Linde Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

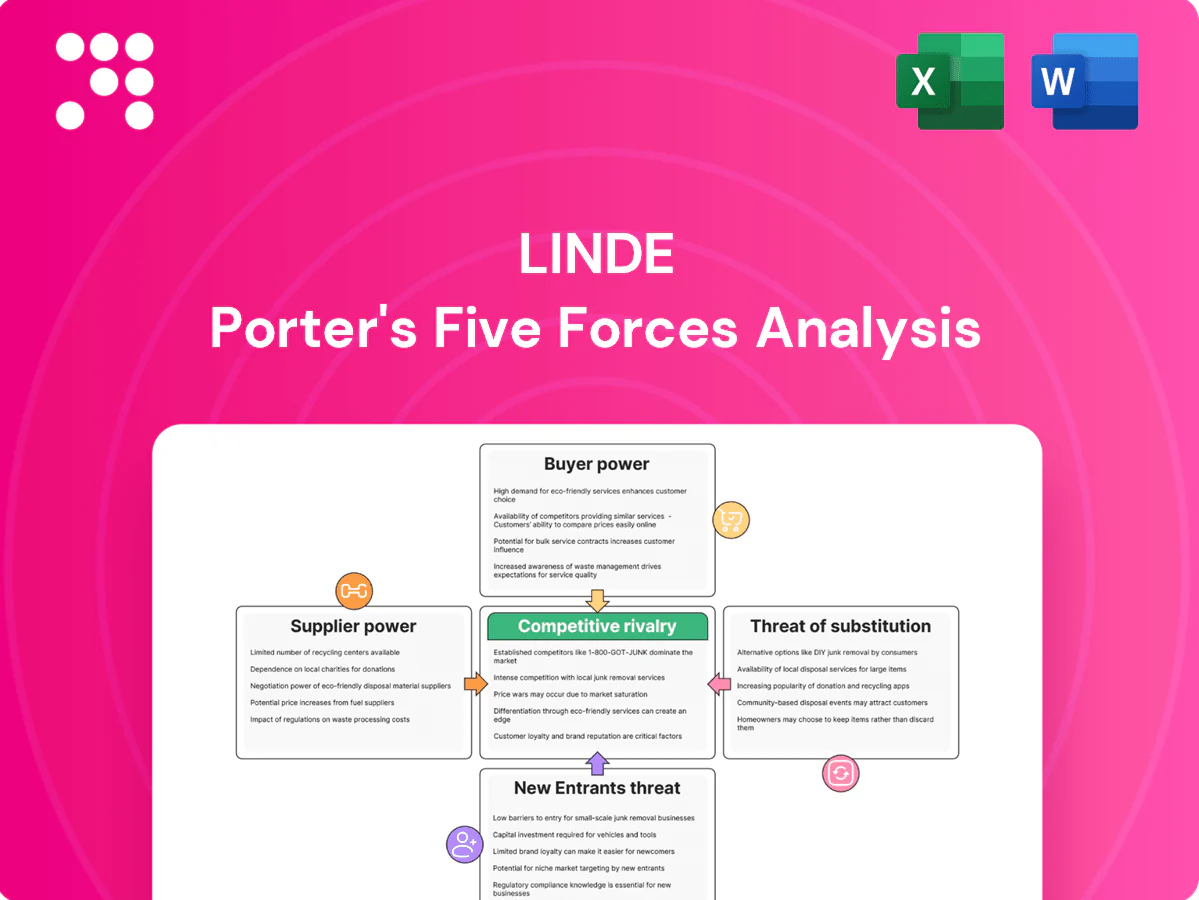

Linde operates in a capital‑intensive, concentrated industrial gas market where supplier leverage, buyer negotiation, substitutes, new entrants, and rivalry determine margins and growth. Regulatory heft and scale bolster its position, while tech shifts and customer consolidation raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Linde’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs (helium, specialty gases)

Helium supply is concentrated in a few geographies and producers, elevating supplier leverage on price and allocation; scarcity periods have forced pass-through pricing and contractual escalators. Linde mitigates via long-term sourcing agreements, customer-side recycling programs, and a broad industrial-gases portfolio, but episodic shortages still tighten supplier power. Supply shocks can ripple into margins and service levels, particularly for specialty-gas reliant end markets.

Energy and power intensity of operations

Cryogenic air separation and liquefaction consume roughly 200–300 kWh per tonne of O2, tying Linde's unit costs to local utility tariffs. In 2024 industrial electricity averaged about $0.07–0.09/kWh in the US and €0.12–0.18/kWh in the EU, and regulated utility oligopolies can pass through costs imperfectly and with lag. Short-term spikes increase supplier bargaining power. Hedging and efficiency projects (waste-heat recovery, electrification) moderate exposure over time.

Specialized equipment and engineering vendors

Large compressors, turbines and cryogenic heat exchangers are sourced from a limited OEM pool (often under 10 firms), with lead times of 12–24 months and 6–18 month qualification cycles giving suppliers leverage. Linde’s global footprint in 100+ countries, scale and strong in-house engineering enable multisourcing and reduce single-vendor risk. Long-term partnerships trade price for reliability and access to joint innovation, supporting asset uptime and cost predictability.

Hydrocarbon and feedstock sourcing

Hydrogen, syngas and CO2 largely come from natural gas/refinery off‑gases; commodity inputs limit supplier power but pipeline bottlenecks and regional gas price spikes (Henry Hub ~ $2.8/MMBtu in 2024) can raise local leverage. Indexed supply contracts align feedstock and product pricing; on‑site SMRs and vertical integration cut third‑party exposure.

- Commodity input: lowers supplier power

- Infrastructure: creates localized leverage

- Indexed contracts: price alignment

- Vertical integration: reduces exposure

Logistics and industrial services

- Specialized transport reliance

- ATA driver shortfall ~80,000 (2023) impacting 2024 capacity

- Linde owned fleet reduces supplier leverage

- Bottlenecks in surges/regulatory changes

Helium squeeze: concentrated producers, <10 OEMs and logistics drive volatility

Supplier power is elevated by concentrated helium sources, limited OEMs (<10) for cryogenic equipment, and logistics bottlenecks (US driver shortfall ~80,000 in 2023 impacting 2024). Energy exposure (US $0.07–0.09/kWh; EU €0.12–0.18/kWh) and regional gas moves (Henry Hub ≈ $2.8/MMBtu) add volatility; Linde offsets via long‑term contracts, vertical integration and owned fleet.

| Metric | 2024 |

|---|---|

| Helium concentration | Few geographies/producers |

| OEM pool | <10 firms |

| Electricity | US $0.07–0.09/kWh; EU €0.12–0.18/kWh |

| Henry Hub | $2.8/MMBtu |

| Driver shortfall | ~80,000 (2023) |

What is included in the product

Concise Porter's Five Forces analysis of Linde, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal key pressures on margins, market share, and strategic positioning within the industrial gases and engineering sectors.

One-sheet Porter's Five Forces tailored for Linde—quickly highlights supplier, buyer, rivalry, new entrant, and substitute pressures so teams can prioritize strategic moves and reduce decision paralysis.

Customers Bargaining Power

Large industrial customers with scale

Steel, chemical and refining customers buy very high volumes and run competitive tenders, enabling significant price concessions and bespoke commercial terms. Their scale drives negotiating leverage, but take-or-pay provisions and indexation to feedstock or CPI limit renegotiation frequency. Multi-year on-site contracts, often 10+ years, lock in supply and materially reduce churn despite initial buyer leverage.

High switching costs from embedded supply

Pipelines, on-site plants and strict customer qualifications make switching disruptive and costly; on-site contracts commonly exceed 5 years, often tying customers into bespoke infrastructure. Reliability and safety track records thus outweigh small price deltas, shrinking ongoing buyer leverage. This structural stickiness reduces customer bargaining power once contracts are in place and lengthens renewal cycles in Linde’s favor.

Fragmented mid/small buyers in healthcare and food

Fragmented mid/small buyers in healthcare and food limit bargaining power because numerous smaller accounts are less able to negotiate bespoke pricing; Linde reported roughly $39.4 billion in 2023 sales, highlighting scale advantages. Packaged and specialty gases command higher margins and service components, reinforcing supplier leverage. Strict delivery, compliance and purity needs lower buyer mobility, though volume-aggregation platforms can modestly increase leverage by pooling demand.

Cyclicality and price sensitivity

Cyclicality raises buyer pushback on price and volumes during industrial downturns, forcing Linde to lean on index-linked clauses and surcharges to protect margins, though these mechanisms often lag spot cost movements. In expansion phases, customers prioritize uptime and delivery speed, reducing price sensitivity as urgency outweighs marginal cost. Quarterly shifts in demand mix between merchant, bulk and project volumes can materially swing bargaining leverage.

- Index-linked pricing: preserves economics but lags

- Downturns: stronger buyer negotiation on price/volumes

- Expansions: uptime reduces price sensitivity

- Quarterly demand-mix swings alter leverage

Technical differentiation and service bundling

Application engineering, digital monitoring and guaranteed uptime (often 99.9% service SLAs) create switching friction—buyers prioritize process optimization and safety over commodity molecules, and bundled solutions dilute pure price comparisons, softening buyer power where performance guarantees are critical.

- Application engineering: increases lock‑in

- Digital monitoring: reduces downtime, improves ROI

- 99.9% uptime SLAs: shifts focus from price to reliability

- Bundled services: mask unit‑price comparisons

Buyers have upfront leverage, but multi-year index-linked contracts and 99.9% SLAs curb it

Linde customers have strong upfront bargaining power via large tenders and volume, but multi‑year on‑site contracts (commonly 5–10+ years), index‑linked pricing and high switching costs materially reduce ongoing leverage; reliability, SLAs (≈99.9%) and bundled services shift negotiations toward service terms. Linde reported $39.4 billion sales in 2023 and maintained margin resilience through indexation in 2024.

| Metric | Value |

|---|---|

| Typical contract length | 5–10+ yrs |

| 2023 sales | $39.4B |

| Service SLA | ≈99.9% |

Preview the Actual Deliverable

Linde Porter's Five Forces Analysis

This preview shows the exact Linde Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.

A Must-Have Tool for Decision-Makers

Linde operates in a capital‑intensive, concentrated industrial gas market where supplier leverage, buyer negotiation, substitutes, new entrants, and rivalry determine margins and growth. Regulatory heft and scale bolster its position, while tech shifts and customer consolidation raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Linde’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs (helium, specialty gases)

Helium supply is concentrated in a few geographies and producers, elevating supplier leverage on price and allocation; scarcity periods have forced pass-through pricing and contractual escalators. Linde mitigates via long-term sourcing agreements, customer-side recycling programs, and a broad industrial-gases portfolio, but episodic shortages still tighten supplier power. Supply shocks can ripple into margins and service levels, particularly for specialty-gas reliant end markets.

Energy and power intensity of operations

Cryogenic air separation and liquefaction consume roughly 200–300 kWh per tonne of O2, tying Linde's unit costs to local utility tariffs. In 2024 industrial electricity averaged about $0.07–0.09/kWh in the US and €0.12–0.18/kWh in the EU, and regulated utility oligopolies can pass through costs imperfectly and with lag. Short-term spikes increase supplier bargaining power. Hedging and efficiency projects (waste-heat recovery, electrification) moderate exposure over time.

Specialized equipment and engineering vendors

Large compressors, turbines and cryogenic heat exchangers are sourced from a limited OEM pool (often under 10 firms), with lead times of 12–24 months and 6–18 month qualification cycles giving suppliers leverage. Linde’s global footprint in 100+ countries, scale and strong in-house engineering enable multisourcing and reduce single-vendor risk. Long-term partnerships trade price for reliability and access to joint innovation, supporting asset uptime and cost predictability.

Hydrocarbon and feedstock sourcing

Hydrogen, syngas and CO2 largely come from natural gas/refinery off‑gases; commodity inputs limit supplier power but pipeline bottlenecks and regional gas price spikes (Henry Hub ~ $2.8/MMBtu in 2024) can raise local leverage. Indexed supply contracts align feedstock and product pricing; on‑site SMRs and vertical integration cut third‑party exposure.

- Commodity input: lowers supplier power

- Infrastructure: creates localized leverage

- Indexed contracts: price alignment

- Vertical integration: reduces exposure

Logistics and industrial services

- Specialized transport reliance

- ATA driver shortfall ~80,000 (2023) impacting 2024 capacity

- Linde owned fleet reduces supplier leverage

- Bottlenecks in surges/regulatory changes

Helium squeeze: concentrated producers, <10 OEMs and logistics drive volatility

Supplier power is elevated by concentrated helium sources, limited OEMs (<10) for cryogenic equipment, and logistics bottlenecks (US driver shortfall ~80,000 in 2023 impacting 2024). Energy exposure (US $0.07–0.09/kWh; EU €0.12–0.18/kWh) and regional gas moves (Henry Hub ≈ $2.8/MMBtu) add volatility; Linde offsets via long‑term contracts, vertical integration and owned fleet.

| Metric | 2024 |

|---|---|

| Helium concentration | Few geographies/producers |

| OEM pool | <10 firms |

| Electricity | US $0.07–0.09/kWh; EU €0.12–0.18/kWh |

| Henry Hub | $2.8/MMBtu |

| Driver shortfall | ~80,000 (2023) |

What is included in the product

Concise Porter's Five Forces analysis of Linde, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal key pressures on margins, market share, and strategic positioning within the industrial gases and engineering sectors.

One-sheet Porter's Five Forces tailored for Linde—quickly highlights supplier, buyer, rivalry, new entrant, and substitute pressures so teams can prioritize strategic moves and reduce decision paralysis.

Customers Bargaining Power

Large industrial customers with scale

Steel, chemical and refining customers buy very high volumes and run competitive tenders, enabling significant price concessions and bespoke commercial terms. Their scale drives negotiating leverage, but take-or-pay provisions and indexation to feedstock or CPI limit renegotiation frequency. Multi-year on-site contracts, often 10+ years, lock in supply and materially reduce churn despite initial buyer leverage.

High switching costs from embedded supply

Pipelines, on-site plants and strict customer qualifications make switching disruptive and costly; on-site contracts commonly exceed 5 years, often tying customers into bespoke infrastructure. Reliability and safety track records thus outweigh small price deltas, shrinking ongoing buyer leverage. This structural stickiness reduces customer bargaining power once contracts are in place and lengthens renewal cycles in Linde’s favor.

Fragmented mid/small buyers in healthcare and food

Fragmented mid/small buyers in healthcare and food limit bargaining power because numerous smaller accounts are less able to negotiate bespoke pricing; Linde reported roughly $39.4 billion in 2023 sales, highlighting scale advantages. Packaged and specialty gases command higher margins and service components, reinforcing supplier leverage. Strict delivery, compliance and purity needs lower buyer mobility, though volume-aggregation platforms can modestly increase leverage by pooling demand.

Cyclicality and price sensitivity

Cyclicality raises buyer pushback on price and volumes during industrial downturns, forcing Linde to lean on index-linked clauses and surcharges to protect margins, though these mechanisms often lag spot cost movements. In expansion phases, customers prioritize uptime and delivery speed, reducing price sensitivity as urgency outweighs marginal cost. Quarterly shifts in demand mix between merchant, bulk and project volumes can materially swing bargaining leverage.

- Index-linked pricing: preserves economics but lags

- Downturns: stronger buyer negotiation on price/volumes

- Expansions: uptime reduces price sensitivity

- Quarterly demand-mix swings alter leverage

Technical differentiation and service bundling

Application engineering, digital monitoring and guaranteed uptime (often 99.9% service SLAs) create switching friction—buyers prioritize process optimization and safety over commodity molecules, and bundled solutions dilute pure price comparisons, softening buyer power where performance guarantees are critical.

- Application engineering: increases lock‑in

- Digital monitoring: reduces downtime, improves ROI

- 99.9% uptime SLAs: shifts focus from price to reliability

- Bundled services: mask unit‑price comparisons

Buyers have upfront leverage, but multi-year index-linked contracts and 99.9% SLAs curb it

Linde customers have strong upfront bargaining power via large tenders and volume, but multi‑year on‑site contracts (commonly 5–10+ years), index‑linked pricing and high switching costs materially reduce ongoing leverage; reliability, SLAs (≈99.9%) and bundled services shift negotiations toward service terms. Linde reported $39.4 billion sales in 2023 and maintained margin resilience through indexation in 2024.

| Metric | Value |

|---|---|

| Typical contract length | 5–10+ yrs |

| 2023 sales | $39.4B |

| Service SLA | ≈99.9% |

Preview the Actual Deliverable

Linde Porter's Five Forces Analysis

This preview shows the exact Linde Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Linde operates in a capital‑intensive, concentrated industrial gas market where supplier leverage, buyer negotiation, substitutes, new entrants, and rivalry determine margins and growth. Regulatory heft and scale bolster its position, while tech shifts and customer consolidation raise strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Linde’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical inputs (helium, specialty gases)

Helium supply is concentrated in a few geographies and producers, elevating supplier leverage on price and allocation; scarcity periods have forced pass-through pricing and contractual escalators. Linde mitigates via long-term sourcing agreements, customer-side recycling programs, and a broad industrial-gases portfolio, but episodic shortages still tighten supplier power. Supply shocks can ripple into margins and service levels, particularly for specialty-gas reliant end markets.

Energy and power intensity of operations

Cryogenic air separation and liquefaction consume roughly 200–300 kWh per tonne of O2, tying Linde's unit costs to local utility tariffs. In 2024 industrial electricity averaged about $0.07–0.09/kWh in the US and €0.12–0.18/kWh in the EU, and regulated utility oligopolies can pass through costs imperfectly and with lag. Short-term spikes increase supplier bargaining power. Hedging and efficiency projects (waste-heat recovery, electrification) moderate exposure over time.

Specialized equipment and engineering vendors

Large compressors, turbines and cryogenic heat exchangers are sourced from a limited OEM pool (often under 10 firms), with lead times of 12–24 months and 6–18 month qualification cycles giving suppliers leverage. Linde’s global footprint in 100+ countries, scale and strong in-house engineering enable multisourcing and reduce single-vendor risk. Long-term partnerships trade price for reliability and access to joint innovation, supporting asset uptime and cost predictability.

Hydrocarbon and feedstock sourcing

Hydrogen, syngas and CO2 largely come from natural gas/refinery off‑gases; commodity inputs limit supplier power but pipeline bottlenecks and regional gas price spikes (Henry Hub ~ $2.8/MMBtu in 2024) can raise local leverage. Indexed supply contracts align feedstock and product pricing; on‑site SMRs and vertical integration cut third‑party exposure.

- Commodity input: lowers supplier power

- Infrastructure: creates localized leverage

- Indexed contracts: price alignment

- Vertical integration: reduces exposure

Logistics and industrial services

- Specialized transport reliance

- ATA driver shortfall ~80,000 (2023) impacting 2024 capacity

- Linde owned fleet reduces supplier leverage

- Bottlenecks in surges/regulatory changes

Helium squeeze: concentrated producers, <10 OEMs and logistics drive volatility

Supplier power is elevated by concentrated helium sources, limited OEMs (<10) for cryogenic equipment, and logistics bottlenecks (US driver shortfall ~80,000 in 2023 impacting 2024). Energy exposure (US $0.07–0.09/kWh; EU €0.12–0.18/kWh) and regional gas moves (Henry Hub ≈ $2.8/MMBtu) add volatility; Linde offsets via long‑term contracts, vertical integration and owned fleet.

| Metric | 2024 |

|---|---|

| Helium concentration | Few geographies/producers |

| OEM pool | <10 firms |

| Electricity | US $0.07–0.09/kWh; EU €0.12–0.18/kWh |

| Henry Hub | $2.8/MMBtu |

| Driver shortfall | ~80,000 (2023) |

What is included in the product

Concise Porter's Five Forces analysis of Linde, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal key pressures on margins, market share, and strategic positioning within the industrial gases and engineering sectors.

One-sheet Porter's Five Forces tailored for Linde—quickly highlights supplier, buyer, rivalry, new entrant, and substitute pressures so teams can prioritize strategic moves and reduce decision paralysis.

Customers Bargaining Power

Large industrial customers with scale

Steel, chemical and refining customers buy very high volumes and run competitive tenders, enabling significant price concessions and bespoke commercial terms. Their scale drives negotiating leverage, but take-or-pay provisions and indexation to feedstock or CPI limit renegotiation frequency. Multi-year on-site contracts, often 10+ years, lock in supply and materially reduce churn despite initial buyer leverage.

High switching costs from embedded supply

Pipelines, on-site plants and strict customer qualifications make switching disruptive and costly; on-site contracts commonly exceed 5 years, often tying customers into bespoke infrastructure. Reliability and safety track records thus outweigh small price deltas, shrinking ongoing buyer leverage. This structural stickiness reduces customer bargaining power once contracts are in place and lengthens renewal cycles in Linde’s favor.

Fragmented mid/small buyers in healthcare and food

Fragmented mid/small buyers in healthcare and food limit bargaining power because numerous smaller accounts are less able to negotiate bespoke pricing; Linde reported roughly $39.4 billion in 2023 sales, highlighting scale advantages. Packaged and specialty gases command higher margins and service components, reinforcing supplier leverage. Strict delivery, compliance and purity needs lower buyer mobility, though volume-aggregation platforms can modestly increase leverage by pooling demand.

Cyclicality and price sensitivity

Cyclicality raises buyer pushback on price and volumes during industrial downturns, forcing Linde to lean on index-linked clauses and surcharges to protect margins, though these mechanisms often lag spot cost movements. In expansion phases, customers prioritize uptime and delivery speed, reducing price sensitivity as urgency outweighs marginal cost. Quarterly shifts in demand mix between merchant, bulk and project volumes can materially swing bargaining leverage.

- Index-linked pricing: preserves economics but lags

- Downturns: stronger buyer negotiation on price/volumes

- Expansions: uptime reduces price sensitivity

- Quarterly demand-mix swings alter leverage

Technical differentiation and service bundling

Application engineering, digital monitoring and guaranteed uptime (often 99.9% service SLAs) create switching friction—buyers prioritize process optimization and safety over commodity molecules, and bundled solutions dilute pure price comparisons, softening buyer power where performance guarantees are critical.

- Application engineering: increases lock‑in

- Digital monitoring: reduces downtime, improves ROI

- 99.9% uptime SLAs: shifts focus from price to reliability

- Bundled services: mask unit‑price comparisons

Buyers have upfront leverage, but multi-year index-linked contracts and 99.9% SLAs curb it

Linde customers have strong upfront bargaining power via large tenders and volume, but multi‑year on‑site contracts (commonly 5–10+ years), index‑linked pricing and high switching costs materially reduce ongoing leverage; reliability, SLAs (≈99.9%) and bundled services shift negotiations toward service terms. Linde reported $39.4 billion sales in 2023 and maintained margin resilience through indexation in 2024.

| Metric | Value |

|---|---|

| Typical contract length | 5–10+ yrs |

| 2023 sales | $39.4B |

| Service SLA | ≈99.9% |

Preview the Actual Deliverable

Linde Porter's Five Forces Analysis

This preview shows the exact Linde Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.