Ligabue S.r.l. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Ligabue S.r.l. faces moderate supplier leverage, niche buyer segments, and evolving substitute threats that shape its competitive landscape; entry barriers in specialized markets limit new rivals but competitive intensity remains significant. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ligabue S.r.l.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global food inputs variability

Commodity swings in proteins, grains and produce drove margin pressure on fixed-price contracts in 2024—FAO food prices moved materially and proteins saw double-digit seasonal volatility—compressing Ligabue’s catering margins. Maritime cold-chain constraints and seasonal route shifts amplified input cost swings; global container rates eased in 2024 but route-specific spikes persisted. Ligabue limits risk via multi-region sourcing and menu flexibility, while long-term supplier contracts (used selectively) stabilize costs but reduce short-term agility.

Specialized logistics providers

Specialized cold-chain shippers, bonded warehouses and last-mile port agents are scarce near remote ports, driving switching costs and peak‑season service premiums (2024 cold‑chain market ~USD 322B). Ligabue’s integrated logistics expertise lowers supplier leverage but cannot erase capacity bottlenecks; SLAs and multi-year volume commitments help rebalance negotiating power.

Compliance and certification dependencies

HACCP (mandated by EU food hygiene rules and the US FDA seafood HACCP rule), Halal and Kosher certifications, plus IMO maritime safety standards, sharply narrow the pool of qualified suppliers; certified vendors typically charge premiums and impose longer lead times, and Ligabue’s audited supplier base reduces compliance risk while concentrating spend among fewer partners; dual-sourcing by certification category mitigates supplier hold-up risk.

Equipment and consumables OEMs

Galleys, refrigeration and hygiene systems depend on OEM parts and approved consumables; OEM lock-in raises aftermarket costs and enforces vendor-defined maintenance schedules, a dynamic still evident in 2024. Service at sea/offshore heightens reliance on authorized technicians and spare pipelines. Framework contracts and proactive inventory planning mitigate downtime and cost spikes.

Fuel and port service passthrough

Bunker fuel (IFO380) averaged about $560/ton in 2024, and bunker, port fees and handling charges directly lift delivered food cost; suppliers in these segments retain cyclical pricing power tied to energy markets and port congestion. Ligabue must hedge fuel or include indexation clauses to reprice clients; absent clauses, a margin squeeze is likely as pass-through windows tighten.

- Bunker: IFO380 ~$560/ton (2024)

- Port fee volatility: congestion-driven spikes

- Mitigation: hedging + indexation clauses

- Risk: margin squeeze if pass-through absent

Supplier leverage and fuel volatility compress margins; multi-sourcing and SLAs mitigate

Supplier leverage is high due to scarce cold‑chain shippers and certified vendors, compressing margins on fixed‑price contracts; multi‑region sourcing and menu flexibility partially offset this. OEM parts and offshore service dependency raise aftermarket costs and downtime risk. Bunker fuel (IFO380 ~$560/ton in 2024) and route‑specific container spikes transmit cost volatility to Ligabue; SLAs, framework contracts and indexation clauses are key mitigants.

| Metric | Value (2024) |

|---|---|

| Cold‑chain market | ~USD 322B |

| IFO380 | ~$560/ton |

| OEM lock‑in | Mandatory for warranties |

| Mitigants | Multi‑sourcing, SLAs, indexation |

What is included in the product

Tailored Porter's Five Forces analysis for Ligabue S.r.l. uncovering key drivers of competition, buyer and supplier power, substitutes and entry barriers, and identifying disruptive threats that affect pricing and profitability.

A compact Porter's Five Forces snapshot for Ligabue S.r.l.—rapidly highlights competitive pressures, supplier/buyer risks and regulatory threats to speed strategic decisions and relieve analysis overload.

Customers Bargaining Power

Concentrated B2B clients

Shipping lines, offshore operators and EPC contractors are highly concentrated buyers—top 5 container lines controlled about 75% of capacity in 2024—so they negotiate multi-country, multi‑vessel frameworks with aggressive terms. Volume scale gives them strong price leverage and tight KPIs; contracts often exceed $50–200M annually. Retention hinges on demonstrable cost and service advantages measured in per‑voyage cost and KPI compliance rates.

High switching feasibility at rebid

Tenders typically allow buyers to switch providers every 1–3 years, creating high rebid feasibility; Ligabue faces regular procurement churn. Data portability for menus, nutrition and inventory materially eases migration by preserving operational continuity. Mobilization to remote sites imposes near-term friction that moderates mid-contract switching. Robust onboarding playbooks reduce perceived buyer risk and accelerate transition confidence.

Price transparency and benchmarking

Global benchmarks like the FAO Food Price Index (avg ~115 in 2024) and rival spot quotes give buyers clear reference prices, driving demands for open-book costing and index-linked contracts and constraining margin expansion in stable commodity periods. Buyers pressure for CPI- or commodity-index escalation clauses. Differentiation must come from waste reduction, improved uptime, and crew satisfaction metrics.

Service breadth demands

Clients increasingly bundle catering with housekeeping, laundry and facility management, concentrating spend and giving buyers more leverage via single-award contracts; industry surveys in 2024 indicated about 60% of corporate buyers favor integrated providers. Deeper integration by Ligabue raises switching costs and permits cross-selling where price concessions are exchanged for greater share of wallet and higher retention.

Stringent compliance and penalties

SLAs commonly include liquidated damages—industry 2024 surveys cite typical ranges of 0.5–2% of contract value per breach—while buyers use performance data to negotiate 1–3% price-downs or credits; Ligabue’s certified quality systems materially reduce penalty exposure but require ongoing reinvestment (~0.8–1.5% of revenue); transparent reporting can lift contract renewals by ~10–15% in 2024 benchmarks.

- Liquidated damages: 0.5–2% of contract value

- Buyer leverage: 1–3% price-downs/credits

- Ligabue reinvestment: ~0.8–1.5% of revenue

- Reporting benefit: ~10–15% higher renewals

Consolidated buyers squeeze margins: top-5 carriers ~75% capacity, tenders 1-3 yrs, 1-3% cuts

Buyers are highly concentrated (top‑5 container lines ~75% capacity in 2024) and use scale to secure multi‑country frameworks with aggressive terms; tenders recur every 1–3 years, raising rebid risk. Open benchmarks (FAO index ~115 in 2024) and bundled sourcing (≈60% prefer integrated providers) compress margins; SLAs and liquidated damages (0.5–2%) enforce performance, buyers extract 1–3% price concessions.

| Metric | 2024 Value |

|---|---|

| Top‑5 capacity | ~75% |

| Tender frequency | 1–3 yrs |

| FAO Food Price Index | ~115 |

| Bundling preference | ~60% |

| Liquidated damages | 0.5–2% |

| Buyer price leverage | 1–3% |

What You See Is What You Get

Ligabue S.r.l. Porter's Five Forces Analysis

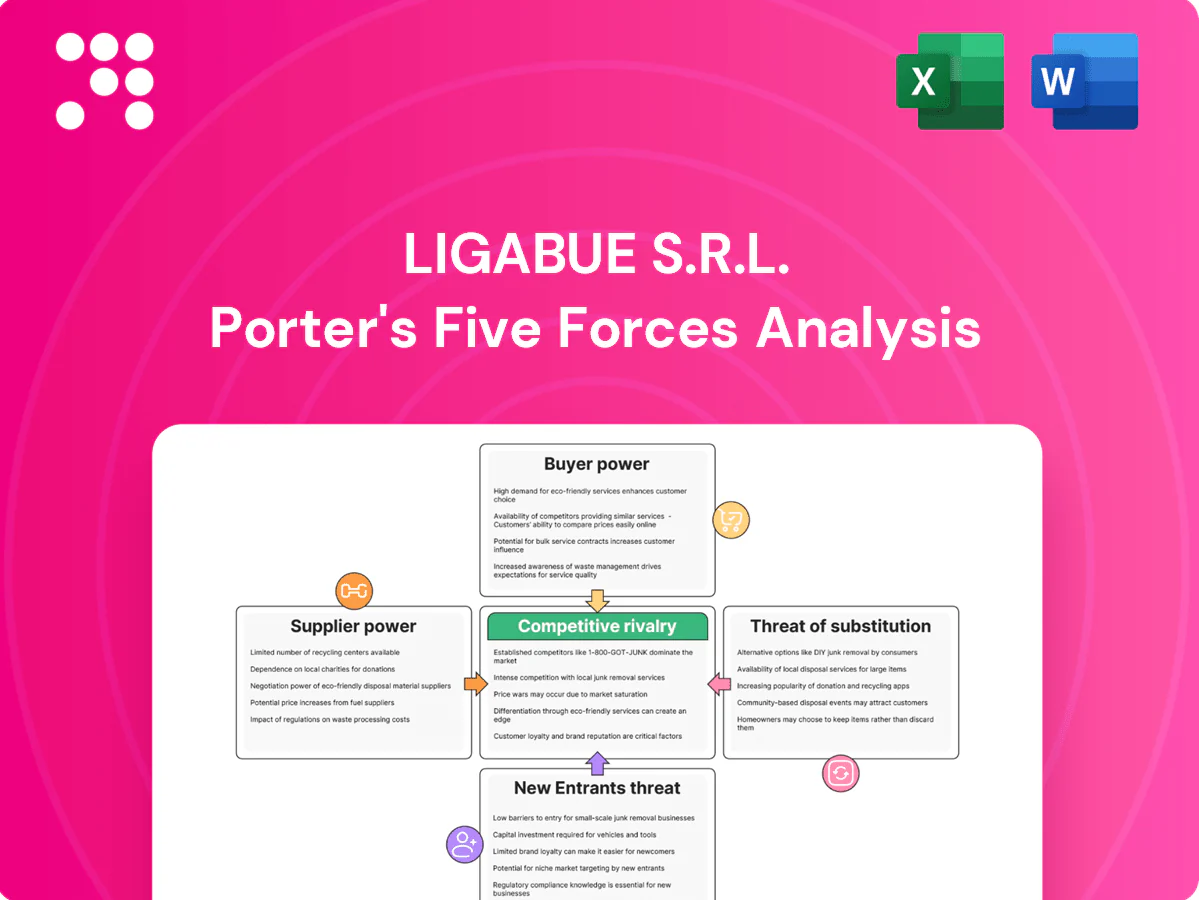

Ligabue S.r.l. Porter's Five Forces Analysis assesses industry rivalry, buyer and supplier power, threats of new entrants and substitutes, and regulatory influences to identify strategic leverage points and risks. It highlights barriers, cost dynamics, and bargaining asymmetries to guide pricing, sourcing and diversification decisions. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Don't Miss the Bigger Picture

Ligabue S.r.l. faces moderate supplier leverage, niche buyer segments, and evolving substitute threats that shape its competitive landscape; entry barriers in specialized markets limit new rivals but competitive intensity remains significant. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ligabue S.r.l.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global food inputs variability

Commodity swings in proteins, grains and produce drove margin pressure on fixed-price contracts in 2024—FAO food prices moved materially and proteins saw double-digit seasonal volatility—compressing Ligabue’s catering margins. Maritime cold-chain constraints and seasonal route shifts amplified input cost swings; global container rates eased in 2024 but route-specific spikes persisted. Ligabue limits risk via multi-region sourcing and menu flexibility, while long-term supplier contracts (used selectively) stabilize costs but reduce short-term agility.

Specialized logistics providers

Specialized cold-chain shippers, bonded warehouses and last-mile port agents are scarce near remote ports, driving switching costs and peak‑season service premiums (2024 cold‑chain market ~USD 322B). Ligabue’s integrated logistics expertise lowers supplier leverage but cannot erase capacity bottlenecks; SLAs and multi-year volume commitments help rebalance negotiating power.

Compliance and certification dependencies

HACCP (mandated by EU food hygiene rules and the US FDA seafood HACCP rule), Halal and Kosher certifications, plus IMO maritime safety standards, sharply narrow the pool of qualified suppliers; certified vendors typically charge premiums and impose longer lead times, and Ligabue’s audited supplier base reduces compliance risk while concentrating spend among fewer partners; dual-sourcing by certification category mitigates supplier hold-up risk.

Equipment and consumables OEMs

Galleys, refrigeration and hygiene systems depend on OEM parts and approved consumables; OEM lock-in raises aftermarket costs and enforces vendor-defined maintenance schedules, a dynamic still evident in 2024. Service at sea/offshore heightens reliance on authorized technicians and spare pipelines. Framework contracts and proactive inventory planning mitigate downtime and cost spikes.

Fuel and port service passthrough

Bunker fuel (IFO380) averaged about $560/ton in 2024, and bunker, port fees and handling charges directly lift delivered food cost; suppliers in these segments retain cyclical pricing power tied to energy markets and port congestion. Ligabue must hedge fuel or include indexation clauses to reprice clients; absent clauses, a margin squeeze is likely as pass-through windows tighten.

- Bunker: IFO380 ~$560/ton (2024)

- Port fee volatility: congestion-driven spikes

- Mitigation: hedging + indexation clauses

- Risk: margin squeeze if pass-through absent

Supplier leverage and fuel volatility compress margins; multi-sourcing and SLAs mitigate

Supplier leverage is high due to scarce cold‑chain shippers and certified vendors, compressing margins on fixed‑price contracts; multi‑region sourcing and menu flexibility partially offset this. OEM parts and offshore service dependency raise aftermarket costs and downtime risk. Bunker fuel (IFO380 ~$560/ton in 2024) and route‑specific container spikes transmit cost volatility to Ligabue; SLAs, framework contracts and indexation clauses are key mitigants.

| Metric | Value (2024) |

|---|---|

| Cold‑chain market | ~USD 322B |

| IFO380 | ~$560/ton |

| OEM lock‑in | Mandatory for warranties |

| Mitigants | Multi‑sourcing, SLAs, indexation |

What is included in the product

Tailored Porter's Five Forces analysis for Ligabue S.r.l. uncovering key drivers of competition, buyer and supplier power, substitutes and entry barriers, and identifying disruptive threats that affect pricing and profitability.

A compact Porter's Five Forces snapshot for Ligabue S.r.l.—rapidly highlights competitive pressures, supplier/buyer risks and regulatory threats to speed strategic decisions and relieve analysis overload.

Customers Bargaining Power

Concentrated B2B clients

Shipping lines, offshore operators and EPC contractors are highly concentrated buyers—top 5 container lines controlled about 75% of capacity in 2024—so they negotiate multi-country, multi‑vessel frameworks with aggressive terms. Volume scale gives them strong price leverage and tight KPIs; contracts often exceed $50–200M annually. Retention hinges on demonstrable cost and service advantages measured in per‑voyage cost and KPI compliance rates.

High switching feasibility at rebid

Tenders typically allow buyers to switch providers every 1–3 years, creating high rebid feasibility; Ligabue faces regular procurement churn. Data portability for menus, nutrition and inventory materially eases migration by preserving operational continuity. Mobilization to remote sites imposes near-term friction that moderates mid-contract switching. Robust onboarding playbooks reduce perceived buyer risk and accelerate transition confidence.

Price transparency and benchmarking

Global benchmarks like the FAO Food Price Index (avg ~115 in 2024) and rival spot quotes give buyers clear reference prices, driving demands for open-book costing and index-linked contracts and constraining margin expansion in stable commodity periods. Buyers pressure for CPI- or commodity-index escalation clauses. Differentiation must come from waste reduction, improved uptime, and crew satisfaction metrics.

Service breadth demands

Clients increasingly bundle catering with housekeeping, laundry and facility management, concentrating spend and giving buyers more leverage via single-award contracts; industry surveys in 2024 indicated about 60% of corporate buyers favor integrated providers. Deeper integration by Ligabue raises switching costs and permits cross-selling where price concessions are exchanged for greater share of wallet and higher retention.

Stringent compliance and penalties

SLAs commonly include liquidated damages—industry 2024 surveys cite typical ranges of 0.5–2% of contract value per breach—while buyers use performance data to negotiate 1–3% price-downs or credits; Ligabue’s certified quality systems materially reduce penalty exposure but require ongoing reinvestment (~0.8–1.5% of revenue); transparent reporting can lift contract renewals by ~10–15% in 2024 benchmarks.

- Liquidated damages: 0.5–2% of contract value

- Buyer leverage: 1–3% price-downs/credits

- Ligabue reinvestment: ~0.8–1.5% of revenue

- Reporting benefit: ~10–15% higher renewals

Consolidated buyers squeeze margins: top-5 carriers ~75% capacity, tenders 1-3 yrs, 1-3% cuts

Buyers are highly concentrated (top‑5 container lines ~75% capacity in 2024) and use scale to secure multi‑country frameworks with aggressive terms; tenders recur every 1–3 years, raising rebid risk. Open benchmarks (FAO index ~115 in 2024) and bundled sourcing (≈60% prefer integrated providers) compress margins; SLAs and liquidated damages (0.5–2%) enforce performance, buyers extract 1–3% price concessions.

| Metric | 2024 Value |

|---|---|

| Top‑5 capacity | ~75% |

| Tender frequency | 1–3 yrs |

| FAO Food Price Index | ~115 |

| Bundling preference | ~60% |

| Liquidated damages | 0.5–2% |

| Buyer price leverage | 1–3% |

What You See Is What You Get

Ligabue S.r.l. Porter's Five Forces Analysis

Ligabue S.r.l. Porter's Five Forces Analysis assesses industry rivalry, buyer and supplier power, threats of new entrants and substitutes, and regulatory influences to identify strategic leverage points and risks. It highlights barriers, cost dynamics, and bargaining asymmetries to guide pricing, sourcing and diversification decisions. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ligabue S.r.l. faces moderate supplier leverage, niche buyer segments, and evolving substitute threats that shape its competitive landscape; entry barriers in specialized markets limit new rivals but competitive intensity remains significant. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ligabue S.r.l.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global food inputs variability

Commodity swings in proteins, grains and produce drove margin pressure on fixed-price contracts in 2024—FAO food prices moved materially and proteins saw double-digit seasonal volatility—compressing Ligabue’s catering margins. Maritime cold-chain constraints and seasonal route shifts amplified input cost swings; global container rates eased in 2024 but route-specific spikes persisted. Ligabue limits risk via multi-region sourcing and menu flexibility, while long-term supplier contracts (used selectively) stabilize costs but reduce short-term agility.

Specialized logistics providers

Specialized cold-chain shippers, bonded warehouses and last-mile port agents are scarce near remote ports, driving switching costs and peak‑season service premiums (2024 cold‑chain market ~USD 322B). Ligabue’s integrated logistics expertise lowers supplier leverage but cannot erase capacity bottlenecks; SLAs and multi-year volume commitments help rebalance negotiating power.

Compliance and certification dependencies

HACCP (mandated by EU food hygiene rules and the US FDA seafood HACCP rule), Halal and Kosher certifications, plus IMO maritime safety standards, sharply narrow the pool of qualified suppliers; certified vendors typically charge premiums and impose longer lead times, and Ligabue’s audited supplier base reduces compliance risk while concentrating spend among fewer partners; dual-sourcing by certification category mitigates supplier hold-up risk.

Equipment and consumables OEMs

Galleys, refrigeration and hygiene systems depend on OEM parts and approved consumables; OEM lock-in raises aftermarket costs and enforces vendor-defined maintenance schedules, a dynamic still evident in 2024. Service at sea/offshore heightens reliance on authorized technicians and spare pipelines. Framework contracts and proactive inventory planning mitigate downtime and cost spikes.

Fuel and port service passthrough

Bunker fuel (IFO380) averaged about $560/ton in 2024, and bunker, port fees and handling charges directly lift delivered food cost; suppliers in these segments retain cyclical pricing power tied to energy markets and port congestion. Ligabue must hedge fuel or include indexation clauses to reprice clients; absent clauses, a margin squeeze is likely as pass-through windows tighten.

- Bunker: IFO380 ~$560/ton (2024)

- Port fee volatility: congestion-driven spikes

- Mitigation: hedging + indexation clauses

- Risk: margin squeeze if pass-through absent

Supplier leverage and fuel volatility compress margins; multi-sourcing and SLAs mitigate

Supplier leverage is high due to scarce cold‑chain shippers and certified vendors, compressing margins on fixed‑price contracts; multi‑region sourcing and menu flexibility partially offset this. OEM parts and offshore service dependency raise aftermarket costs and downtime risk. Bunker fuel (IFO380 ~$560/ton in 2024) and route‑specific container spikes transmit cost volatility to Ligabue; SLAs, framework contracts and indexation clauses are key mitigants.

| Metric | Value (2024) |

|---|---|

| Cold‑chain market | ~USD 322B |

| IFO380 | ~$560/ton |

| OEM lock‑in | Mandatory for warranties |

| Mitigants | Multi‑sourcing, SLAs, indexation |

What is included in the product

Tailored Porter's Five Forces analysis for Ligabue S.r.l. uncovering key drivers of competition, buyer and supplier power, substitutes and entry barriers, and identifying disruptive threats that affect pricing and profitability.

A compact Porter's Five Forces snapshot for Ligabue S.r.l.—rapidly highlights competitive pressures, supplier/buyer risks and regulatory threats to speed strategic decisions and relieve analysis overload.

Customers Bargaining Power

Concentrated B2B clients

Shipping lines, offshore operators and EPC contractors are highly concentrated buyers—top 5 container lines controlled about 75% of capacity in 2024—so they negotiate multi-country, multi‑vessel frameworks with aggressive terms. Volume scale gives them strong price leverage and tight KPIs; contracts often exceed $50–200M annually. Retention hinges on demonstrable cost and service advantages measured in per‑voyage cost and KPI compliance rates.

High switching feasibility at rebid

Tenders typically allow buyers to switch providers every 1–3 years, creating high rebid feasibility; Ligabue faces regular procurement churn. Data portability for menus, nutrition and inventory materially eases migration by preserving operational continuity. Mobilization to remote sites imposes near-term friction that moderates mid-contract switching. Robust onboarding playbooks reduce perceived buyer risk and accelerate transition confidence.

Price transparency and benchmarking

Global benchmarks like the FAO Food Price Index (avg ~115 in 2024) and rival spot quotes give buyers clear reference prices, driving demands for open-book costing and index-linked contracts and constraining margin expansion in stable commodity periods. Buyers pressure for CPI- or commodity-index escalation clauses. Differentiation must come from waste reduction, improved uptime, and crew satisfaction metrics.

Service breadth demands

Clients increasingly bundle catering with housekeeping, laundry and facility management, concentrating spend and giving buyers more leverage via single-award contracts; industry surveys in 2024 indicated about 60% of corporate buyers favor integrated providers. Deeper integration by Ligabue raises switching costs and permits cross-selling where price concessions are exchanged for greater share of wallet and higher retention.

Stringent compliance and penalties

SLAs commonly include liquidated damages—industry 2024 surveys cite typical ranges of 0.5–2% of contract value per breach—while buyers use performance data to negotiate 1–3% price-downs or credits; Ligabue’s certified quality systems materially reduce penalty exposure but require ongoing reinvestment (~0.8–1.5% of revenue); transparent reporting can lift contract renewals by ~10–15% in 2024 benchmarks.

- Liquidated damages: 0.5–2% of contract value

- Buyer leverage: 1–3% price-downs/credits

- Ligabue reinvestment: ~0.8–1.5% of revenue

- Reporting benefit: ~10–15% higher renewals

Consolidated buyers squeeze margins: top-5 carriers ~75% capacity, tenders 1-3 yrs, 1-3% cuts

Buyers are highly concentrated (top‑5 container lines ~75% capacity in 2024) and use scale to secure multi‑country frameworks with aggressive terms; tenders recur every 1–3 years, raising rebid risk. Open benchmarks (FAO index ~115 in 2024) and bundled sourcing (≈60% prefer integrated providers) compress margins; SLAs and liquidated damages (0.5–2%) enforce performance, buyers extract 1–3% price concessions.

| Metric | 2024 Value |

|---|---|

| Top‑5 capacity | ~75% |

| Tender frequency | 1–3 yrs |

| FAO Food Price Index | ~115 |

| Bundling preference | ~60% |

| Liquidated damages | 0.5–2% |

| Buyer price leverage | 1–3% |

What You See Is What You Get

Ligabue S.r.l. Porter's Five Forces Analysis

Ligabue S.r.l. Porter's Five Forces Analysis assesses industry rivalry, buyer and supplier power, threats of new entrants and substitutes, and regulatory influences to identify strategic leverage points and risks. It highlights barriers, cost dynamics, and bargaining asymmetries to guide pricing, sourcing and diversification decisions. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use.