈60% life-market share; ≈290 million policyholders in 2024) to drive co-marketing, pre-qualified cross-sell and lower acquisition costs. Maintains diversified funding from PSU/private banks, money markets and NHB refinance lines to preserve margins and ALM. Partners with developers, DSAs, credit bureaus, UIDAI, NPCI and fintechs to scale sourcing, speed underwriting and reduce fraud.

| Metric | 2024 |

|---|---|

| LIC market share | ≈60% |

| LIC policyholders | ≈290M |

| NHB/refinance | Active 2024 schemes |

What is included in the product

A concise Business Model Canvas for LIC Housing Finance detailing customer segments, channels, value propositions, revenue streams, cost structure, key resources, activities, partnerships and customer relationships to reflect its mortgage lending operations. It highlights competitive advantages, linked SWOT insights, and is tailored for presentations, investor discussions and strategic decision-making.

High-level snapshot that relieves lending pain points by mapping LIC Housing Finance’s customer segments, underwriting controls, risk mitigation and distribution channels into editable cells for fast problem diagnosis and team collaboration.

Activities

Loan origination

LIC Housing Finance sources applications via its branch network, digital platform and distribution partners, operating through 200+ branches across India to widen reach. KYC and preliminary screening follow RBI/NHB-compliant Aadhaar and PAN verifications and automated credit checks to speed processing. Documentation is collected efficiently through digital uploads and field verification, enabling quick in-principle sanctions typically within 48–72 hours.

Credit underwriting

Assess borrower income, credit history, collateral value and property title using automated scorecards plus expert judgment; LIC Housing Finance manages a loan book ~Rs 1.1 lakh crore (FY24) with gross NPA ~1.7% (FY24). Price loans for risk, set covenants (LTV, insurance), and approve within defined TAT SLAs (typically 48–72 hours for salaried cases).

Collections and servicing

Manage repayment schedules and customer queries across a loan book of about Rs 81,000 crore (FY2024), using reminders, auto-debits and targeted cure programs to keep collection efficiency high; handle restructures strictly per policy and credit norms; aim to maintain GNPA near reported FY2024 levels of ~0.68% through proactive servicing and early NPA interventions.

ALM and treasury

ALM and treasury align retail and home loan maturities with funding tenors to reduce rollover risk, hedge interest-rate exposure through swaps and options, and keep liquidity buffers covering 3–6 months of expected contractual outflows while seeking to optimize borrowing costs via diversified short- and long-term markets and negotiable bank lines.

- Match maturities

- Prudent hedging

- 3–6 months liquidity

- Optimize borrowing

Risk, compliance, and audit

Ensure regulatory adherence across operations by aligning policies with RBI and NHB guidelines, maintaining timely statutory filings and KYC/AML compliance to protect lending licenses and reputation.

Monitor portfolio analytics and early warnings through vintage analysis, stress-testing and automated watchlists to pre-empt delinquencies and optimize provisioning.

Conduct internal audits and vendor oversight with risk-based audit plans and third-party controls, while continuously strengthening governance, policy updates, and remediation tracking.

- Regulatory alignment: RBI/NHB compliance

- Analytics: vintage, stress tests, watchlists

- Audit: risk-based internal audits, vendor controls

- Controls: continuous policy and remediation

200+ branches; Rs 1.1L cr loan book, GNPA 0.68%

Originate via 200+ branches, digital channels and partners; KYC, automated credit checks and e-docs enable 48–72h in‑principle sanctions. Underwrite using scorecards and manual review; manage loan book ~Rs 1.1 lakh crore (FY24) with GNPA ~0.68% (FY24). Collections use auto-debits and cure programs across ~Rs 81,000 crore retail book; ALM keeps 3–6 months liquidity.

| Metric | Value (FY24) |

|---|---|

| Branches | 200+ |

| Loan book | Rs 1.1 lakh crore |

| Retail book | Rs 81,000 crore |

| GNPA | 0.68% |

| TAT | 48–72 hrs |

| Liquidity buffer | 3–6 months |

What You See Is What You Get

Business Model Canvas

The document previewed here is the actual LIC Housing Finance Business Model Canvas, not a mockup. When you purchase, you will receive this same complete file with all sections included. It arrives ready to edit and present in Word and Excel formats. No placeholders, no surprises.