LKQ SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

LKQ’s SWOT snapshot reveals strengths in scale and aftermarket reach, offset by supply-chain exposure and cyclicality; growth hinges on parts diversification and digital channels. Want the full strategic picture with executable recommendations? Purchase the complete SWOT for a professionally formatted, editable report and Excel matrix to support investment, planning, and pitching.

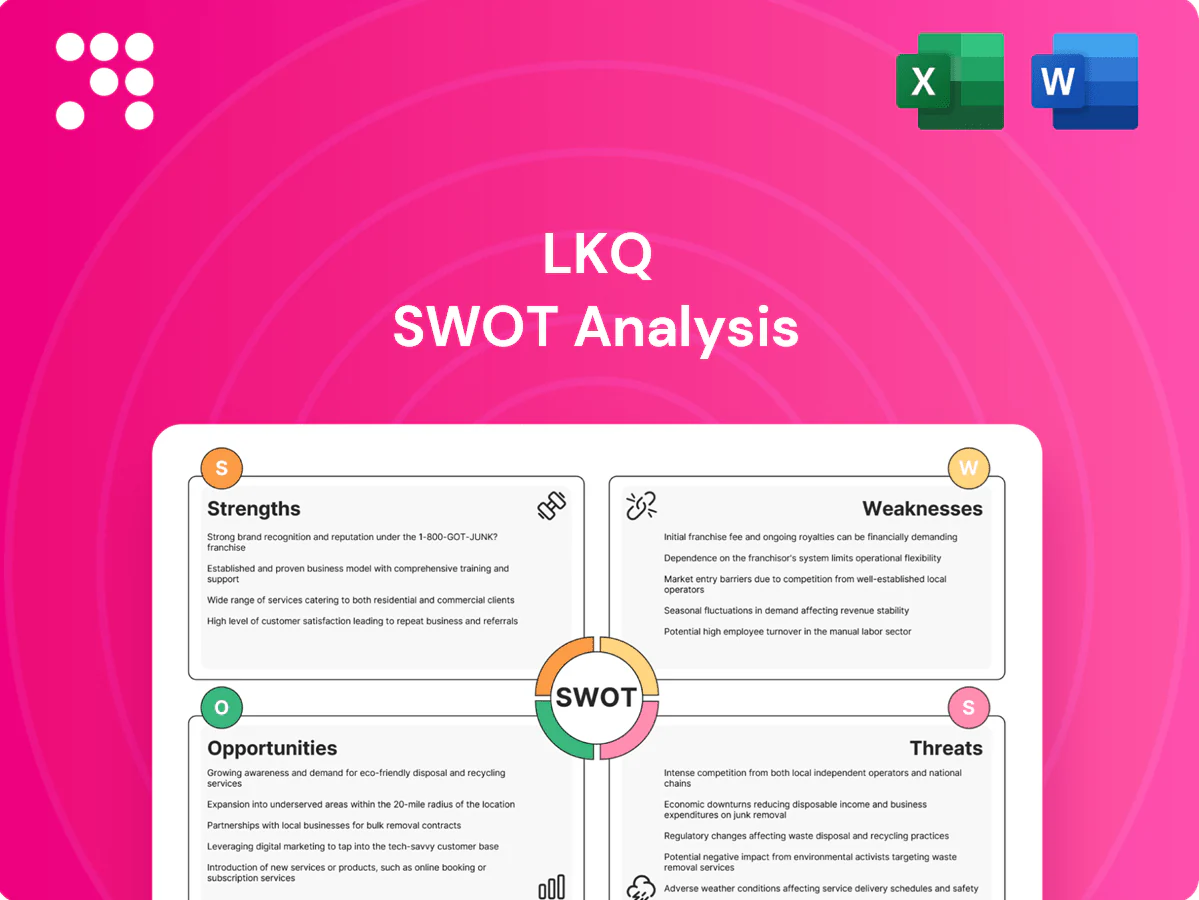

Strengths

Global distribution scale

LKQ’s global distribution scale—with over 1,000 locations across North America and Europe—lets it reach tens of thousands of collision and mechanical shops with fast, often next‑day delivery, cutting per‑unit logistics and procurement costs. Broad geographic coverage diversifies demand across regions, and this footprint and buying power are difficult for smaller rivals to replicate.

Diversified parts portfolio

LKQ offers recycled OEM, aftermarket, specialty, and remanufactured mechanical parts, meeting varied price and quality preferences and reducing reliance on any single category. This portfolio breadth enables cross-selling into adjacent repair jobs and buffers revenue when specific categories cycle; LKQ reported roughly $13.3 billion in revenue in FY2024, underpinning scale and inventory depth.

Cost-advantaged value proposition

Alternative parts typically undercut OEM prices by 20–30% while meeting repair standards, a value that helped LKQ—which reported about $12.7 billion revenue in 2024—win business from insurers, fleets and cost-conscious consumers. This value positioning supports share gains in collision and mechanical channels and contributed to its ability to defend margins, with adjusted operating margins remaining in the low double digits.

Sourcing and salvage expertise

LKQ's decades of vehicle procurement, dismantling and remanufacturing experience drives consistent yield and quality; proprietary processes lift parts recovery rates and inventory turn. Reliable core supply from a salvage network supporting over 1,000 facilities across North America and Europe underpinned roughly 14 billion USD revenue in 2024, keeping availability for high-volume models. This operational know-how creates a durable competitive moat.

- Experience: high-yield sourcing and remanufacturing

- Proprietary processes: improved recovery and turn

- Core supply: reliable availability for popular models

Operational data and logistics

LKQ leverages advanced cataloging, fitment data and inventory analytics to boost fill rates and reduce stockouts; these capabilities supported company net sales of about $14.1 billion in FY2024. Route-density planning and hub-and-spoke logistics cut delivery times, while digital ordering tools streamline shop workflows and raise retention, cumulatively increasing customer switching costs.

- Advanced fitment and analytics: higher fill rates

- Route density + hubs: faster deliveries

- Digital ordering: improved retention

- Higher switching costs: stronger customer stickiness

Global parts network: 1,000+ locations, $14.1B sales and low-double-digit margins

LKQ’s >1,000 global locations and hub‑and‑spoke logistics enable fast, high‑fill distribution and strong route density advantages. Diverse parts mix—recycled OEM, aftermarket, remanufactured—supports cross‑selling and resilience. Scale drove FY2024 net sales of $14.1B and adjusted operating margins in the low double digits, underpinning a durable cost and supply moat.

| Metric | Value | FY |

|---|---|---|

| Global locations | >1,000 | 2024 |

| Net sales | $14.1B | 2024 |

| Adj. operating margin | Low double digits | 2024 |

What is included in the product

Provides a strategic SWOT overview of LKQ, outlining internal strengths and weaknesses and external opportunities and threats shaping its position in automotive parts distribution, aftermarket services, and related growth markets.

Delivers a concise SWOT matrix tailored to LKQ for rapid strategic alignment and risk mitigation. Editable format enables quick updates to reflect supply-chain shifts and changing market dynamics.

Weaknesses

Integration complexity

LKQs history of 100+ acquisitions creates systems harmonization and cultural challenges after rapid consolidation. Disparate IT and processes elevate operating costs and error rates, eroding margins and raising integration spend. Integration delays have historically muted expected synergies, and this risk is amplified by cross-border operations spanning multiple regulatory regimes.

Margin exposure to mix

Aftermarket and recycled parts are increasingly price-competitive and commoditizing, pressuring LKQ’s mix; in 2024 LKQ reported about $11.2 billion in revenue with gross margin near 29%, exposing earnings to mix shifts. Movement into lower-margin categories compresses profitability and can swing operating margins by several hundred basis points. Managing core costs and scrap values adds volatility, so sustaining differentiation requires continuous process and service improvements.

Regulatory and compliance burden

Handling salvage vehicles and hazardous components exposes LKQ to strict environmental rules such as the EU End-of-Life Vehicles Directive requiring 95% reuse/recycling by weight and differing standards across 27 EU member states. Non-compliance can trigger multimillion-dollar fines, business interruptions, and reputational harm. Varied jurisdictional rules complicate logistics and inventory flows, and compliance investments can compress operating leverage and margins.

Perception vs OEM parts

Inventory complexity and obsolescence

Inventory complexity across thousands of SKUs for multiple makes, models and vintages raises carrying costs and pressure on working capital; LKQ held about $3.9 billion in inventory at year-end 2023, heightening exposure to slow-moving stock. Forecast errors produce obsolescence; EV and ADAS component evolution shortens part lifecycles and increases risk to margins, requiring tighter inventory controls to protect cash.

- High SKU breadth → elevated carrying costs

- Forecast errors → slow/obsolete stock

- EV/ADAS → accelerated lifecycle risk

- Tight control needed to protect cash & margins

100+ M&A deals fragment IT, raising integration costs; $11.6B, $3.9B inventory

Rapid M&A (100+ deals) drives IT/process fragmentation, higher integration costs and delayed synergies across jurisdictions. Commoditizing aftermarket mix pressures margins—LKQ reported about $11.6 billion revenue in 2024 with gross margin near 29%, while inventory complexity (inventory $3.9B at YE2023) raises working capital and obsolescence risk, amplified by EV/ADAS part churn.

| Metric | Value | Impact |

|---|---|---|

| Deals | 100+ | Integration burden |

| Revenue (2024) | $11.6B | Mix-sensitive margins |

| Inventory (YE2023) | $3.9B | Working capital/obsolescence |

Preview the Actual Deliverable

LKQ SWOT Analysis

This is the actual SWOT analysis document for LKQ you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy to unlock the complete, editable file with in-depth strengths, weaknesses, opportunities and threats.

Dive Deeper Into the Company’s Strategic Blueprint

LKQ’s SWOT snapshot reveals strengths in scale and aftermarket reach, offset by supply-chain exposure and cyclicality; growth hinges on parts diversification and digital channels. Want the full strategic picture with executable recommendations? Purchase the complete SWOT for a professionally formatted, editable report and Excel matrix to support investment, planning, and pitching.

Strengths

Global distribution scale

LKQ’s global distribution scale—with over 1,000 locations across North America and Europe—lets it reach tens of thousands of collision and mechanical shops with fast, often next‑day delivery, cutting per‑unit logistics and procurement costs. Broad geographic coverage diversifies demand across regions, and this footprint and buying power are difficult for smaller rivals to replicate.

Diversified parts portfolio

LKQ offers recycled OEM, aftermarket, specialty, and remanufactured mechanical parts, meeting varied price and quality preferences and reducing reliance on any single category. This portfolio breadth enables cross-selling into adjacent repair jobs and buffers revenue when specific categories cycle; LKQ reported roughly $13.3 billion in revenue in FY2024, underpinning scale and inventory depth.

Cost-advantaged value proposition

Alternative parts typically undercut OEM prices by 20–30% while meeting repair standards, a value that helped LKQ—which reported about $12.7 billion revenue in 2024—win business from insurers, fleets and cost-conscious consumers. This value positioning supports share gains in collision and mechanical channels and contributed to its ability to defend margins, with adjusted operating margins remaining in the low double digits.

Sourcing and salvage expertise

LKQ's decades of vehicle procurement, dismantling and remanufacturing experience drives consistent yield and quality; proprietary processes lift parts recovery rates and inventory turn. Reliable core supply from a salvage network supporting over 1,000 facilities across North America and Europe underpinned roughly 14 billion USD revenue in 2024, keeping availability for high-volume models. This operational know-how creates a durable competitive moat.

- Experience: high-yield sourcing and remanufacturing

- Proprietary processes: improved recovery and turn

- Core supply: reliable availability for popular models

Operational data and logistics

LKQ leverages advanced cataloging, fitment data and inventory analytics to boost fill rates and reduce stockouts; these capabilities supported company net sales of about $14.1 billion in FY2024. Route-density planning and hub-and-spoke logistics cut delivery times, while digital ordering tools streamline shop workflows and raise retention, cumulatively increasing customer switching costs.

- Advanced fitment and analytics: higher fill rates

- Route density + hubs: faster deliveries

- Digital ordering: improved retention

- Higher switching costs: stronger customer stickiness

Global parts network: 1,000+ locations, $14.1B sales and low-double-digit margins

LKQ’s >1,000 global locations and hub‑and‑spoke logistics enable fast, high‑fill distribution and strong route density advantages. Diverse parts mix—recycled OEM, aftermarket, remanufactured—supports cross‑selling and resilience. Scale drove FY2024 net sales of $14.1B and adjusted operating margins in the low double digits, underpinning a durable cost and supply moat.

| Metric | Value | FY |

|---|---|---|

| Global locations | >1,000 | 2024 |

| Net sales | $14.1B | 2024 |

| Adj. operating margin | Low double digits | 2024 |

What is included in the product

Provides a strategic SWOT overview of LKQ, outlining internal strengths and weaknesses and external opportunities and threats shaping its position in automotive parts distribution, aftermarket services, and related growth markets.

Delivers a concise SWOT matrix tailored to LKQ for rapid strategic alignment and risk mitigation. Editable format enables quick updates to reflect supply-chain shifts and changing market dynamics.

Weaknesses

Integration complexity

LKQs history of 100+ acquisitions creates systems harmonization and cultural challenges after rapid consolidation. Disparate IT and processes elevate operating costs and error rates, eroding margins and raising integration spend. Integration delays have historically muted expected synergies, and this risk is amplified by cross-border operations spanning multiple regulatory regimes.

Margin exposure to mix

Aftermarket and recycled parts are increasingly price-competitive and commoditizing, pressuring LKQ’s mix; in 2024 LKQ reported about $11.2 billion in revenue with gross margin near 29%, exposing earnings to mix shifts. Movement into lower-margin categories compresses profitability and can swing operating margins by several hundred basis points. Managing core costs and scrap values adds volatility, so sustaining differentiation requires continuous process and service improvements.

Regulatory and compliance burden

Handling salvage vehicles and hazardous components exposes LKQ to strict environmental rules such as the EU End-of-Life Vehicles Directive requiring 95% reuse/recycling by weight and differing standards across 27 EU member states. Non-compliance can trigger multimillion-dollar fines, business interruptions, and reputational harm. Varied jurisdictional rules complicate logistics and inventory flows, and compliance investments can compress operating leverage and margins.

Perception vs OEM parts

Inventory complexity and obsolescence

Inventory complexity across thousands of SKUs for multiple makes, models and vintages raises carrying costs and pressure on working capital; LKQ held about $3.9 billion in inventory at year-end 2023, heightening exposure to slow-moving stock. Forecast errors produce obsolescence; EV and ADAS component evolution shortens part lifecycles and increases risk to margins, requiring tighter inventory controls to protect cash.

- High SKU breadth → elevated carrying costs

- Forecast errors → slow/obsolete stock

- EV/ADAS → accelerated lifecycle risk

- Tight control needed to protect cash & margins

100+ M&A deals fragment IT, raising integration costs; $11.6B, $3.9B inventory

Rapid M&A (100+ deals) drives IT/process fragmentation, higher integration costs and delayed synergies across jurisdictions. Commoditizing aftermarket mix pressures margins—LKQ reported about $11.6 billion revenue in 2024 with gross margin near 29%, while inventory complexity (inventory $3.9B at YE2023) raises working capital and obsolescence risk, amplified by EV/ADAS part churn.

| Metric | Value | Impact |

|---|---|---|

| Deals | 100+ | Integration burden |

| Revenue (2024) | $11.6B | Mix-sensitive margins |

| Inventory (YE2023) | $3.9B | Working capital/obsolescence |

Preview the Actual Deliverable

LKQ SWOT Analysis

This is the actual SWOT analysis document for LKQ you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy to unlock the complete, editable file with in-depth strengths, weaknesses, opportunities and threats.

Description

Dive Deeper Into the Company’s Strategic Blueprint

LKQ’s SWOT snapshot reveals strengths in scale and aftermarket reach, offset by supply-chain exposure and cyclicality; growth hinges on parts diversification and digital channels. Want the full strategic picture with executable recommendations? Purchase the complete SWOT for a professionally formatted, editable report and Excel matrix to support investment, planning, and pitching.

Strengths

Global distribution scale

LKQ’s global distribution scale—with over 1,000 locations across North America and Europe—lets it reach tens of thousands of collision and mechanical shops with fast, often next‑day delivery, cutting per‑unit logistics and procurement costs. Broad geographic coverage diversifies demand across regions, and this footprint and buying power are difficult for smaller rivals to replicate.

Diversified parts portfolio

LKQ offers recycled OEM, aftermarket, specialty, and remanufactured mechanical parts, meeting varied price and quality preferences and reducing reliance on any single category. This portfolio breadth enables cross-selling into adjacent repair jobs and buffers revenue when specific categories cycle; LKQ reported roughly $13.3 billion in revenue in FY2024, underpinning scale and inventory depth.

Cost-advantaged value proposition

Alternative parts typically undercut OEM prices by 20–30% while meeting repair standards, a value that helped LKQ—which reported about $12.7 billion revenue in 2024—win business from insurers, fleets and cost-conscious consumers. This value positioning supports share gains in collision and mechanical channels and contributed to its ability to defend margins, with adjusted operating margins remaining in the low double digits.

Sourcing and salvage expertise

LKQ's decades of vehicle procurement, dismantling and remanufacturing experience drives consistent yield and quality; proprietary processes lift parts recovery rates and inventory turn. Reliable core supply from a salvage network supporting over 1,000 facilities across North America and Europe underpinned roughly 14 billion USD revenue in 2024, keeping availability for high-volume models. This operational know-how creates a durable competitive moat.

- Experience: high-yield sourcing and remanufacturing

- Proprietary processes: improved recovery and turn

- Core supply: reliable availability for popular models

Operational data and logistics

LKQ leverages advanced cataloging, fitment data and inventory analytics to boost fill rates and reduce stockouts; these capabilities supported company net sales of about $14.1 billion in FY2024. Route-density planning and hub-and-spoke logistics cut delivery times, while digital ordering tools streamline shop workflows and raise retention, cumulatively increasing customer switching costs.

- Advanced fitment and analytics: higher fill rates

- Route density + hubs: faster deliveries

- Digital ordering: improved retention

- Higher switching costs: stronger customer stickiness

Global parts network: 1,000+ locations, $14.1B sales and low-double-digit margins

LKQ’s >1,000 global locations and hub‑and‑spoke logistics enable fast, high‑fill distribution and strong route density advantages. Diverse parts mix—recycled OEM, aftermarket, remanufactured—supports cross‑selling and resilience. Scale drove FY2024 net sales of $14.1B and adjusted operating margins in the low double digits, underpinning a durable cost and supply moat.

| Metric | Value | FY |

|---|---|---|

| Global locations | >1,000 | 2024 |

| Net sales | $14.1B | 2024 |

| Adj. operating margin | Low double digits | 2024 |

What is included in the product

Provides a strategic SWOT overview of LKQ, outlining internal strengths and weaknesses and external opportunities and threats shaping its position in automotive parts distribution, aftermarket services, and related growth markets.

Delivers a concise SWOT matrix tailored to LKQ for rapid strategic alignment and risk mitigation. Editable format enables quick updates to reflect supply-chain shifts and changing market dynamics.

Weaknesses

Integration complexity

LKQs history of 100+ acquisitions creates systems harmonization and cultural challenges after rapid consolidation. Disparate IT and processes elevate operating costs and error rates, eroding margins and raising integration spend. Integration delays have historically muted expected synergies, and this risk is amplified by cross-border operations spanning multiple regulatory regimes.

Margin exposure to mix

Aftermarket and recycled parts are increasingly price-competitive and commoditizing, pressuring LKQ’s mix; in 2024 LKQ reported about $11.2 billion in revenue with gross margin near 29%, exposing earnings to mix shifts. Movement into lower-margin categories compresses profitability and can swing operating margins by several hundred basis points. Managing core costs and scrap values adds volatility, so sustaining differentiation requires continuous process and service improvements.

Regulatory and compliance burden

Handling salvage vehicles and hazardous components exposes LKQ to strict environmental rules such as the EU End-of-Life Vehicles Directive requiring 95% reuse/recycling by weight and differing standards across 27 EU member states. Non-compliance can trigger multimillion-dollar fines, business interruptions, and reputational harm. Varied jurisdictional rules complicate logistics and inventory flows, and compliance investments can compress operating leverage and margins.

Perception vs OEM parts

Inventory complexity and obsolescence

Inventory complexity across thousands of SKUs for multiple makes, models and vintages raises carrying costs and pressure on working capital; LKQ held about $3.9 billion in inventory at year-end 2023, heightening exposure to slow-moving stock. Forecast errors produce obsolescence; EV and ADAS component evolution shortens part lifecycles and increases risk to margins, requiring tighter inventory controls to protect cash.

- High SKU breadth → elevated carrying costs

- Forecast errors → slow/obsolete stock

- EV/ADAS → accelerated lifecycle risk

- Tight control needed to protect cash & margins

100+ M&A deals fragment IT, raising integration costs; $11.6B, $3.9B inventory

Rapid M&A (100+ deals) drives IT/process fragmentation, higher integration costs and delayed synergies across jurisdictions. Commoditizing aftermarket mix pressures margins—LKQ reported about $11.6 billion revenue in 2024 with gross margin near 29%, while inventory complexity (inventory $3.9B at YE2023) raises working capital and obsolescence risk, amplified by EV/ADAS part churn.

| Metric | Value | Impact |

|---|---|---|

| Deals | 100+ | Integration burden |

| Revenue (2024) | $11.6B | Mix-sensitive margins |

| Inventory (YE2023) | $3.9B | Working capital/obsolescence |

Preview the Actual Deliverable

LKQ SWOT Analysis

This is the actual SWOT analysis document for LKQ you'll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Buy to unlock the complete, editable file with in-depth strengths, weaknesses, opportunities and threats.