LIC Housing Finance PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, monetary trends, and regulatory reforms are reshaping LIC Housing Finance’s competitive landscape. This concise PESTLE snapshot highlights key risks and opportunities for investors and strategists. Ready to act? Purchase the full analysis for a detailed, actionable roadmap and downloadable templates.

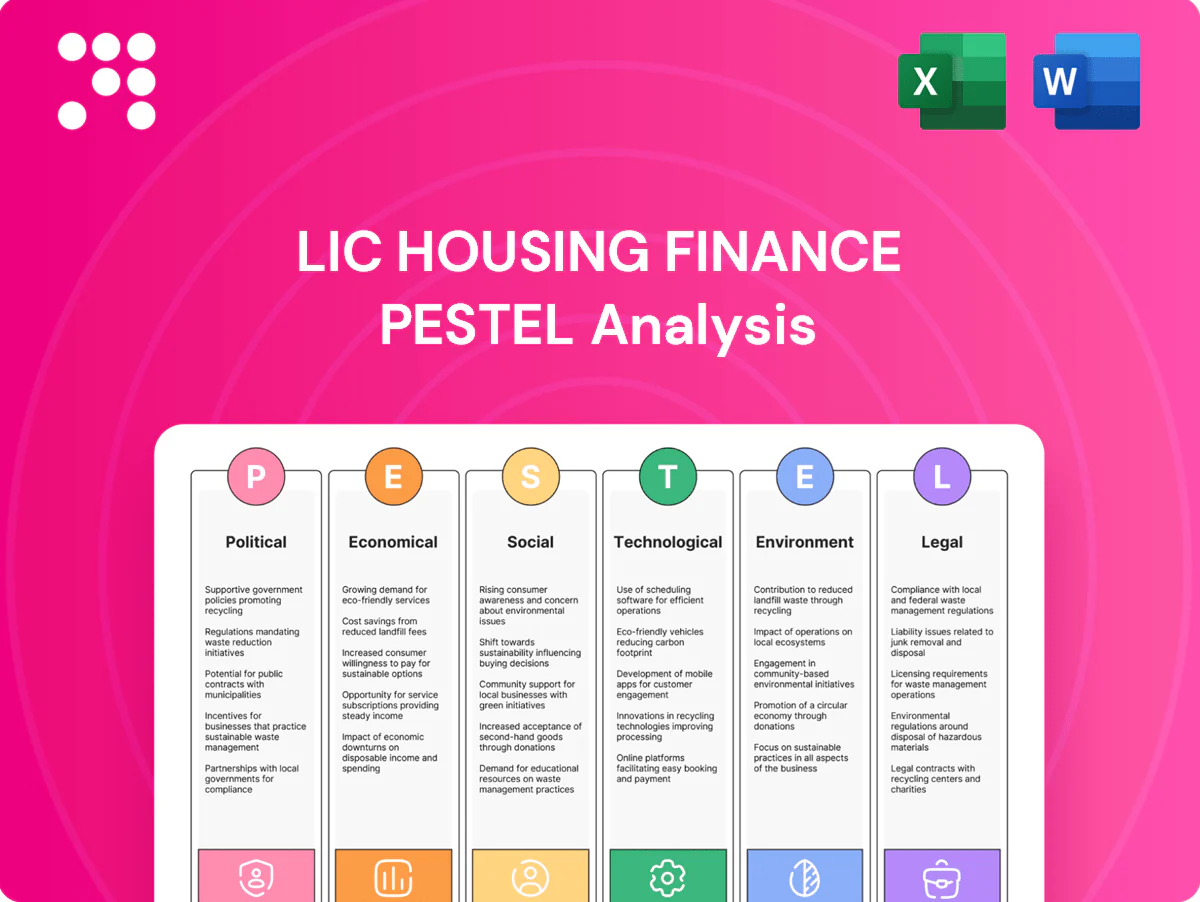

Political factors

Affordable housing push

Government affordable housing push via PMAY (target 2.95 crore houses since 2015) and CLSS interest subsidies (up to 6.5% for EWS/LIG) materially lifts mortgage demand in lower-ticket segments; policy continuity or redesign alters pipeline visibility and subsidy recognition. LIC Housing Finance can realign products and sourcing to capture priority segments, while budgetary shifts or allocation delays can slow disbursements and origination timelines.

Regulatory oversight alignment

RBI supervision of HFCs since 2019 means prudential norms, capital requirements and provisioning standards directly shape LIC Housing Finance’s growth and profitability; policy tightening tends to support asset quality while compressing spreads and raising compliance costs. Coordination with NHB for refinance lines influences liquidity access, and the government’s stance on financial stability determines supervisory intensity.

Urban development priorities

Central and state emphasis on 100 Smart Cities and over 900 km of metro corridors expands housing catchments, raising demand for LIC Housing Finance lending. Zoning and FSI revisions plus municipal approvals directly affect project viability and collateral quality, altering loan-to-value and recovery timelines. Timely public capex crowds in private housing finance, while policy delays prolong construction cycles and loan utilization.

State-level realty policies

State-level stamp duty, registration charges and property tax policies vary across India, directly affecting affordability and housing demand; differences can widen transaction costs and alter borrower eligibility. Targeted incentives for affordable-housing projects improve LTV feasibility and accelerate sales velocity, while sudden political changes can quickly withdraw or reshape local subsidies. LIC Housing Finance must calibrate state-specific pricing, sourcing and risk models to maintain margins and growth.

- Stamp duty/registration: state-dependent, impacts transaction cost

- Affordable project incentives: boost LTV and sales velocity

- Political shifts: risk of rapid policy change

- Action: state-tailored pricing, sourcing and risk calibration

Public sector ecosystem linkages

Association with the LIC brand strengthens consumer trust, amplifies distribution reach through LIC's agency network and eases policy dialogue with regulators and ministries.

Government posture toward public-sector financial entities affects market perception and access to contingent funding, while social-housing directives (eg priority lending or subsidy-linked schemes) can reorient LIC Housing Finance’s portfolio toward affordable housing.

Public scrutiny keeps governance, disclosure and compliance standards heightened, reinforcing conservative risk management and board oversight expectations.

- Brand trust: LIC affiliation boosts distribution and policy access

- Funding perception: government stance shapes market confidence

- Portfolio tilt: social-housing directives drive affordable-lending mix

- Governance: elevated public-domain oversight and compliance

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Government affordable-housing push (PMAY target 2.95 crore houses since 2015) and CLSS subsidies (up to 6.5% for EWS/LIG) enlarge lower-ticket mortgage demand; RBI supervision of HFCs since 2019 tightens prudential norms, affecting spreads and provisioning. Urban infra (100 Smart Cities, 900+ km metro) and state stamp-duty variance reshape origination economics and LTVs.

| Policy | Metric | Impact |

|---|---|---|

| PMAY | 2.95 crore houses (since 2015) | ↑ affordable demand |

| CLSS | up to 6.5% subsidy | ↑ lower-ticket uptake |

| HFC regulation | RBI oversight since 2019 | ↑ provisioning/compliance |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect LIC Housing Finance, with data‑backed insights on regulation, interest rate cycles, housing demand, digital lending, sustainability and compliance risks. Designed for executives and investors, the analysis links current market and policy dynamics to forward‑looking opportunities and threats for strategy and funding decisions.

A concise, PESTLE-segmented summary of LIC Housing Finance that relieves prep pain by highlighting regulatory, economic, social, technological and environmental risks and opportunities for quick insertion into presentations or planning sessions.

Economic factors

Interest rate cycle

RBI policy rates, with the repo at 6.50% as of July 2025, directly lift borrowing costs, EMIs and refinance activity for LIC Housing, tightening affordability and slowing disbursals when rising and boosting originations when eased. Rising rates pressure prepayment and raise churn; declines spur disbursals. Spread management depends on how quickly liabilities reprice versus asset yields; balance-sheet duration strategy is critical in volatile cycles.

Income and employment trends

Real wage growth and rising formalization underpin mortgage eligibility for LIC Housing Finance; India recorded GDP growth of 7.2% in FY2023-24, supporting real incomes and demand for housing credit. Expansion of incomes in Tier-2 and Tier-3 cities has materially widened addressable markets as urbanization and salaried hiring rise. Economic slowdowns heighten delinquency risk, especially among self-employed borrowers with volatile cashflows. Credit filters must adapt dynamically to sectoral employment shocks and shifting job stability metrics.

Real estate cycle health

Inventory overhang and new launches directly influence LTVs and sales traction; India residential launches recovered ~2024 with prices up about 4–6% YoY, helping sales velocity and permitting somewhat higher LTVs.

Healthy absorption narrows time-to-sale, improving collateral liquidity and recovery prospects for LIC Housing Finance; housing credit growth remained robust near mid‑teens in 2024.

Construction input inflation in 2023–24 extended project timelines by several quarters, widening execution risk and cost overruns; concentrated exposure to a few large developers (top developers hold roughly a third of organized supply) increases correlated default risk.

Liquidity and funding access

Access to bank lines, NCDs, CPs and NHB refinance shapes LIC Housing Finance growth capacity and pricing; India CP outstanding was about ₹6 lakh crore in 2024, determining wholesale term availability. Debt market risk appetite drives spreads and tenor; tighter markets raise spreads and shorten tenors. Strong credit ratings materially lower cost of funds, improving competitiveness; tight-liquidity phases force granular deposit substitutes and securitizations.

- Access: bank lines, NCDs, CPs, NHB

- Market size: CP ~₹6 lakh crore (2024)

- Risk appetite: affects spreads/tenor

- Ratings: lower funding cost

- Liquidity shocks: push securitization/deposit substitutes

Affordability dynamics

House price-to-income ratios in major Indian metros averaged about 7–10x in 2024, constraining conversion rates as lenders target EMI-to-income caps around 40–50% to preserve repayment capacity. Tax incentives and subsidy pass-throughs (PMAY/credit-linked subsidies) add affordability buffers and lift effective buying power. Calibrated LTV and FOIR tweaks can unlock salaried and self-employed segments without overleveraging. Ongoing product tailoring—tenor, step-up EMIs, blended rates—supports balanced growth.

- HPI 7–10x (2024); EMI/Income 40–50% caps; PMAY subsidies expand demand; LTV/FOIR fine-tuning to target new segments

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Repo at 6.50% (Jul 2025) raises borrowing costs and tightens disbursals; housing credit grew mid‑teens in 2024 supporting demand. GDP 7.2% (FY23‑24) and HPI 7–10x (2024) shape affordability; PMAY subsidies and rising Tier‑2 incomes widen addressable market. CP stock ~₹6 lakh crore (2024) and funding spreads determine growth capacity; concentrated developer exposure raises correlated execution risk.

| Metric | Value |

|---|---|

| Repo | 6.50% (Jul 2025) |

| GDP | 7.2% (FY23‑24) |

| Housing credit growth | Mid‑teens (2024) |

| CP outstanding | ≈₹6 lakh crore (2024) |

| HPI (metros) | 7–10x (2024) |

Same Document Delivered

LIC Housing Finance PESTLE Analysis

The preview shown here is the exact LIC Housing Finance PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The file you see is the final version with complete content and structure, no placeholders or teasers. After payment you’ll instantly download this exact document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, monetary trends, and regulatory reforms are reshaping LIC Housing Finance’s competitive landscape. This concise PESTLE snapshot highlights key risks and opportunities for investors and strategists. Ready to act? Purchase the full analysis for a detailed, actionable roadmap and downloadable templates.

Political factors

Affordable housing push

Government affordable housing push via PMAY (target 2.95 crore houses since 2015) and CLSS interest subsidies (up to 6.5% for EWS/LIG) materially lifts mortgage demand in lower-ticket segments; policy continuity or redesign alters pipeline visibility and subsidy recognition. LIC Housing Finance can realign products and sourcing to capture priority segments, while budgetary shifts or allocation delays can slow disbursements and origination timelines.

Regulatory oversight alignment

RBI supervision of HFCs since 2019 means prudential norms, capital requirements and provisioning standards directly shape LIC Housing Finance’s growth and profitability; policy tightening tends to support asset quality while compressing spreads and raising compliance costs. Coordination with NHB for refinance lines influences liquidity access, and the government’s stance on financial stability determines supervisory intensity.

Urban development priorities

Central and state emphasis on 100 Smart Cities and over 900 km of metro corridors expands housing catchments, raising demand for LIC Housing Finance lending. Zoning and FSI revisions plus municipal approvals directly affect project viability and collateral quality, altering loan-to-value and recovery timelines. Timely public capex crowds in private housing finance, while policy delays prolong construction cycles and loan utilization.

State-level realty policies

State-level stamp duty, registration charges and property tax policies vary across India, directly affecting affordability and housing demand; differences can widen transaction costs and alter borrower eligibility. Targeted incentives for affordable-housing projects improve LTV feasibility and accelerate sales velocity, while sudden political changes can quickly withdraw or reshape local subsidies. LIC Housing Finance must calibrate state-specific pricing, sourcing and risk models to maintain margins and growth.

- Stamp duty/registration: state-dependent, impacts transaction cost

- Affordable project incentives: boost LTV and sales velocity

- Political shifts: risk of rapid policy change

- Action: state-tailored pricing, sourcing and risk calibration

Public sector ecosystem linkages

Association with the LIC brand strengthens consumer trust, amplifies distribution reach through LIC's agency network and eases policy dialogue with regulators and ministries.

Government posture toward public-sector financial entities affects market perception and access to contingent funding, while social-housing directives (eg priority lending or subsidy-linked schemes) can reorient LIC Housing Finance’s portfolio toward affordable housing.

Public scrutiny keeps governance, disclosure and compliance standards heightened, reinforcing conservative risk management and board oversight expectations.

- Brand trust: LIC affiliation boosts distribution and policy access

- Funding perception: government stance shapes market confidence

- Portfolio tilt: social-housing directives drive affordable-lending mix

- Governance: elevated public-domain oversight and compliance

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Government affordable-housing push (PMAY target 2.95 crore houses since 2015) and CLSS subsidies (up to 6.5% for EWS/LIG) enlarge lower-ticket mortgage demand; RBI supervision of HFCs since 2019 tightens prudential norms, affecting spreads and provisioning. Urban infra (100 Smart Cities, 900+ km metro) and state stamp-duty variance reshape origination economics and LTVs.

| Policy | Metric | Impact |

|---|---|---|

| PMAY | 2.95 crore houses (since 2015) | ↑ affordable demand |

| CLSS | up to 6.5% subsidy | ↑ lower-ticket uptake |

| HFC regulation | RBI oversight since 2019 | ↑ provisioning/compliance |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect LIC Housing Finance, with data‑backed insights on regulation, interest rate cycles, housing demand, digital lending, sustainability and compliance risks. Designed for executives and investors, the analysis links current market and policy dynamics to forward‑looking opportunities and threats for strategy and funding decisions.

A concise, PESTLE-segmented summary of LIC Housing Finance that relieves prep pain by highlighting regulatory, economic, social, technological and environmental risks and opportunities for quick insertion into presentations or planning sessions.

Economic factors

Interest rate cycle

RBI policy rates, with the repo at 6.50% as of July 2025, directly lift borrowing costs, EMIs and refinance activity for LIC Housing, tightening affordability and slowing disbursals when rising and boosting originations when eased. Rising rates pressure prepayment and raise churn; declines spur disbursals. Spread management depends on how quickly liabilities reprice versus asset yields; balance-sheet duration strategy is critical in volatile cycles.

Income and employment trends

Real wage growth and rising formalization underpin mortgage eligibility for LIC Housing Finance; India recorded GDP growth of 7.2% in FY2023-24, supporting real incomes and demand for housing credit. Expansion of incomes in Tier-2 and Tier-3 cities has materially widened addressable markets as urbanization and salaried hiring rise. Economic slowdowns heighten delinquency risk, especially among self-employed borrowers with volatile cashflows. Credit filters must adapt dynamically to sectoral employment shocks and shifting job stability metrics.

Real estate cycle health

Inventory overhang and new launches directly influence LTVs and sales traction; India residential launches recovered ~2024 with prices up about 4–6% YoY, helping sales velocity and permitting somewhat higher LTVs.

Healthy absorption narrows time-to-sale, improving collateral liquidity and recovery prospects for LIC Housing Finance; housing credit growth remained robust near mid‑teens in 2024.

Construction input inflation in 2023–24 extended project timelines by several quarters, widening execution risk and cost overruns; concentrated exposure to a few large developers (top developers hold roughly a third of organized supply) increases correlated default risk.

Liquidity and funding access

Access to bank lines, NCDs, CPs and NHB refinance shapes LIC Housing Finance growth capacity and pricing; India CP outstanding was about ₹6 lakh crore in 2024, determining wholesale term availability. Debt market risk appetite drives spreads and tenor; tighter markets raise spreads and shorten tenors. Strong credit ratings materially lower cost of funds, improving competitiveness; tight-liquidity phases force granular deposit substitutes and securitizations.

- Access: bank lines, NCDs, CPs, NHB

- Market size: CP ~₹6 lakh crore (2024)

- Risk appetite: affects spreads/tenor

- Ratings: lower funding cost

- Liquidity shocks: push securitization/deposit substitutes

Affordability dynamics

House price-to-income ratios in major Indian metros averaged about 7–10x in 2024, constraining conversion rates as lenders target EMI-to-income caps around 40–50% to preserve repayment capacity. Tax incentives and subsidy pass-throughs (PMAY/credit-linked subsidies) add affordability buffers and lift effective buying power. Calibrated LTV and FOIR tweaks can unlock salaried and self-employed segments without overleveraging. Ongoing product tailoring—tenor, step-up EMIs, blended rates—supports balanced growth.

- HPI 7–10x (2024); EMI/Income 40–50% caps; PMAY subsidies expand demand; LTV/FOIR fine-tuning to target new segments

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Repo at 6.50% (Jul 2025) raises borrowing costs and tightens disbursals; housing credit grew mid‑teens in 2024 supporting demand. GDP 7.2% (FY23‑24) and HPI 7–10x (2024) shape affordability; PMAY subsidies and rising Tier‑2 incomes widen addressable market. CP stock ~₹6 lakh crore (2024) and funding spreads determine growth capacity; concentrated developer exposure raises correlated execution risk.

| Metric | Value |

|---|---|

| Repo | 6.50% (Jul 2025) |

| GDP | 7.2% (FY23‑24) |

| Housing credit growth | Mid‑teens (2024) |

| CP outstanding | ≈₹6 lakh crore (2024) |

| HPI (metros) | 7–10x (2024) |

Same Document Delivered

LIC Housing Finance PESTLE Analysis

The preview shown here is the exact LIC Housing Finance PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The file you see is the final version with complete content and structure, no placeholders or teasers. After payment you’ll instantly download this exact document.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, monetary trends, and regulatory reforms are reshaping LIC Housing Finance’s competitive landscape. This concise PESTLE snapshot highlights key risks and opportunities for investors and strategists. Ready to act? Purchase the full analysis for a detailed, actionable roadmap and downloadable templates.

Political factors

Affordable housing push

Government affordable housing push via PMAY (target 2.95 crore houses since 2015) and CLSS interest subsidies (up to 6.5% for EWS/LIG) materially lifts mortgage demand in lower-ticket segments; policy continuity or redesign alters pipeline visibility and subsidy recognition. LIC Housing Finance can realign products and sourcing to capture priority segments, while budgetary shifts or allocation delays can slow disbursements and origination timelines.

Regulatory oversight alignment

RBI supervision of HFCs since 2019 means prudential norms, capital requirements and provisioning standards directly shape LIC Housing Finance’s growth and profitability; policy tightening tends to support asset quality while compressing spreads and raising compliance costs. Coordination with NHB for refinance lines influences liquidity access, and the government’s stance on financial stability determines supervisory intensity.

Urban development priorities

Central and state emphasis on 100 Smart Cities and over 900 km of metro corridors expands housing catchments, raising demand for LIC Housing Finance lending. Zoning and FSI revisions plus municipal approvals directly affect project viability and collateral quality, altering loan-to-value and recovery timelines. Timely public capex crowds in private housing finance, while policy delays prolong construction cycles and loan utilization.

State-level realty policies

State-level stamp duty, registration charges and property tax policies vary across India, directly affecting affordability and housing demand; differences can widen transaction costs and alter borrower eligibility. Targeted incentives for affordable-housing projects improve LTV feasibility and accelerate sales velocity, while sudden political changes can quickly withdraw or reshape local subsidies. LIC Housing Finance must calibrate state-specific pricing, sourcing and risk models to maintain margins and growth.

- Stamp duty/registration: state-dependent, impacts transaction cost

- Affordable project incentives: boost LTV and sales velocity

- Political shifts: risk of rapid policy change

- Action: state-tailored pricing, sourcing and risk calibration

Public sector ecosystem linkages

Association with the LIC brand strengthens consumer trust, amplifies distribution reach through LIC's agency network and eases policy dialogue with regulators and ministries.

Government posture toward public-sector financial entities affects market perception and access to contingent funding, while social-housing directives (eg priority lending or subsidy-linked schemes) can reorient LIC Housing Finance’s portfolio toward affordable housing.

Public scrutiny keeps governance, disclosure and compliance standards heightened, reinforcing conservative risk management and board oversight expectations.

- Brand trust: LIC affiliation boosts distribution and policy access

- Funding perception: government stance shapes market confidence

- Portfolio tilt: social-housing directives drive affordable-lending mix

- Governance: elevated public-domain oversight and compliance

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Government affordable-housing push (PMAY target 2.95 crore houses since 2015) and CLSS subsidies (up to 6.5% for EWS/LIG) enlarge lower-ticket mortgage demand; RBI supervision of HFCs since 2019 tightens prudential norms, affecting spreads and provisioning. Urban infra (100 Smart Cities, 900+ km metro) and state stamp-duty variance reshape origination economics and LTVs.

| Policy | Metric | Impact |

|---|---|---|

| PMAY | 2.95 crore houses (since 2015) | ↑ affordable demand |

| CLSS | up to 6.5% subsidy | ↑ lower-ticket uptake |

| HFC regulation | RBI oversight since 2019 | ↑ provisioning/compliance |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect LIC Housing Finance, with data‑backed insights on regulation, interest rate cycles, housing demand, digital lending, sustainability and compliance risks. Designed for executives and investors, the analysis links current market and policy dynamics to forward‑looking opportunities and threats for strategy and funding decisions.

A concise, PESTLE-segmented summary of LIC Housing Finance that relieves prep pain by highlighting regulatory, economic, social, technological and environmental risks and opportunities for quick insertion into presentations or planning sessions.

Economic factors

Interest rate cycle

RBI policy rates, with the repo at 6.50% as of July 2025, directly lift borrowing costs, EMIs and refinance activity for LIC Housing, tightening affordability and slowing disbursals when rising and boosting originations when eased. Rising rates pressure prepayment and raise churn; declines spur disbursals. Spread management depends on how quickly liabilities reprice versus asset yields; balance-sheet duration strategy is critical in volatile cycles.

Income and employment trends

Real wage growth and rising formalization underpin mortgage eligibility for LIC Housing Finance; India recorded GDP growth of 7.2% in FY2023-24, supporting real incomes and demand for housing credit. Expansion of incomes in Tier-2 and Tier-3 cities has materially widened addressable markets as urbanization and salaried hiring rise. Economic slowdowns heighten delinquency risk, especially among self-employed borrowers with volatile cashflows. Credit filters must adapt dynamically to sectoral employment shocks and shifting job stability metrics.

Real estate cycle health

Inventory overhang and new launches directly influence LTVs and sales traction; India residential launches recovered ~2024 with prices up about 4–6% YoY, helping sales velocity and permitting somewhat higher LTVs.

Healthy absorption narrows time-to-sale, improving collateral liquidity and recovery prospects for LIC Housing Finance; housing credit growth remained robust near mid‑teens in 2024.

Construction input inflation in 2023–24 extended project timelines by several quarters, widening execution risk and cost overruns; concentrated exposure to a few large developers (top developers hold roughly a third of organized supply) increases correlated default risk.

Liquidity and funding access

Access to bank lines, NCDs, CPs and NHB refinance shapes LIC Housing Finance growth capacity and pricing; India CP outstanding was about ₹6 lakh crore in 2024, determining wholesale term availability. Debt market risk appetite drives spreads and tenor; tighter markets raise spreads and shorten tenors. Strong credit ratings materially lower cost of funds, improving competitiveness; tight-liquidity phases force granular deposit substitutes and securitizations.

- Access: bank lines, NCDs, CPs, NHB

- Market size: CP ~₹6 lakh crore (2024)

- Risk appetite: affects spreads/tenor

- Ratings: lower funding cost

- Liquidity shocks: push securitization/deposit substitutes

Affordability dynamics

House price-to-income ratios in major Indian metros averaged about 7–10x in 2024, constraining conversion rates as lenders target EMI-to-income caps around 40–50% to preserve repayment capacity. Tax incentives and subsidy pass-throughs (PMAY/credit-linked subsidies) add affordability buffers and lift effective buying power. Calibrated LTV and FOIR tweaks can unlock salaried and self-employed segments without overleveraging. Ongoing product tailoring—tenor, step-up EMIs, blended rates—supports balanced growth.

- HPI 7–10x (2024); EMI/Income 40–50% caps; PMAY subsidies expand demand; LTV/FOIR fine-tuning to target new segments

PMAY 2.95 cr + CLSS 6.5% swell affordable-mortgage demand

Repo at 6.50% (Jul 2025) raises borrowing costs and tightens disbursals; housing credit grew mid‑teens in 2024 supporting demand. GDP 7.2% (FY23‑24) and HPI 7–10x (2024) shape affordability; PMAY subsidies and rising Tier‑2 incomes widen addressable market. CP stock ~₹6 lakh crore (2024) and funding spreads determine growth capacity; concentrated developer exposure raises correlated execution risk.

| Metric | Value |

|---|---|

| Repo | 6.50% (Jul 2025) |

| GDP | 7.2% (FY23‑24) |

| Housing credit growth | Mid‑teens (2024) |

| CP outstanding | ≈₹6 lakh crore (2024) |

| HPI (metros) | 7–10x (2024) |

Same Document Delivered

LIC Housing Finance PESTLE Analysis

The preview shown here is the exact LIC Housing Finance PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The file you see is the final version with complete content and structure, no placeholders or teasers. After payment you’ll instantly download this exact document.