LIC Housing Finance SWOT Analysis

Your Strategic Toolkit Starts Here

LIC Housing Finance shows strong brand, extensive retail franchise and improving asset quality, yet faces margin pressure, regulatory shifts and competition from fintechs. Our concise SWOT highlights core strengths, weaknesses, opportunities and threats to inform strategy or investment decisions. Purchase the full SWOT analysis for a professionally formatted Word and Excel package with research-backed, actionable insights.

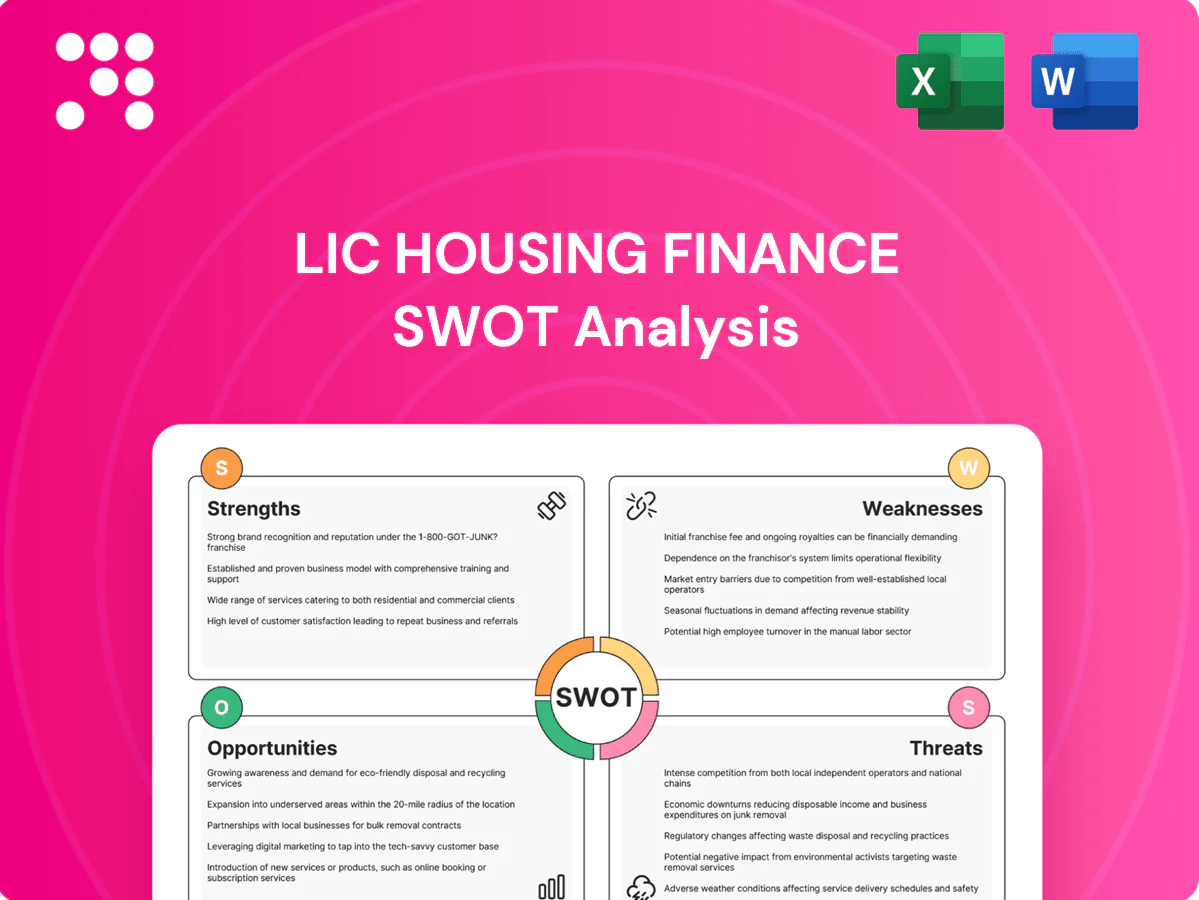

Strengths

Strong LIC brand and trust

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing Finance benefits from exceptional brand equity and customer trust; this lowers acquisition costs, boosts loan conversion and supports customer stickiness across cycles, making brand assurance a durable moat in retail home finance.

Pan-India reach and distribution

LIC Housing Finance leverages a pan‑India network of 300+ branches and an extensive DSA footprint, plus distribution synergy with LIC’s agent force of over 1.2 million, driving steady originations and strong penetration in Tier II/III towns. This broad reach diversifies geographic risk, supports scalable growth without disproportionate marketing spend and underpins repeatable low‑cost sourcing across regions.

Stable retail-dominated portfolio

LIC Housing’s portfolio is retail-heavy, with salaried/home loans accounting for roughly 88% of AUM, which historically lowers credit costs and volatility; ancillary LAP, repair/renovation and small commercial exposures augment yield without concentration risk. Retail orientation supported a GNPA near 1.6% (Mar 2024), underpinning steady asset quality and more predictable cash flows for the firm.

Access to diversified, relatively low-cost funding

Strong parentage from Life Insurance Corporation of India gives LIC Housing Finance deep market access to bonds, bank lines and NHB refinance, supporting liquidity and investor confidence.

Competitive borrowing costs versus smaller HFCs help sustain NIMs and underwriting economics amid rising rates.

Stable, diversified funding supports prudent ALM and allows more aggressive retail pricing versus peers to win market share.

- Parent backing: enhanced bond & bank access

- Low-cost borrowing: supports NIMs

- Prudent ALM: stable liquidity

- Competitive pricing vs peers

Improving digitization and risk controls

Investments in digital onboarding, underwriting and collections have cut turnaround times and improved monitoring, with data-led scorecards refining risk selection and reducing vintage delinquencies.

Process automation has lowered opex and improved cost-to-income dynamics, while enhanced analytics provide early-warning signals to detect stress sooner and tighten recoveries.

- Digital onboarding: faster TAT, better monitoring

- Data scorecards: improved risk selection

- Automation: lower opex, improved efficiency

- Analytics: early warning on borrower stress

State-backed housing lender: parent trust, pan-India reach, retail focus & low GNPA

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing benefits from strong brand trust that lowers acquisition costs.

Pan‑India 300+ branches and distribution synergy with LIC’s 1.2 million agents drive steady originations and deeper Tier II/III penetration.

Retail‑heavy AUM (~88%) and GNPA near 1.6% (Mar 2024) underpin stable asset quality; parent backing strengthens liquidity access.

| Metric | Value |

|---|---|

| AUM (FY2023/24) | ₹40+ lakh crore |

| LIC policyholders | 290m+ |

| Branches | 300+ |

| LIC agents | 1.2m |

| Retail share | ~88% |

| GNPA (Mar 2024) | ~1.6% |

What is included in the product

Delivers a concise SWOT overview of LIC Housing Finance, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise LIC Housing Finance SWOT matrix that highlights critical risks and opportunities for rapid pain-point resolution and strategic prioritization.

Weaknesses

Sensitivity to interest-rate cycles

Sharp rate moves—RBI repo up ~250 bps through 2022–23, repo ~6.5% by mid‑2024—can compress spreads and pressure LIC Housing Finance’s NIMs.

Repricing lags on assets versus faster funding resets hurt profitability and, with intense competition, limit pass‑through to borrowers.

Resultant margin volatility reduces earnings visibility and raises sensitivity to further rate swings.

ALM and liquidity management constraints

As a housing financier LIC Housing Finance faces structural ALM strain from long-tenor mortgages vs shorter-term wholesale liabilities, contributing to reported cumulative positive mismatches in 1–3 year buckets in recent disclosures; refinancing dependence makes the firm sensitive to market-wide spread widening and higher CP/G-Sec-linked costs. Maintaining liquidity buffers raises funding costs and compresses margins, while NBFC stress episodes (eg. episodic CP market freezes) can sharply tighten access to wholesale funding.

Limited fee-income diversification

Earnings remain predominantly interest-driven, with non-interest income accounting for under 5% of total income in FY2024, making profitability highly sensitive to NIM compression and credit costs. Limited fee-income and underexploited cross-sell opportunities reduce recurring revenue potential and constrain margin diversification. The fee-light model weakens counter-cyclical buffers during downturns, exposing earnings to rate and asset-quality shocks.

Slower agility versus fintech and agile NBFCs

Legacy systems and manual processes extend turnaround times, leaving LIC Housing Finance slower to approve and disburse loans compared with nimble fintechs and agile NBFCs; customer expectations set by faster competitors increase churn in urban markets. Product personalization and UX improvements lag, reducing appeal to high-net-worth and premium urban borrowers, impacting acquisition and cross-sell potential.

- Slower turnaround versus fintechs

- Lower product personalization and UX

- Hinders premium urban customer acquisition

Pricing power constrained by intense competition

LIC Housing's pricing power is constrained by intense competition from public sector and large private banks, notably SBI, the largest home lender in India. Rate wars in 2024—against a backdrop of RBI repo rate at 6.5%—have compressed yields in prime segments and raised churn risk at reset points. Retentions frequently require concessional pricing, squeezing NIMs.

- Public and large private banks (e.g., SBI) drive aggressive pricing

- RBI repo rate 6.5% (2024) — rate wars compress prime yields

- Higher churn at resets; retention often needs concessional pricing

Repo at 6.5%, 1–3yr ALM gaps squeeze NIMs; fee-light income <5%

High interest-rate sensitivity compresses spreads and NIMs after RBI repo rose to 6.5% (mid-2024). Funding/refinancing reliance and 1–3yr ALM positive mismatches heighten liquidity and wholesale-funding risk. Fee-light model (non-interest income <5% of FY2024 income) limits diversification and worsens earnings cyclicality.

| Metric | Value |

|---|---|

| RBI repo (mid-2024) | 6.5% |

| Non-interest income (FY2024) | <5% |

| ALM 1–3yr | Cumulative positive mismatch (reported) |

Preview the Actual Deliverable

LIC Housing Finance SWOT Analysis

This is the actual LIC Housing Finance SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same editable, structured content. Buy to unlock the complete, downloadable file.

Your Strategic Toolkit Starts Here

LIC Housing Finance shows strong brand, extensive retail franchise and improving asset quality, yet faces margin pressure, regulatory shifts and competition from fintechs. Our concise SWOT highlights core strengths, weaknesses, opportunities and threats to inform strategy or investment decisions. Purchase the full SWOT analysis for a professionally formatted Word and Excel package with research-backed, actionable insights.

Strengths

Strong LIC brand and trust

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing Finance benefits from exceptional brand equity and customer trust; this lowers acquisition costs, boosts loan conversion and supports customer stickiness across cycles, making brand assurance a durable moat in retail home finance.

Pan-India reach and distribution

LIC Housing Finance leverages a pan‑India network of 300+ branches and an extensive DSA footprint, plus distribution synergy with LIC’s agent force of over 1.2 million, driving steady originations and strong penetration in Tier II/III towns. This broad reach diversifies geographic risk, supports scalable growth without disproportionate marketing spend and underpins repeatable low‑cost sourcing across regions.

Stable retail-dominated portfolio

LIC Housing’s portfolio is retail-heavy, with salaried/home loans accounting for roughly 88% of AUM, which historically lowers credit costs and volatility; ancillary LAP, repair/renovation and small commercial exposures augment yield without concentration risk. Retail orientation supported a GNPA near 1.6% (Mar 2024), underpinning steady asset quality and more predictable cash flows for the firm.

Access to diversified, relatively low-cost funding

Strong parentage from Life Insurance Corporation of India gives LIC Housing Finance deep market access to bonds, bank lines and NHB refinance, supporting liquidity and investor confidence.

Competitive borrowing costs versus smaller HFCs help sustain NIMs and underwriting economics amid rising rates.

Stable, diversified funding supports prudent ALM and allows more aggressive retail pricing versus peers to win market share.

- Parent backing: enhanced bond & bank access

- Low-cost borrowing: supports NIMs

- Prudent ALM: stable liquidity

- Competitive pricing vs peers

Improving digitization and risk controls

Investments in digital onboarding, underwriting and collections have cut turnaround times and improved monitoring, with data-led scorecards refining risk selection and reducing vintage delinquencies.

Process automation has lowered opex and improved cost-to-income dynamics, while enhanced analytics provide early-warning signals to detect stress sooner and tighten recoveries.

- Digital onboarding: faster TAT, better monitoring

- Data scorecards: improved risk selection

- Automation: lower opex, improved efficiency

- Analytics: early warning on borrower stress

State-backed housing lender: parent trust, pan-India reach, retail focus & low GNPA

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing benefits from strong brand trust that lowers acquisition costs.

Pan‑India 300+ branches and distribution synergy with LIC’s 1.2 million agents drive steady originations and deeper Tier II/III penetration.

Retail‑heavy AUM (~88%) and GNPA near 1.6% (Mar 2024) underpin stable asset quality; parent backing strengthens liquidity access.

| Metric | Value |

|---|---|

| AUM (FY2023/24) | ₹40+ lakh crore |

| LIC policyholders | 290m+ |

| Branches | 300+ |

| LIC agents | 1.2m |

| Retail share | ~88% |

| GNPA (Mar 2024) | ~1.6% |

What is included in the product

Delivers a concise SWOT overview of LIC Housing Finance, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise LIC Housing Finance SWOT matrix that highlights critical risks and opportunities for rapid pain-point resolution and strategic prioritization.

Weaknesses

Sensitivity to interest-rate cycles

Sharp rate moves—RBI repo up ~250 bps through 2022–23, repo ~6.5% by mid‑2024—can compress spreads and pressure LIC Housing Finance’s NIMs.

Repricing lags on assets versus faster funding resets hurt profitability and, with intense competition, limit pass‑through to borrowers.

Resultant margin volatility reduces earnings visibility and raises sensitivity to further rate swings.

ALM and liquidity management constraints

As a housing financier LIC Housing Finance faces structural ALM strain from long-tenor mortgages vs shorter-term wholesale liabilities, contributing to reported cumulative positive mismatches in 1–3 year buckets in recent disclosures; refinancing dependence makes the firm sensitive to market-wide spread widening and higher CP/G-Sec-linked costs. Maintaining liquidity buffers raises funding costs and compresses margins, while NBFC stress episodes (eg. episodic CP market freezes) can sharply tighten access to wholesale funding.

Limited fee-income diversification

Earnings remain predominantly interest-driven, with non-interest income accounting for under 5% of total income in FY2024, making profitability highly sensitive to NIM compression and credit costs. Limited fee-income and underexploited cross-sell opportunities reduce recurring revenue potential and constrain margin diversification. The fee-light model weakens counter-cyclical buffers during downturns, exposing earnings to rate and asset-quality shocks.

Slower agility versus fintech and agile NBFCs

Legacy systems and manual processes extend turnaround times, leaving LIC Housing Finance slower to approve and disburse loans compared with nimble fintechs and agile NBFCs; customer expectations set by faster competitors increase churn in urban markets. Product personalization and UX improvements lag, reducing appeal to high-net-worth and premium urban borrowers, impacting acquisition and cross-sell potential.

- Slower turnaround versus fintechs

- Lower product personalization and UX

- Hinders premium urban customer acquisition

Pricing power constrained by intense competition

LIC Housing's pricing power is constrained by intense competition from public sector and large private banks, notably SBI, the largest home lender in India. Rate wars in 2024—against a backdrop of RBI repo rate at 6.5%—have compressed yields in prime segments and raised churn risk at reset points. Retentions frequently require concessional pricing, squeezing NIMs.

- Public and large private banks (e.g., SBI) drive aggressive pricing

- RBI repo rate 6.5% (2024) — rate wars compress prime yields

- Higher churn at resets; retention often needs concessional pricing

Repo at 6.5%, 1–3yr ALM gaps squeeze NIMs; fee-light income <5%

High interest-rate sensitivity compresses spreads and NIMs after RBI repo rose to 6.5% (mid-2024). Funding/refinancing reliance and 1–3yr ALM positive mismatches heighten liquidity and wholesale-funding risk. Fee-light model (non-interest income <5% of FY2024 income) limits diversification and worsens earnings cyclicality.

| Metric | Value |

|---|---|

| RBI repo (mid-2024) | 6.5% |

| Non-interest income (FY2024) | <5% |

| ALM 1–3yr | Cumulative positive mismatch (reported) |

Preview the Actual Deliverable

LIC Housing Finance SWOT Analysis

This is the actual LIC Housing Finance SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same editable, structured content. Buy to unlock the complete, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

LIC Housing Finance shows strong brand, extensive retail franchise and improving asset quality, yet faces margin pressure, regulatory shifts and competition from fintechs. Our concise SWOT highlights core strengths, weaknesses, opportunities and threats to inform strategy or investment decisions. Purchase the full SWOT analysis for a professionally formatted Word and Excel package with research-backed, actionable insights.

Strengths

Strong LIC brand and trust

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing Finance benefits from exceptional brand equity and customer trust; this lowers acquisition costs, boosts loan conversion and supports customer stickiness across cycles, making brand assurance a durable moat in retail home finance.

Pan-India reach and distribution

LIC Housing Finance leverages a pan‑India network of 300+ branches and an extensive DSA footprint, plus distribution synergy with LIC’s agent force of over 1.2 million, driving steady originations and strong penetration in Tier II/III towns. This broad reach diversifies geographic risk, supports scalable growth without disproportionate marketing spend and underpins repeatable low‑cost sourcing across regions.

Stable retail-dominated portfolio

LIC Housing’s portfolio is retail-heavy, with salaried/home loans accounting for roughly 88% of AUM, which historically lowers credit costs and volatility; ancillary LAP, repair/renovation and small commercial exposures augment yield without concentration risk. Retail orientation supported a GNPA near 1.6% (Mar 2024), underpinning steady asset quality and more predictable cash flows for the firm.

Access to diversified, relatively low-cost funding

Strong parentage from Life Insurance Corporation of India gives LIC Housing Finance deep market access to bonds, bank lines and NHB refinance, supporting liquidity and investor confidence.

Competitive borrowing costs versus smaller HFCs help sustain NIMs and underwriting economics amid rising rates.

Stable, diversified funding supports prudent ALM and allows more aggressive retail pricing versus peers to win market share.

- Parent backing: enhanced bond & bank access

- Low-cost borrowing: supports NIMs

- Prudent ALM: stable liquidity

- Competitive pricing vs peers

Improving digitization and risk controls

Investments in digital onboarding, underwriting and collections have cut turnaround times and improved monitoring, with data-led scorecards refining risk selection and reducing vintage delinquencies.

Process automation has lowered opex and improved cost-to-income dynamics, while enhanced analytics provide early-warning signals to detect stress sooner and tighten recoveries.

- Digital onboarding: faster TAT, better monitoring

- Data scorecards: improved risk selection

- Automation: lower opex, improved efficiency

- Analytics: early warning on borrower stress

State-backed housing lender: parent trust, pan-India reach, retail focus & low GNPA

Backed by Life Insurance Corporation of India (established 1956) with over 290 million policyholders and AUM exceeding ₹40 lakh crore (FY2023/24), LIC Housing benefits from strong brand trust that lowers acquisition costs.

Pan‑India 300+ branches and distribution synergy with LIC’s 1.2 million agents drive steady originations and deeper Tier II/III penetration.

Retail‑heavy AUM (~88%) and GNPA near 1.6% (Mar 2024) underpin stable asset quality; parent backing strengthens liquidity access.

| Metric | Value |

|---|---|

| AUM (FY2023/24) | ₹40+ lakh crore |

| LIC policyholders | 290m+ |

| Branches | 300+ |

| LIC agents | 1.2m |

| Retail share | ~88% |

| GNPA (Mar 2024) | ~1.6% |

What is included in the product

Delivers a concise SWOT overview of LIC Housing Finance, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise LIC Housing Finance SWOT matrix that highlights critical risks and opportunities for rapid pain-point resolution and strategic prioritization.

Weaknesses

Sensitivity to interest-rate cycles

Sharp rate moves—RBI repo up ~250 bps through 2022–23, repo ~6.5% by mid‑2024—can compress spreads and pressure LIC Housing Finance’s NIMs.

Repricing lags on assets versus faster funding resets hurt profitability and, with intense competition, limit pass‑through to borrowers.

Resultant margin volatility reduces earnings visibility and raises sensitivity to further rate swings.

ALM and liquidity management constraints

As a housing financier LIC Housing Finance faces structural ALM strain from long-tenor mortgages vs shorter-term wholesale liabilities, contributing to reported cumulative positive mismatches in 1–3 year buckets in recent disclosures; refinancing dependence makes the firm sensitive to market-wide spread widening and higher CP/G-Sec-linked costs. Maintaining liquidity buffers raises funding costs and compresses margins, while NBFC stress episodes (eg. episodic CP market freezes) can sharply tighten access to wholesale funding.

Limited fee-income diversification

Earnings remain predominantly interest-driven, with non-interest income accounting for under 5% of total income in FY2024, making profitability highly sensitive to NIM compression and credit costs. Limited fee-income and underexploited cross-sell opportunities reduce recurring revenue potential and constrain margin diversification. The fee-light model weakens counter-cyclical buffers during downturns, exposing earnings to rate and asset-quality shocks.

Slower agility versus fintech and agile NBFCs

Legacy systems and manual processes extend turnaround times, leaving LIC Housing Finance slower to approve and disburse loans compared with nimble fintechs and agile NBFCs; customer expectations set by faster competitors increase churn in urban markets. Product personalization and UX improvements lag, reducing appeal to high-net-worth and premium urban borrowers, impacting acquisition and cross-sell potential.

- Slower turnaround versus fintechs

- Lower product personalization and UX

- Hinders premium urban customer acquisition

Pricing power constrained by intense competition

LIC Housing's pricing power is constrained by intense competition from public sector and large private banks, notably SBI, the largest home lender in India. Rate wars in 2024—against a backdrop of RBI repo rate at 6.5%—have compressed yields in prime segments and raised churn risk at reset points. Retentions frequently require concessional pricing, squeezing NIMs.

- Public and large private banks (e.g., SBI) drive aggressive pricing

- RBI repo rate 6.5% (2024) — rate wars compress prime yields

- Higher churn at resets; retention often needs concessional pricing

Repo at 6.5%, 1–3yr ALM gaps squeeze NIMs; fee-light income <5%

High interest-rate sensitivity compresses spreads and NIMs after RBI repo rose to 6.5% (mid-2024). Funding/refinancing reliance and 1–3yr ALM positive mismatches heighten liquidity and wholesale-funding risk. Fee-light model (non-interest income <5% of FY2024 income) limits diversification and worsens earnings cyclicality.

| Metric | Value |

|---|---|

| RBI repo (mid-2024) | 6.5% |

| Non-interest income (FY2024) | <5% |

| ALM 1–3yr | Cumulative positive mismatch (reported) |

Preview the Actual Deliverable

LIC Housing Finance SWOT Analysis

This is the actual LIC Housing Finance SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same editable, structured content. Buy to unlock the complete, downloadable file.