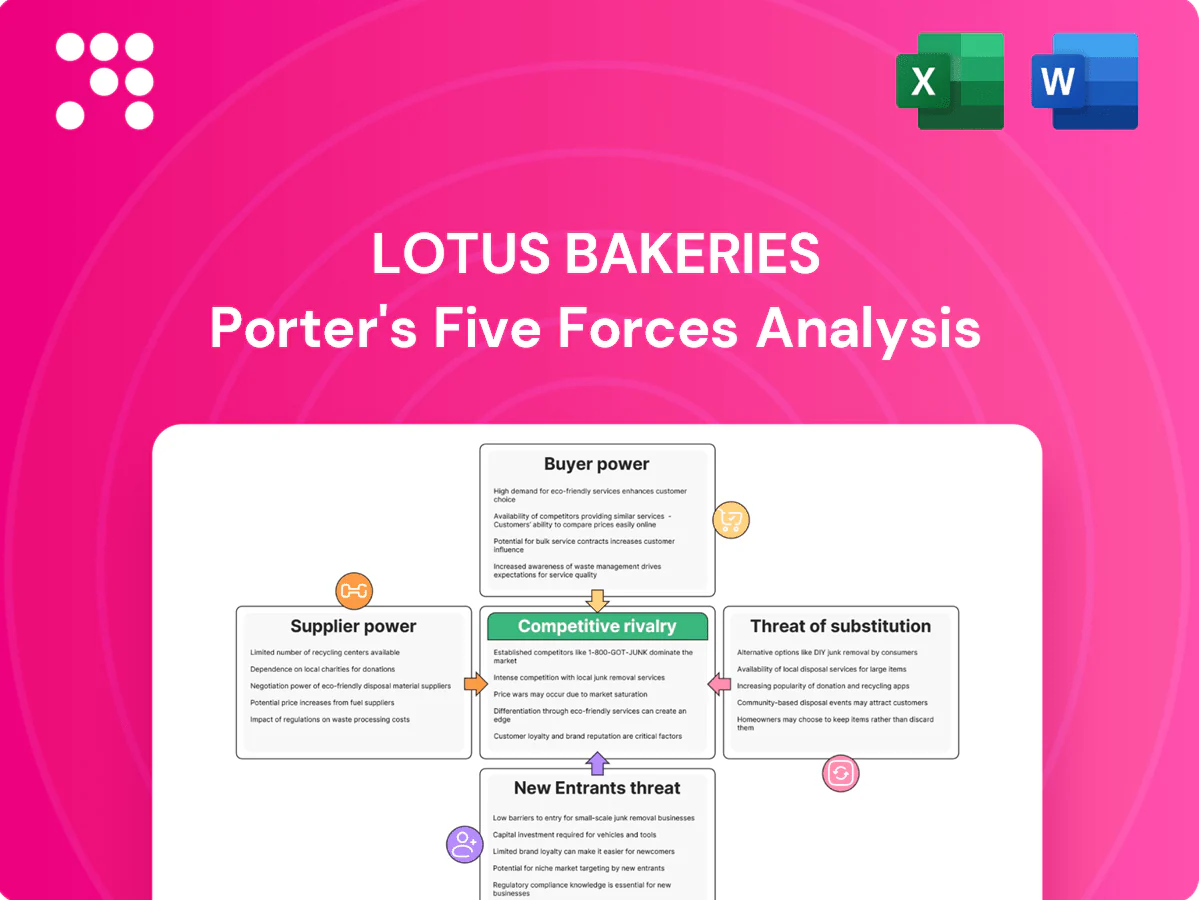

Lotus Bakeries Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Lotus Bakeries faces moderate supplier power but strong buyer expectations, intense rivalry among branded bakery players, moderate threat of new entrants due to brand and scale, and growing substitute pressure from healthier snacks. The analysis highlights how brand equity and innovation buffer risks yet expose margin pressures. This brief overview teases force-by-force implications. Unlock the full Porter's Five Forces Analysis to explore Lotus Bakeries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Broad commodity input base

Lotus sources wheat, sugar, oils and spices from a fragmented global market with hundreds of suppliers, limiting individual leverage; in 2024 Lotus reported group net sales of €1.49bn, supporting scale purchasing. Multiple qualified suppliers and dual-sourcing enable competitive bidding and lower costs. Standardized specs and global commodity contracts reduce switching costs, keeping baseline supplier power moderate.

Quality and specialty specs

Signature taste depends on specific spice blends and consistent flour profiles, narrowing acceptable supplier pools and raising qualification barriers; Biscoff is sold in over 50 markets, so any taste drift risks broad brand equity. Qualification and audit requirements increase switching friction, giving select suppliers marginal leverage. Rigorous QA systems and periodic sensory testing partially offset supplier power.

Sustainability certifications

Sustainability certifications narrow supplier options: by 2024 RSPO-certified palm oil made up about 20% of global supply and certified cocoa programs covered roughly 35–40% of trade, while demand for traceable packaging rose double digits, tightening availability. Compliance premiums can lift input costs when certified supply is tight, yet Lotus uses long-term contracts and supplier development to dampen volatility and accept some pricing power from certified suppliers as ESG is strategic.

Packaging and logistics dependencies

Specialized packaging lines for Lotus Bakeries require specific film and carton specs, concentrating spend with a limited set of suppliers and raising switching costs; freight and port bottlenecks plus cold-chain needs for some SKUs can constrain inbound/outbound flows. Diversified 3PL partners and regional hubs reduce single-point risk, though in tight markets logistics providers can gain temporary bargaining leverage, driving spot-cost volatility.

- Concentrated supplier base increases switching costs

- Freight, cold-chain and port limits constrain flows

- 3PL diversification and regional hubs mitigate disruption

- Logistics providers can gain short-term pricing power in tight markets

Commodity and energy volatility

Agricultural cycles and energy-price swings drive input-cost volatility for Lotus Bakeries, creating episodic upward pressure on sugar, wheat and oil-based ingredients; hedging and forward contracts reduce but do not eliminate spikes. Large procurement volumes and multi-regional sourcing give Lotus scale and negotiation leverage, keeping supplier power generally contained despite occasional episodic pressure.

- Volatility: episodic supplier leverage

- Risk mitigation: hedging/forwards limit spikes

- Scale advantage: stronger negotiation

- Net: contained but not eliminated exposure

Moderate supplier power: €1.49bn scale vs certified palm ~20%, cocoa 35–40%

Lotus faces moderate supplier power: fragmented ingredient markets and €1.49bn 2024 sales provide scale, but specialty spices, certified inputs and packaging specs increase leverage. RSPO palm ~20% and certified cocoa ~35–40% narrow pools and can raise costs. Hedging, long-term contracts and multi-sourcing limit but do not eliminate episodic supplier pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Group net sales | €1.49bn | Purchasing scale |

| RSPO palm | ~20% | Supply constraint/premium |

| Certified cocoa | 35–40% | Limited qualified suppliers |

What is included in the product

Concise Porter's Five Forces review of Lotus Bakeries, evaluating competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlighting disruptive trends and strategic implications for pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Lotus Bakeries—perfect for quick decision-making and identifying where competitive pressure hurts margins. Swap in your own data or scenario tabs to model impacts (new entrants, supplier shifts, or regulation) without macros—ready for pitch decks or boardroom slides.

Customers Bargaining Power

Retailer concentration vs brand pull

Large grocers and discounters negotiate hard on price, promotions and shelf fees, leveraging concentrated buying power in key European markets where top chains often control c.60% of grocery sales. Lotus Biscoff’s distinctive taste and low substitutability, sold in 50+ countries and widely used on airlines, preserves niche loyalty. Strong brand equity secures premium placement and mitigates concession pressure. Overall buyer power is balanced by steady consumer demand.

Private label pressure

Retailers push own‑label speculoos and cookies to widen margins and anchor price points, forcing promotional activity; private label penetration in many European categories reached roughly 30–40% by 2023. Lotus Bakeries, with group turnover of EUR 1,174.9m in 2023, defends margin via taste, consistency and marketing investment, so private label raises buyer leverage but does not erase Lotus’ brand premium.

D2C and e-commerce

Lotus Bakeries’ company webshops and presence on marketplaces reduce dependence on traditional retailers by enabling direct sales and richer first-party data for targeting and merchandising, improving gross margin capture versus wholesale channels. Direct channels give control over assortment and pricing, but the bulk of volume and shelf prominence is still controlled by large brick-and-mortar chains. E-commerce growth moderates buyer power but does not fully neutralize the negotiating leverage of major retailers.

Global customer diversification

Global customer diversification reduces reliance on any single buyer, as Lotus Bakeries expanded channel and regional reach by 2024. New market entries shifted the mix toward growth partners, weakening individual buyer leverage. Localized assortments sustain shelf relevance across markets.

- Regional reach reduces single-buyer exposure

- New markets increase growth-partner share

- Diversification lowers buyer bargaining power

- Localized SKUs protect shelf presence

Premium positioning, elasticity

Premium indulgence and distinct flavor lower price sensitivity versus mainstream cookies, sustaining margins; 2023 group turnover was €1.206bn. Euro-area inflation in 2024 (approx. 2.9%) can still test willingness-to-pay. Targeted pack sizes and tactical promotions manage elasticity, while buyer power increases in downturns but stays manageable for Lotus.

- Premium positioning: lower elasticity

- 2023 turnover: €1.206bn

- 2024 inflation (~2.9%) pressures WTP

- Packs/promos mitigate demand shifts

Grocer leverage, private labels 30-40% and turnover €1.206bn vs. 2.9% inflation

Large European grocers (top chains ~60% share) and private‑label penetration (30–40% in 2023) keep buyer leverage, pressuring price and promotions. Lotus’ strong Biscoff brand, €1.206bn turnover (2023) and growing direct e‑commerce reduce retailer dependence, but brick‑and‑mortar still drives volumes; 2024 euro‑area inflation ~2.9% tests willingness‑to‑pay.

| Metric | Value |

|---|---|

| 2023 turnover | €1.206bn |

| Top chains market share | ~60% |

| Private label (2023) | 30–40% |

| Euro‑area inflation (2024) | ~2.9% |

Preview Before You Purchase

Lotus Bakeries Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Lotus Bakeries you’ll receive immediately after purchase—no placeholders. The document is fully formatted, actionable and download‑ready. It provides tailored assessments of supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes.

A Must-Have Tool for Decision-Makers

Lotus Bakeries faces moderate supplier power but strong buyer expectations, intense rivalry among branded bakery players, moderate threat of new entrants due to brand and scale, and growing substitute pressure from healthier snacks. The analysis highlights how brand equity and innovation buffer risks yet expose margin pressures. This brief overview teases force-by-force implications. Unlock the full Porter's Five Forces Analysis to explore Lotus Bakeries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Broad commodity input base

Lotus sources wheat, sugar, oils and spices from a fragmented global market with hundreds of suppliers, limiting individual leverage; in 2024 Lotus reported group net sales of €1.49bn, supporting scale purchasing. Multiple qualified suppliers and dual-sourcing enable competitive bidding and lower costs. Standardized specs and global commodity contracts reduce switching costs, keeping baseline supplier power moderate.

Quality and specialty specs

Signature taste depends on specific spice blends and consistent flour profiles, narrowing acceptable supplier pools and raising qualification barriers; Biscoff is sold in over 50 markets, so any taste drift risks broad brand equity. Qualification and audit requirements increase switching friction, giving select suppliers marginal leverage. Rigorous QA systems and periodic sensory testing partially offset supplier power.

Sustainability certifications

Sustainability certifications narrow supplier options: by 2024 RSPO-certified palm oil made up about 20% of global supply and certified cocoa programs covered roughly 35–40% of trade, while demand for traceable packaging rose double digits, tightening availability. Compliance premiums can lift input costs when certified supply is tight, yet Lotus uses long-term contracts and supplier development to dampen volatility and accept some pricing power from certified suppliers as ESG is strategic.

Packaging and logistics dependencies

Specialized packaging lines for Lotus Bakeries require specific film and carton specs, concentrating spend with a limited set of suppliers and raising switching costs; freight and port bottlenecks plus cold-chain needs for some SKUs can constrain inbound/outbound flows. Diversified 3PL partners and regional hubs reduce single-point risk, though in tight markets logistics providers can gain temporary bargaining leverage, driving spot-cost volatility.

- Concentrated supplier base increases switching costs

- Freight, cold-chain and port limits constrain flows

- 3PL diversification and regional hubs mitigate disruption

- Logistics providers can gain short-term pricing power in tight markets

Commodity and energy volatility

Agricultural cycles and energy-price swings drive input-cost volatility for Lotus Bakeries, creating episodic upward pressure on sugar, wheat and oil-based ingredients; hedging and forward contracts reduce but do not eliminate spikes. Large procurement volumes and multi-regional sourcing give Lotus scale and negotiation leverage, keeping supplier power generally contained despite occasional episodic pressure.

- Volatility: episodic supplier leverage

- Risk mitigation: hedging/forwards limit spikes

- Scale advantage: stronger negotiation

- Net: contained but not eliminated exposure

Moderate supplier power: €1.49bn scale vs certified palm ~20%, cocoa 35–40%

Lotus faces moderate supplier power: fragmented ingredient markets and €1.49bn 2024 sales provide scale, but specialty spices, certified inputs and packaging specs increase leverage. RSPO palm ~20% and certified cocoa ~35–40% narrow pools and can raise costs. Hedging, long-term contracts and multi-sourcing limit but do not eliminate episodic supplier pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Group net sales | €1.49bn | Purchasing scale |

| RSPO palm | ~20% | Supply constraint/premium |

| Certified cocoa | 35–40% | Limited qualified suppliers |

What is included in the product

Concise Porter's Five Forces review of Lotus Bakeries, evaluating competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlighting disruptive trends and strategic implications for pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Lotus Bakeries—perfect for quick decision-making and identifying where competitive pressure hurts margins. Swap in your own data or scenario tabs to model impacts (new entrants, supplier shifts, or regulation) without macros—ready for pitch decks or boardroom slides.

Customers Bargaining Power

Retailer concentration vs brand pull

Large grocers and discounters negotiate hard on price, promotions and shelf fees, leveraging concentrated buying power in key European markets where top chains often control c.60% of grocery sales. Lotus Biscoff’s distinctive taste and low substitutability, sold in 50+ countries and widely used on airlines, preserves niche loyalty. Strong brand equity secures premium placement and mitigates concession pressure. Overall buyer power is balanced by steady consumer demand.

Private label pressure

Retailers push own‑label speculoos and cookies to widen margins and anchor price points, forcing promotional activity; private label penetration in many European categories reached roughly 30–40% by 2023. Lotus Bakeries, with group turnover of EUR 1,174.9m in 2023, defends margin via taste, consistency and marketing investment, so private label raises buyer leverage but does not erase Lotus’ brand premium.

D2C and e-commerce

Lotus Bakeries’ company webshops and presence on marketplaces reduce dependence on traditional retailers by enabling direct sales and richer first-party data for targeting and merchandising, improving gross margin capture versus wholesale channels. Direct channels give control over assortment and pricing, but the bulk of volume and shelf prominence is still controlled by large brick-and-mortar chains. E-commerce growth moderates buyer power but does not fully neutralize the negotiating leverage of major retailers.

Global customer diversification

Global customer diversification reduces reliance on any single buyer, as Lotus Bakeries expanded channel and regional reach by 2024. New market entries shifted the mix toward growth partners, weakening individual buyer leverage. Localized assortments sustain shelf relevance across markets.

- Regional reach reduces single-buyer exposure

- New markets increase growth-partner share

- Diversification lowers buyer bargaining power

- Localized SKUs protect shelf presence

Premium positioning, elasticity

Premium indulgence and distinct flavor lower price sensitivity versus mainstream cookies, sustaining margins; 2023 group turnover was €1.206bn. Euro-area inflation in 2024 (approx. 2.9%) can still test willingness-to-pay. Targeted pack sizes and tactical promotions manage elasticity, while buyer power increases in downturns but stays manageable for Lotus.

- Premium positioning: lower elasticity

- 2023 turnover: €1.206bn

- 2024 inflation (~2.9%) pressures WTP

- Packs/promos mitigate demand shifts

Grocer leverage, private labels 30-40% and turnover €1.206bn vs. 2.9% inflation

Large European grocers (top chains ~60% share) and private‑label penetration (30–40% in 2023) keep buyer leverage, pressuring price and promotions. Lotus’ strong Biscoff brand, €1.206bn turnover (2023) and growing direct e‑commerce reduce retailer dependence, but brick‑and‑mortar still drives volumes; 2024 euro‑area inflation ~2.9% tests willingness‑to‑pay.

| Metric | Value |

|---|---|

| 2023 turnover | €1.206bn |

| Top chains market share | ~60% |

| Private label (2023) | 30–40% |

| Euro‑area inflation (2024) | ~2.9% |

Preview Before You Purchase

Lotus Bakeries Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Lotus Bakeries you’ll receive immediately after purchase—no placeholders. The document is fully formatted, actionable and download‑ready. It provides tailored assessments of supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lotus Bakeries faces moderate supplier power but strong buyer expectations, intense rivalry among branded bakery players, moderate threat of new entrants due to brand and scale, and growing substitute pressure from healthier snacks. The analysis highlights how brand equity and innovation buffer risks yet expose margin pressures. This brief overview teases force-by-force implications. Unlock the full Porter's Five Forces Analysis to explore Lotus Bakeries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Broad commodity input base

Lotus sources wheat, sugar, oils and spices from a fragmented global market with hundreds of suppliers, limiting individual leverage; in 2024 Lotus reported group net sales of €1.49bn, supporting scale purchasing. Multiple qualified suppliers and dual-sourcing enable competitive bidding and lower costs. Standardized specs and global commodity contracts reduce switching costs, keeping baseline supplier power moderate.

Quality and specialty specs

Signature taste depends on specific spice blends and consistent flour profiles, narrowing acceptable supplier pools and raising qualification barriers; Biscoff is sold in over 50 markets, so any taste drift risks broad brand equity. Qualification and audit requirements increase switching friction, giving select suppliers marginal leverage. Rigorous QA systems and periodic sensory testing partially offset supplier power.

Sustainability certifications

Sustainability certifications narrow supplier options: by 2024 RSPO-certified palm oil made up about 20% of global supply and certified cocoa programs covered roughly 35–40% of trade, while demand for traceable packaging rose double digits, tightening availability. Compliance premiums can lift input costs when certified supply is tight, yet Lotus uses long-term contracts and supplier development to dampen volatility and accept some pricing power from certified suppliers as ESG is strategic.

Packaging and logistics dependencies

Specialized packaging lines for Lotus Bakeries require specific film and carton specs, concentrating spend with a limited set of suppliers and raising switching costs; freight and port bottlenecks plus cold-chain needs for some SKUs can constrain inbound/outbound flows. Diversified 3PL partners and regional hubs reduce single-point risk, though in tight markets logistics providers can gain temporary bargaining leverage, driving spot-cost volatility.

- Concentrated supplier base increases switching costs

- Freight, cold-chain and port limits constrain flows

- 3PL diversification and regional hubs mitigate disruption

- Logistics providers can gain short-term pricing power in tight markets

Commodity and energy volatility

Agricultural cycles and energy-price swings drive input-cost volatility for Lotus Bakeries, creating episodic upward pressure on sugar, wheat and oil-based ingredients; hedging and forward contracts reduce but do not eliminate spikes. Large procurement volumes and multi-regional sourcing give Lotus scale and negotiation leverage, keeping supplier power generally contained despite occasional episodic pressure.

- Volatility: episodic supplier leverage

- Risk mitigation: hedging/forwards limit spikes

- Scale advantage: stronger negotiation

- Net: contained but not eliminated exposure

Moderate supplier power: €1.49bn scale vs certified palm ~20%, cocoa 35–40%

Lotus faces moderate supplier power: fragmented ingredient markets and €1.49bn 2024 sales provide scale, but specialty spices, certified inputs and packaging specs increase leverage. RSPO palm ~20% and certified cocoa ~35–40% narrow pools and can raise costs. Hedging, long-term contracts and multi-sourcing limit but do not eliminate episodic supplier pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Group net sales | €1.49bn | Purchasing scale |

| RSPO palm | ~20% | Supply constraint/premium |

| Certified cocoa | 35–40% | Limited qualified suppliers |

What is included in the product

Concise Porter's Five Forces review of Lotus Bakeries, evaluating competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlighting disruptive trends and strategic implications for pricing and market share.

A clear, one-sheet Porter's Five Forces summary for Lotus Bakeries—perfect for quick decision-making and identifying where competitive pressure hurts margins. Swap in your own data or scenario tabs to model impacts (new entrants, supplier shifts, or regulation) without macros—ready for pitch decks or boardroom slides.

Customers Bargaining Power

Retailer concentration vs brand pull

Large grocers and discounters negotiate hard on price, promotions and shelf fees, leveraging concentrated buying power in key European markets where top chains often control c.60% of grocery sales. Lotus Biscoff’s distinctive taste and low substitutability, sold in 50+ countries and widely used on airlines, preserves niche loyalty. Strong brand equity secures premium placement and mitigates concession pressure. Overall buyer power is balanced by steady consumer demand.

Private label pressure

Retailers push own‑label speculoos and cookies to widen margins and anchor price points, forcing promotional activity; private label penetration in many European categories reached roughly 30–40% by 2023. Lotus Bakeries, with group turnover of EUR 1,174.9m in 2023, defends margin via taste, consistency and marketing investment, so private label raises buyer leverage but does not erase Lotus’ brand premium.

D2C and e-commerce

Lotus Bakeries’ company webshops and presence on marketplaces reduce dependence on traditional retailers by enabling direct sales and richer first-party data for targeting and merchandising, improving gross margin capture versus wholesale channels. Direct channels give control over assortment and pricing, but the bulk of volume and shelf prominence is still controlled by large brick-and-mortar chains. E-commerce growth moderates buyer power but does not fully neutralize the negotiating leverage of major retailers.

Global customer diversification

Global customer diversification reduces reliance on any single buyer, as Lotus Bakeries expanded channel and regional reach by 2024. New market entries shifted the mix toward growth partners, weakening individual buyer leverage. Localized assortments sustain shelf relevance across markets.

- Regional reach reduces single-buyer exposure

- New markets increase growth-partner share

- Diversification lowers buyer bargaining power

- Localized SKUs protect shelf presence

Premium positioning, elasticity

Premium indulgence and distinct flavor lower price sensitivity versus mainstream cookies, sustaining margins; 2023 group turnover was €1.206bn. Euro-area inflation in 2024 (approx. 2.9%) can still test willingness-to-pay. Targeted pack sizes and tactical promotions manage elasticity, while buyer power increases in downturns but stays manageable for Lotus.

- Premium positioning: lower elasticity

- 2023 turnover: €1.206bn

- 2024 inflation (~2.9%) pressures WTP

- Packs/promos mitigate demand shifts

Grocer leverage, private labels 30-40% and turnover €1.206bn vs. 2.9% inflation

Large European grocers (top chains ~60% share) and private‑label penetration (30–40% in 2023) keep buyer leverage, pressuring price and promotions. Lotus’ strong Biscoff brand, €1.206bn turnover (2023) and growing direct e‑commerce reduce retailer dependence, but brick‑and‑mortar still drives volumes; 2024 euro‑area inflation ~2.9% tests willingness‑to‑pay.

| Metric | Value |

|---|---|

| 2023 turnover | €1.206bn |

| Top chains market share | ~60% |

| Private label (2023) | 30–40% |

| Euro‑area inflation (2024) | ~2.9% |

Preview Before You Purchase

Lotus Bakeries Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Lotus Bakeries you’ll receive immediately after purchase—no placeholders. The document is fully formatted, actionable and download‑ready. It provides tailored assessments of supplier power, buyer power, competitive rivalry, threat of new entrants and substitutes.