Liljedahl Group AB PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Liljedahl Group AB—three to five targeted insights reveal how political, economic, social, technological, legal, and environmental forces shape its outlook. Perfect for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use data.

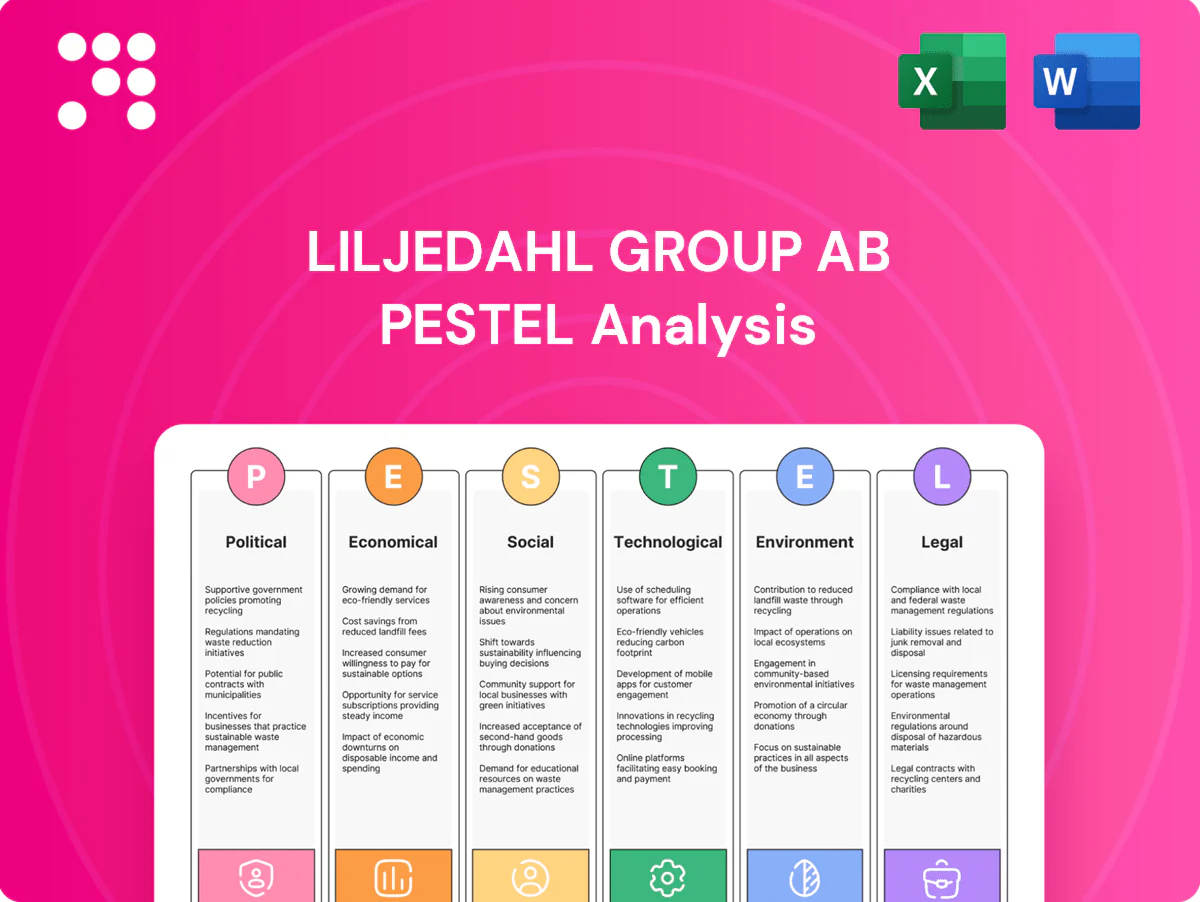

Political factors

EU industrial and energy policy

EU Green Deal (climate neutrality by 2050) and the Net-Zero Industry Act (targeting at least 40% EU production of key net-zero technologies by 2030) plus grid modernization drive demand for Liljedahl Group AB’s electrification-focused holdings. Subsidies and public procurement can accelerate orders but impose strict compliance and reporting. EU investment needs estimated at about EUR 520bn/yr to 2030 support long-term capital plans in Sweden and the EU, though post-election shifts could reprioritize funding and timelines.

Trade policy and tariffs

US–EU–China tensions disrupt component and metal flows for electrical equipment, with LME copper around 9,500 USD/t and aluminum near 2,300 USD/t (mid‑2025), amplifying supply risk. Tariff shifts—notably US tariffs on Chinese goods in the 7.5–25% range—can compress margins on copper/aluminum products and electronics. Preferential EU trade deals provide alternative sourcing corridors. Strict origin rules and fines, back duties and interest make monitoring critical.

Public infrastructure spending

Government-backed grid upgrades, rail electrification and renewable interconnections expand addressable markets for Liljedahl Group by unlocking demand for electrical and civil works; EU Recovery and Resilience Facility mobilizes €723.8 billion 2021–2026 to support such infrastructure. Multi-year budgets give project visibility but remain exposed to fiscal pressure and shifting allocations. Regional funding priorities and tender rules increasingly favor local content and verifiable sustainability credentials, shaping plant footprint and sales mix.

Geopolitical supply risk

Conflicts and sanctions since 2022 have tightened flows of raw materials and critical components, creating episodic disruption risks for Liljedahl Group AB’s laminated packaging and component sourcing through 2024.

Diversifying suppliers and nearshoring within Europe reduces exposure; higher insurance and inventory buffers improve resilience but raise working capital needs in 2024.

Board-level scenario planning and stress tests through 2024 inform portfolio resilience and procurement flexibility.

- Risk: sanctions-driven supply interruptions

- Mitigation: supplier diversification, nearshoring in Europe

- Cost: higher insurance and inventory inflate working capital

- Governance: board-led scenario planning

Labor and industrial relations

Stable labor relations and low strike incidence in the Nordics support productivity in advanced manufacturing, aiding predictable operations and supply chains.

Political debates on labor migration and targeted reskilling incentives (increasing EU/Swedish funding for upskilling) will directly affect technical talent availability and ease skill shortages.

- coverage: ~85–90% collective bargaining

- impact: low strike risk, higher productivity

- risk: migration policy limits talent

- opportunity: reskilling incentives to fill technical gaps

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

EU Green Deal and Net‑Zero Industry Act (40% EU production target by 2030) plus EUR 520bn/yr investment need to 2030 boost electrification demand; RRRF €723.8bn (2021–26) funds grid/rail projects. Mid‑2025 LME copper ~9,500 USD/t, aluminum ~2,300 USD/t; tariffs and sanctions since 2022 raise supply risk. Nordic collective bargaining ~85–90% limits pay flexibility; nearshoring raises working capital.

| Indicator | Latest | Implication |

|---|---|---|

| EU invest need | ≈EUR 520bn/yr to 2030 | Long‑term demand |

| Copper (LME) | ~9,500 USD/t (mid‑2025) | Input cost volatility |

| Collective bargaining | 85–90% | Stable labor, limited pay flexibility |

What is included in the product

Provides a concise PESTLE review of Liljedahl Group AB, analyzing Political, Economic, Social, Technological, Environmental and Legal forces shaping its packaging and paper business; each section links current data and trends to strategic risks and opportunities. Designed for executives and investors to support scenario planning, funding pitches and operational decision-making.

A clean, summarized PESTLE of Liljedahl Group AB that’s visually segmented for quick meetings, easily editable for local context and drop-in ready for presentations.

Economic factors

Industrial cycle sensitivity

Demand for Liljedahl Group AB’s electrical products is cyclical and closely tracks capex and construction; Eurozone manufacturing PMI slipped below 50 through much of 2024, signalling softer demand. Diversified end-markets (industrial, utilities, construction) mute swings, while high-quality order backlog and c.30% recurring service revenues in 2024 helped smooth earnings. Early indicators to watch: PMI trends, announced grid capex plans, and housing starts.

Interest rates and cost of capital

Higher interest rates compress valuations and reduce M&A leverage headroom for Liljedahl Group; Sweden’s Riksbank policy rate stood at 4.00% in July 2024, lifting corporate borrowing costs and refinancing hurdles. A blend of fixed-to-floating debt and interest hedges mitigates financing volatility. Customer capex approvals historically slow as rates rise, while any sustained rate relief would broaden investment and refinancing options.

Commodity prices (copper/aluminum)

Metal price swings directly affect Liljedahl Group ABs input costs and inventory valuations; LME copper averaged about 8,500 USD/ton in 2024 and primary aluminum near 2,300 USD/ton, amplifying margin pressure on tight contracts. Pass-through clauses and dynamic pricing mitigate impact but often lag market moves. Strategic sourcing and scrap recycling lower exposure, while hedging policies are calibrated to the companys cash-flow needs and risk appetite.

FX exposure (SEK/EUR/USD)

Liljedahl Group faces translation and transaction FX risks from revenue and sourcing in SEK, EUR and USD, with natural hedges where costs match currency receipts but residual exposures remain.

Use of forwards and FX swaps can stabilize reported EBITDA yet increases hedging complexity and counterparty risk.

FX rates materially affect cross-border M&A affordability by changing acquisition pricing and debt-servicing in foreign currencies.

- Exposure: SEK/EUR/USD translation and transaction risk

- Mitigation: matched-cost natural hedges, but gaps persist

- Derivatives: reduce EBITDA volatility, add complexity

- M&A: FX shifts alter target affordability

M&A market and multiples

Deal flow in industrial tech and electrification remains highly competitive, with add-ons accounting for about two-thirds of private equity buyouts in 2024 (Preqin), pushing multiples upward. Valuation discipline and clear value-creation playbooks are essential as buyers target 10–15x EBITDA segments in electrification and 8–12x in industrial tech. Add-on acquisitions can unlock operational and channel synergies, but integration capacity ultimately sets the practical pace of growth.

- Deal flow: competitive; add-ons ~2/3 of PE buyouts (2024)

- Multiples: electrification 10–15x, industrial tech 8–12x

- Focus: valuation discipline + value-creation playbooks

- Constraint: integration capacity limits growth

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

Demand is cyclical; Eurozone manufacturing PMI stayed below 50 through much of 2024, while c.30% recurring service revenue in 2024 and diversified end-markets smooth earnings. Riksbank rate 4.00% (Jul 2024) raises borrowing costs and slows capex; rate relief would ease refinancing. LME copper ~8,500 USD/t and aluminium ~2,300 USD/t in 2024 pressure margins; FX (SEK/EUR/USD) and competitive PE multiples (electrification 10–15x) affect M&A.

| Metric | Value (2024) |

|---|---|

| Eurozone PMI | <50 |

| Recurring rev | ~30% |

| Riksbank rate | 4.00% |

| Copper (LME) | ~8,500 USD/t |

| Aluminium | ~2,300 USD/t |

| PE multiples (electr.) | 10–15x |

What You See Is What You Get

Liljedahl Group AB PESTLE Analysis

The preview shown here is the exact Liljedahl Group AB PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with actionable insights. No placeholders or teasers—this is the final file you can download immediately after payment.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Liljedahl Group AB—three to five targeted insights reveal how political, economic, social, technological, legal, and environmental forces shape its outlook. Perfect for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use data.

Political factors

EU industrial and energy policy

EU Green Deal (climate neutrality by 2050) and the Net-Zero Industry Act (targeting at least 40% EU production of key net-zero technologies by 2030) plus grid modernization drive demand for Liljedahl Group AB’s electrification-focused holdings. Subsidies and public procurement can accelerate orders but impose strict compliance and reporting. EU investment needs estimated at about EUR 520bn/yr to 2030 support long-term capital plans in Sweden and the EU, though post-election shifts could reprioritize funding and timelines.

Trade policy and tariffs

US–EU–China tensions disrupt component and metal flows for electrical equipment, with LME copper around 9,500 USD/t and aluminum near 2,300 USD/t (mid‑2025), amplifying supply risk. Tariff shifts—notably US tariffs on Chinese goods in the 7.5–25% range—can compress margins on copper/aluminum products and electronics. Preferential EU trade deals provide alternative sourcing corridors. Strict origin rules and fines, back duties and interest make monitoring critical.

Public infrastructure spending

Government-backed grid upgrades, rail electrification and renewable interconnections expand addressable markets for Liljedahl Group by unlocking demand for electrical and civil works; EU Recovery and Resilience Facility mobilizes €723.8 billion 2021–2026 to support such infrastructure. Multi-year budgets give project visibility but remain exposed to fiscal pressure and shifting allocations. Regional funding priorities and tender rules increasingly favor local content and verifiable sustainability credentials, shaping plant footprint and sales mix.

Geopolitical supply risk

Conflicts and sanctions since 2022 have tightened flows of raw materials and critical components, creating episodic disruption risks for Liljedahl Group AB’s laminated packaging and component sourcing through 2024.

Diversifying suppliers and nearshoring within Europe reduces exposure; higher insurance and inventory buffers improve resilience but raise working capital needs in 2024.

Board-level scenario planning and stress tests through 2024 inform portfolio resilience and procurement flexibility.

- Risk: sanctions-driven supply interruptions

- Mitigation: supplier diversification, nearshoring in Europe

- Cost: higher insurance and inventory inflate working capital

- Governance: board-led scenario planning

Labor and industrial relations

Stable labor relations and low strike incidence in the Nordics support productivity in advanced manufacturing, aiding predictable operations and supply chains.

Political debates on labor migration and targeted reskilling incentives (increasing EU/Swedish funding for upskilling) will directly affect technical talent availability and ease skill shortages.

- coverage: ~85–90% collective bargaining

- impact: low strike risk, higher productivity

- risk: migration policy limits talent

- opportunity: reskilling incentives to fill technical gaps

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

EU Green Deal and Net‑Zero Industry Act (40% EU production target by 2030) plus EUR 520bn/yr investment need to 2030 boost electrification demand; RRRF €723.8bn (2021–26) funds grid/rail projects. Mid‑2025 LME copper ~9,500 USD/t, aluminum ~2,300 USD/t; tariffs and sanctions since 2022 raise supply risk. Nordic collective bargaining ~85–90% limits pay flexibility; nearshoring raises working capital.

| Indicator | Latest | Implication |

|---|---|---|

| EU invest need | ≈EUR 520bn/yr to 2030 | Long‑term demand |

| Copper (LME) | ~9,500 USD/t (mid‑2025) | Input cost volatility |

| Collective bargaining | 85–90% | Stable labor, limited pay flexibility |

What is included in the product

Provides a concise PESTLE review of Liljedahl Group AB, analyzing Political, Economic, Social, Technological, Environmental and Legal forces shaping its packaging and paper business; each section links current data and trends to strategic risks and opportunities. Designed for executives and investors to support scenario planning, funding pitches and operational decision-making.

A clean, summarized PESTLE of Liljedahl Group AB that’s visually segmented for quick meetings, easily editable for local context and drop-in ready for presentations.

Economic factors

Industrial cycle sensitivity

Demand for Liljedahl Group AB’s electrical products is cyclical and closely tracks capex and construction; Eurozone manufacturing PMI slipped below 50 through much of 2024, signalling softer demand. Diversified end-markets (industrial, utilities, construction) mute swings, while high-quality order backlog and c.30% recurring service revenues in 2024 helped smooth earnings. Early indicators to watch: PMI trends, announced grid capex plans, and housing starts.

Interest rates and cost of capital

Higher interest rates compress valuations and reduce M&A leverage headroom for Liljedahl Group; Sweden’s Riksbank policy rate stood at 4.00% in July 2024, lifting corporate borrowing costs and refinancing hurdles. A blend of fixed-to-floating debt and interest hedges mitigates financing volatility. Customer capex approvals historically slow as rates rise, while any sustained rate relief would broaden investment and refinancing options.

Commodity prices (copper/aluminum)

Metal price swings directly affect Liljedahl Group ABs input costs and inventory valuations; LME copper averaged about 8,500 USD/ton in 2024 and primary aluminum near 2,300 USD/ton, amplifying margin pressure on tight contracts. Pass-through clauses and dynamic pricing mitigate impact but often lag market moves. Strategic sourcing and scrap recycling lower exposure, while hedging policies are calibrated to the companys cash-flow needs and risk appetite.

FX exposure (SEK/EUR/USD)

Liljedahl Group faces translation and transaction FX risks from revenue and sourcing in SEK, EUR and USD, with natural hedges where costs match currency receipts but residual exposures remain.

Use of forwards and FX swaps can stabilize reported EBITDA yet increases hedging complexity and counterparty risk.

FX rates materially affect cross-border M&A affordability by changing acquisition pricing and debt-servicing in foreign currencies.

- Exposure: SEK/EUR/USD translation and transaction risk

- Mitigation: matched-cost natural hedges, but gaps persist

- Derivatives: reduce EBITDA volatility, add complexity

- M&A: FX shifts alter target affordability

M&A market and multiples

Deal flow in industrial tech and electrification remains highly competitive, with add-ons accounting for about two-thirds of private equity buyouts in 2024 (Preqin), pushing multiples upward. Valuation discipline and clear value-creation playbooks are essential as buyers target 10–15x EBITDA segments in electrification and 8–12x in industrial tech. Add-on acquisitions can unlock operational and channel synergies, but integration capacity ultimately sets the practical pace of growth.

- Deal flow: competitive; add-ons ~2/3 of PE buyouts (2024)

- Multiples: electrification 10–15x, industrial tech 8–12x

- Focus: valuation discipline + value-creation playbooks

- Constraint: integration capacity limits growth

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

Demand is cyclical; Eurozone manufacturing PMI stayed below 50 through much of 2024, while c.30% recurring service revenue in 2024 and diversified end-markets smooth earnings. Riksbank rate 4.00% (Jul 2024) raises borrowing costs and slows capex; rate relief would ease refinancing. LME copper ~8,500 USD/t and aluminium ~2,300 USD/t in 2024 pressure margins; FX (SEK/EUR/USD) and competitive PE multiples (electrification 10–15x) affect M&A.

| Metric | Value (2024) |

|---|---|

| Eurozone PMI | <50 |

| Recurring rev | ~30% |

| Riksbank rate | 4.00% |

| Copper (LME) | ~8,500 USD/t |

| Aluminium | ~2,300 USD/t |

| PE multiples (electr.) | 10–15x |

What You See Is What You Get

Liljedahl Group AB PESTLE Analysis

The preview shown here is the exact Liljedahl Group AB PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with actionable insights. No placeholders or teasers—this is the final file you can download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Liljedahl Group AB—three to five targeted insights reveal how political, economic, social, technological, legal, and environmental forces shape its outlook. Perfect for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use data.

Political factors

EU industrial and energy policy

EU Green Deal (climate neutrality by 2050) and the Net-Zero Industry Act (targeting at least 40% EU production of key net-zero technologies by 2030) plus grid modernization drive demand for Liljedahl Group AB’s electrification-focused holdings. Subsidies and public procurement can accelerate orders but impose strict compliance and reporting. EU investment needs estimated at about EUR 520bn/yr to 2030 support long-term capital plans in Sweden and the EU, though post-election shifts could reprioritize funding and timelines.

Trade policy and tariffs

US–EU–China tensions disrupt component and metal flows for electrical equipment, with LME copper around 9,500 USD/t and aluminum near 2,300 USD/t (mid‑2025), amplifying supply risk. Tariff shifts—notably US tariffs on Chinese goods in the 7.5–25% range—can compress margins on copper/aluminum products and electronics. Preferential EU trade deals provide alternative sourcing corridors. Strict origin rules and fines, back duties and interest make monitoring critical.

Public infrastructure spending

Government-backed grid upgrades, rail electrification and renewable interconnections expand addressable markets for Liljedahl Group by unlocking demand for electrical and civil works; EU Recovery and Resilience Facility mobilizes €723.8 billion 2021–2026 to support such infrastructure. Multi-year budgets give project visibility but remain exposed to fiscal pressure and shifting allocations. Regional funding priorities and tender rules increasingly favor local content and verifiable sustainability credentials, shaping plant footprint and sales mix.

Geopolitical supply risk

Conflicts and sanctions since 2022 have tightened flows of raw materials and critical components, creating episodic disruption risks for Liljedahl Group AB’s laminated packaging and component sourcing through 2024.

Diversifying suppliers and nearshoring within Europe reduces exposure; higher insurance and inventory buffers improve resilience but raise working capital needs in 2024.

Board-level scenario planning and stress tests through 2024 inform portfolio resilience and procurement flexibility.

- Risk: sanctions-driven supply interruptions

- Mitigation: supplier diversification, nearshoring in Europe

- Cost: higher insurance and inventory inflate working capital

- Governance: board-led scenario planning

Labor and industrial relations

Stable labor relations and low strike incidence in the Nordics support productivity in advanced manufacturing, aiding predictable operations and supply chains.

Political debates on labor migration and targeted reskilling incentives (increasing EU/Swedish funding for upskilling) will directly affect technical talent availability and ease skill shortages.

- coverage: ~85–90% collective bargaining

- impact: low strike risk, higher productivity

- risk: migration policy limits talent

- opportunity: reskilling incentives to fill technical gaps

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

EU Green Deal and Net‑Zero Industry Act (40% EU production target by 2030) plus EUR 520bn/yr investment need to 2030 boost electrification demand; RRRF €723.8bn (2021–26) funds grid/rail projects. Mid‑2025 LME copper ~9,500 USD/t, aluminum ~2,300 USD/t; tariffs and sanctions since 2022 raise supply risk. Nordic collective bargaining ~85–90% limits pay flexibility; nearshoring raises working capital.

| Indicator | Latest | Implication |

|---|---|---|

| EU invest need | ≈EUR 520bn/yr to 2030 | Long‑term demand |

| Copper (LME) | ~9,500 USD/t (mid‑2025) | Input cost volatility |

| Collective bargaining | 85–90% | Stable labor, limited pay flexibility |

What is included in the product

Provides a concise PESTLE review of Liljedahl Group AB, analyzing Political, Economic, Social, Technological, Environmental and Legal forces shaping its packaging and paper business; each section links current data and trends to strategic risks and opportunities. Designed for executives and investors to support scenario planning, funding pitches and operational decision-making.

A clean, summarized PESTLE of Liljedahl Group AB that’s visually segmented for quick meetings, easily editable for local context and drop-in ready for presentations.

Economic factors

Industrial cycle sensitivity

Demand for Liljedahl Group AB’s electrical products is cyclical and closely tracks capex and construction; Eurozone manufacturing PMI slipped below 50 through much of 2024, signalling softer demand. Diversified end-markets (industrial, utilities, construction) mute swings, while high-quality order backlog and c.30% recurring service revenues in 2024 helped smooth earnings. Early indicators to watch: PMI trends, announced grid capex plans, and housing starts.

Interest rates and cost of capital

Higher interest rates compress valuations and reduce M&A leverage headroom for Liljedahl Group; Sweden’s Riksbank policy rate stood at 4.00% in July 2024, lifting corporate borrowing costs and refinancing hurdles. A blend of fixed-to-floating debt and interest hedges mitigates financing volatility. Customer capex approvals historically slow as rates rise, while any sustained rate relief would broaden investment and refinancing options.

Commodity prices (copper/aluminum)

Metal price swings directly affect Liljedahl Group ABs input costs and inventory valuations; LME copper averaged about 8,500 USD/ton in 2024 and primary aluminum near 2,300 USD/ton, amplifying margin pressure on tight contracts. Pass-through clauses and dynamic pricing mitigate impact but often lag market moves. Strategic sourcing and scrap recycling lower exposure, while hedging policies are calibrated to the companys cash-flow needs and risk appetite.

FX exposure (SEK/EUR/USD)

Liljedahl Group faces translation and transaction FX risks from revenue and sourcing in SEK, EUR and USD, with natural hedges where costs match currency receipts but residual exposures remain.

Use of forwards and FX swaps can stabilize reported EBITDA yet increases hedging complexity and counterparty risk.

FX rates materially affect cross-border M&A affordability by changing acquisition pricing and debt-servicing in foreign currencies.

- Exposure: SEK/EUR/USD translation and transaction risk

- Mitigation: matched-cost natural hedges, but gaps persist

- Derivatives: reduce EBITDA volatility, add complexity

- M&A: FX shifts alter target affordability

M&A market and multiples

Deal flow in industrial tech and electrification remains highly competitive, with add-ons accounting for about two-thirds of private equity buyouts in 2024 (Preqin), pushing multiples upward. Valuation discipline and clear value-creation playbooks are essential as buyers target 10–15x EBITDA segments in electrification and 8–12x in industrial tech. Add-on acquisitions can unlock operational and channel synergies, but integration capacity ultimately sets the practical pace of growth.

- Deal flow: competitive; add-ons ~2/3 of PE buyouts (2024)

- Multiples: electrification 10–15x, industrial tech 8–12x

- Focus: valuation discipline + value-creation playbooks

- Constraint: integration capacity limits growth

EU net-zero: ≈EUR 520bn/yr to 2030, 40% output target; metals, labor & supply risks

Demand is cyclical; Eurozone manufacturing PMI stayed below 50 through much of 2024, while c.30% recurring service revenue in 2024 and diversified end-markets smooth earnings. Riksbank rate 4.00% (Jul 2024) raises borrowing costs and slows capex; rate relief would ease refinancing. LME copper ~8,500 USD/t and aluminium ~2,300 USD/t in 2024 pressure margins; FX (SEK/EUR/USD) and competitive PE multiples (electrification 10–15x) affect M&A.

| Metric | Value (2024) |

|---|---|

| Eurozone PMI | <50 |

| Recurring rev | ~30% |

| Riksbank rate | 4.00% |

| Copper (LME) | ~8,500 USD/t |

| Aluminium | ~2,300 USD/t |

| PE multiples (electr.) | 10–15x |

What You See Is What You Get

Liljedahl Group AB PESTLE Analysis

The preview shown here is the exact Liljedahl Group AB PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with actionable insights. No placeholders or teasers—this is the final file you can download immediately after payment.