loanDepot SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

loanDepot faces scale and digital distribution strengths but contends with rate sensitivity, regulatory scrutiny, and intense competition; growth hinges on tech integration and credit cycle navigation. Want the full strategic picture and editable report? Purchase the complete SWOT analysis for in-depth findings, financial context, and actionable recommendations.

Strengths

Omnichannel distribution

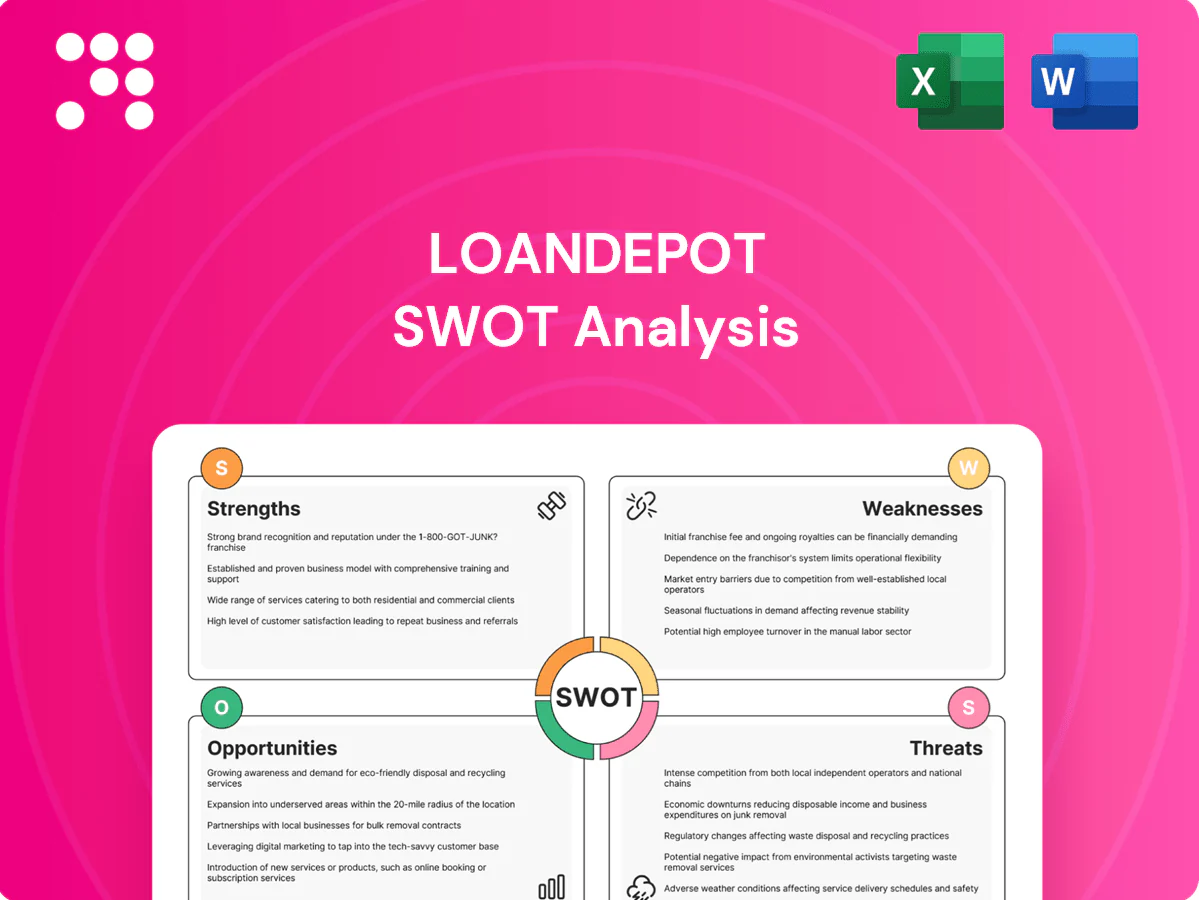

loanDepot combines a strong digital platform with a retail footprint of over 300 branches and nationwide coverage across all 50 states, improving lead capture and conversion. This mix expands geographic reach and supports both self-serve borrowers and high-touch consultative sales. The omnichannel model enabled lower per-loan costs when online origination scales, giving flexibility to shift toward cheaper digital channels as volumes tighten.

Broad product lineup

loanDepot offers purchase, refinance and HELOC products, allowing it to serve multiple borrower needs and smooth originations through rate cycles. That product breadth enables cross-sell and improves retention as customers move from purchase to tapping equity. Diversification reduces dependence on any single revenue stream and supports steadier fee and interest income across market shifts.

Brand and marketing scale

National consumer brand recognition—loanDepot was a top-5 nonbank mortgage originator in 2023—supports efficient customer acquisition, lowering per-lead costs and raising conversion. Scaled marketing and partnerships with agents and builders sustain steady purchase funnels and recurring pipelines. Brand trust improves pull-through and referral rates, helping compete with both banks and fintech lenders.

Technology-enabled origination

Technology-enabled origination at loanDepot leverages a digital application, automation, and data integrations to reduce friction and cycle times, lowering per-loan fulfillment costs while improving customer experience. Enhanced data and workflow tools strengthen underwriting quality and consistency. The platform foundation supports rapid product and pricing updates to respond to market moves.

- Digital application and automation

- Lower per-loan fulfillment cost

- Improved underwriting quality

- Fast product/pricing agility

Secondary market access

Secondary market access allows loanDepot to sell loans into agencies and private investors, supporting liquidity and capital recycling; balanced gain-on-sale versus servicing economics improves margin capture while retaining servicing rights; strong investor relationships expand take-out options across product types and help mitigate balance sheet risk during volume swings.

- Supports liquidity via agency/investor sales

- Optimizes economics: gain-on-sale vs servicing

- Broader take-out options across products

- Reduces balance-sheet exposure in volume shifts

Digital lender: 300+ branches, 50 states, Top-5

loanDepot combines a strong digital platform with 300+ branches and coverage in all 50 states, boosting lead capture and conversion.

Product breadth (purchase, refinance, HELOC) smooths originations across cycles and supports cross-sell and retention.

Top-5 nonbank originator in 2023 with agency/private investor access, enabling liquidity and optimized gain-on-sale economics.

| Metric | Value |

|---|---|

| Branches | 300+ |

| Geographic | 50 states |

| Market Rank | Top-5 nonbank (2023) |

What is included in the product

Delivers a strategic overview of loanDepot’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping the company's future.

Delivers a concise SWOT matrix tailored to loanDepot for rapid identification of risks and opportunities, easing strategic alignment and quick decision-making across lending, technology, and regulatory teams.

Weaknesses

Rate-cycle sensitivity

loanDepot faces sharp rate-cycle sensitivity: U.S. mortgage originations plunged about 67% from the 2021 peak (~$4.3T) to roughly $1.4T in 2023 (MBA), making revenue unpredictable as volumes swing. Refi-driven booms can abruptly flip to purchase-only markets, whipsawing margins. Staffing and fixed cost structures often lag demand shifts, compressing margins and reducing planning visibility.

Higher funding costs

Lacking low-cost deposits, loanDepot depends on warehouse lines and capital markets for funding, exposing it to rising cost of funds as liquidity tightens; the Fed funds target near 5.25–5.50% in 2024–25 amplified market borrowing costs. This reduces pricing flexibility versus depository competitors and can compress margins. During stress, higher funding costs can limit originations and capacity.

Margin pressure in commoditized pricing

Rate and fee transparency drives intense price competition, pressuring margins and contributing to loanDepot's April 2024 Chapter 11 restructuring. Large peers and broker platforms can undercut pricing at scale, forcing concessions. Low consumer switching costs elevate churn and pricing pressure. Sustaining unit economics requires relentless cost discipline and efficiency gains to avoid repeat distress.

Operational complexity

Managing both digital platforms and a nationwide retail network (over 200 branches) creates process variation across channels; maintaining consistent workflows and quality control at scale has strained operations. Holding licenses in all 50 states increases compliance overhead and reporting complexity. Large platform upgrades have previously disrupted origination workflows when sequencing and change management lagged.

- Channel variation: online vs 200+ branches

- Compliance: licensed in 50 states

- Quality control: scale-related inconsistency

- Technology: upgrades risk workflow disruption

Regulatory burden

Nonbank mortgage lenders like loanDepot operate under rigorous federal and state oversight, and ongoing rule changes increase compliance costs and force frequent operational adjustments. Examinations and enforcement actions—CFPB and state authorities have stepped up oversight in recent years—create measurable financial and reputational risk. Complex disclosure and fair-lending requirements raise execution risk across origination and servicing.

- Regulatory scope: multiple federal and state agencies

- Compliance cost growth: ongoing rule changes

- Enforcement risk: examinations can trigger fines or restrictions

- Execution risk: complex disclosure and fair-lending rules

Rate-sensitive mortgage lender: 67% originations drop, Chapter 11

loanDepot is highly rate-sensitive—U.S. originations fell ~67% from ~$4.3T (2021) to ~$1.4T (2023), making revenue volatile; April 2024 Chapter 11 underscored liquidity strain. Funding relies on warehouse/markets, exposed to Fed funds ~5.25–5.50% (2024–25) and higher costs vs depositories. Large retail footprint (200+ branches) and 50-state licensing raise ops and compliance costs.

| Metric | Value |

|---|---|

| Originations change | -67% |

| 2023 originations | $1.4T |

| Branches | 200+ |

Full Version Awaits

loanDepot SWOT Analysis

This is the actual loanDepot SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities and threats clearly outlined. Purchase unlocks the complete, editable file so you can use it immediately.

Elevate Your Analysis with the Complete SWOT Report

loanDepot faces scale and digital distribution strengths but contends with rate sensitivity, regulatory scrutiny, and intense competition; growth hinges on tech integration and credit cycle navigation. Want the full strategic picture and editable report? Purchase the complete SWOT analysis for in-depth findings, financial context, and actionable recommendations.

Strengths

Omnichannel distribution

loanDepot combines a strong digital platform with a retail footprint of over 300 branches and nationwide coverage across all 50 states, improving lead capture and conversion. This mix expands geographic reach and supports both self-serve borrowers and high-touch consultative sales. The omnichannel model enabled lower per-loan costs when online origination scales, giving flexibility to shift toward cheaper digital channels as volumes tighten.

Broad product lineup

loanDepot offers purchase, refinance and HELOC products, allowing it to serve multiple borrower needs and smooth originations through rate cycles. That product breadth enables cross-sell and improves retention as customers move from purchase to tapping equity. Diversification reduces dependence on any single revenue stream and supports steadier fee and interest income across market shifts.

Brand and marketing scale

National consumer brand recognition—loanDepot was a top-5 nonbank mortgage originator in 2023—supports efficient customer acquisition, lowering per-lead costs and raising conversion. Scaled marketing and partnerships with agents and builders sustain steady purchase funnels and recurring pipelines. Brand trust improves pull-through and referral rates, helping compete with both banks and fintech lenders.

Technology-enabled origination

Technology-enabled origination at loanDepot leverages a digital application, automation, and data integrations to reduce friction and cycle times, lowering per-loan fulfillment costs while improving customer experience. Enhanced data and workflow tools strengthen underwriting quality and consistency. The platform foundation supports rapid product and pricing updates to respond to market moves.

- Digital application and automation

- Lower per-loan fulfillment cost

- Improved underwriting quality

- Fast product/pricing agility

Secondary market access

Secondary market access allows loanDepot to sell loans into agencies and private investors, supporting liquidity and capital recycling; balanced gain-on-sale versus servicing economics improves margin capture while retaining servicing rights; strong investor relationships expand take-out options across product types and help mitigate balance sheet risk during volume swings.

- Supports liquidity via agency/investor sales

- Optimizes economics: gain-on-sale vs servicing

- Broader take-out options across products

- Reduces balance-sheet exposure in volume shifts

Digital lender: 300+ branches, 50 states, Top-5

loanDepot combines a strong digital platform with 300+ branches and coverage in all 50 states, boosting lead capture and conversion.

Product breadth (purchase, refinance, HELOC) smooths originations across cycles and supports cross-sell and retention.

Top-5 nonbank originator in 2023 with agency/private investor access, enabling liquidity and optimized gain-on-sale economics.

| Metric | Value |

|---|---|

| Branches | 300+ |

| Geographic | 50 states |

| Market Rank | Top-5 nonbank (2023) |

What is included in the product

Delivers a strategic overview of loanDepot’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping the company's future.

Delivers a concise SWOT matrix tailored to loanDepot for rapid identification of risks and opportunities, easing strategic alignment and quick decision-making across lending, technology, and regulatory teams.

Weaknesses

Rate-cycle sensitivity

loanDepot faces sharp rate-cycle sensitivity: U.S. mortgage originations plunged about 67% from the 2021 peak (~$4.3T) to roughly $1.4T in 2023 (MBA), making revenue unpredictable as volumes swing. Refi-driven booms can abruptly flip to purchase-only markets, whipsawing margins. Staffing and fixed cost structures often lag demand shifts, compressing margins and reducing planning visibility.

Higher funding costs

Lacking low-cost deposits, loanDepot depends on warehouse lines and capital markets for funding, exposing it to rising cost of funds as liquidity tightens; the Fed funds target near 5.25–5.50% in 2024–25 amplified market borrowing costs. This reduces pricing flexibility versus depository competitors and can compress margins. During stress, higher funding costs can limit originations and capacity.

Margin pressure in commoditized pricing

Rate and fee transparency drives intense price competition, pressuring margins and contributing to loanDepot's April 2024 Chapter 11 restructuring. Large peers and broker platforms can undercut pricing at scale, forcing concessions. Low consumer switching costs elevate churn and pricing pressure. Sustaining unit economics requires relentless cost discipline and efficiency gains to avoid repeat distress.

Operational complexity

Managing both digital platforms and a nationwide retail network (over 200 branches) creates process variation across channels; maintaining consistent workflows and quality control at scale has strained operations. Holding licenses in all 50 states increases compliance overhead and reporting complexity. Large platform upgrades have previously disrupted origination workflows when sequencing and change management lagged.

- Channel variation: online vs 200+ branches

- Compliance: licensed in 50 states

- Quality control: scale-related inconsistency

- Technology: upgrades risk workflow disruption

Regulatory burden

Nonbank mortgage lenders like loanDepot operate under rigorous federal and state oversight, and ongoing rule changes increase compliance costs and force frequent operational adjustments. Examinations and enforcement actions—CFPB and state authorities have stepped up oversight in recent years—create measurable financial and reputational risk. Complex disclosure and fair-lending requirements raise execution risk across origination and servicing.

- Regulatory scope: multiple federal and state agencies

- Compliance cost growth: ongoing rule changes

- Enforcement risk: examinations can trigger fines or restrictions

- Execution risk: complex disclosure and fair-lending rules

Rate-sensitive mortgage lender: 67% originations drop, Chapter 11

loanDepot is highly rate-sensitive—U.S. originations fell ~67% from ~$4.3T (2021) to ~$1.4T (2023), making revenue volatile; April 2024 Chapter 11 underscored liquidity strain. Funding relies on warehouse/markets, exposed to Fed funds ~5.25–5.50% (2024–25) and higher costs vs depositories. Large retail footprint (200+ branches) and 50-state licensing raise ops and compliance costs.

| Metric | Value |

|---|---|

| Originations change | -67% |

| 2023 originations | $1.4T |

| Branches | 200+ |

Full Version Awaits

loanDepot SWOT Analysis

This is the actual loanDepot SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities and threats clearly outlined. Purchase unlocks the complete, editable file so you can use it immediately.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

loanDepot faces scale and digital distribution strengths but contends with rate sensitivity, regulatory scrutiny, and intense competition; growth hinges on tech integration and credit cycle navigation. Want the full strategic picture and editable report? Purchase the complete SWOT analysis for in-depth findings, financial context, and actionable recommendations.

Strengths

Omnichannel distribution

loanDepot combines a strong digital platform with a retail footprint of over 300 branches and nationwide coverage across all 50 states, improving lead capture and conversion. This mix expands geographic reach and supports both self-serve borrowers and high-touch consultative sales. The omnichannel model enabled lower per-loan costs when online origination scales, giving flexibility to shift toward cheaper digital channels as volumes tighten.

Broad product lineup

loanDepot offers purchase, refinance and HELOC products, allowing it to serve multiple borrower needs and smooth originations through rate cycles. That product breadth enables cross-sell and improves retention as customers move from purchase to tapping equity. Diversification reduces dependence on any single revenue stream and supports steadier fee and interest income across market shifts.

Brand and marketing scale

National consumer brand recognition—loanDepot was a top-5 nonbank mortgage originator in 2023—supports efficient customer acquisition, lowering per-lead costs and raising conversion. Scaled marketing and partnerships with agents and builders sustain steady purchase funnels and recurring pipelines. Brand trust improves pull-through and referral rates, helping compete with both banks and fintech lenders.

Technology-enabled origination

Technology-enabled origination at loanDepot leverages a digital application, automation, and data integrations to reduce friction and cycle times, lowering per-loan fulfillment costs while improving customer experience. Enhanced data and workflow tools strengthen underwriting quality and consistency. The platform foundation supports rapid product and pricing updates to respond to market moves.

- Digital application and automation

- Lower per-loan fulfillment cost

- Improved underwriting quality

- Fast product/pricing agility

Secondary market access

Secondary market access allows loanDepot to sell loans into agencies and private investors, supporting liquidity and capital recycling; balanced gain-on-sale versus servicing economics improves margin capture while retaining servicing rights; strong investor relationships expand take-out options across product types and help mitigate balance sheet risk during volume swings.

- Supports liquidity via agency/investor sales

- Optimizes economics: gain-on-sale vs servicing

- Broader take-out options across products

- Reduces balance-sheet exposure in volume shifts

Digital lender: 300+ branches, 50 states, Top-5

loanDepot combines a strong digital platform with 300+ branches and coverage in all 50 states, boosting lead capture and conversion.

Product breadth (purchase, refinance, HELOC) smooths originations across cycles and supports cross-sell and retention.

Top-5 nonbank originator in 2023 with agency/private investor access, enabling liquidity and optimized gain-on-sale economics.

| Metric | Value |

|---|---|

| Branches | 300+ |

| Geographic | 50 states |

| Market Rank | Top-5 nonbank (2023) |

What is included in the product

Delivers a strategic overview of loanDepot’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, key growth drivers, operational gaps and market risks shaping the company's future.

Delivers a concise SWOT matrix tailored to loanDepot for rapid identification of risks and opportunities, easing strategic alignment and quick decision-making across lending, technology, and regulatory teams.

Weaknesses

Rate-cycle sensitivity

loanDepot faces sharp rate-cycle sensitivity: U.S. mortgage originations plunged about 67% from the 2021 peak (~$4.3T) to roughly $1.4T in 2023 (MBA), making revenue unpredictable as volumes swing. Refi-driven booms can abruptly flip to purchase-only markets, whipsawing margins. Staffing and fixed cost structures often lag demand shifts, compressing margins and reducing planning visibility.

Higher funding costs

Lacking low-cost deposits, loanDepot depends on warehouse lines and capital markets for funding, exposing it to rising cost of funds as liquidity tightens; the Fed funds target near 5.25–5.50% in 2024–25 amplified market borrowing costs. This reduces pricing flexibility versus depository competitors and can compress margins. During stress, higher funding costs can limit originations and capacity.

Margin pressure in commoditized pricing

Rate and fee transparency drives intense price competition, pressuring margins and contributing to loanDepot's April 2024 Chapter 11 restructuring. Large peers and broker platforms can undercut pricing at scale, forcing concessions. Low consumer switching costs elevate churn and pricing pressure. Sustaining unit economics requires relentless cost discipline and efficiency gains to avoid repeat distress.

Operational complexity

Managing both digital platforms and a nationwide retail network (over 200 branches) creates process variation across channels; maintaining consistent workflows and quality control at scale has strained operations. Holding licenses in all 50 states increases compliance overhead and reporting complexity. Large platform upgrades have previously disrupted origination workflows when sequencing and change management lagged.

- Channel variation: online vs 200+ branches

- Compliance: licensed in 50 states

- Quality control: scale-related inconsistency

- Technology: upgrades risk workflow disruption

Regulatory burden

Nonbank mortgage lenders like loanDepot operate under rigorous federal and state oversight, and ongoing rule changes increase compliance costs and force frequent operational adjustments. Examinations and enforcement actions—CFPB and state authorities have stepped up oversight in recent years—create measurable financial and reputational risk. Complex disclosure and fair-lending requirements raise execution risk across origination and servicing.

- Regulatory scope: multiple federal and state agencies

- Compliance cost growth: ongoing rule changes

- Enforcement risk: examinations can trigger fines or restrictions

- Execution risk: complex disclosure and fair-lending rules

Rate-sensitive mortgage lender: 67% originations drop, Chapter 11

loanDepot is highly rate-sensitive—U.S. originations fell ~67% from ~$4.3T (2021) to ~$1.4T (2023), making revenue volatile; April 2024 Chapter 11 underscored liquidity strain. Funding relies on warehouse/markets, exposed to Fed funds ~5.25–5.50% (2024–25) and higher costs vs depositories. Large retail footprint (200+ branches) and 50-state licensing raise ops and compliance costs.

| Metric | Value |

|---|---|

| Originations change | -67% |

| 2023 originations | $1.4T |

| Branches | 200+ |

Full Version Awaits

loanDepot SWOT Analysis

This is the actual loanDepot SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, with strengths, weaknesses, opportunities and threats clearly outlined. Purchase unlocks the complete, editable file so you can use it immediately.