Lifestyle International Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

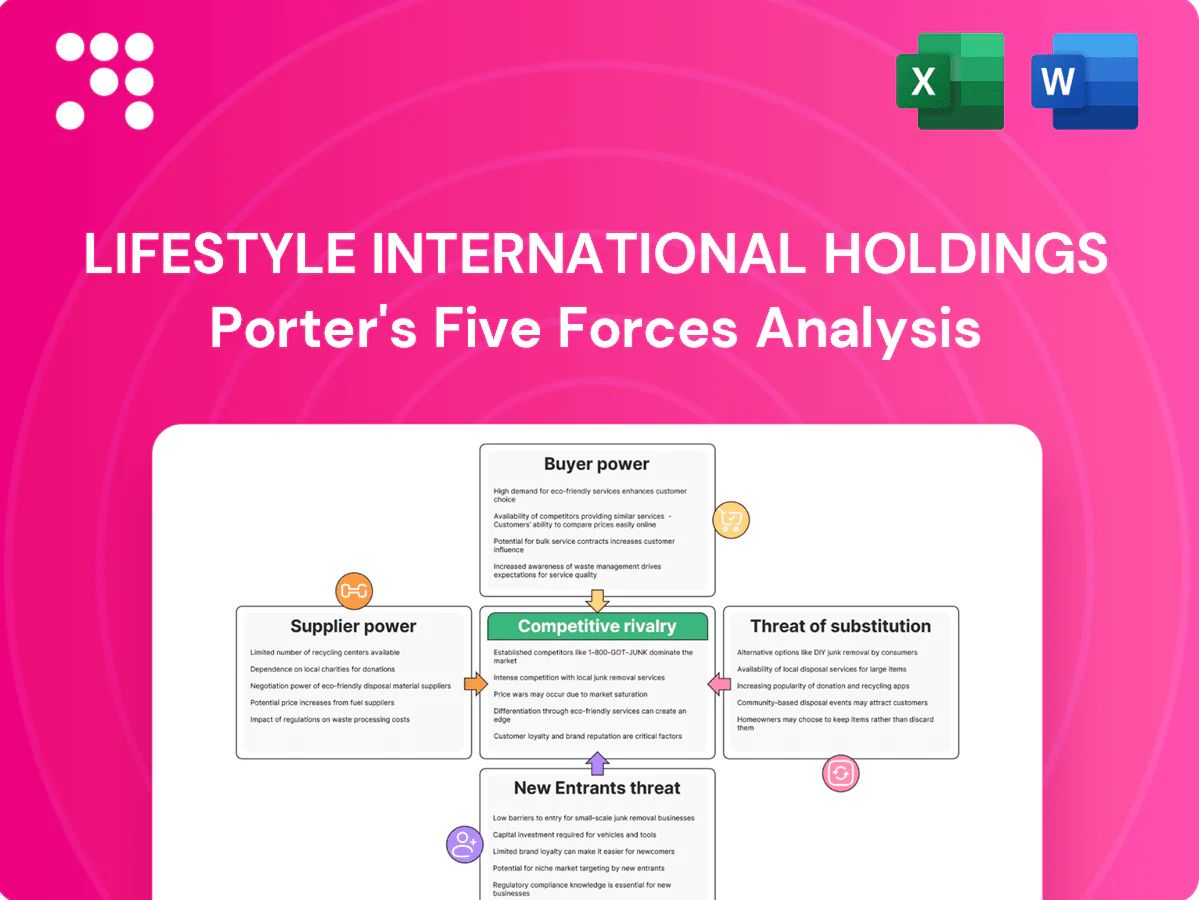

Lifestyle International Holdings faces intense retail competition, evolving buyer preferences, and supplier concentration that shape its margins and growth prospects. Differentiation and omnichannel execution are key strategic levers amid moderate threat of new entrants and substitutes. This snapshot highlights core pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore detailed competitive dynamics and actionable recommendations.

Suppliers Bargaining Power

Global brand leverage

International fashion and cosmetics brands carry strong equity and often dictate terms, visual merchandising and pricing corridors; must‑have labels on Hong Kong premium floors can secure higher margins or marketing commitments. SOGO Causeway Bay, operated by Lifestyle International, drives unparalleled exposure with c.10 million annual visitors, which reduces supplier leverage but exclusive capsule drops or limited launch windows still tilt power toward marquee suppliers.

Concession model dynamics

The concession/consignment model shifts inventory risk to brands while embedding revenue‑sharing and staffing control with suppliers; high‑performing counters win leverage over space, staffing and promo calendars. Lifestyle offsets this by enforcing performance clauses and reallocating space based on sales density. Overall bargaining power is balanced but tilts to suppliers in star categories such as beauty, where counters drive footfall and margin.

Supplier fragmentation vs concentration

Household, FMCG and homeware suppliers to Lifestyle are highly fragmented, diluting bargaining power, while concentrated luxury/masstige cosmetics and major fashion houses exert stronger leverage; the global personal luxury goods market rose to about €366bn in 2023 and was projected near €398bn in 2024, amplifying supplier clout. Category mix creates a barbell of weak and strong supplier power, but active portfolio curation—adding emerging and regional brands—reduces reliance on dominant houses and mitigates concentration risk.

Private label and exclusives

Private label and exclusives cut supplier leverage by shifting spend from global brands to in-house ranges, improving gross margins; industry surveys in 2024 show department stores' private-label penetration ~8% versus specialty retailers ~25%, leaving room for Lifestyle to reweight assortments. Building proprietary home, accessories and gourmet ranges can lift margin and bargaining leverage, but success hinges on design capability and quality-control execution risk.

Logistics, currency, and lead times

Imported assortments expose Lifestyle International Holdings (1212.HK) to FX pass‑through despite the Hong Kong dollar peg to the USD, and long apparel lead times constrain in‑season flexibility, raising markdown risk if demand misses. Large, predictable orders secure better supplier terms while volatile demand weakens clout; SOGO’s scheduled sales events aggregate volume to negotiate rebates.

- 1212.HK: SOGO operator

- HKD pegged to USD

- Long lead times → higher markdown risk

- Aggregated sales cadence → better rebates

10M visitors dilute supplier clout; luxury fashion and beauty keep pricing power

SOGO Causeway Bay c.10m annual visitors reduces supplier clout but marquee fashion/beauty brands (global luxury market ~€398bn in 2024) retain pricing and launch leverage. Concession/consignment shifts inventory risk to suppliers; beauty counters tilt power. Private‑label penetration dept stores ~8% (2024) limits supplier power; long lead times raise markdown risk.

| Metric | Value (2024) |

|---|---|

| Annual visitors | ~10,000,000 |

| Global luxury market | ~€398bn |

| Private‑label dept stores | ~8% |

| Private‑label margin uplift | +20–30pp |

What is included in the product

Concise Porter's Five Forces assessment of Lifestyle International Holdings, highlighting competitive intensity in Hong Kong retail, buyer price sensitivity, supplier leverage, threat of substitutes and online disruption, and structural barriers that protect incumbency and affect profitability.

A concise one-sheet Porter’s Five Forces for Lifestyle International Holdings that highlights competitive pressures, supplier/buyer leverage and substitute threats—ready to drop into decks; tweak force intensities to model scenarios and simplify strategic decision-making.

Customers Bargaining Power

High price transparency

High price transparency lets shoppers compare instantly across brand boutiques, HKTVmall and cross‑border platforms, raising bargaining power; low switching costs drive frequent promotions and margin pressure. International travel and outlet shopping widen reference pricing, forcing department stores to justify premiums through superior service, loyalty benefits and exclusive merchandise to retain spend.

Loyalty programs and events

SOGO Rewards and annual Thankful Week create perceived value and switching frictions, often delivering double-digit sales uplift during campaign periods. Points, vouchers and member previews reduce immediate price sensitivity and raise repeat purchase rates. However recurring promotions train customers to postpone purchases, sustaining high buyer power. Targeted use of transaction and CRM data enables personalized offers to recover margin and improve basket size.

Tourist vs local mix

Mainland tourist flows rebounded in 2024, swinging category demand and raising discount expectations; when visitation softens, locals’ steady but value‑oriented spend gains share and increases buyer power. Currency and macro cycles can shift this mix quickly, altering average basket and markdown needs. Deeper merchandise assortments and diverse payment options help Lifestyle International flex across tourist and local segments.

Abundant alternatives

Abundant alternatives from specialty chains, brand stores, e‑commerce and outlets create overlapping assortments, enabling buyers to switch quickly; buyers now demand breadth and instant availability and penalize stock‑outs with rapid defection. Easy access via MTR hubs (weekday ridership recovered to about 85% of 2019 levels in 2023) compresses convenience differentiation for Lifestyle’s flagship formats.

- Overlapping assortments across channels

- High buyer leverage for breadth and immediacy

- Stock‑outs trigger rapid defections

- MTR access reduces convenience moat (~85% pre‑COVID ridership, 2023)

Service and experience sensitivity

Customers now demand concierge service, in‑store beauty consultations and seamless returns; 2024 surveys show 72% consider omnichannel (click‑and‑collect, easy exchanges) baseline and brands lose customers fast—returns or poor service drive ~43% immediate churn and 1‑star reviews can cut conversion by ~25%. Superior in‑store experience can partially reduce this bargaining power.

- Service expectation: concierge & consultations

- Omnichannel baseline: 72% (2024)

- Churn risk: ~43% from service/returns

- Reputation impact: ~25% conversion hit

High transparency and low switching boost buyer power; failures risk 43%

High price transparency and low switching costs (omnichannel baseline 72% in 2024) keep customer bargaining power high; loyalty campaigns drive double‑digit uplifts but train postponement. Tourist mix swings demand (MTR ridership ~85% of 2019 in 2023) and abundant alternatives punish stock‑outs and poor service (43% churn risk, ~25% conversion hit).

| Metric | Value |

|---|---|

| Omnichannel baseline (2024) | 72% |

| MTR ridership vs 2019 (2023) | ~85% |

| Churn from poor service/returns | ~43% |

| Conversion hit from 1‑star reviews | ~25% |

Preview Before You Purchase

Lifestyle International Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lifestyle International Holdings you'll receive upon purchase—no placeholders or mockups. The file is fully formatted, ready to download and use instantly. It provides the same comprehensive strategic assessment contained in the final deliverable.

Don't Miss the Bigger Picture

Lifestyle International Holdings faces intense retail competition, evolving buyer preferences, and supplier concentration that shape its margins and growth prospects. Differentiation and omnichannel execution are key strategic levers amid moderate threat of new entrants and substitutes. This snapshot highlights core pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore detailed competitive dynamics and actionable recommendations.

Suppliers Bargaining Power

Global brand leverage

International fashion and cosmetics brands carry strong equity and often dictate terms, visual merchandising and pricing corridors; must‑have labels on Hong Kong premium floors can secure higher margins or marketing commitments. SOGO Causeway Bay, operated by Lifestyle International, drives unparalleled exposure with c.10 million annual visitors, which reduces supplier leverage but exclusive capsule drops or limited launch windows still tilt power toward marquee suppliers.

Concession model dynamics

The concession/consignment model shifts inventory risk to brands while embedding revenue‑sharing and staffing control with suppliers; high‑performing counters win leverage over space, staffing and promo calendars. Lifestyle offsets this by enforcing performance clauses and reallocating space based on sales density. Overall bargaining power is balanced but tilts to suppliers in star categories such as beauty, where counters drive footfall and margin.

Supplier fragmentation vs concentration

Household, FMCG and homeware suppliers to Lifestyle are highly fragmented, diluting bargaining power, while concentrated luxury/masstige cosmetics and major fashion houses exert stronger leverage; the global personal luxury goods market rose to about €366bn in 2023 and was projected near €398bn in 2024, amplifying supplier clout. Category mix creates a barbell of weak and strong supplier power, but active portfolio curation—adding emerging and regional brands—reduces reliance on dominant houses and mitigates concentration risk.

Private label and exclusives

Private label and exclusives cut supplier leverage by shifting spend from global brands to in-house ranges, improving gross margins; industry surveys in 2024 show department stores' private-label penetration ~8% versus specialty retailers ~25%, leaving room for Lifestyle to reweight assortments. Building proprietary home, accessories and gourmet ranges can lift margin and bargaining leverage, but success hinges on design capability and quality-control execution risk.

Logistics, currency, and lead times

Imported assortments expose Lifestyle International Holdings (1212.HK) to FX pass‑through despite the Hong Kong dollar peg to the USD, and long apparel lead times constrain in‑season flexibility, raising markdown risk if demand misses. Large, predictable orders secure better supplier terms while volatile demand weakens clout; SOGO’s scheduled sales events aggregate volume to negotiate rebates.

- 1212.HK: SOGO operator

- HKD pegged to USD

- Long lead times → higher markdown risk

- Aggregated sales cadence → better rebates

10M visitors dilute supplier clout; luxury fashion and beauty keep pricing power

SOGO Causeway Bay c.10m annual visitors reduces supplier clout but marquee fashion/beauty brands (global luxury market ~€398bn in 2024) retain pricing and launch leverage. Concession/consignment shifts inventory risk to suppliers; beauty counters tilt power. Private‑label penetration dept stores ~8% (2024) limits supplier power; long lead times raise markdown risk.

| Metric | Value (2024) |

|---|---|

| Annual visitors | ~10,000,000 |

| Global luxury market | ~€398bn |

| Private‑label dept stores | ~8% |

| Private‑label margin uplift | +20–30pp |

What is included in the product

Concise Porter's Five Forces assessment of Lifestyle International Holdings, highlighting competitive intensity in Hong Kong retail, buyer price sensitivity, supplier leverage, threat of substitutes and online disruption, and structural barriers that protect incumbency and affect profitability.

A concise one-sheet Porter’s Five Forces for Lifestyle International Holdings that highlights competitive pressures, supplier/buyer leverage and substitute threats—ready to drop into decks; tweak force intensities to model scenarios and simplify strategic decision-making.

Customers Bargaining Power

High price transparency

High price transparency lets shoppers compare instantly across brand boutiques, HKTVmall and cross‑border platforms, raising bargaining power; low switching costs drive frequent promotions and margin pressure. International travel and outlet shopping widen reference pricing, forcing department stores to justify premiums through superior service, loyalty benefits and exclusive merchandise to retain spend.

Loyalty programs and events

SOGO Rewards and annual Thankful Week create perceived value and switching frictions, often delivering double-digit sales uplift during campaign periods. Points, vouchers and member previews reduce immediate price sensitivity and raise repeat purchase rates. However recurring promotions train customers to postpone purchases, sustaining high buyer power. Targeted use of transaction and CRM data enables personalized offers to recover margin and improve basket size.

Tourist vs local mix

Mainland tourist flows rebounded in 2024, swinging category demand and raising discount expectations; when visitation softens, locals’ steady but value‑oriented spend gains share and increases buyer power. Currency and macro cycles can shift this mix quickly, altering average basket and markdown needs. Deeper merchandise assortments and diverse payment options help Lifestyle International flex across tourist and local segments.

Abundant alternatives

Abundant alternatives from specialty chains, brand stores, e‑commerce and outlets create overlapping assortments, enabling buyers to switch quickly; buyers now demand breadth and instant availability and penalize stock‑outs with rapid defection. Easy access via MTR hubs (weekday ridership recovered to about 85% of 2019 levels in 2023) compresses convenience differentiation for Lifestyle’s flagship formats.

- Overlapping assortments across channels

- High buyer leverage for breadth and immediacy

- Stock‑outs trigger rapid defections

- MTR access reduces convenience moat (~85% pre‑COVID ridership, 2023)

Service and experience sensitivity

Customers now demand concierge service, in‑store beauty consultations and seamless returns; 2024 surveys show 72% consider omnichannel (click‑and‑collect, easy exchanges) baseline and brands lose customers fast—returns or poor service drive ~43% immediate churn and 1‑star reviews can cut conversion by ~25%. Superior in‑store experience can partially reduce this bargaining power.

- Service expectation: concierge & consultations

- Omnichannel baseline: 72% (2024)

- Churn risk: ~43% from service/returns

- Reputation impact: ~25% conversion hit

High transparency and low switching boost buyer power; failures risk 43%

High price transparency and low switching costs (omnichannel baseline 72% in 2024) keep customer bargaining power high; loyalty campaigns drive double‑digit uplifts but train postponement. Tourist mix swings demand (MTR ridership ~85% of 2019 in 2023) and abundant alternatives punish stock‑outs and poor service (43% churn risk, ~25% conversion hit).

| Metric | Value |

|---|---|

| Omnichannel baseline (2024) | 72% |

| MTR ridership vs 2019 (2023) | ~85% |

| Churn from poor service/returns | ~43% |

| Conversion hit from 1‑star reviews | ~25% |

Preview Before You Purchase

Lifestyle International Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lifestyle International Holdings you'll receive upon purchase—no placeholders or mockups. The file is fully formatted, ready to download and use instantly. It provides the same comprehensive strategic assessment contained in the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Lifestyle International Holdings faces intense retail competition, evolving buyer preferences, and supplier concentration that shape its margins and growth prospects. Differentiation and omnichannel execution are key strategic levers amid moderate threat of new entrants and substitutes. This snapshot highlights core pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to explore detailed competitive dynamics and actionable recommendations.

Suppliers Bargaining Power

Global brand leverage

International fashion and cosmetics brands carry strong equity and often dictate terms, visual merchandising and pricing corridors; must‑have labels on Hong Kong premium floors can secure higher margins or marketing commitments. SOGO Causeway Bay, operated by Lifestyle International, drives unparalleled exposure with c.10 million annual visitors, which reduces supplier leverage but exclusive capsule drops or limited launch windows still tilt power toward marquee suppliers.

Concession model dynamics

The concession/consignment model shifts inventory risk to brands while embedding revenue‑sharing and staffing control with suppliers; high‑performing counters win leverage over space, staffing and promo calendars. Lifestyle offsets this by enforcing performance clauses and reallocating space based on sales density. Overall bargaining power is balanced but tilts to suppliers in star categories such as beauty, where counters drive footfall and margin.

Supplier fragmentation vs concentration

Household, FMCG and homeware suppliers to Lifestyle are highly fragmented, diluting bargaining power, while concentrated luxury/masstige cosmetics and major fashion houses exert stronger leverage; the global personal luxury goods market rose to about €366bn in 2023 and was projected near €398bn in 2024, amplifying supplier clout. Category mix creates a barbell of weak and strong supplier power, but active portfolio curation—adding emerging and regional brands—reduces reliance on dominant houses and mitigates concentration risk.

Private label and exclusives

Private label and exclusives cut supplier leverage by shifting spend from global brands to in-house ranges, improving gross margins; industry surveys in 2024 show department stores' private-label penetration ~8% versus specialty retailers ~25%, leaving room for Lifestyle to reweight assortments. Building proprietary home, accessories and gourmet ranges can lift margin and bargaining leverage, but success hinges on design capability and quality-control execution risk.

Logistics, currency, and lead times

Imported assortments expose Lifestyle International Holdings (1212.HK) to FX pass‑through despite the Hong Kong dollar peg to the USD, and long apparel lead times constrain in‑season flexibility, raising markdown risk if demand misses. Large, predictable orders secure better supplier terms while volatile demand weakens clout; SOGO’s scheduled sales events aggregate volume to negotiate rebates.

- 1212.HK: SOGO operator

- HKD pegged to USD

- Long lead times → higher markdown risk

- Aggregated sales cadence → better rebates

10M visitors dilute supplier clout; luxury fashion and beauty keep pricing power

SOGO Causeway Bay c.10m annual visitors reduces supplier clout but marquee fashion/beauty brands (global luxury market ~€398bn in 2024) retain pricing and launch leverage. Concession/consignment shifts inventory risk to suppliers; beauty counters tilt power. Private‑label penetration dept stores ~8% (2024) limits supplier power; long lead times raise markdown risk.

| Metric | Value (2024) |

|---|---|

| Annual visitors | ~10,000,000 |

| Global luxury market | ~€398bn |

| Private‑label dept stores | ~8% |

| Private‑label margin uplift | +20–30pp |

What is included in the product

Concise Porter's Five Forces assessment of Lifestyle International Holdings, highlighting competitive intensity in Hong Kong retail, buyer price sensitivity, supplier leverage, threat of substitutes and online disruption, and structural barriers that protect incumbency and affect profitability.

A concise one-sheet Porter’s Five Forces for Lifestyle International Holdings that highlights competitive pressures, supplier/buyer leverage and substitute threats—ready to drop into decks; tweak force intensities to model scenarios and simplify strategic decision-making.

Customers Bargaining Power

High price transparency

High price transparency lets shoppers compare instantly across brand boutiques, HKTVmall and cross‑border platforms, raising bargaining power; low switching costs drive frequent promotions and margin pressure. International travel and outlet shopping widen reference pricing, forcing department stores to justify premiums through superior service, loyalty benefits and exclusive merchandise to retain spend.

Loyalty programs and events

SOGO Rewards and annual Thankful Week create perceived value and switching frictions, often delivering double-digit sales uplift during campaign periods. Points, vouchers and member previews reduce immediate price sensitivity and raise repeat purchase rates. However recurring promotions train customers to postpone purchases, sustaining high buyer power. Targeted use of transaction and CRM data enables personalized offers to recover margin and improve basket size.

Tourist vs local mix

Mainland tourist flows rebounded in 2024, swinging category demand and raising discount expectations; when visitation softens, locals’ steady but value‑oriented spend gains share and increases buyer power. Currency and macro cycles can shift this mix quickly, altering average basket and markdown needs. Deeper merchandise assortments and diverse payment options help Lifestyle International flex across tourist and local segments.

Abundant alternatives

Abundant alternatives from specialty chains, brand stores, e‑commerce and outlets create overlapping assortments, enabling buyers to switch quickly; buyers now demand breadth and instant availability and penalize stock‑outs with rapid defection. Easy access via MTR hubs (weekday ridership recovered to about 85% of 2019 levels in 2023) compresses convenience differentiation for Lifestyle’s flagship formats.

- Overlapping assortments across channels

- High buyer leverage for breadth and immediacy

- Stock‑outs trigger rapid defections

- MTR access reduces convenience moat (~85% pre‑COVID ridership, 2023)

Service and experience sensitivity

Customers now demand concierge service, in‑store beauty consultations and seamless returns; 2024 surveys show 72% consider omnichannel (click‑and‑collect, easy exchanges) baseline and brands lose customers fast—returns or poor service drive ~43% immediate churn and 1‑star reviews can cut conversion by ~25%. Superior in‑store experience can partially reduce this bargaining power.

- Service expectation: concierge & consultations

- Omnichannel baseline: 72% (2024)

- Churn risk: ~43% from service/returns

- Reputation impact: ~25% conversion hit

High transparency and low switching boost buyer power; failures risk 43%

High price transparency and low switching costs (omnichannel baseline 72% in 2024) keep customer bargaining power high; loyalty campaigns drive double‑digit uplifts but train postponement. Tourist mix swings demand (MTR ridership ~85% of 2019 in 2023) and abundant alternatives punish stock‑outs and poor service (43% churn risk, ~25% conversion hit).

| Metric | Value |

|---|---|

| Omnichannel baseline (2024) | 72% |

| MTR ridership vs 2019 (2023) | ~85% |

| Churn from poor service/returns | ~43% |

| Conversion hit from 1‑star reviews | ~25% |

Preview Before You Purchase

Lifestyle International Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lifestyle International Holdings you'll receive upon purchase—no placeholders or mockups. The file is fully formatted, ready to download and use instantly. It provides the same comprehensive strategic assessment contained in the final deliverable.