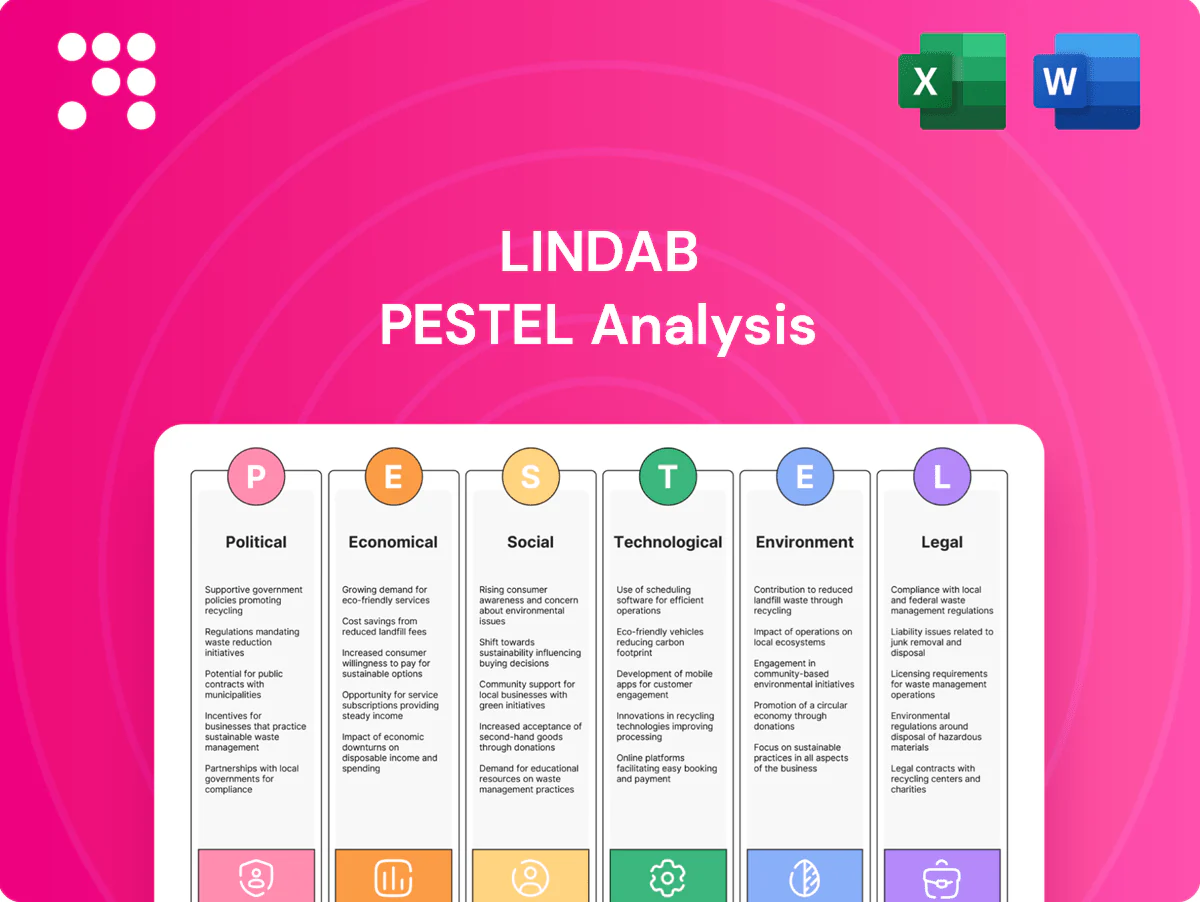

Lindab PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental regulations are shaping Lindab’s strategic outlook with our concise PESTLE snapshot; perfect for investors and strategists needing quick, reliable context. Dive deeper—buy the full PESTLE for actionable insights, editable charts, and ready-to-use recommendations. Download now to make smarter, faster decisions.

Political factors

EU energy-efficiency policies and subsidies

Stronger EU and national policies—Fit for 55 and the Renovation Wave, which aims to at least double the current annual building renovation rate by 2030—boost demand for high-efficiency ventilation and building envelopes; buildings account for about 40% of EU energy consumption. Subsidy programs financed via NextGenerationEU (≈€806.9bn) and national schemes can accelerate retrofit uptake and pipeline visibility for Lindab. Policy stability directly shapes investment cycles and project financing timelines, while shifts in political leadership can reallocate subsidies and change priority sectors, altering short-term project pipelines and demand forecasts.

Trade relations and steel tariffs

Import tariffs such as the US Section 232 25% levy and anti-dumping duties that in some cases exceed 30% materially lift Lindab’s steel input costs, while trade disputes have driven steel price swings of roughly 20–40% between 2022–24. Favorable trade agreements can lower sourcing costs and improve margins by reducing these levies. Rising protectionism increases volatility and planning complexity, so Lindab must diversify suppliers and geographies to mitigate political trade risks.

Public infrastructure and housing programs

Government-backed construction, including allocations from the EU Recovery and Resilience Facility (€723.8bn), boosts demand for HVAC and building systems and can lift Lindab order intake. Stimulus-driven cyclical upswings are common, while EU Fit for 55 policies (‑55% GHG by 2030) and green procurement increasingly favor sustainable, standardized solutions. Political budget-cycle delays can defer public project starts and revenue recognition.

Geopolitical stability and energy security

Geopolitical shocks since the 2022 Russia‑Ukraine war heightened focus on energy security, boosting demand for insulation and energy‑efficient ventilation that align with Lindab’s product mix; supply‑chain disruptions and volatile energy prices have intermittently delayed projects and raised costs.

- Policy support for resilient buildings favors Lindab

- Regional instability => higher inventory/logistics needs

Local content and public procurement rules

Local-content and certified-supplier rules significantly affect Lindab in markets where public procurement is large: EU public procurement totals about 14% of GDP (roughly €2 trillion annually), so certification and local sourcing materially boost bid competitiveness. Compliance shapes plant siting and partner selection, and non-compliance risks exclusion from major tenders under EU procurement rules.

- Compliance: certified suppliers preferred

- Bidding: affects public project wins

- Operations: influences plant location/partners

- Risk: exclusion from key tenders

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

EU Fit for 55 and Renovation Wave aim to double renovation rates by 2030; buildings = ~40% EU energy use, boosting demand for Lindab; NextGenerationEU ≈€806.9bn and RRF €723.8bn support retrofits. US Section 232 25% tariff and 20–40% steel price swings (2022–24) raise input cost volatility; EU public procurement ≈14% GDP (~€2tn) makes local-content rules material.

| Factor | Key stat | Impact |

|---|---|---|

| Renovation policy | Double rate by 2030 | Higher HVAC/insulation demand |

| Funding | NextGenerationEU €806.9bn | Accelerates projects |

| Trade | US tariff 25%; steel ±20–40% | Input cost risk |

| Procurement | EU public ≈€2tn | Local-content importance |

What is included in the product

Explores how macro-environmental factors uniquely affect Lindab across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, company-specific sub-points and examples. Backed by current data and forward-looking insights, the analysis is formatted for executives and investors to identify risks, opportunities and inform scenario-driven strategy.

Condensed, visually segmented PESTLE of Lindab that highlights key external risks and opportunities for quick decision-making, easily dropped into presentations or shared across teams and annotated for local context or business lines.

Economic factors

Construction cycle sensitivity

New builds and renovations closely follow GDP and financing costs: euro area GDP grew about 0.6% in 2024 with IMF/EC forecasts near 1.2% for 2025, while European policy rates averaged around 3.5–3.8% by mid‑2025, influencing capex timing. Slowdowns defer projects; falling rates and stronger growth unlock construction spending. Renovation demand has been more resilient than new builds, and Lindab’s exposure to both segments helps smooth revenue across cycles.

Steel price volatility

Steel price volatility is a primary driver of Lindab’s COGS variability, directly influencing gross margins. Sudden price spikes erode profitability on fixed-price contracts unless mitigated. Hedging programs and index-linked pricing clauses are used to protect margins. Supply diversification and secure sourcing reduce exposure; global crude steel production was about 1.95 billion tonnes in 2023 (Worldsteel).

Inflation and interest rates

High inflation lifts wages and transport costs—Euro area HICP eased to about 2.5% in H1 2025 but input costs spiked in 2024, forcing timely price adjustments. Rate hikes (ECB deposit rate around 4% in 2024–25) have dampened construction financing and developer appetite. Deflation risks would force inventory revaluation and reduce demand. Working capital discipline is critical across cycles.

Labor availability and productivity

Skilled installer shortages are delaying HVAC and ventilation projects, pushing clients toward systems that are faster to fit; easy-to-assemble Lindab solutions gain preference when labor is constrained. Rising wage pressures increase total installation cost, favoring prefabricated components that cut on-site hours. Strategic training programs and installer partnerships improve throughput and shorten lead times.

- Skilled installer shortages: project delays

- Easy-assemble products: higher preference

- Wage growth: shifts demand to prefab

- Training/partnerships: unlock throughput

Currency fluctuations

Currency fluctuations create both translation and transaction risk for Lindab, which operates in about 30 countries; FX moves affected reported results in 2024 as SEK strength compressed export competitiveness. Natural hedges from local sourcing and local invoicing reduce exposure, while pricing and contract terms must enable FX pass-through to protect margins.

- FX translation risk: multi-market reporting

- Transaction risk: export pricing vs strong SEK

- Mitigation: local sourcing, local invoicing, FX pass-through

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

Euro area growth ~0.6% in 2024, IMF/EC ~1.2% for 2025 and ECB deposit rate ~4% (2024–25) shaping capex; HICP ≈2.5% H1 2025 raising input/wage costs. Steel volatility (global crude steel ~1.95bn t in 2023) drives COGS; hedging and index pricing mitigate margin risk. Lindab present in ~30 countries — SEK strength in 2024 hit export competitiveness, local sourcing/invoicing reduce FX exposure.

| Metric | Value |

|---|---|

| Euro area GDP 2024/25 | 0.6% / 1.2% (2025F) |

| ECB deposit rate | ~4% |

| Euro area HICP H1 2025 | ~2.5% |

| Global crude steel 2023 | 1.95 bn t |

| Countries | ~30 |

Preview the Actual Deliverable

Lindab PESTLE Analysis

The preview shown here is the exact Lindab PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final deliverable with no placeholders or edits required. After checkout you’ll instantly download this same professionally structured file.

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental regulations are shaping Lindab’s strategic outlook with our concise PESTLE snapshot; perfect for investors and strategists needing quick, reliable context. Dive deeper—buy the full PESTLE for actionable insights, editable charts, and ready-to-use recommendations. Download now to make smarter, faster decisions.

Political factors

EU energy-efficiency policies and subsidies

Stronger EU and national policies—Fit for 55 and the Renovation Wave, which aims to at least double the current annual building renovation rate by 2030—boost demand for high-efficiency ventilation and building envelopes; buildings account for about 40% of EU energy consumption. Subsidy programs financed via NextGenerationEU (≈€806.9bn) and national schemes can accelerate retrofit uptake and pipeline visibility for Lindab. Policy stability directly shapes investment cycles and project financing timelines, while shifts in political leadership can reallocate subsidies and change priority sectors, altering short-term project pipelines and demand forecasts.

Trade relations and steel tariffs

Import tariffs such as the US Section 232 25% levy and anti-dumping duties that in some cases exceed 30% materially lift Lindab’s steel input costs, while trade disputes have driven steel price swings of roughly 20–40% between 2022–24. Favorable trade agreements can lower sourcing costs and improve margins by reducing these levies. Rising protectionism increases volatility and planning complexity, so Lindab must diversify suppliers and geographies to mitigate political trade risks.

Public infrastructure and housing programs

Government-backed construction, including allocations from the EU Recovery and Resilience Facility (€723.8bn), boosts demand for HVAC and building systems and can lift Lindab order intake. Stimulus-driven cyclical upswings are common, while EU Fit for 55 policies (‑55% GHG by 2030) and green procurement increasingly favor sustainable, standardized solutions. Political budget-cycle delays can defer public project starts and revenue recognition.

Geopolitical stability and energy security

Geopolitical shocks since the 2022 Russia‑Ukraine war heightened focus on energy security, boosting demand for insulation and energy‑efficient ventilation that align with Lindab’s product mix; supply‑chain disruptions and volatile energy prices have intermittently delayed projects and raised costs.

- Policy support for resilient buildings favors Lindab

- Regional instability => higher inventory/logistics needs

Local content and public procurement rules

Local-content and certified-supplier rules significantly affect Lindab in markets where public procurement is large: EU public procurement totals about 14% of GDP (roughly €2 trillion annually), so certification and local sourcing materially boost bid competitiveness. Compliance shapes plant siting and partner selection, and non-compliance risks exclusion from major tenders under EU procurement rules.

- Compliance: certified suppliers preferred

- Bidding: affects public project wins

- Operations: influences plant location/partners

- Risk: exclusion from key tenders

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

EU Fit for 55 and Renovation Wave aim to double renovation rates by 2030; buildings = ~40% EU energy use, boosting demand for Lindab; NextGenerationEU ≈€806.9bn and RRF €723.8bn support retrofits. US Section 232 25% tariff and 20–40% steel price swings (2022–24) raise input cost volatility; EU public procurement ≈14% GDP (~€2tn) makes local-content rules material.

| Factor | Key stat | Impact |

|---|---|---|

| Renovation policy | Double rate by 2030 | Higher HVAC/insulation demand |

| Funding | NextGenerationEU €806.9bn | Accelerates projects |

| Trade | US tariff 25%; steel ±20–40% | Input cost risk |

| Procurement | EU public ≈€2tn | Local-content importance |

What is included in the product

Explores how macro-environmental factors uniquely affect Lindab across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, company-specific sub-points and examples. Backed by current data and forward-looking insights, the analysis is formatted for executives and investors to identify risks, opportunities and inform scenario-driven strategy.

Condensed, visually segmented PESTLE of Lindab that highlights key external risks and opportunities for quick decision-making, easily dropped into presentations or shared across teams and annotated for local context or business lines.

Economic factors

Construction cycle sensitivity

New builds and renovations closely follow GDP and financing costs: euro area GDP grew about 0.6% in 2024 with IMF/EC forecasts near 1.2% for 2025, while European policy rates averaged around 3.5–3.8% by mid‑2025, influencing capex timing. Slowdowns defer projects; falling rates and stronger growth unlock construction spending. Renovation demand has been more resilient than new builds, and Lindab’s exposure to both segments helps smooth revenue across cycles.

Steel price volatility

Steel price volatility is a primary driver of Lindab’s COGS variability, directly influencing gross margins. Sudden price spikes erode profitability on fixed-price contracts unless mitigated. Hedging programs and index-linked pricing clauses are used to protect margins. Supply diversification and secure sourcing reduce exposure; global crude steel production was about 1.95 billion tonnes in 2023 (Worldsteel).

Inflation and interest rates

High inflation lifts wages and transport costs—Euro area HICP eased to about 2.5% in H1 2025 but input costs spiked in 2024, forcing timely price adjustments. Rate hikes (ECB deposit rate around 4% in 2024–25) have dampened construction financing and developer appetite. Deflation risks would force inventory revaluation and reduce demand. Working capital discipline is critical across cycles.

Labor availability and productivity

Skilled installer shortages are delaying HVAC and ventilation projects, pushing clients toward systems that are faster to fit; easy-to-assemble Lindab solutions gain preference when labor is constrained. Rising wage pressures increase total installation cost, favoring prefabricated components that cut on-site hours. Strategic training programs and installer partnerships improve throughput and shorten lead times.

- Skilled installer shortages: project delays

- Easy-assemble products: higher preference

- Wage growth: shifts demand to prefab

- Training/partnerships: unlock throughput

Currency fluctuations

Currency fluctuations create both translation and transaction risk for Lindab, which operates in about 30 countries; FX moves affected reported results in 2024 as SEK strength compressed export competitiveness. Natural hedges from local sourcing and local invoicing reduce exposure, while pricing and contract terms must enable FX pass-through to protect margins.

- FX translation risk: multi-market reporting

- Transaction risk: export pricing vs strong SEK

- Mitigation: local sourcing, local invoicing, FX pass-through

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

Euro area growth ~0.6% in 2024, IMF/EC ~1.2% for 2025 and ECB deposit rate ~4% (2024–25) shaping capex; HICP ≈2.5% H1 2025 raising input/wage costs. Steel volatility (global crude steel ~1.95bn t in 2023) drives COGS; hedging and index pricing mitigate margin risk. Lindab present in ~30 countries — SEK strength in 2024 hit export competitiveness, local sourcing/invoicing reduce FX exposure.

| Metric | Value |

|---|---|

| Euro area GDP 2024/25 | 0.6% / 1.2% (2025F) |

| ECB deposit rate | ~4% |

| Euro area HICP H1 2025 | ~2.5% |

| Global crude steel 2023 | 1.95 bn t |

| Countries | ~30 |

Preview the Actual Deliverable

Lindab PESTLE Analysis

The preview shown here is the exact Lindab PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final deliverable with no placeholders or edits required. After checkout you’ll instantly download this same professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic cycles, and environmental regulations are shaping Lindab’s strategic outlook with our concise PESTLE snapshot; perfect for investors and strategists needing quick, reliable context. Dive deeper—buy the full PESTLE for actionable insights, editable charts, and ready-to-use recommendations. Download now to make smarter, faster decisions.

Political factors

EU energy-efficiency policies and subsidies

Stronger EU and national policies—Fit for 55 and the Renovation Wave, which aims to at least double the current annual building renovation rate by 2030—boost demand for high-efficiency ventilation and building envelopes; buildings account for about 40% of EU energy consumption. Subsidy programs financed via NextGenerationEU (≈€806.9bn) and national schemes can accelerate retrofit uptake and pipeline visibility for Lindab. Policy stability directly shapes investment cycles and project financing timelines, while shifts in political leadership can reallocate subsidies and change priority sectors, altering short-term project pipelines and demand forecasts.

Trade relations and steel tariffs

Import tariffs such as the US Section 232 25% levy and anti-dumping duties that in some cases exceed 30% materially lift Lindab’s steel input costs, while trade disputes have driven steel price swings of roughly 20–40% between 2022–24. Favorable trade agreements can lower sourcing costs and improve margins by reducing these levies. Rising protectionism increases volatility and planning complexity, so Lindab must diversify suppliers and geographies to mitigate political trade risks.

Public infrastructure and housing programs

Government-backed construction, including allocations from the EU Recovery and Resilience Facility (€723.8bn), boosts demand for HVAC and building systems and can lift Lindab order intake. Stimulus-driven cyclical upswings are common, while EU Fit for 55 policies (‑55% GHG by 2030) and green procurement increasingly favor sustainable, standardized solutions. Political budget-cycle delays can defer public project starts and revenue recognition.

Geopolitical stability and energy security

Geopolitical shocks since the 2022 Russia‑Ukraine war heightened focus on energy security, boosting demand for insulation and energy‑efficient ventilation that align with Lindab’s product mix; supply‑chain disruptions and volatile energy prices have intermittently delayed projects and raised costs.

- Policy support for resilient buildings favors Lindab

- Regional instability => higher inventory/logistics needs

Local content and public procurement rules

Local-content and certified-supplier rules significantly affect Lindab in markets where public procurement is large: EU public procurement totals about 14% of GDP (roughly €2 trillion annually), so certification and local sourcing materially boost bid competitiveness. Compliance shapes plant siting and partner selection, and non-compliance risks exclusion from major tenders under EU procurement rules.

- Compliance: certified suppliers preferred

- Bidding: affects public project wins

- Operations: influences plant location/partners

- Risk: exclusion from key tenders

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

EU Fit for 55 and Renovation Wave aim to double renovation rates by 2030; buildings = ~40% EU energy use, boosting demand for Lindab; NextGenerationEU ≈€806.9bn and RRF €723.8bn support retrofits. US Section 232 25% tariff and 20–40% steel price swings (2022–24) raise input cost volatility; EU public procurement ≈14% GDP (~€2tn) makes local-content rules material.

| Factor | Key stat | Impact |

|---|---|---|

| Renovation policy | Double rate by 2030 | Higher HVAC/insulation demand |

| Funding | NextGenerationEU €806.9bn | Accelerates projects |

| Trade | US tariff 25%; steel ±20–40% | Input cost risk |

| Procurement | EU public ≈€2tn | Local-content importance |

What is included in the product

Explores how macro-environmental factors uniquely affect Lindab across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, company-specific sub-points and examples. Backed by current data and forward-looking insights, the analysis is formatted for executives and investors to identify risks, opportunities and inform scenario-driven strategy.

Condensed, visually segmented PESTLE of Lindab that highlights key external risks and opportunities for quick decision-making, easily dropped into presentations or shared across teams and annotated for local context or business lines.

Economic factors

Construction cycle sensitivity

New builds and renovations closely follow GDP and financing costs: euro area GDP grew about 0.6% in 2024 with IMF/EC forecasts near 1.2% for 2025, while European policy rates averaged around 3.5–3.8% by mid‑2025, influencing capex timing. Slowdowns defer projects; falling rates and stronger growth unlock construction spending. Renovation demand has been more resilient than new builds, and Lindab’s exposure to both segments helps smooth revenue across cycles.

Steel price volatility

Steel price volatility is a primary driver of Lindab’s COGS variability, directly influencing gross margins. Sudden price spikes erode profitability on fixed-price contracts unless mitigated. Hedging programs and index-linked pricing clauses are used to protect margins. Supply diversification and secure sourcing reduce exposure; global crude steel production was about 1.95 billion tonnes in 2023 (Worldsteel).

Inflation and interest rates

High inflation lifts wages and transport costs—Euro area HICP eased to about 2.5% in H1 2025 but input costs spiked in 2024, forcing timely price adjustments. Rate hikes (ECB deposit rate around 4% in 2024–25) have dampened construction financing and developer appetite. Deflation risks would force inventory revaluation and reduce demand. Working capital discipline is critical across cycles.

Labor availability and productivity

Skilled installer shortages are delaying HVAC and ventilation projects, pushing clients toward systems that are faster to fit; easy-to-assemble Lindab solutions gain preference when labor is constrained. Rising wage pressures increase total installation cost, favoring prefabricated components that cut on-site hours. Strategic training programs and installer partnerships improve throughput and shorten lead times.

- Skilled installer shortages: project delays

- Easy-assemble products: higher preference

- Wage growth: shifts demand to prefab

- Training/partnerships: unlock throughput

Currency fluctuations

Currency fluctuations create both translation and transaction risk for Lindab, which operates in about 30 countries; FX moves affected reported results in 2024 as SEK strength compressed export competitiveness. Natural hedges from local sourcing and local invoicing reduce exposure, while pricing and contract terms must enable FX pass-through to protect margins.

- FX translation risk: multi-market reporting

- Transaction risk: export pricing vs strong SEK

- Mitigation: local sourcing, local invoicing, FX pass-through

EU retrofit surge, €806.9bn funding and tariffs drive demand and cost volatility

Euro area growth ~0.6% in 2024, IMF/EC ~1.2% for 2025 and ECB deposit rate ~4% (2024–25) shaping capex; HICP ≈2.5% H1 2025 raising input/wage costs. Steel volatility (global crude steel ~1.95bn t in 2023) drives COGS; hedging and index pricing mitigate margin risk. Lindab present in ~30 countries — SEK strength in 2024 hit export competitiveness, local sourcing/invoicing reduce FX exposure.

| Metric | Value |

|---|---|

| Euro area GDP 2024/25 | 0.6% / 1.2% (2025F) |

| ECB deposit rate | ~4% |

| Euro area HICP H1 2025 | ~2.5% |

| Global crude steel 2023 | 1.95 bn t |

| Countries | ~30 |

Preview the Actual Deliverable

Lindab PESTLE Analysis

The preview shown here is the exact Lindab PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are the final deliverable with no placeholders or edits required. After checkout you’ll instantly download this same professionally structured file.