Lincoln Electric Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

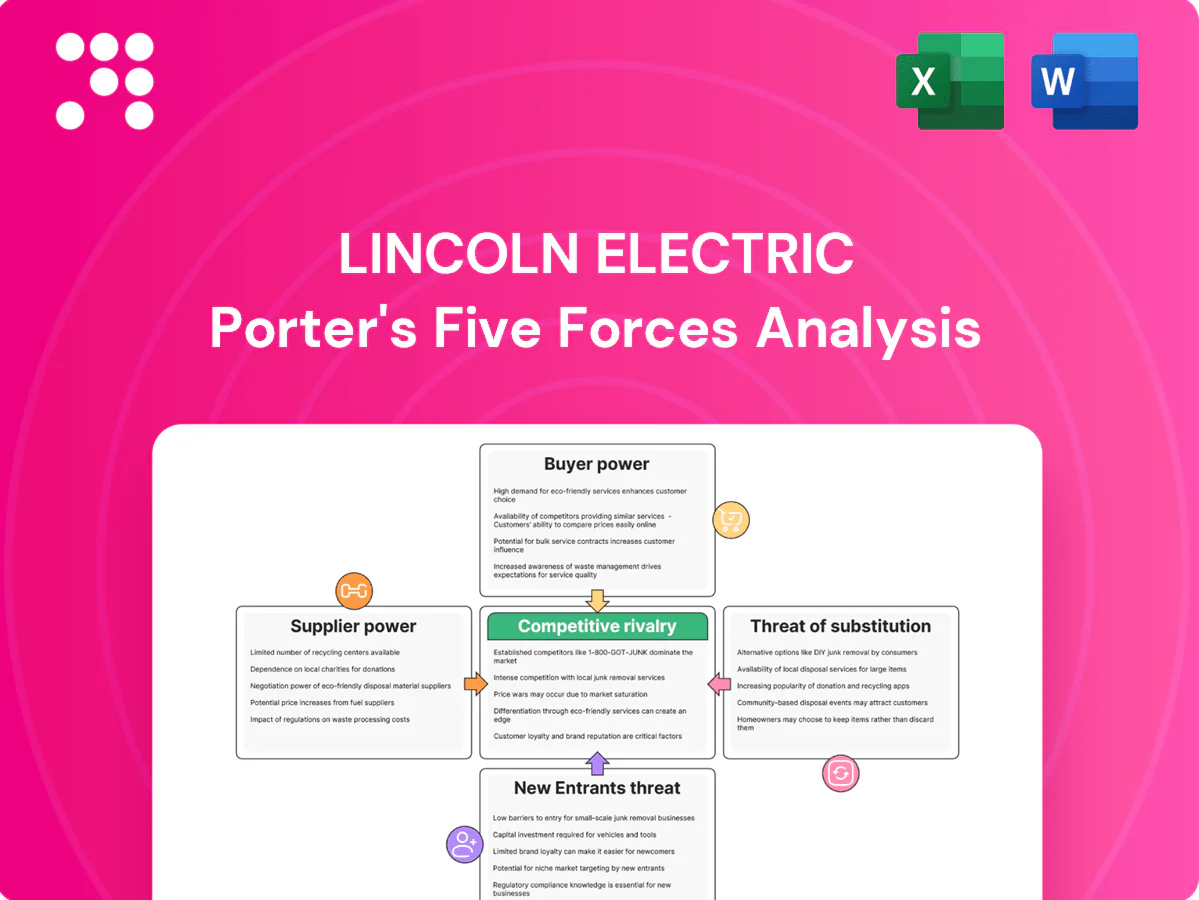

Lincoln Electric faces moderate buyer power, concentrated supplier relationships, and steady rivalry driven by price and innovation; barriers to entry are moderate while substitutes pose sector-specific risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lincoln Electric’s competitive dynamics in detail.

Suppliers Bargaining Power

Raw materials concentration

Raw materials such as steel wire rod, specialty alloys and flux chemicals are sourced from a concentrated set of global producers, and 2024 saw renewed metal and energy price volatility that passed through to consumables costs.

Lincoln’s global scale and long-term supply contracts mitigated many short-term spikes in 2024 but could not fully eliminate input-price volatility.

Logistics bottlenecks and geopolitics in 2024 temporarily increased supplier leverage, raising spot premiums and delivery lead times for certain alloys.

Specialized components

Power electronics, sensors and robotics parts for Lincoln Electric often rely on fewer than 10 qualified suppliers due to precision and certification requirements, concentrating supplier power; qualification and validation typically require 3–6 months of testing and can cause nontrivial downtime costs. Dual-sourcing and in-house engineering have reduced dependency—internal programs claim roughly 30% fewer single-supplier items—but do not eliminate it. In market upcycles lead times can stretch 20–40%, pressuring margins through expedited freight and production delays.

Consumables vs. equipment mix

Consumables demand steady inputs, creating continuous supplier exposure while equipment purchases are episodic and capital-driven. High volumes give Lincoln purchasing leverage on commodity inputs, and proprietary formulations developed by Lincoln (notably expanded in 2024) increase control over specs and vendor choices. Nonetheless, strict compliance and consistency standards constrain rapid supplier substitution.

Vertical integration options

Lincoln Electric’s process know-how enables partial backward integration into wire drawing and flux blending, creating credible insourcing alternatives that constrain supplier bargaining power; Lincoln reported $3.6 billion in net sales in fiscal 2024, supporting investment capacity for selective insourcing.

- Partial integration: wire drawing, flux blending

- Limits supplier leverage: credible threat to insource

- Full integration impractical: mining/semiconductor fabs

- Overall: moderate supplier power

ESG and compliance pressures

Rising ESG, safety, and traceability requirements in 2024 have narrowed approved supplier pools, letting compliant vendors command price premiums and stricter contract terms; Lincoln Electric, with reported 2024 net sales of about $4.3 billion, must manage region-specific sourcing across Americas, EMEA and APAC, increasing logistical and compliance complexity.

- Compliant suppliers enforce premiums and terms

- Region-specific sourcing raises operational complexity

- Supplier audits stabilize quality but raise procurement costs

Moderate supplier power: $4.3B, fewer than 10 suppliers, 3-6mo quals

Supplier power is moderate: commodity inputs give Lincoln scale leverage amid $4.3B 2024 sales, but concentrated electronics/alloy suppliers (<10) and stricter ESG compliance raised premiums. Dual-sourcing and partial insourcing cut single-supplier items ~30%, yet qualification (3–6 months) and lead-time spikes (20–40%) sustain supplier leverage. Overall supplier bargaining power remains constrained but nontrivial.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Qualified suppliers (electronics/alloys) | <10 |

| Qualification time | 3–6 months |

| Lead-time stretch in upcycle | 20–40% |

| Single-supplier reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis of Lincoln Electric that evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlights disruptive forces and strategic barriers protecting incumbency.

A concise Porter's Five Forces one-sheet for Lincoln Electric that clarifies supplier, buyer, entrant, substitute, and rivalry pressures for swift strategic decisions. Editable pressure sliders and clean visuals make it easy to model scenarios and drop into decks or boardroom slides.

Customers Bargaining Power

Diverse industry base

Customers span fabrication, construction, energy, automotive and general industrial, diluting any single buyer’s leverage; Lincoln reported FY2024 net sales of $4.3 billion, reflecting wide market reach. Cyclical end-markets still create synchronized demand swings, with industrial production volatility rippling across segments. Lincoln’s broad portfolio and cross-selling reduced customer churn, supporting recurring order flows.

Large enterprise buyers

Global OEMs and EPCs press Lincoln on price, service levels and total cost of ownership; 2024 procurement surveys show buyers targeting 10–15% TCO reductions and routinely staging competitive bids among top brands. Multi-year framework agreements in 2024 cut unit prices roughly 5–20% while locking in volume. Lincoln counters with performance guarantees, uptime SLAs and integrated weld-to-automation solutions.

Consumables lock-in

Welding wire, electrodes and flux consumables are tightly matched to Lincoln Electric equipment settings and quality specs, so qualification tests, operator retraining and warranty alignment create meaningful switching costs. This embeddedness reduces pure price bargaining by customers and is reinforced by technical support and uptime service commitments. Field service SLAs and application engineering deepen supplier lock-in.

Performance-critical applications

In energy, heavy fabrication and automotive, failure costs far exceed weld consumable prices, so buyers prioritize reliability, certifications and metallurgy over lowest bid, reducing bargaining power for premium-grade consumables and robotic cells. Value-added services—training, process optimization and onsite support—increase switching costs and customer stickiness, strengthening Lincoln Electric’s position in performance-critical segments.

- Reliability over price

- Certifications drive purchasing

- Premium grades lower buyer leverage

- Services reinforce retention

Aftermarket and service

Installed base drives recurring revenue in spares, software, and maintenance, typically accounting for 20–40% of OEM aftermarket revenue in industrial equipment (2024 industry estimates). Buyers gain leverage when alternatives are compatible and readily available, but Lincoln Electrics proprietary torch interfaces and warranty terms temper that leverage. Subscription software and analytics (growing adoption in 2024) deepen lifetime engagement and recurring margins.

- Installed base: 20–40% of aftermarket revenue (2024)

- Leverage rises with compatibility and third-party parts

- Proprietary interfaces/warranties reduce switching

- Subscriptions/analytics increase lifetime value

Moderate buyer leverage with $4.3B sales; procurement seeks 10–15% TCO cuts

Customer bargaining power is moderate: Lincoln’s $4.3B FY2024 sales span diverse end-markets, limiting single-buyer leverage, while procurement targets (2024) seek 10–15% TCO cuts. High switching costs from qualified consumables, proprietary interfaces and service SLAs protect pricing; installed base drives 20–40% aftermarket revenue, strengthening recurring margins.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Buyer TCO target | 10–15% |

| Aftermarket share | 20–40% |

Full Version Awaits

Lincoln Electric Porter's Five Forces Analysis

This preview shows the exact Lincoln Electric Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professional, and complete. No placeholders or mockups are included. Upon payment you'll get instant access to this identical file, ready for download and use.

A Must-Have Tool for Decision-Makers

Lincoln Electric faces moderate buyer power, concentrated supplier relationships, and steady rivalry driven by price and innovation; barriers to entry are moderate while substitutes pose sector-specific risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lincoln Electric’s competitive dynamics in detail.

Suppliers Bargaining Power

Raw materials concentration

Raw materials such as steel wire rod, specialty alloys and flux chemicals are sourced from a concentrated set of global producers, and 2024 saw renewed metal and energy price volatility that passed through to consumables costs.

Lincoln’s global scale and long-term supply contracts mitigated many short-term spikes in 2024 but could not fully eliminate input-price volatility.

Logistics bottlenecks and geopolitics in 2024 temporarily increased supplier leverage, raising spot premiums and delivery lead times for certain alloys.

Specialized components

Power electronics, sensors and robotics parts for Lincoln Electric often rely on fewer than 10 qualified suppliers due to precision and certification requirements, concentrating supplier power; qualification and validation typically require 3–6 months of testing and can cause nontrivial downtime costs. Dual-sourcing and in-house engineering have reduced dependency—internal programs claim roughly 30% fewer single-supplier items—but do not eliminate it. In market upcycles lead times can stretch 20–40%, pressuring margins through expedited freight and production delays.

Consumables vs. equipment mix

Consumables demand steady inputs, creating continuous supplier exposure while equipment purchases are episodic and capital-driven. High volumes give Lincoln purchasing leverage on commodity inputs, and proprietary formulations developed by Lincoln (notably expanded in 2024) increase control over specs and vendor choices. Nonetheless, strict compliance and consistency standards constrain rapid supplier substitution.

Vertical integration options

Lincoln Electric’s process know-how enables partial backward integration into wire drawing and flux blending, creating credible insourcing alternatives that constrain supplier bargaining power; Lincoln reported $3.6 billion in net sales in fiscal 2024, supporting investment capacity for selective insourcing.

- Partial integration: wire drawing, flux blending

- Limits supplier leverage: credible threat to insource

- Full integration impractical: mining/semiconductor fabs

- Overall: moderate supplier power

ESG and compliance pressures

Rising ESG, safety, and traceability requirements in 2024 have narrowed approved supplier pools, letting compliant vendors command price premiums and stricter contract terms; Lincoln Electric, with reported 2024 net sales of about $4.3 billion, must manage region-specific sourcing across Americas, EMEA and APAC, increasing logistical and compliance complexity.

- Compliant suppliers enforce premiums and terms

- Region-specific sourcing raises operational complexity

- Supplier audits stabilize quality but raise procurement costs

Moderate supplier power: $4.3B, fewer than 10 suppliers, 3-6mo quals

Supplier power is moderate: commodity inputs give Lincoln scale leverage amid $4.3B 2024 sales, but concentrated electronics/alloy suppliers (<10) and stricter ESG compliance raised premiums. Dual-sourcing and partial insourcing cut single-supplier items ~30%, yet qualification (3–6 months) and lead-time spikes (20–40%) sustain supplier leverage. Overall supplier bargaining power remains constrained but nontrivial.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Qualified suppliers (electronics/alloys) | <10 |

| Qualification time | 3–6 months |

| Lead-time stretch in upcycle | 20–40% |

| Single-supplier reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis of Lincoln Electric that evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlights disruptive forces and strategic barriers protecting incumbency.

A concise Porter's Five Forces one-sheet for Lincoln Electric that clarifies supplier, buyer, entrant, substitute, and rivalry pressures for swift strategic decisions. Editable pressure sliders and clean visuals make it easy to model scenarios and drop into decks or boardroom slides.

Customers Bargaining Power

Diverse industry base

Customers span fabrication, construction, energy, automotive and general industrial, diluting any single buyer’s leverage; Lincoln reported FY2024 net sales of $4.3 billion, reflecting wide market reach. Cyclical end-markets still create synchronized demand swings, with industrial production volatility rippling across segments. Lincoln’s broad portfolio and cross-selling reduced customer churn, supporting recurring order flows.

Large enterprise buyers

Global OEMs and EPCs press Lincoln on price, service levels and total cost of ownership; 2024 procurement surveys show buyers targeting 10–15% TCO reductions and routinely staging competitive bids among top brands. Multi-year framework agreements in 2024 cut unit prices roughly 5–20% while locking in volume. Lincoln counters with performance guarantees, uptime SLAs and integrated weld-to-automation solutions.

Consumables lock-in

Welding wire, electrodes and flux consumables are tightly matched to Lincoln Electric equipment settings and quality specs, so qualification tests, operator retraining and warranty alignment create meaningful switching costs. This embeddedness reduces pure price bargaining by customers and is reinforced by technical support and uptime service commitments. Field service SLAs and application engineering deepen supplier lock-in.

Performance-critical applications

In energy, heavy fabrication and automotive, failure costs far exceed weld consumable prices, so buyers prioritize reliability, certifications and metallurgy over lowest bid, reducing bargaining power for premium-grade consumables and robotic cells. Value-added services—training, process optimization and onsite support—increase switching costs and customer stickiness, strengthening Lincoln Electric’s position in performance-critical segments.

- Reliability over price

- Certifications drive purchasing

- Premium grades lower buyer leverage

- Services reinforce retention

Aftermarket and service

Installed base drives recurring revenue in spares, software, and maintenance, typically accounting for 20–40% of OEM aftermarket revenue in industrial equipment (2024 industry estimates). Buyers gain leverage when alternatives are compatible and readily available, but Lincoln Electrics proprietary torch interfaces and warranty terms temper that leverage. Subscription software and analytics (growing adoption in 2024) deepen lifetime engagement and recurring margins.

- Installed base: 20–40% of aftermarket revenue (2024)

- Leverage rises with compatibility and third-party parts

- Proprietary interfaces/warranties reduce switching

- Subscriptions/analytics increase lifetime value

Moderate buyer leverage with $4.3B sales; procurement seeks 10–15% TCO cuts

Customer bargaining power is moderate: Lincoln’s $4.3B FY2024 sales span diverse end-markets, limiting single-buyer leverage, while procurement targets (2024) seek 10–15% TCO cuts. High switching costs from qualified consumables, proprietary interfaces and service SLAs protect pricing; installed base drives 20–40% aftermarket revenue, strengthening recurring margins.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Buyer TCO target | 10–15% |

| Aftermarket share | 20–40% |

Full Version Awaits

Lincoln Electric Porter's Five Forces Analysis

This preview shows the exact Lincoln Electric Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professional, and complete. No placeholders or mockups are included. Upon payment you'll get instant access to this identical file, ready for download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lincoln Electric faces moderate buyer power, concentrated supplier relationships, and steady rivalry driven by price and innovation; barriers to entry are moderate while substitutes pose sector-specific risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lincoln Electric’s competitive dynamics in detail.

Suppliers Bargaining Power

Raw materials concentration

Raw materials such as steel wire rod, specialty alloys and flux chemicals are sourced from a concentrated set of global producers, and 2024 saw renewed metal and energy price volatility that passed through to consumables costs.

Lincoln’s global scale and long-term supply contracts mitigated many short-term spikes in 2024 but could not fully eliminate input-price volatility.

Logistics bottlenecks and geopolitics in 2024 temporarily increased supplier leverage, raising spot premiums and delivery lead times for certain alloys.

Specialized components

Power electronics, sensors and robotics parts for Lincoln Electric often rely on fewer than 10 qualified suppliers due to precision and certification requirements, concentrating supplier power; qualification and validation typically require 3–6 months of testing and can cause nontrivial downtime costs. Dual-sourcing and in-house engineering have reduced dependency—internal programs claim roughly 30% fewer single-supplier items—but do not eliminate it. In market upcycles lead times can stretch 20–40%, pressuring margins through expedited freight and production delays.

Consumables vs. equipment mix

Consumables demand steady inputs, creating continuous supplier exposure while equipment purchases are episodic and capital-driven. High volumes give Lincoln purchasing leverage on commodity inputs, and proprietary formulations developed by Lincoln (notably expanded in 2024) increase control over specs and vendor choices. Nonetheless, strict compliance and consistency standards constrain rapid supplier substitution.

Vertical integration options

Lincoln Electric’s process know-how enables partial backward integration into wire drawing and flux blending, creating credible insourcing alternatives that constrain supplier bargaining power; Lincoln reported $3.6 billion in net sales in fiscal 2024, supporting investment capacity for selective insourcing.

- Partial integration: wire drawing, flux blending

- Limits supplier leverage: credible threat to insource

- Full integration impractical: mining/semiconductor fabs

- Overall: moderate supplier power

ESG and compliance pressures

Rising ESG, safety, and traceability requirements in 2024 have narrowed approved supplier pools, letting compliant vendors command price premiums and stricter contract terms; Lincoln Electric, with reported 2024 net sales of about $4.3 billion, must manage region-specific sourcing across Americas, EMEA and APAC, increasing logistical and compliance complexity.

- Compliant suppliers enforce premiums and terms

- Region-specific sourcing raises operational complexity

- Supplier audits stabilize quality but raise procurement costs

Moderate supplier power: $4.3B, fewer than 10 suppliers, 3-6mo quals

Supplier power is moderate: commodity inputs give Lincoln scale leverage amid $4.3B 2024 sales, but concentrated electronics/alloy suppliers (<10) and stricter ESG compliance raised premiums. Dual-sourcing and partial insourcing cut single-supplier items ~30%, yet qualification (3–6 months) and lead-time spikes (20–40%) sustain supplier leverage. Overall supplier bargaining power remains constrained but nontrivial.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Qualified suppliers (electronics/alloys) | <10 |

| Qualification time | 3–6 months |

| Lead-time stretch in upcycle | 20–40% |

| Single-supplier reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis of Lincoln Electric that evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlights disruptive forces and strategic barriers protecting incumbency.

A concise Porter's Five Forces one-sheet for Lincoln Electric that clarifies supplier, buyer, entrant, substitute, and rivalry pressures for swift strategic decisions. Editable pressure sliders and clean visuals make it easy to model scenarios and drop into decks or boardroom slides.

Customers Bargaining Power

Diverse industry base

Customers span fabrication, construction, energy, automotive and general industrial, diluting any single buyer’s leverage; Lincoln reported FY2024 net sales of $4.3 billion, reflecting wide market reach. Cyclical end-markets still create synchronized demand swings, with industrial production volatility rippling across segments. Lincoln’s broad portfolio and cross-selling reduced customer churn, supporting recurring order flows.

Large enterprise buyers

Global OEMs and EPCs press Lincoln on price, service levels and total cost of ownership; 2024 procurement surveys show buyers targeting 10–15% TCO reductions and routinely staging competitive bids among top brands. Multi-year framework agreements in 2024 cut unit prices roughly 5–20% while locking in volume. Lincoln counters with performance guarantees, uptime SLAs and integrated weld-to-automation solutions.

Consumables lock-in

Welding wire, electrodes and flux consumables are tightly matched to Lincoln Electric equipment settings and quality specs, so qualification tests, operator retraining and warranty alignment create meaningful switching costs. This embeddedness reduces pure price bargaining by customers and is reinforced by technical support and uptime service commitments. Field service SLAs and application engineering deepen supplier lock-in.

Performance-critical applications

In energy, heavy fabrication and automotive, failure costs far exceed weld consumable prices, so buyers prioritize reliability, certifications and metallurgy over lowest bid, reducing bargaining power for premium-grade consumables and robotic cells. Value-added services—training, process optimization and onsite support—increase switching costs and customer stickiness, strengthening Lincoln Electric’s position in performance-critical segments.

- Reliability over price

- Certifications drive purchasing

- Premium grades lower buyer leverage

- Services reinforce retention

Aftermarket and service

Installed base drives recurring revenue in spares, software, and maintenance, typically accounting for 20–40% of OEM aftermarket revenue in industrial equipment (2024 industry estimates). Buyers gain leverage when alternatives are compatible and readily available, but Lincoln Electrics proprietary torch interfaces and warranty terms temper that leverage. Subscription software and analytics (growing adoption in 2024) deepen lifetime engagement and recurring margins.

- Installed base: 20–40% of aftermarket revenue (2024)

- Leverage rises with compatibility and third-party parts

- Proprietary interfaces/warranties reduce switching

- Subscriptions/analytics increase lifetime value

Moderate buyer leverage with $4.3B sales; procurement seeks 10–15% TCO cuts

Customer bargaining power is moderate: Lincoln’s $4.3B FY2024 sales span diverse end-markets, limiting single-buyer leverage, while procurement targets (2024) seek 10–15% TCO cuts. High switching costs from qualified consumables, proprietary interfaces and service SLAs protect pricing; installed base drives 20–40% aftermarket revenue, strengthening recurring margins.

| Metric | 2024 Value |

|---|---|

| Net sales | $4.3B |

| Buyer TCO target | 10–15% |

| Aftermarket share | 20–40% |

Full Version Awaits

Lincoln Electric Porter's Five Forces Analysis

This preview shows the exact Lincoln Electric Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professional, and complete. No placeholders or mockups are included. Upon payment you'll get instant access to this identical file, ready for download and use.