Lowe's Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

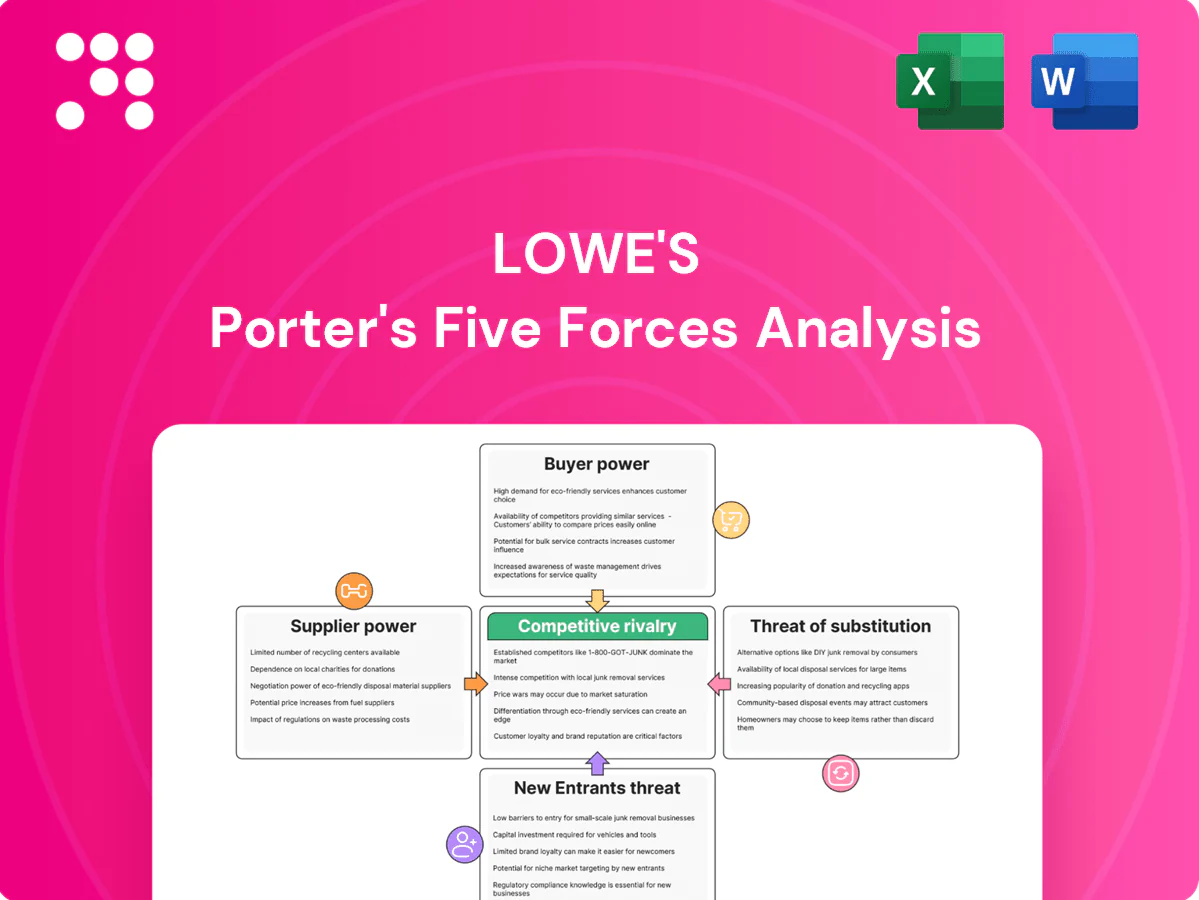

Lowe's faces intense rivalry from Home Depot and e-commerce, moderate supplier power, strong buyer bargaining, low threat of substitutes for big-ticket items but rising for convenience, and moderate barriers to entry due to scale and logistics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lowe's’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base limits power

Lowe's sources from thousands of vendors across categories from lumber to lighting, supplying its network of over 2,100 stores, which fragments supplier power and limits any single vendor’s leverage. The company routinely dual-sources key SKUs and uses broad benchmarking to drive down costs. This supplier breadth strengthens Lowe's negotiating position on price, lead times and service terms.

Branded vendors retain some influence

Premium brands in appliances, tools and paint carry consumer pull, enabling suppliers to negotiate placement, co-op marketing and MAP policies; in 2024 Lowe's reported over $100 billion in revenue, underscoring the scale that attracts brand leverage. Lowe's counters with private labels like Kobalt and Allen+Roth to dilute supplier power. Brand exclusives can lock in traffic but raise dependence and margin risk.

Scale and private label strengthen leverage

Lowe's national footprint—about 1,970 stores and roughly $97.2 billion in FY2024 sales—gives it significant purchasing clout over suppliers. Expanding private labels such as Kobalt, Blue Hawk and Everbilt provide alternative sourcing and margin upside, increasing private-brand penetration. The ability to shift mix and favor competing vendors for shelf and promotional slots pressures supplier pricing and forces suppliers to compete for scarce space.

Logistics integration and data sharing

Vendor-managed inventory, EDI links and joint demand forecasting tightly integrate suppliers into Lowe's supply chain, raising switching costs for smaller vendors; operational ties amplify dependency as Lowe's recorded FY2024 net sales of $96.3B. Lowe's enforces service levels and OTIF compliance via scorecards; non-performers face penalties or delisting to protect store availability and margins.

- VMI, EDI, forecasting: deeper integration

- Higher switching costs for small vendors

- OTIF/service-level mandates enforced

- Penalties/delisting for non-compliance

Commodity exposure and volatility

Lumber, copper, and chemicals drive input-cost volatility for Lowe's, with suppliers pushing for price pass-throughs during spikes and tight markets increasing bargaining power.

Lowe's uses hedging, forward buys, and assortment shifts to dilute exposure, while contract structures and index-based pricing help mediate disputes and enable faster cost recovery.

- commodity concentration: lumber/copper/chemicals

- supplier tactics: pass-throughs during spikes

- mitigants: hedging, forward buys, assortment shifts

- contracts: index-based pricing reduces disputes

Scale and private labels curb supplier leverage amid commodity volatility

Lowe's sources from thousands of vendors across ~1,970 stores, limiting single-supplier leverage; FY2024 net sales $96.3B boost purchasing clout. Private labels (Kobalt, Allen+Roth, Blue Hawk) and dual-sourcing reduce supplier power, while premium appliance/brand exclusives retain supplier pull. VMI/EDI integration raises switching costs; commodities (lumber, copper) add price volatility.

| Metric | Value |

|---|---|

| Stores | ~1,970 |

| FY2024 sales | $96.3B |

| Private-labels | Kobalt, Allen+Roth, Blue Hawk |

| Key commodities | Lumber, copper, chemicals |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, substitute threats, and entry barriers specific to Lowe's, with strategic implications for pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot for Lowe's that pinpoints competitive intensity, supplier/buyer risks, and substitute threats to slash analysis time; editable pressure scores and an instant radar chart let you adapt to market shifts and drop visuals straight into decks.

Customers Bargaining Power

High price transparency

High price transparency lets DIY and Pro customers easily compare Lowe's with Home Depot, Menards and online marketplaces, increasing buyer leverage as switching costs are low. With Home Depot and Lowe's holding roughly half of U.S. home improvement sales in 2024, price matching and everyday low price strategies are essential. Promotions, rebates and timed discounts heavily influence purchase timing and margin management.

Project bundling vs item-by-item

Complex projects that require advice, delivery and installation increase customer stickiness as buyers bundle products and services, reducing price sensitivity and raising average order value; simpler commodity purchases have higher churn and greater bargaining power. Attachment of services — installation, design, haul-away — softens buyer leverage by creating switching costs. Lowe's and Home Depot together control roughly 50% of the US home improvement market in 2024.

Pro customers negotiate terms

Pro customers at Lowe's—who account for roughly 40% of sales—drive higher purchase frequency and larger tickets, contributing to Lowe's 2024 revenue of about $93.6 billion. They demand volume discounts, dedicated pro service and jobsite delivery, pressuring margins. Account management and loyalty tiers trade perks for share-of-wallet and repeat business. Local concentration of large contractors elevates bargaining leverage in regional markets.

Omnichannel expectations

Buyers now expect inventory visibility, BOPIS, curbside pickup and rapid delivery; failures to meet SLAs drive churn to rivals, with 70% of US shoppers using BOPIS in 2024 and convenience often outweighing small price differences. Seamless returns are a critical loyalty determinant and can flip purchase decisions within minutes if cumbersome.

- Inventory visibility: real-time

- BOPIS adoption: 70% (2024)

- Convenience > price

- Returns: loyalty driver

Reviews and social proof

Online ratings drive selection and pressure pricing for Lowe's: 87% of shoppers in 2024 said reviews influence product choice, so negative feedback can rapidly shift demand away from a SKU and erode margins. Private-label lines must meet quality thresholds to retain margins, while amplified customer voice increases buyers' indirect negotiating power.

- 87% 2024: reviews influence choice

- Negative reviews → rapid SKU demand shifts

- Private label needs quality to sustain margins

Price transparency and BOPIS raise buyer leverage over big-box home-improvement chains

High price transparency and low switching costs boost buyer leverage vs Home Depot, Menards and online rivals; Lowe's and Home Depot hold ~50% of US market (2024). Pro customers ~40% of sales; Lowe's 2024 revenue ~$93.6B. BOPIS adoption ~70% and reviews influence ~87% of purchases, raising service/fulfillment bargaining.

| Metric | 2024 |

|---|---|

| Market share (Lowe's+HD) | ~50% |

| Lowe's revenue | $93.6B |

| Pro sales share | ~40% |

| BOPIS use | 70% |

| Reviews influence | 87% |

Same Document Delivered

Lowe's Porter's Five Forces Analysis

This preview shows the exact Lowe's Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. It's professionally formatted and ready to download and use the moment you buy.

A Must-Have Tool for Decision-Makers

Lowe's faces intense rivalry from Home Depot and e-commerce, moderate supplier power, strong buyer bargaining, low threat of substitutes for big-ticket items but rising for convenience, and moderate barriers to entry due to scale and logistics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lowe's’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base limits power

Lowe's sources from thousands of vendors across categories from lumber to lighting, supplying its network of over 2,100 stores, which fragments supplier power and limits any single vendor’s leverage. The company routinely dual-sources key SKUs and uses broad benchmarking to drive down costs. This supplier breadth strengthens Lowe's negotiating position on price, lead times and service terms.

Branded vendors retain some influence

Premium brands in appliances, tools and paint carry consumer pull, enabling suppliers to negotiate placement, co-op marketing and MAP policies; in 2024 Lowe's reported over $100 billion in revenue, underscoring the scale that attracts brand leverage. Lowe's counters with private labels like Kobalt and Allen+Roth to dilute supplier power. Brand exclusives can lock in traffic but raise dependence and margin risk.

Scale and private label strengthen leverage

Lowe's national footprint—about 1,970 stores and roughly $97.2 billion in FY2024 sales—gives it significant purchasing clout over suppliers. Expanding private labels such as Kobalt, Blue Hawk and Everbilt provide alternative sourcing and margin upside, increasing private-brand penetration. The ability to shift mix and favor competing vendors for shelf and promotional slots pressures supplier pricing and forces suppliers to compete for scarce space.

Logistics integration and data sharing

Vendor-managed inventory, EDI links and joint demand forecasting tightly integrate suppliers into Lowe's supply chain, raising switching costs for smaller vendors; operational ties amplify dependency as Lowe's recorded FY2024 net sales of $96.3B. Lowe's enforces service levels and OTIF compliance via scorecards; non-performers face penalties or delisting to protect store availability and margins.

- VMI, EDI, forecasting: deeper integration

- Higher switching costs for small vendors

- OTIF/service-level mandates enforced

- Penalties/delisting for non-compliance

Commodity exposure and volatility

Lumber, copper, and chemicals drive input-cost volatility for Lowe's, with suppliers pushing for price pass-throughs during spikes and tight markets increasing bargaining power.

Lowe's uses hedging, forward buys, and assortment shifts to dilute exposure, while contract structures and index-based pricing help mediate disputes and enable faster cost recovery.

- commodity concentration: lumber/copper/chemicals

- supplier tactics: pass-throughs during spikes

- mitigants: hedging, forward buys, assortment shifts

- contracts: index-based pricing reduces disputes

Scale and private labels curb supplier leverage amid commodity volatility

Lowe's sources from thousands of vendors across ~1,970 stores, limiting single-supplier leverage; FY2024 net sales $96.3B boost purchasing clout. Private labels (Kobalt, Allen+Roth, Blue Hawk) and dual-sourcing reduce supplier power, while premium appliance/brand exclusives retain supplier pull. VMI/EDI integration raises switching costs; commodities (lumber, copper) add price volatility.

| Metric | Value |

|---|---|

| Stores | ~1,970 |

| FY2024 sales | $96.3B |

| Private-labels | Kobalt, Allen+Roth, Blue Hawk |

| Key commodities | Lumber, copper, chemicals |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, substitute threats, and entry barriers specific to Lowe's, with strategic implications for pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot for Lowe's that pinpoints competitive intensity, supplier/buyer risks, and substitute threats to slash analysis time; editable pressure scores and an instant radar chart let you adapt to market shifts and drop visuals straight into decks.

Customers Bargaining Power

High price transparency

High price transparency lets DIY and Pro customers easily compare Lowe's with Home Depot, Menards and online marketplaces, increasing buyer leverage as switching costs are low. With Home Depot and Lowe's holding roughly half of U.S. home improvement sales in 2024, price matching and everyday low price strategies are essential. Promotions, rebates and timed discounts heavily influence purchase timing and margin management.

Project bundling vs item-by-item

Complex projects that require advice, delivery and installation increase customer stickiness as buyers bundle products and services, reducing price sensitivity and raising average order value; simpler commodity purchases have higher churn and greater bargaining power. Attachment of services — installation, design, haul-away — softens buyer leverage by creating switching costs. Lowe's and Home Depot together control roughly 50% of the US home improvement market in 2024.

Pro customers negotiate terms

Pro customers at Lowe's—who account for roughly 40% of sales—drive higher purchase frequency and larger tickets, contributing to Lowe's 2024 revenue of about $93.6 billion. They demand volume discounts, dedicated pro service and jobsite delivery, pressuring margins. Account management and loyalty tiers trade perks for share-of-wallet and repeat business. Local concentration of large contractors elevates bargaining leverage in regional markets.

Omnichannel expectations

Buyers now expect inventory visibility, BOPIS, curbside pickup and rapid delivery; failures to meet SLAs drive churn to rivals, with 70% of US shoppers using BOPIS in 2024 and convenience often outweighing small price differences. Seamless returns are a critical loyalty determinant and can flip purchase decisions within minutes if cumbersome.

- Inventory visibility: real-time

- BOPIS adoption: 70% (2024)

- Convenience > price

- Returns: loyalty driver

Reviews and social proof

Online ratings drive selection and pressure pricing for Lowe's: 87% of shoppers in 2024 said reviews influence product choice, so negative feedback can rapidly shift demand away from a SKU and erode margins. Private-label lines must meet quality thresholds to retain margins, while amplified customer voice increases buyers' indirect negotiating power.

- 87% 2024: reviews influence choice

- Negative reviews → rapid SKU demand shifts

- Private label needs quality to sustain margins

Price transparency and BOPIS raise buyer leverage over big-box home-improvement chains

High price transparency and low switching costs boost buyer leverage vs Home Depot, Menards and online rivals; Lowe's and Home Depot hold ~50% of US market (2024). Pro customers ~40% of sales; Lowe's 2024 revenue ~$93.6B. BOPIS adoption ~70% and reviews influence ~87% of purchases, raising service/fulfillment bargaining.

| Metric | 2024 |

|---|---|

| Market share (Lowe's+HD) | ~50% |

| Lowe's revenue | $93.6B |

| Pro sales share | ~40% |

| BOPIS use | 70% |

| Reviews influence | 87% |

Same Document Delivered

Lowe's Porter's Five Forces Analysis

This preview shows the exact Lowe's Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. It's professionally formatted and ready to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Lowe's faces intense rivalry from Home Depot and e-commerce, moderate supplier power, strong buyer bargaining, low threat of substitutes for big-ticket items but rising for convenience, and moderate barriers to entry due to scale and logistics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lowe's’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base limits power

Lowe's sources from thousands of vendors across categories from lumber to lighting, supplying its network of over 2,100 stores, which fragments supplier power and limits any single vendor’s leverage. The company routinely dual-sources key SKUs and uses broad benchmarking to drive down costs. This supplier breadth strengthens Lowe's negotiating position on price, lead times and service terms.

Branded vendors retain some influence

Premium brands in appliances, tools and paint carry consumer pull, enabling suppliers to negotiate placement, co-op marketing and MAP policies; in 2024 Lowe's reported over $100 billion in revenue, underscoring the scale that attracts brand leverage. Lowe's counters with private labels like Kobalt and Allen+Roth to dilute supplier power. Brand exclusives can lock in traffic but raise dependence and margin risk.

Scale and private label strengthen leverage

Lowe's national footprint—about 1,970 stores and roughly $97.2 billion in FY2024 sales—gives it significant purchasing clout over suppliers. Expanding private labels such as Kobalt, Blue Hawk and Everbilt provide alternative sourcing and margin upside, increasing private-brand penetration. The ability to shift mix and favor competing vendors for shelf and promotional slots pressures supplier pricing and forces suppliers to compete for scarce space.

Logistics integration and data sharing

Vendor-managed inventory, EDI links and joint demand forecasting tightly integrate suppliers into Lowe's supply chain, raising switching costs for smaller vendors; operational ties amplify dependency as Lowe's recorded FY2024 net sales of $96.3B. Lowe's enforces service levels and OTIF compliance via scorecards; non-performers face penalties or delisting to protect store availability and margins.

- VMI, EDI, forecasting: deeper integration

- Higher switching costs for small vendors

- OTIF/service-level mandates enforced

- Penalties/delisting for non-compliance

Commodity exposure and volatility

Lumber, copper, and chemicals drive input-cost volatility for Lowe's, with suppliers pushing for price pass-throughs during spikes and tight markets increasing bargaining power.

Lowe's uses hedging, forward buys, and assortment shifts to dilute exposure, while contract structures and index-based pricing help mediate disputes and enable faster cost recovery.

- commodity concentration: lumber/copper/chemicals

- supplier tactics: pass-throughs during spikes

- mitigants: hedging, forward buys, assortment shifts

- contracts: index-based pricing reduces disputes

Scale and private labels curb supplier leverage amid commodity volatility

Lowe's sources from thousands of vendors across ~1,970 stores, limiting single-supplier leverage; FY2024 net sales $96.3B boost purchasing clout. Private labels (Kobalt, Allen+Roth, Blue Hawk) and dual-sourcing reduce supplier power, while premium appliance/brand exclusives retain supplier pull. VMI/EDI integration raises switching costs; commodities (lumber, copper) add price volatility.

| Metric | Value |

|---|---|

| Stores | ~1,970 |

| FY2024 sales | $96.3B |

| Private-labels | Kobalt, Allen+Roth, Blue Hawk |

| Key commodities | Lumber, copper, chemicals |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, substitute threats, and entry barriers specific to Lowe's, with strategic implications for pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot for Lowe's that pinpoints competitive intensity, supplier/buyer risks, and substitute threats to slash analysis time; editable pressure scores and an instant radar chart let you adapt to market shifts and drop visuals straight into decks.

Customers Bargaining Power

High price transparency

High price transparency lets DIY and Pro customers easily compare Lowe's with Home Depot, Menards and online marketplaces, increasing buyer leverage as switching costs are low. With Home Depot and Lowe's holding roughly half of U.S. home improvement sales in 2024, price matching and everyday low price strategies are essential. Promotions, rebates and timed discounts heavily influence purchase timing and margin management.

Project bundling vs item-by-item

Complex projects that require advice, delivery and installation increase customer stickiness as buyers bundle products and services, reducing price sensitivity and raising average order value; simpler commodity purchases have higher churn and greater bargaining power. Attachment of services — installation, design, haul-away — softens buyer leverage by creating switching costs. Lowe's and Home Depot together control roughly 50% of the US home improvement market in 2024.

Pro customers negotiate terms

Pro customers at Lowe's—who account for roughly 40% of sales—drive higher purchase frequency and larger tickets, contributing to Lowe's 2024 revenue of about $93.6 billion. They demand volume discounts, dedicated pro service and jobsite delivery, pressuring margins. Account management and loyalty tiers trade perks for share-of-wallet and repeat business. Local concentration of large contractors elevates bargaining leverage in regional markets.

Omnichannel expectations

Buyers now expect inventory visibility, BOPIS, curbside pickup and rapid delivery; failures to meet SLAs drive churn to rivals, with 70% of US shoppers using BOPIS in 2024 and convenience often outweighing small price differences. Seamless returns are a critical loyalty determinant and can flip purchase decisions within minutes if cumbersome.

- Inventory visibility: real-time

- BOPIS adoption: 70% (2024)

- Convenience > price

- Returns: loyalty driver

Reviews and social proof

Online ratings drive selection and pressure pricing for Lowe's: 87% of shoppers in 2024 said reviews influence product choice, so negative feedback can rapidly shift demand away from a SKU and erode margins. Private-label lines must meet quality thresholds to retain margins, while amplified customer voice increases buyers' indirect negotiating power.

- 87% 2024: reviews influence choice

- Negative reviews → rapid SKU demand shifts

- Private label needs quality to sustain margins

Price transparency and BOPIS raise buyer leverage over big-box home-improvement chains

High price transparency and low switching costs boost buyer leverage vs Home Depot, Menards and online rivals; Lowe's and Home Depot hold ~50% of US market (2024). Pro customers ~40% of sales; Lowe's 2024 revenue ~$93.6B. BOPIS adoption ~70% and reviews influence ~87% of purchases, raising service/fulfillment bargaining.

| Metric | 2024 |

|---|---|

| Market share (Lowe's+HD) | ~50% |

| Lowe's revenue | $93.6B |

| Pro sales share | ~40% |

| BOPIS use | 70% |

| Reviews influence | 87% |

Same Document Delivered

Lowe's Porter's Five Forces Analysis

This preview shows the exact Lowe's Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document provides a complete evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. It's professionally formatted and ready to download and use the moment you buy.