Lindab Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

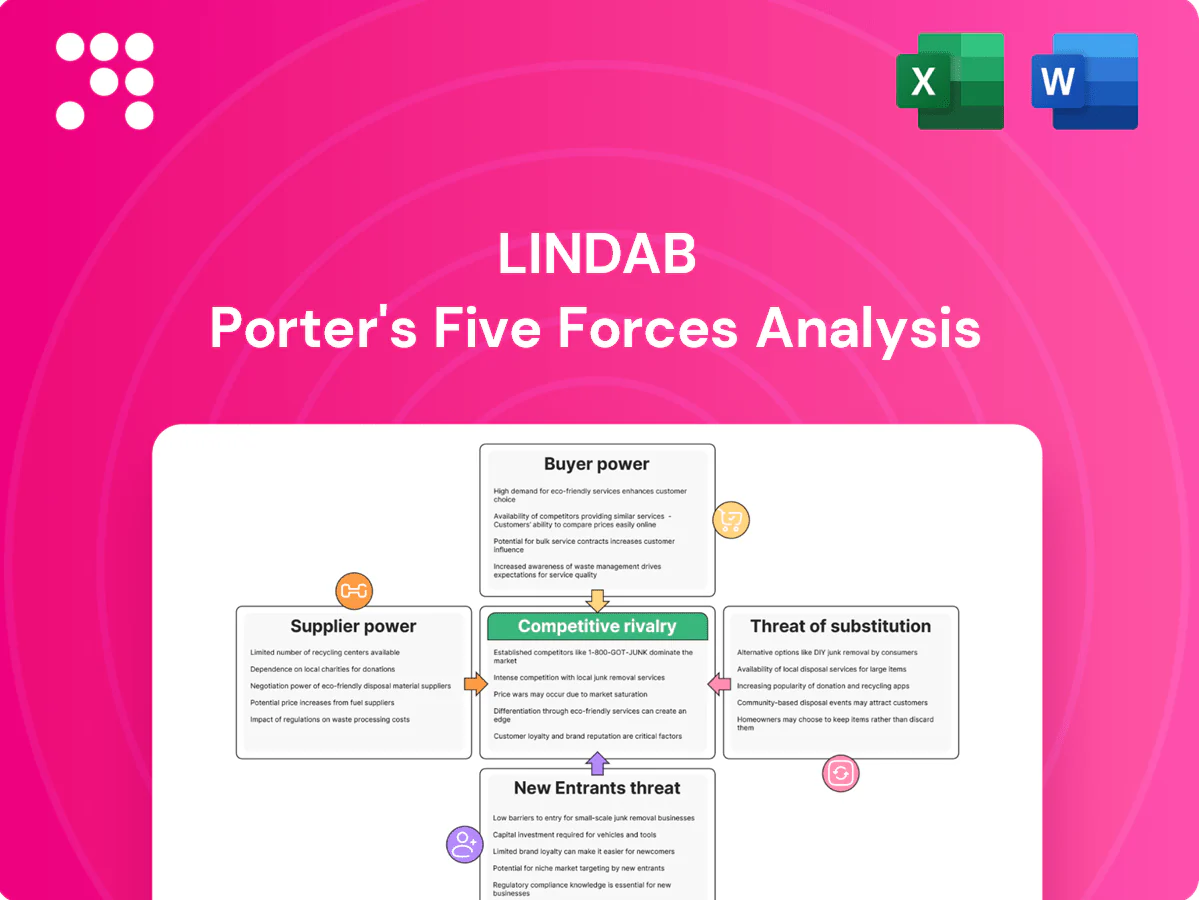

Lindab’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, and competitive rivalry driven by regional HVAC and building-product players; substitutes and regulatory pressures add strategic complexity. This brief shows core dynamics but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and actionable recommendations tailored to Lindab.

Suppliers Bargaining Power

Concentrated steel inputs

Steel sheet and coil are sourced from a concentrated pool of global/regional mills, with global crude steel production at about 1.9 Gt in 2024 (World Steel Association), giving suppliers notable pricing leverage. Price volatility in coils—often swinging hundreds of dollars/ton—can compress Lindab margins if not hedged or indexed. Long-term agreements and volume commitments partially mitigate spikes, while limited green-steel availability and premiums further tighten effective options.

Specialized HVAC components

Specialized motors, fans, filters, controls and corrosion-resistant coatings for HVAC have differentiated specs and certification demands (CE, Eurovent), limiting substitution and increasing supplier power; the global HVAC components market was about USD 230 billion in 2024, concentrating pricing leverage. Dual-sourcing and modular designs can cut dependency and cost risk, while lead-time management (often 6–12 weeks for specialty items) is critical to avoid project delays.

Logistics and energy costs

Freight, energy and coated/galvanized processing materially affect Lindab input costs; EU industrial electricity averaged about €0.14/kWh in 2024 and EU ETS carbon pricing hovered near €85/ton, both increasing supplier leverage on pricing. Regional disruptions or sudden carbon price moves raise supplier bargaining strength by tightening supply or adding surcharges. Lindab’s nearshoring and multi-plant footprint reduce exposure to single-route shocks. Ability to pass through surcharges depends on contract terms and customer mix.

Quality and compliance constraints

EN and ISO compliance plus project code requirements narrow Lindab’s acceptable supplier pool, while audited quality systems and EPDs further limit alternatives and support supplier pricing power.

Approved vendor lists in major projects can lock in upstream partners, and joint engineering reduces unit costs but raises supplier stickiness and switching costs.

Scale and hedging counterweights

High purchasing volumes and centralized sourcing give Lindab stronger terms with metal mills and suppliers, while hedging, index-linked contracts and inventory buffers reduce input-price volatility; supplier development and VAVE programs have reclaimed margin through cost-out initiatives. In tight market cycles in 2024 mills can reassert pricing power, eroding some scale advantages.

- Scale: centralized sourcing improves negotiation leverage

- Hedging: index-linked pricing and inventory mitigate volatility

- Value capture: supplier development and VAVE claw back margin

- Risk: tight 2024 cycles let mills regain leverage

Steel, HVAC & energy supplier power drives 2024 cost volatility; scale helps, risk remains

Suppliers of steel, specialized HVAC components and energy exert moderate-to-high bargaining power due to concentration, spec/certification barriers and carbon/energy cost pass-throughs. Lindab’s scale, hedging, dual-sourcing and supplier development mitigate but cannot eliminate volatility risk in tight 2024 cycles. Passing on surcharges depends on contract mix and project approvals.

| Item | 2024 Data |

|---|---|

| Global crude steel | 1.9 Gt |

| EU electricity | €0.14/kWh |

| EU ETS | €85/t |

| HVAC components market | USD 230bn |

| Lead times (specialty) | 6–12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Lindab, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to assess pricing influence and strategic positioning.

A clear one-sheet Porter's Five Forces for Lindab—customize pressure levels, swap in your data, and instantly visualize strategic intensity with a spider chart for quick deck-ready decisions.

Customers Bargaining Power

Professional, price-sensitive buyers

Contractors, installers and distributors rigorously compare bids, driving strong price pressure as project-based procurement often awards the lowest compliant offer; this forces Lindab to compete on unit cost and margins.

Standardization eases switching

Many steel ducts and fittings are highly standardized — roughly 65% of common components are cross-compatible in 2024 — so switching suppliers is feasible for most projects. Compatibility with existing systems and BIM libraries (BIM adoption ~65% in Europe 2024) still creates moderate friction. Service levels, delivery reliability and technical support remain key differentiators, while penetration of proprietary components increases lock-in.

Large accounts concentrate power

National distributors and major construction groups consolidate volumes and negotiate aggressively; for building-systems suppliers top customers can account for roughly 20–35% of revenue. Lindab reported net sales of about SEK 6.6 billion in 2023, so payment-term extensions and rebate demands from large accounts can materially squeeze margins. Preferred-supplier status brings scale but forces tighter pricing; losing a key account can lower plant utilization and depress fixed-cost coverage.

Spec-driven but revisable

Consultant specs often name brands, but value engineering during tendering commonly reopens competition and can erode supplier margins; change orders after award typically range 5-10% of project value, posing margin risk. Early design-stage influence by consultants or architects reduces buyer leverage later in procurement. Demonstrated energy performance and certifications (eg, BREEAM/LEED) increase spec stickiness and limit substitutions.

- Specs named by consultants

- Value engineering reopens competition

- Early design influence reduces buyer leverage

- Certifications strengthen stickiness

- Post-award change orders 5-10% risk margins

Aftermarket and lifecycle value

Aftermarket and lifecycle value for Lindab—maintenance, filters and upgrades—drive recurring revenue with lower price sensitivity; service contracts represented about 12% of group sales in 2024 and typically carry 15–20% higher gross margins than product sales. Performance guarantees and digital monitoring raised perceived value and reduced churn, while bundling services helps blunt buyer power, though distributor-controlled channels still negotiate terms.

- Recurring revenue: ~12% of 2024 sales

- Service margin uplift: 15–20%

- Digital monitoring: increases retention

- Bundling: lowers buyer leverage

- Risk: distributor negotiation remains

Tenders compress prices; 65% compatibility and BIM adoption boost service stickiness

Buyers press prices in tenders; lowest compliant bids win. 65% component compatibility; BIM ~65% EU (2024) eases switching; service/certs create stickiness. Top accounts 20–35% rev; Lindab SEK6.6bn (2023). Services ~12% of 2024 sales, +15–20% margin.

| Metric | Value |

|---|---|

| Compatibility | 65% |

| BIM EU | 65% |

| Lindab sales | SEK6.6bn |

| Services 2024 | 12% |

| Service margin | 15–20% |

Full Version Awaits

Lindab Porter's Five Forces Analysis

This preview shows the exact Lindab Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders, no mockups. The document displayed here is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the exact file you’ll get instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Lindab’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, and competitive rivalry driven by regional HVAC and building-product players; substitutes and regulatory pressures add strategic complexity. This brief shows core dynamics but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and actionable recommendations tailored to Lindab.

Suppliers Bargaining Power

Concentrated steel inputs

Steel sheet and coil are sourced from a concentrated pool of global/regional mills, with global crude steel production at about 1.9 Gt in 2024 (World Steel Association), giving suppliers notable pricing leverage. Price volatility in coils—often swinging hundreds of dollars/ton—can compress Lindab margins if not hedged or indexed. Long-term agreements and volume commitments partially mitigate spikes, while limited green-steel availability and premiums further tighten effective options.

Specialized HVAC components

Specialized motors, fans, filters, controls and corrosion-resistant coatings for HVAC have differentiated specs and certification demands (CE, Eurovent), limiting substitution and increasing supplier power; the global HVAC components market was about USD 230 billion in 2024, concentrating pricing leverage. Dual-sourcing and modular designs can cut dependency and cost risk, while lead-time management (often 6–12 weeks for specialty items) is critical to avoid project delays.

Logistics and energy costs

Freight, energy and coated/galvanized processing materially affect Lindab input costs; EU industrial electricity averaged about €0.14/kWh in 2024 and EU ETS carbon pricing hovered near €85/ton, both increasing supplier leverage on pricing. Regional disruptions or sudden carbon price moves raise supplier bargaining strength by tightening supply or adding surcharges. Lindab’s nearshoring and multi-plant footprint reduce exposure to single-route shocks. Ability to pass through surcharges depends on contract terms and customer mix.

Quality and compliance constraints

EN and ISO compliance plus project code requirements narrow Lindab’s acceptable supplier pool, while audited quality systems and EPDs further limit alternatives and support supplier pricing power.

Approved vendor lists in major projects can lock in upstream partners, and joint engineering reduces unit costs but raises supplier stickiness and switching costs.

Scale and hedging counterweights

High purchasing volumes and centralized sourcing give Lindab stronger terms with metal mills and suppliers, while hedging, index-linked contracts and inventory buffers reduce input-price volatility; supplier development and VAVE programs have reclaimed margin through cost-out initiatives. In tight market cycles in 2024 mills can reassert pricing power, eroding some scale advantages.

- Scale: centralized sourcing improves negotiation leverage

- Hedging: index-linked pricing and inventory mitigate volatility

- Value capture: supplier development and VAVE claw back margin

- Risk: tight 2024 cycles let mills regain leverage

Steel, HVAC & energy supplier power drives 2024 cost volatility; scale helps, risk remains

Suppliers of steel, specialized HVAC components and energy exert moderate-to-high bargaining power due to concentration, spec/certification barriers and carbon/energy cost pass-throughs. Lindab’s scale, hedging, dual-sourcing and supplier development mitigate but cannot eliminate volatility risk in tight 2024 cycles. Passing on surcharges depends on contract mix and project approvals.

| Item | 2024 Data |

|---|---|

| Global crude steel | 1.9 Gt |

| EU electricity | €0.14/kWh |

| EU ETS | €85/t |

| HVAC components market | USD 230bn |

| Lead times (specialty) | 6–12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Lindab, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to assess pricing influence and strategic positioning.

A clear one-sheet Porter's Five Forces for Lindab—customize pressure levels, swap in your data, and instantly visualize strategic intensity with a spider chart for quick deck-ready decisions.

Customers Bargaining Power

Professional, price-sensitive buyers

Contractors, installers and distributors rigorously compare bids, driving strong price pressure as project-based procurement often awards the lowest compliant offer; this forces Lindab to compete on unit cost and margins.

Standardization eases switching

Many steel ducts and fittings are highly standardized — roughly 65% of common components are cross-compatible in 2024 — so switching suppliers is feasible for most projects. Compatibility with existing systems and BIM libraries (BIM adoption ~65% in Europe 2024) still creates moderate friction. Service levels, delivery reliability and technical support remain key differentiators, while penetration of proprietary components increases lock-in.

Large accounts concentrate power

National distributors and major construction groups consolidate volumes and negotiate aggressively; for building-systems suppliers top customers can account for roughly 20–35% of revenue. Lindab reported net sales of about SEK 6.6 billion in 2023, so payment-term extensions and rebate demands from large accounts can materially squeeze margins. Preferred-supplier status brings scale but forces tighter pricing; losing a key account can lower plant utilization and depress fixed-cost coverage.

Spec-driven but revisable

Consultant specs often name brands, but value engineering during tendering commonly reopens competition and can erode supplier margins; change orders after award typically range 5-10% of project value, posing margin risk. Early design-stage influence by consultants or architects reduces buyer leverage later in procurement. Demonstrated energy performance and certifications (eg, BREEAM/LEED) increase spec stickiness and limit substitutions.

- Specs named by consultants

- Value engineering reopens competition

- Early design influence reduces buyer leverage

- Certifications strengthen stickiness

- Post-award change orders 5-10% risk margins

Aftermarket and lifecycle value

Aftermarket and lifecycle value for Lindab—maintenance, filters and upgrades—drive recurring revenue with lower price sensitivity; service contracts represented about 12% of group sales in 2024 and typically carry 15–20% higher gross margins than product sales. Performance guarantees and digital monitoring raised perceived value and reduced churn, while bundling services helps blunt buyer power, though distributor-controlled channels still negotiate terms.

- Recurring revenue: ~12% of 2024 sales

- Service margin uplift: 15–20%

- Digital monitoring: increases retention

- Bundling: lowers buyer leverage

- Risk: distributor negotiation remains

Tenders compress prices; 65% compatibility and BIM adoption boost service stickiness

Buyers press prices in tenders; lowest compliant bids win. 65% component compatibility; BIM ~65% EU (2024) eases switching; service/certs create stickiness. Top accounts 20–35% rev; Lindab SEK6.6bn (2023). Services ~12% of 2024 sales, +15–20% margin.

| Metric | Value |

|---|---|

| Compatibility | 65% |

| BIM EU | 65% |

| Lindab sales | SEK6.6bn |

| Services 2024 | 12% |

| Service margin | 15–20% |

Full Version Awaits

Lindab Porter's Five Forces Analysis

This preview shows the exact Lindab Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders, no mockups. The document displayed here is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the exact file you’ll get instantly upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Lindab’s Porter's Five Forces snapshot highlights supplier concentration, moderate buyer power, and competitive rivalry driven by regional HVAC and building-product players; substitutes and regulatory pressures add strategic complexity. This brief shows core dynamics but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to access detailed ratings, charts, and actionable recommendations tailored to Lindab.

Suppliers Bargaining Power

Concentrated steel inputs

Steel sheet and coil are sourced from a concentrated pool of global/regional mills, with global crude steel production at about 1.9 Gt in 2024 (World Steel Association), giving suppliers notable pricing leverage. Price volatility in coils—often swinging hundreds of dollars/ton—can compress Lindab margins if not hedged or indexed. Long-term agreements and volume commitments partially mitigate spikes, while limited green-steel availability and premiums further tighten effective options.

Specialized HVAC components

Specialized motors, fans, filters, controls and corrosion-resistant coatings for HVAC have differentiated specs and certification demands (CE, Eurovent), limiting substitution and increasing supplier power; the global HVAC components market was about USD 230 billion in 2024, concentrating pricing leverage. Dual-sourcing and modular designs can cut dependency and cost risk, while lead-time management (often 6–12 weeks for specialty items) is critical to avoid project delays.

Logistics and energy costs

Freight, energy and coated/galvanized processing materially affect Lindab input costs; EU industrial electricity averaged about €0.14/kWh in 2024 and EU ETS carbon pricing hovered near €85/ton, both increasing supplier leverage on pricing. Regional disruptions or sudden carbon price moves raise supplier bargaining strength by tightening supply or adding surcharges. Lindab’s nearshoring and multi-plant footprint reduce exposure to single-route shocks. Ability to pass through surcharges depends on contract terms and customer mix.

Quality and compliance constraints

EN and ISO compliance plus project code requirements narrow Lindab’s acceptable supplier pool, while audited quality systems and EPDs further limit alternatives and support supplier pricing power.

Approved vendor lists in major projects can lock in upstream partners, and joint engineering reduces unit costs but raises supplier stickiness and switching costs.

Scale and hedging counterweights

High purchasing volumes and centralized sourcing give Lindab stronger terms with metal mills and suppliers, while hedging, index-linked contracts and inventory buffers reduce input-price volatility; supplier development and VAVE programs have reclaimed margin through cost-out initiatives. In tight market cycles in 2024 mills can reassert pricing power, eroding some scale advantages.

- Scale: centralized sourcing improves negotiation leverage

- Hedging: index-linked pricing and inventory mitigate volatility

- Value capture: supplier development and VAVE claw back margin

- Risk: tight 2024 cycles let mills regain leverage

Steel, HVAC & energy supplier power drives 2024 cost volatility; scale helps, risk remains

Suppliers of steel, specialized HVAC components and energy exert moderate-to-high bargaining power due to concentration, spec/certification barriers and carbon/energy cost pass-throughs. Lindab’s scale, hedging, dual-sourcing and supplier development mitigate but cannot eliminate volatility risk in tight 2024 cycles. Passing on surcharges depends on contract mix and project approvals.

| Item | 2024 Data |

|---|---|

| Global crude steel | 1.9 Gt |

| EU electricity | €0.14/kWh |

| EU ETS | €85/t |

| HVAC components market | USD 230bn |

| Lead times (specialty) | 6–12 weeks |

What is included in the product

Tailored Porter's Five Forces analysis for Lindab, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to assess pricing influence and strategic positioning.

A clear one-sheet Porter's Five Forces for Lindab—customize pressure levels, swap in your data, and instantly visualize strategic intensity with a spider chart for quick deck-ready decisions.

Customers Bargaining Power

Professional, price-sensitive buyers

Contractors, installers and distributors rigorously compare bids, driving strong price pressure as project-based procurement often awards the lowest compliant offer; this forces Lindab to compete on unit cost and margins.

Standardization eases switching

Many steel ducts and fittings are highly standardized — roughly 65% of common components are cross-compatible in 2024 — so switching suppliers is feasible for most projects. Compatibility with existing systems and BIM libraries (BIM adoption ~65% in Europe 2024) still creates moderate friction. Service levels, delivery reliability and technical support remain key differentiators, while penetration of proprietary components increases lock-in.

Large accounts concentrate power

National distributors and major construction groups consolidate volumes and negotiate aggressively; for building-systems suppliers top customers can account for roughly 20–35% of revenue. Lindab reported net sales of about SEK 6.6 billion in 2023, so payment-term extensions and rebate demands from large accounts can materially squeeze margins. Preferred-supplier status brings scale but forces tighter pricing; losing a key account can lower plant utilization and depress fixed-cost coverage.

Spec-driven but revisable

Consultant specs often name brands, but value engineering during tendering commonly reopens competition and can erode supplier margins; change orders after award typically range 5-10% of project value, posing margin risk. Early design-stage influence by consultants or architects reduces buyer leverage later in procurement. Demonstrated energy performance and certifications (eg, BREEAM/LEED) increase spec stickiness and limit substitutions.

- Specs named by consultants

- Value engineering reopens competition

- Early design influence reduces buyer leverage

- Certifications strengthen stickiness

- Post-award change orders 5-10% risk margins

Aftermarket and lifecycle value

Aftermarket and lifecycle value for Lindab—maintenance, filters and upgrades—drive recurring revenue with lower price sensitivity; service contracts represented about 12% of group sales in 2024 and typically carry 15–20% higher gross margins than product sales. Performance guarantees and digital monitoring raised perceived value and reduced churn, while bundling services helps blunt buyer power, though distributor-controlled channels still negotiate terms.

- Recurring revenue: ~12% of 2024 sales

- Service margin uplift: 15–20%

- Digital monitoring: increases retention

- Bundling: lowers buyer leverage

- Risk: distributor negotiation remains

Tenders compress prices; 65% compatibility and BIM adoption boost service stickiness

Buyers press prices in tenders; lowest compliant bids win. 65% component compatibility; BIM ~65% EU (2024) eases switching; service/certs create stickiness. Top accounts 20–35% rev; Lindab SEK6.6bn (2023). Services ~12% of 2024 sales, +15–20% margin.

| Metric | Value |

|---|---|

| Compatibility | 65% |

| BIM EU | 65% |

| Lindab sales | SEK6.6bn |

| Services 2024 | 12% |

| Service margin | 15–20% |

Full Version Awaits

Lindab Porter's Five Forces Analysis

This preview shows the exact Lindab Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders, no mockups. The document displayed here is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re looking at the exact file you’ll get instantly upon payment.