World Acceptance Business Model Canvas

Download the Business Model Canvas — strategic blueprint for investors

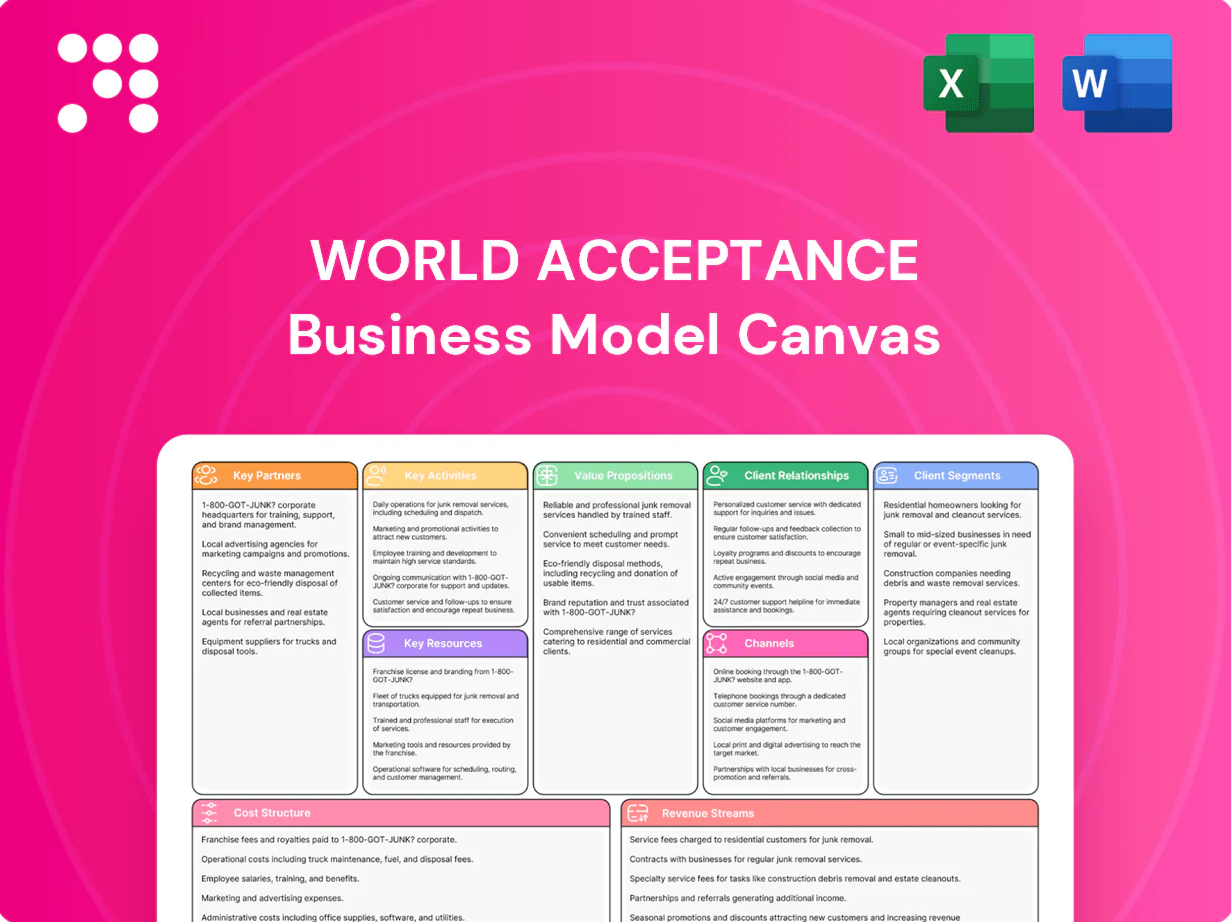

Unlock the full strategic blueprint behind World Acceptance’s Business Model Canvas in one concise download. This in-depth canvas maps value propositions, customer segments, key partners and revenue drivers to reveal how the company scales and mitigates risk. Perfect for investors, consultants and founders—purchase the full editable Word/Excel file to dive deep.

Partnerships

Credit bureaus

Partnerships with major credit bureaus allow World Acceptance to pull credit files and report payment behavior for over 200 million U.S. consumers, supporting tighter underwriting and continuous portfolio monitoring. On-time reporting feeds credit histories and matters for score calculation—payment history comprises 35% of a FICO score—helping customers build or repair credit. Data reciprocity across bureaus reduces fraud and sharpens risk calibration for pricing and collections.

Insurance carriers

Alliances with insurance carriers supply credit-related insurance bundled with World Acceptance loans, with carriers managing risk pooling and claims while World Acceptance distributes policies at point of sale. Commission structures create non-interest revenue streams for World Acceptance, enhancing fee income. Carriers and World Acceptance align on compliance, disclosures and suitability to meet regulatory obligations.

Payment processors

Third-party processors enable ACH, debit card and digital wallet collections, with ACH costs typically under $1 per transaction versus card fees of 1.5–3.5%, and provide settlement, reconciliation and chargeback handling. Reliable rails cut cash-handling risks and reduce delinquency friction, while APIs support automated reminders, autopay and flexible schedules. Autopay adoption often lifts on-time payments by roughly 15–25%, improving cash flow predictability.

Tax prep partners

Tax prep partners provide seasonal support to World Acceptance, leveraging external software to streamline intake, e-file and refund timelines; 2024 IRS e-file volumes exceeded 150 million returns, underscoring scale during Jan–Apr. Integrations enable faster underwriting and cross-sell offers during peak tax season, while partner tooling enforces IRS and state compliance checks. Partnerships boost customer acquisition and operational efficiency in high-volume months.

Regulators & community orgs

Engagement with state regulators and consumer groups secures licensing and policy compliance, aligning World Acceptance with evolving rules while FDIC/Community Reinvestment signals (FDIC 2023 Household Survey: 4.5% unbanked, ~5.4M households) guide outreach strategies. Community partners extend reach into underbanked segments and their feedback refines responsible lending, lowering default and reputational risk and advancing financial inclusion.

- Regulatory alignment: licensing, reduced enforcement risk

- Community outreach: access to ~5.4M unbanked households

- Feedback loop: improves responsible lending practices

- Outcome: stronger reputation and greater financial inclusion

Partners boost underwriting, lift autopay ~20% and expand credit to 200M+ consumers

Key partners — credit bureaus, insurers, payment processors, tax-prep vendors and community/regulatory bodies — enable underwriting, non-interest revenue, low-cost collections and seasonal acquisition, lifting autopay payments ~20% and leveraging credit files for ~200M U.S. consumers. Partnerships reduce fraud, cut costs and expand access to ~5.4M unbanked households.

| Partner | Metric |

|---|---|

| Credit bureaus | 200M consumers |

| Autopay uplift | ~15–25% |

| IRS e-file (2024) | ≈150M returns |

| Unbanked (FDIC 2023) | 4.5% ≈5.4M |

What is included in the product

A concise, pre-written Business Model Canvas for World Acceptance detailing customer segments, value propositions, channels, revenue streams and cost structure aligned to its consumer finance strategy. Ideal for investors and analysts, it includes competitive analysis, SWOT-linked insights and actionable validation using real company operations.

Condenses World Acceptance’s customer-centric loan and collections strategy into a digestible one-page Business Model Canvas, quickly identifying pain points in underwriting, distribution, and compliance for fast decision-making and team collaboration.

Activities

Underwriting

Underwriting uses credit bureau scores, documented income and affordability checks to quantify risk, with policy rules tuned to balance approval rates against loss targets; fraud screening and ID verification are embedded into workflows, and continuous model tuning—accelerated in 2024—improves predictiveness and reduces losses through ongoing calibration and backtesting.

Loan servicing

Loan servicing covers disbursement, payment scheduling, and account maintenance for thousands of installment loans, with same-day posting and bureau reporting typically within 24–48 hours. Autopay setup, rescheduling, and payoff processing target 60–70% autopay enrollment to lower delinquencies. Customer support manages hardship requests and short-term extensions via phone and digital channels. Accurate posting and structured reporting feed credit bureaus and management dashboards.

Collections

Collections deploy early-stage reminders and cure strategies to minimize roll rates, with segmented late-stage workflows and recoveries focused on prioritized accounts. Outreach is data-driven across phone (industry contact rates ~12%), SMS (open rates ~98%), and in-person channels. Operations strictly follow FDCPA and TCPA rules, with FDCPA statutory damages up to 1,000. Recovery segmentation targets maximize yield per account class.

Compliance & risk

Compliance & risk ensures adherence to state lending caps, required disclosures, UDAAP and insurance rules, supported by monitoring, periodic audits and recurring staff training. Complaint handling, QA testing, model governance and fair lending reviews mitigate regulatory and reputational exposures. Controls feed reporting to senior management and the board.

- Adherence: state caps, disclosures, insurance, UDAAP

- Oversight: monitoring, audits, model governance

- Operations: staff training, complaint handling, QA testing

- Reviews: fair lending and senior reporting

Branch ops & sales

Branch ops & sales drive in-branch origination and relationship management through face-to-face underwriting, onboarding, and regular account reviews to reduce delinquency and boost lifetime value.

Teams run community outreach and local marketing, maintain strict cash handling and layered security controls, and cross-sell insurance and tax-prep services where regulation and customer need align.

- In-branch origination

- Community outreach

- Cash & security controls

- Cross-selling insurance/tax prep

Fast underwriting & same-day servicing with 60-70% autopay

Underwriting uses bureau scores, documented income and accelerated 2024 model tuning to balance approvals and losses; fraud screening and ID verification are embedded. Servicing handles same-day posting with bureau reporting in 24–48 hours, targeting 60–70% autopay to lower delinquencies. Collections use segmented outreach (phone contact ~12%, SMS open ~98%) within FDCPA/TCPA limits (FDCPA statutory damages up to 1,000).

| Metric | Value |

|---|---|

| Autopay target | 60–70% |

| Phone contact rate | ~12% |

| SMS open rate | ~98% |

| Bureau reporting | 24–48 hours |

| FDCPA damages | 1,000 |

Preview Before You Purchase

Business Model Canvas

The World Acceptance Business Model Canvas previewed here is the actual deliverable, not a mockup. It contains the same content, layout, and structure you will receive after purchase. Upon ordering, you’ll download this exact, editable document ready for use.

Download the Business Model Canvas — strategic blueprint for investors

Unlock the full strategic blueprint behind World Acceptance’s Business Model Canvas in one concise download. This in-depth canvas maps value propositions, customer segments, key partners and revenue drivers to reveal how the company scales and mitigates risk. Perfect for investors, consultants and founders—purchase the full editable Word/Excel file to dive deep.

Partnerships

Credit bureaus

Partnerships with major credit bureaus allow World Acceptance to pull credit files and report payment behavior for over 200 million U.S. consumers, supporting tighter underwriting and continuous portfolio monitoring. On-time reporting feeds credit histories and matters for score calculation—payment history comprises 35% of a FICO score—helping customers build or repair credit. Data reciprocity across bureaus reduces fraud and sharpens risk calibration for pricing and collections.

Insurance carriers

Alliances with insurance carriers supply credit-related insurance bundled with World Acceptance loans, with carriers managing risk pooling and claims while World Acceptance distributes policies at point of sale. Commission structures create non-interest revenue streams for World Acceptance, enhancing fee income. Carriers and World Acceptance align on compliance, disclosures and suitability to meet regulatory obligations.

Payment processors

Third-party processors enable ACH, debit card and digital wallet collections, with ACH costs typically under $1 per transaction versus card fees of 1.5–3.5%, and provide settlement, reconciliation and chargeback handling. Reliable rails cut cash-handling risks and reduce delinquency friction, while APIs support automated reminders, autopay and flexible schedules. Autopay adoption often lifts on-time payments by roughly 15–25%, improving cash flow predictability.

Tax prep partners

Tax prep partners provide seasonal support to World Acceptance, leveraging external software to streamline intake, e-file and refund timelines; 2024 IRS e-file volumes exceeded 150 million returns, underscoring scale during Jan–Apr. Integrations enable faster underwriting and cross-sell offers during peak tax season, while partner tooling enforces IRS and state compliance checks. Partnerships boost customer acquisition and operational efficiency in high-volume months.

Regulators & community orgs

Engagement with state regulators and consumer groups secures licensing and policy compliance, aligning World Acceptance with evolving rules while FDIC/Community Reinvestment signals (FDIC 2023 Household Survey: 4.5% unbanked, ~5.4M households) guide outreach strategies. Community partners extend reach into underbanked segments and their feedback refines responsible lending, lowering default and reputational risk and advancing financial inclusion.

- Regulatory alignment: licensing, reduced enforcement risk

- Community outreach: access to ~5.4M unbanked households

- Feedback loop: improves responsible lending practices

- Outcome: stronger reputation and greater financial inclusion

Partners boost underwriting, lift autopay ~20% and expand credit to 200M+ consumers

Key partners — credit bureaus, insurers, payment processors, tax-prep vendors and community/regulatory bodies — enable underwriting, non-interest revenue, low-cost collections and seasonal acquisition, lifting autopay payments ~20% and leveraging credit files for ~200M U.S. consumers. Partnerships reduce fraud, cut costs and expand access to ~5.4M unbanked households.

| Partner | Metric |

|---|---|

| Credit bureaus | 200M consumers |

| Autopay uplift | ~15–25% |

| IRS e-file (2024) | ≈150M returns |

| Unbanked (FDIC 2023) | 4.5% ≈5.4M |

What is included in the product

A concise, pre-written Business Model Canvas for World Acceptance detailing customer segments, value propositions, channels, revenue streams and cost structure aligned to its consumer finance strategy. Ideal for investors and analysts, it includes competitive analysis, SWOT-linked insights and actionable validation using real company operations.

Condenses World Acceptance’s customer-centric loan and collections strategy into a digestible one-page Business Model Canvas, quickly identifying pain points in underwriting, distribution, and compliance for fast decision-making and team collaboration.

Activities

Underwriting

Underwriting uses credit bureau scores, documented income and affordability checks to quantify risk, with policy rules tuned to balance approval rates against loss targets; fraud screening and ID verification are embedded into workflows, and continuous model tuning—accelerated in 2024—improves predictiveness and reduces losses through ongoing calibration and backtesting.

Loan servicing

Loan servicing covers disbursement, payment scheduling, and account maintenance for thousands of installment loans, with same-day posting and bureau reporting typically within 24–48 hours. Autopay setup, rescheduling, and payoff processing target 60–70% autopay enrollment to lower delinquencies. Customer support manages hardship requests and short-term extensions via phone and digital channels. Accurate posting and structured reporting feed credit bureaus and management dashboards.

Collections

Collections deploy early-stage reminders and cure strategies to minimize roll rates, with segmented late-stage workflows and recoveries focused on prioritized accounts. Outreach is data-driven across phone (industry contact rates ~12%), SMS (open rates ~98%), and in-person channels. Operations strictly follow FDCPA and TCPA rules, with FDCPA statutory damages up to 1,000. Recovery segmentation targets maximize yield per account class.

Compliance & risk

Compliance & risk ensures adherence to state lending caps, required disclosures, UDAAP and insurance rules, supported by monitoring, periodic audits and recurring staff training. Complaint handling, QA testing, model governance and fair lending reviews mitigate regulatory and reputational exposures. Controls feed reporting to senior management and the board.

- Adherence: state caps, disclosures, insurance, UDAAP

- Oversight: monitoring, audits, model governance

- Operations: staff training, complaint handling, QA testing

- Reviews: fair lending and senior reporting

Branch ops & sales

Branch ops & sales drive in-branch origination and relationship management through face-to-face underwriting, onboarding, and regular account reviews to reduce delinquency and boost lifetime value.

Teams run community outreach and local marketing, maintain strict cash handling and layered security controls, and cross-sell insurance and tax-prep services where regulation and customer need align.

- In-branch origination

- Community outreach

- Cash & security controls

- Cross-selling insurance/tax prep

Fast underwriting & same-day servicing with 60-70% autopay

Underwriting uses bureau scores, documented income and accelerated 2024 model tuning to balance approvals and losses; fraud screening and ID verification are embedded. Servicing handles same-day posting with bureau reporting in 24–48 hours, targeting 60–70% autopay to lower delinquencies. Collections use segmented outreach (phone contact ~12%, SMS open ~98%) within FDCPA/TCPA limits (FDCPA statutory damages up to 1,000).

| Metric | Value |

|---|---|

| Autopay target | 60–70% |

| Phone contact rate | ~12% |

| SMS open rate | ~98% |

| Bureau reporting | 24–48 hours |

| FDCPA damages | 1,000 |

Preview Before You Purchase

Business Model Canvas

The World Acceptance Business Model Canvas previewed here is the actual deliverable, not a mockup. It contains the same content, layout, and structure you will receive after purchase. Upon ordering, you’ll download this exact, editable document ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Download the Business Model Canvas — strategic blueprint for investors

Unlock the full strategic blueprint behind World Acceptance’s Business Model Canvas in one concise download. This in-depth canvas maps value propositions, customer segments, key partners and revenue drivers to reveal how the company scales and mitigates risk. Perfect for investors, consultants and founders—purchase the full editable Word/Excel file to dive deep.

Partnerships

Credit bureaus

Partnerships with major credit bureaus allow World Acceptance to pull credit files and report payment behavior for over 200 million U.S. consumers, supporting tighter underwriting and continuous portfolio monitoring. On-time reporting feeds credit histories and matters for score calculation—payment history comprises 35% of a FICO score—helping customers build or repair credit. Data reciprocity across bureaus reduces fraud and sharpens risk calibration for pricing and collections.

Insurance carriers

Alliances with insurance carriers supply credit-related insurance bundled with World Acceptance loans, with carriers managing risk pooling and claims while World Acceptance distributes policies at point of sale. Commission structures create non-interest revenue streams for World Acceptance, enhancing fee income. Carriers and World Acceptance align on compliance, disclosures and suitability to meet regulatory obligations.

Payment processors

Third-party processors enable ACH, debit card and digital wallet collections, with ACH costs typically under $1 per transaction versus card fees of 1.5–3.5%, and provide settlement, reconciliation and chargeback handling. Reliable rails cut cash-handling risks and reduce delinquency friction, while APIs support automated reminders, autopay and flexible schedules. Autopay adoption often lifts on-time payments by roughly 15–25%, improving cash flow predictability.

Tax prep partners

Tax prep partners provide seasonal support to World Acceptance, leveraging external software to streamline intake, e-file and refund timelines; 2024 IRS e-file volumes exceeded 150 million returns, underscoring scale during Jan–Apr. Integrations enable faster underwriting and cross-sell offers during peak tax season, while partner tooling enforces IRS and state compliance checks. Partnerships boost customer acquisition and operational efficiency in high-volume months.

Regulators & community orgs

Engagement with state regulators and consumer groups secures licensing and policy compliance, aligning World Acceptance with evolving rules while FDIC/Community Reinvestment signals (FDIC 2023 Household Survey: 4.5% unbanked, ~5.4M households) guide outreach strategies. Community partners extend reach into underbanked segments and their feedback refines responsible lending, lowering default and reputational risk and advancing financial inclusion.

- Regulatory alignment: licensing, reduced enforcement risk

- Community outreach: access to ~5.4M unbanked households

- Feedback loop: improves responsible lending practices

- Outcome: stronger reputation and greater financial inclusion

Partners boost underwriting, lift autopay ~20% and expand credit to 200M+ consumers

Key partners — credit bureaus, insurers, payment processors, tax-prep vendors and community/regulatory bodies — enable underwriting, non-interest revenue, low-cost collections and seasonal acquisition, lifting autopay payments ~20% and leveraging credit files for ~200M U.S. consumers. Partnerships reduce fraud, cut costs and expand access to ~5.4M unbanked households.

| Partner | Metric |

|---|---|

| Credit bureaus | 200M consumers |

| Autopay uplift | ~15–25% |

| IRS e-file (2024) | ≈150M returns |

| Unbanked (FDIC 2023) | 4.5% ≈5.4M |

What is included in the product

A concise, pre-written Business Model Canvas for World Acceptance detailing customer segments, value propositions, channels, revenue streams and cost structure aligned to its consumer finance strategy. Ideal for investors and analysts, it includes competitive analysis, SWOT-linked insights and actionable validation using real company operations.

Condenses World Acceptance’s customer-centric loan and collections strategy into a digestible one-page Business Model Canvas, quickly identifying pain points in underwriting, distribution, and compliance for fast decision-making and team collaboration.

Activities

Underwriting

Underwriting uses credit bureau scores, documented income and affordability checks to quantify risk, with policy rules tuned to balance approval rates against loss targets; fraud screening and ID verification are embedded into workflows, and continuous model tuning—accelerated in 2024—improves predictiveness and reduces losses through ongoing calibration and backtesting.

Loan servicing

Loan servicing covers disbursement, payment scheduling, and account maintenance for thousands of installment loans, with same-day posting and bureau reporting typically within 24–48 hours. Autopay setup, rescheduling, and payoff processing target 60–70% autopay enrollment to lower delinquencies. Customer support manages hardship requests and short-term extensions via phone and digital channels. Accurate posting and structured reporting feed credit bureaus and management dashboards.

Collections

Collections deploy early-stage reminders and cure strategies to minimize roll rates, with segmented late-stage workflows and recoveries focused on prioritized accounts. Outreach is data-driven across phone (industry contact rates ~12%), SMS (open rates ~98%), and in-person channels. Operations strictly follow FDCPA and TCPA rules, with FDCPA statutory damages up to 1,000. Recovery segmentation targets maximize yield per account class.

Compliance & risk

Compliance & risk ensures adherence to state lending caps, required disclosures, UDAAP and insurance rules, supported by monitoring, periodic audits and recurring staff training. Complaint handling, QA testing, model governance and fair lending reviews mitigate regulatory and reputational exposures. Controls feed reporting to senior management and the board.

- Adherence: state caps, disclosures, insurance, UDAAP

- Oversight: monitoring, audits, model governance

- Operations: staff training, complaint handling, QA testing

- Reviews: fair lending and senior reporting

Branch ops & sales

Branch ops & sales drive in-branch origination and relationship management through face-to-face underwriting, onboarding, and regular account reviews to reduce delinquency and boost lifetime value.

Teams run community outreach and local marketing, maintain strict cash handling and layered security controls, and cross-sell insurance and tax-prep services where regulation and customer need align.

- In-branch origination

- Community outreach

- Cash & security controls

- Cross-selling insurance/tax prep

Fast underwriting & same-day servicing with 60-70% autopay

Underwriting uses bureau scores, documented income and accelerated 2024 model tuning to balance approvals and losses; fraud screening and ID verification are embedded. Servicing handles same-day posting with bureau reporting in 24–48 hours, targeting 60–70% autopay to lower delinquencies. Collections use segmented outreach (phone contact ~12%, SMS open ~98%) within FDCPA/TCPA limits (FDCPA statutory damages up to 1,000).

| Metric | Value |

|---|---|

| Autopay target | 60–70% |

| Phone contact rate | ~12% |

| SMS open rate | ~98% |

| Bureau reporting | 24–48 hours |

| FDCPA damages | 1,000 |

Preview Before You Purchase

Business Model Canvas

The World Acceptance Business Model Canvas previewed here is the actual deliverable, not a mockup. It contains the same content, layout, and structure you will receive after purchase. Upon ordering, you’ll download this exact, editable document ready for use.