Eli Lilly Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Eli Lilly faces intense competitive rivalry driven by blockbuster drugs, patent cliffs and aggressive R&D rivals, while buyer and supplier power, regulatory scrutiny, and substitute therapies shape its margins and strategic choices. Understanding these forces highlights where Lilly can defend pricing or pivot investment. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Eli Lilly’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialized inputs

Lilly depends on a small set of suppliers for critical APIs, biologics media, single‑use systems and rare excipients, which raises switching costs and extends lead times. Supplier concentration increases risk of launch delays or supply constraints; Lilly reported $43.1B revenue in 2024 and said supplier resilience was a strategic priority. Dual‑sourcing and long‑term contracts partially mitigate this supplier power but cannot eliminate single‑source bottlenecks.

Biologics and advanced modalities

Complex biologics, peptides and GLP‑1 manufacturing heighten supplier leverage as specialized equipment, cell lines and cold‑chain logistics are poorly substitutable; top biopharma CDMOs held roughly 55% of global biologics capacity in 2023. Technology transfers for biologics commonly take 12–24 months and cost tens of millions, slowing vendor switches. Approved second sources reduce but do not eliminate dependency due to qualification time and capacity constraints.

Regulatory and quality gatekeeping

cGMP compliance ties Eli Lilly to a limited pool of qualified suppliers that pass FDA audits; as of 2024 cGMP is codified under 21 CFR Parts 210 and 211. Any supplier change triggers regulatory filings and validation, raising supplier stickiness and negotiating leverage. Strong QA oversight lets Lilly push back on price/terms but increases time and cost for sourcing changes.

IP, exclusivity, and custom components

Supplier-held IP for device components, novel excipients and delivery systems raises switching costs and can push prices up; customization narrows vendor options and increases dependency. Co-development deals (used by Lilly to secure biologics and device access) can lock suppliers while sharing margin upside; 2024 R&D investment remained above $8B, increasing bargaining leverage through partnerships.

- Proprietary inputs elevate price power

- Customization reduces supplier pool

- Co-development secures access and aligns value

Scale counterbalances vendor power

Lilly’s sheer volume, improved forecasting and global manufacturing footprint give it negotiating leverage with suppliers, and use of firm commitments, vendor-managed inventory and strategic capacity partnerships helps secure inputs; however, in tight categories such as sterile injectables and specialized syringes suppliers retain pricing power.

- Volume leverage: global sourcing

- Operational tools: VMI, forecasts, commitments

- Risk: sterile injectables/syringes seller power

- Mitigation: geographic diversification

CDMO concentration and cGMP constraints raise supplier leverage despite $43.1B sales

Lilly faces elevated supplier power due to concentrated vendors for APIs, biologics media and sterile components, raising switching costs and launch risk; 2024 revenue $43.1B and R&D >$8B drive partnership but not eliminate bottlenecks. Biologics CDMO concentration (~55% capacity top players, 2023) and cGMP constraints (21 CFR 210/211) increase supplier leverage despite dual‑sourcing and volume discounts.

| Metric | Value |

|---|---|

| 2024 revenue | $43.1B |

| 2024 R&D | >$8B |

| CDMO biologics share (2023) | ~55% |

What is included in the product

Tailored exclusively for Eli Lilly, this Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and highlights regulatory and R&D-driven barriers shaping the company’s pricing, profitability, and strategic positioning.

A concise, one-sheet Porter’s Five Forces for Eli Lilly—instantly clarifies supplier/buyer power, competitive rivalry, substitutes and entry barriers to remove analysis complexity and provide slide-ready insights for faster strategic decisions.

Customers Bargaining Power

PBMs and payers negotiate hard

U.S. PBMs and managed care plans wield strong leverage—CVS Caremark, Express Scripts and OptumRx together cover roughly 80% of prescription lives—and drive rebate and formulary pressure, often extracting rebates in the 20–30% range for branded medicines. They steer utilization via tiering and prior authorization, forcing access-for-rebate tradeoffs on high-demand drugs, while outcomes-based contracts are increasingly used to align reimbursement with real-world value.

Government purchasers globally

As of 2024 government purchasers in single-payer systems and HTA bodies (eg NICE, IQWiG, CADTH) wield strong price-setting power, with NICE using a ~20,000–30,000 pound/QALY threshold. Reference pricing and public tendering in Europe often compress prices by 20–50%, cutting manufacturer margins. Demonstrating cost‑effectiveness is pivotal for market access, driving localization and differential pricing strategies by Eli Lilly.

Provider systems and hospitals

Large IDNs and GPOs (eg Vizient, Premier, HealthTrust) aggregate purchasing for thousands of facilities across roughly 6,000 US hospitals, driving protocol- and formulary-led restrictions on brand choice; contracting and discounts are routinely required to secure share, while Eli Lilly relies on clinical differentiation and real-world evidence to support hospital/inpatient positioning and formulary inclusion.

Patient cost sensitivity

Patient out-of-pocket exposure strongly affects adherence and brand loyalty; cost-driven nonadherence is common, and policy changes like the Medicare insulin cap at 35 USD/month (effective 2023) alter demand dynamics for diabetes treatments.

Co-pay assistance and patient support programs from Eli Lilly reduce churn by lowering effective prices for patients, especially for high-cost biologics.

For chronic conditions switching occurs if lower-cost alternatives exist, but strong efficacy and tolerability—hallmarks of several Lilly products—reduce price elasticity.

- Out-of-pocket exposure -> adherence risk

- Co-pay aid -> lower churn

- Chronic care -> switching if alternatives

- High efficacy/tolerability -> lower elasticity

Switching costs vary by therapy

Biologics and complex regimens impose higher switching and monitoring costs, raising customer lock-in for Eli Lilly across injectable therapies. GLP-1s have alternatives but titration and heterogeneous patient response—with Mounjaro and peers driving multi‑billion dollar 2024 demand—increase stickiness. In oncology, biomarker fit (companion diagnostics) constrains interchangeability. Patent exclusivity (patents typically 20 years) temporarily weakens buyer power.

- Higher monitoring costs for biologics

- GLP‑1 titration fosters retention

- Biomarkers limit oncology switches

- Patent terms create temporary price power

PBMs steer ~80% lives with 20–30% rebates; HTA caps and GLP‑1s reshape pricing

PBMs/managed care dominate (~80% prescription lives), driving 20–30% branded rebates and formulary steering; outcomes contracts rising. HTA/government payers exert price caps (NICE ~20,000–30,000 £/QALY), cutting EU prices 20–50%. Patient OOP and Medicare insulin cap $35/mo (2023) affect adherence; biologics/GLP‑1s (multi‑$bn 2024) raise switching costs.

| Buyer | Influence | 2024 stat |

|---|---|---|

| PBMs | Rebates/formularies | ~80% lives, 20–30% rebates |

Preview the Actual Deliverable

Eli Lilly Porter's Five Forces Analysis

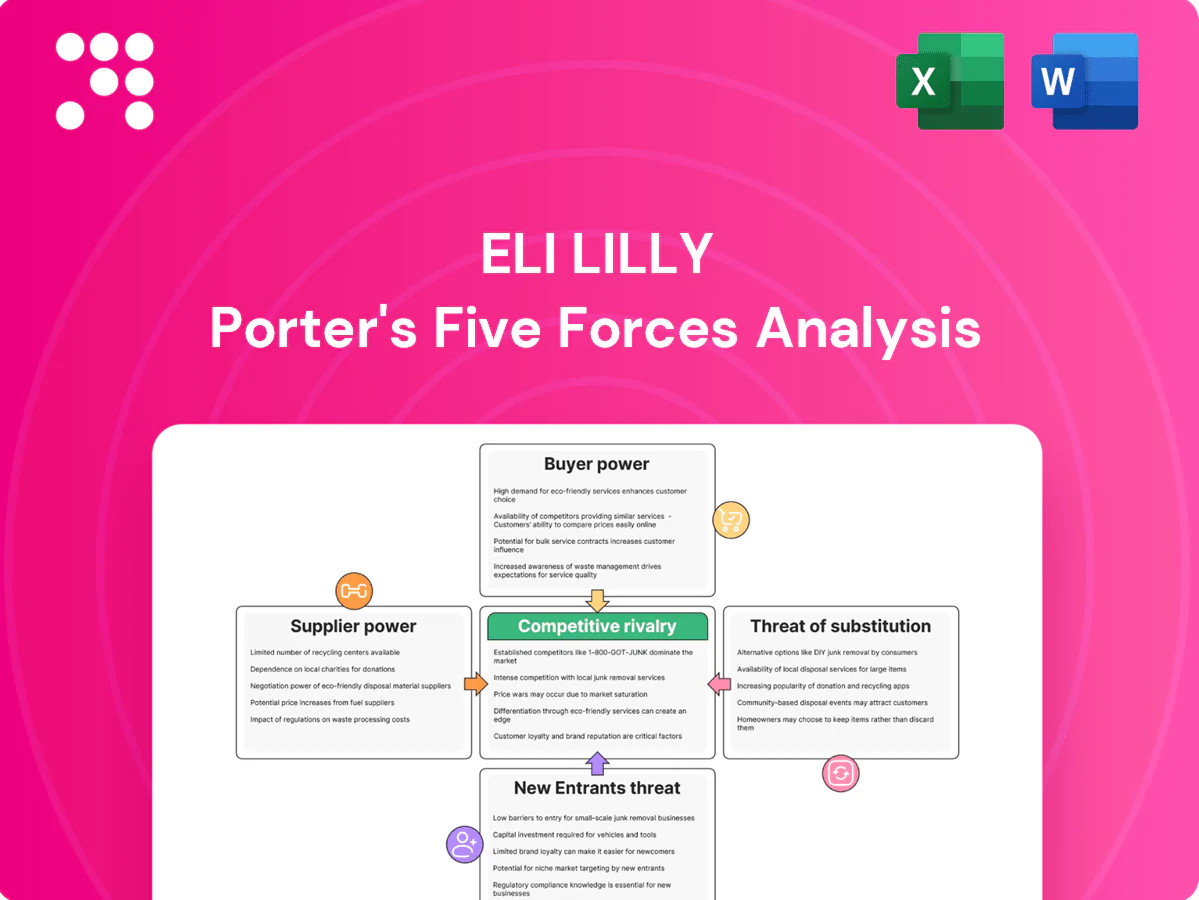

This Porter’s Five Forces analysis of Eli Lilly assesses industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes, drawing clear strategic implications for competitiveness and long‑term profitability. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. Immediate download follows purchase for investment, strategic planning, or academic use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Eli Lilly faces intense competitive rivalry driven by blockbuster drugs, patent cliffs and aggressive R&D rivals, while buyer and supplier power, regulatory scrutiny, and substitute therapies shape its margins and strategic choices. Understanding these forces highlights where Lilly can defend pricing or pivot investment. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Eli Lilly’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialized inputs

Lilly depends on a small set of suppliers for critical APIs, biologics media, single‑use systems and rare excipients, which raises switching costs and extends lead times. Supplier concentration increases risk of launch delays or supply constraints; Lilly reported $43.1B revenue in 2024 and said supplier resilience was a strategic priority. Dual‑sourcing and long‑term contracts partially mitigate this supplier power but cannot eliminate single‑source bottlenecks.

Biologics and advanced modalities

Complex biologics, peptides and GLP‑1 manufacturing heighten supplier leverage as specialized equipment, cell lines and cold‑chain logistics are poorly substitutable; top biopharma CDMOs held roughly 55% of global biologics capacity in 2023. Technology transfers for biologics commonly take 12–24 months and cost tens of millions, slowing vendor switches. Approved second sources reduce but do not eliminate dependency due to qualification time and capacity constraints.

Regulatory and quality gatekeeping

cGMP compliance ties Eli Lilly to a limited pool of qualified suppliers that pass FDA audits; as of 2024 cGMP is codified under 21 CFR Parts 210 and 211. Any supplier change triggers regulatory filings and validation, raising supplier stickiness and negotiating leverage. Strong QA oversight lets Lilly push back on price/terms but increases time and cost for sourcing changes.

IP, exclusivity, and custom components

Supplier-held IP for device components, novel excipients and delivery systems raises switching costs and can push prices up; customization narrows vendor options and increases dependency. Co-development deals (used by Lilly to secure biologics and device access) can lock suppliers while sharing margin upside; 2024 R&D investment remained above $8B, increasing bargaining leverage through partnerships.

- Proprietary inputs elevate price power

- Customization reduces supplier pool

- Co-development secures access and aligns value

Scale counterbalances vendor power

Lilly’s sheer volume, improved forecasting and global manufacturing footprint give it negotiating leverage with suppliers, and use of firm commitments, vendor-managed inventory and strategic capacity partnerships helps secure inputs; however, in tight categories such as sterile injectables and specialized syringes suppliers retain pricing power.

- Volume leverage: global sourcing

- Operational tools: VMI, forecasts, commitments

- Risk: sterile injectables/syringes seller power

- Mitigation: geographic diversification

CDMO concentration and cGMP constraints raise supplier leverage despite $43.1B sales

Lilly faces elevated supplier power due to concentrated vendors for APIs, biologics media and sterile components, raising switching costs and launch risk; 2024 revenue $43.1B and R&D >$8B drive partnership but not eliminate bottlenecks. Biologics CDMO concentration (~55% capacity top players, 2023) and cGMP constraints (21 CFR 210/211) increase supplier leverage despite dual‑sourcing and volume discounts.

| Metric | Value |

|---|---|

| 2024 revenue | $43.1B |

| 2024 R&D | >$8B |

| CDMO biologics share (2023) | ~55% |

What is included in the product

Tailored exclusively for Eli Lilly, this Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and highlights regulatory and R&D-driven barriers shaping the company’s pricing, profitability, and strategic positioning.

A concise, one-sheet Porter’s Five Forces for Eli Lilly—instantly clarifies supplier/buyer power, competitive rivalry, substitutes and entry barriers to remove analysis complexity and provide slide-ready insights for faster strategic decisions.

Customers Bargaining Power

PBMs and payers negotiate hard

U.S. PBMs and managed care plans wield strong leverage—CVS Caremark, Express Scripts and OptumRx together cover roughly 80% of prescription lives—and drive rebate and formulary pressure, often extracting rebates in the 20–30% range for branded medicines. They steer utilization via tiering and prior authorization, forcing access-for-rebate tradeoffs on high-demand drugs, while outcomes-based contracts are increasingly used to align reimbursement with real-world value.

Government purchasers globally

As of 2024 government purchasers in single-payer systems and HTA bodies (eg NICE, IQWiG, CADTH) wield strong price-setting power, with NICE using a ~20,000–30,000 pound/QALY threshold. Reference pricing and public tendering in Europe often compress prices by 20–50%, cutting manufacturer margins. Demonstrating cost‑effectiveness is pivotal for market access, driving localization and differential pricing strategies by Eli Lilly.

Provider systems and hospitals

Large IDNs and GPOs (eg Vizient, Premier, HealthTrust) aggregate purchasing for thousands of facilities across roughly 6,000 US hospitals, driving protocol- and formulary-led restrictions on brand choice; contracting and discounts are routinely required to secure share, while Eli Lilly relies on clinical differentiation and real-world evidence to support hospital/inpatient positioning and formulary inclusion.

Patient cost sensitivity

Patient out-of-pocket exposure strongly affects adherence and brand loyalty; cost-driven nonadherence is common, and policy changes like the Medicare insulin cap at 35 USD/month (effective 2023) alter demand dynamics for diabetes treatments.

Co-pay assistance and patient support programs from Eli Lilly reduce churn by lowering effective prices for patients, especially for high-cost biologics.

For chronic conditions switching occurs if lower-cost alternatives exist, but strong efficacy and tolerability—hallmarks of several Lilly products—reduce price elasticity.

- Out-of-pocket exposure -> adherence risk

- Co-pay aid -> lower churn

- Chronic care -> switching if alternatives

- High efficacy/tolerability -> lower elasticity

Switching costs vary by therapy

Biologics and complex regimens impose higher switching and monitoring costs, raising customer lock-in for Eli Lilly across injectable therapies. GLP-1s have alternatives but titration and heterogeneous patient response—with Mounjaro and peers driving multi‑billion dollar 2024 demand—increase stickiness. In oncology, biomarker fit (companion diagnostics) constrains interchangeability. Patent exclusivity (patents typically 20 years) temporarily weakens buyer power.

- Higher monitoring costs for biologics

- GLP‑1 titration fosters retention

- Biomarkers limit oncology switches

- Patent terms create temporary price power

PBMs steer ~80% lives with 20–30% rebates; HTA caps and GLP‑1s reshape pricing

PBMs/managed care dominate (~80% prescription lives), driving 20–30% branded rebates and formulary steering; outcomes contracts rising. HTA/government payers exert price caps (NICE ~20,000–30,000 £/QALY), cutting EU prices 20–50%. Patient OOP and Medicare insulin cap $35/mo (2023) affect adherence; biologics/GLP‑1s (multi‑$bn 2024) raise switching costs.

| Buyer | Influence | 2024 stat |

|---|---|---|

| PBMs | Rebates/formularies | ~80% lives, 20–30% rebates |

Preview the Actual Deliverable

Eli Lilly Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Eli Lilly assesses industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes, drawing clear strategic implications for competitiveness and long‑term profitability. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. Immediate download follows purchase for investment, strategic planning, or academic use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Eli Lilly faces intense competitive rivalry driven by blockbuster drugs, patent cliffs and aggressive R&D rivals, while buyer and supplier power, regulatory scrutiny, and substitute therapies shape its margins and strategic choices. Understanding these forces highlights where Lilly can defend pricing or pivot investment. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Eli Lilly’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated specialized inputs

Lilly depends on a small set of suppliers for critical APIs, biologics media, single‑use systems and rare excipients, which raises switching costs and extends lead times. Supplier concentration increases risk of launch delays or supply constraints; Lilly reported $43.1B revenue in 2024 and said supplier resilience was a strategic priority. Dual‑sourcing and long‑term contracts partially mitigate this supplier power but cannot eliminate single‑source bottlenecks.

Biologics and advanced modalities

Complex biologics, peptides and GLP‑1 manufacturing heighten supplier leverage as specialized equipment, cell lines and cold‑chain logistics are poorly substitutable; top biopharma CDMOs held roughly 55% of global biologics capacity in 2023. Technology transfers for biologics commonly take 12–24 months and cost tens of millions, slowing vendor switches. Approved second sources reduce but do not eliminate dependency due to qualification time and capacity constraints.

Regulatory and quality gatekeeping

cGMP compliance ties Eli Lilly to a limited pool of qualified suppliers that pass FDA audits; as of 2024 cGMP is codified under 21 CFR Parts 210 and 211. Any supplier change triggers regulatory filings and validation, raising supplier stickiness and negotiating leverage. Strong QA oversight lets Lilly push back on price/terms but increases time and cost for sourcing changes.

IP, exclusivity, and custom components

Supplier-held IP for device components, novel excipients and delivery systems raises switching costs and can push prices up; customization narrows vendor options and increases dependency. Co-development deals (used by Lilly to secure biologics and device access) can lock suppliers while sharing margin upside; 2024 R&D investment remained above $8B, increasing bargaining leverage through partnerships.

- Proprietary inputs elevate price power

- Customization reduces supplier pool

- Co-development secures access and aligns value

Scale counterbalances vendor power

Lilly’s sheer volume, improved forecasting and global manufacturing footprint give it negotiating leverage with suppliers, and use of firm commitments, vendor-managed inventory and strategic capacity partnerships helps secure inputs; however, in tight categories such as sterile injectables and specialized syringes suppliers retain pricing power.

- Volume leverage: global sourcing

- Operational tools: VMI, forecasts, commitments

- Risk: sterile injectables/syringes seller power

- Mitigation: geographic diversification

CDMO concentration and cGMP constraints raise supplier leverage despite $43.1B sales

Lilly faces elevated supplier power due to concentrated vendors for APIs, biologics media and sterile components, raising switching costs and launch risk; 2024 revenue $43.1B and R&D >$8B drive partnership but not eliminate bottlenecks. Biologics CDMO concentration (~55% capacity top players, 2023) and cGMP constraints (21 CFR 210/211) increase supplier leverage despite dual‑sourcing and volume discounts.

| Metric | Value |

|---|---|

| 2024 revenue | $43.1B |

| 2024 R&D | >$8B |

| CDMO biologics share (2023) | ~55% |

What is included in the product

Tailored exclusively for Eli Lilly, this Porter's Five Forces analysis assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and highlights regulatory and R&D-driven barriers shaping the company’s pricing, profitability, and strategic positioning.

A concise, one-sheet Porter’s Five Forces for Eli Lilly—instantly clarifies supplier/buyer power, competitive rivalry, substitutes and entry barriers to remove analysis complexity and provide slide-ready insights for faster strategic decisions.

Customers Bargaining Power

PBMs and payers negotiate hard

U.S. PBMs and managed care plans wield strong leverage—CVS Caremark, Express Scripts and OptumRx together cover roughly 80% of prescription lives—and drive rebate and formulary pressure, often extracting rebates in the 20–30% range for branded medicines. They steer utilization via tiering and prior authorization, forcing access-for-rebate tradeoffs on high-demand drugs, while outcomes-based contracts are increasingly used to align reimbursement with real-world value.

Government purchasers globally

As of 2024 government purchasers in single-payer systems and HTA bodies (eg NICE, IQWiG, CADTH) wield strong price-setting power, with NICE using a ~20,000–30,000 pound/QALY threshold. Reference pricing and public tendering in Europe often compress prices by 20–50%, cutting manufacturer margins. Demonstrating cost‑effectiveness is pivotal for market access, driving localization and differential pricing strategies by Eli Lilly.

Provider systems and hospitals

Large IDNs and GPOs (eg Vizient, Premier, HealthTrust) aggregate purchasing for thousands of facilities across roughly 6,000 US hospitals, driving protocol- and formulary-led restrictions on brand choice; contracting and discounts are routinely required to secure share, while Eli Lilly relies on clinical differentiation and real-world evidence to support hospital/inpatient positioning and formulary inclusion.

Patient cost sensitivity

Patient out-of-pocket exposure strongly affects adherence and brand loyalty; cost-driven nonadherence is common, and policy changes like the Medicare insulin cap at 35 USD/month (effective 2023) alter demand dynamics for diabetes treatments.

Co-pay assistance and patient support programs from Eli Lilly reduce churn by lowering effective prices for patients, especially for high-cost biologics.

For chronic conditions switching occurs if lower-cost alternatives exist, but strong efficacy and tolerability—hallmarks of several Lilly products—reduce price elasticity.

- Out-of-pocket exposure -> adherence risk

- Co-pay aid -> lower churn

- Chronic care -> switching if alternatives

- High efficacy/tolerability -> lower elasticity

Switching costs vary by therapy

Biologics and complex regimens impose higher switching and monitoring costs, raising customer lock-in for Eli Lilly across injectable therapies. GLP-1s have alternatives but titration and heterogeneous patient response—with Mounjaro and peers driving multi‑billion dollar 2024 demand—increase stickiness. In oncology, biomarker fit (companion diagnostics) constrains interchangeability. Patent exclusivity (patents typically 20 years) temporarily weakens buyer power.

- Higher monitoring costs for biologics

- GLP‑1 titration fosters retention

- Biomarkers limit oncology switches

- Patent terms create temporary price power

PBMs steer ~80% lives with 20–30% rebates; HTA caps and GLP‑1s reshape pricing

PBMs/managed care dominate (~80% prescription lives), driving 20–30% branded rebates and formulary steering; outcomes contracts rising. HTA/government payers exert price caps (NICE ~20,000–30,000 £/QALY), cutting EU prices 20–50%. Patient OOP and Medicare insulin cap $35/mo (2023) affect adherence; biologics/GLP‑1s (multi‑$bn 2024) raise switching costs.

| Buyer | Influence | 2024 stat |

|---|---|---|

| PBMs | Rebates/formularies | ~80% lives, 20–30% rebates |

Preview the Actual Deliverable

Eli Lilly Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Eli Lilly assesses industry rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes, drawing clear strategic implications for competitiveness and long‑term profitability. The document shown is the same professionally written analysis you'll receive—fully formatted and ready to use. Immediate download follows purchase for investment, strategic planning, or academic use.